For global property investors, the term rental yield London is a critical benchmark. However, relying solely on the city-wide average can be a costly oversight. While the average gross yield across the capital currently sits between 4.5% and 5.5%, this single figure conceals the market's true dynamics.

The genuine investment potential lies in the detail: the vast disparity between boroughs and, most importantly, London's powerful, market-beating rental growth. This guide provides a practical, data-driven analysis for investors seeking long-term returns.

A Snapshot of London Rental Yields

At first glance, London's headline yields may seem less compelling than those in other major UK cities. This is where a superficial analysis can mislead investors. The investment case for London is not built on initial yield alone, but on two fundamental pillars: relentless tenant demand and a chronic undersupply of housing.

This imbalance creates an environment of exceptional rental growth that few other global cities can match.

Consider this comparison: an investor might achieve a 7% gross yield in a regional city. If rental growth in that market is stagnant, the return remains flat. In contrast, a London property starting with a 5.5% gross yield could experience consistent rental income growth year-on-year, significantly enhancing the total return over the long term.

London Rental Yields at a Glance

This table offers a concise comparison of London’s rental market against the UK average, highlighting the core dynamics for investors.

| Metric | London Average | UK Average | Key Driver |

|---|---|---|---|

| Gross Yield | 4.5% – 5.5% | 5.5% – 6.5% | High property values temper London's gross yield percentage. |

| Rental Growth (Annual) | ~11.5% | ~6.0% | Extreme demand and supply shortages fuel rapid rent inflation. |

| Capital Growth | Strong (Long-term) | Moderate (Varies by city) | Global city status, economic resilience, and housing undersupply. |

| Tenant Demand | Exceptionally High | High | Driven by jobs, education, migration, and lifestyle appeal. |

While the initial yield may appear lower, London's powerful rental and capital growth often deliver a superior total return over time, making it a cornerstone for long-term wealth-building strategies.

Rental Growth: The London Advantage

Recent data from the Office for National Statistics (ONS) substantiates this point. London's private rental market has experienced significant inflation, positioning it as a prime target for investors focused on income growth.

In the 12 months to December 2024, London recorded the highest private rent inflation in England at 11.5%. For context, a region like Yorkshire and The Humber saw growth of just 5.4% in the same period. You can review the latest ONS private rent report for detailed data.

This powerful rental appreciation is the key to a successful London investment. It means that despite higher purchase prices, your income has the potential to grow at a pace that can deliver far better long-term returns than markets with higher initial yields but stagnant rents.

For the global investor, London's appeal is not just its status as a world city, but its proven ability to generate consistent, market-beating rental growth. This factor often outweighs the appeal of a higher, but less dynamic, headline yield found elsewhere.

Prime Central vs. Outer Boroughs: An Essential Distinction

To truly understand the rental yield London offers, one must differentiate between its two distinct markets: the established, high-value core and the emerging, more accessible outer zones.

Prime Central London (PCL): In areas like Kensington and Mayfair, high property values depress gross rental yields, which typically range between 2.5% and 4.0%. Investment here is primarily a strategy for long-term wealth preservation and capital appreciation, rather than monthly income.

Outer London Boroughs: In contrast, areas like East Ham, Barking, and Woolwich offer more accessible entry prices. This results in healthier gross yields, frequently reaching 5.5% to 6.5% or more. These are the prime locations for investors who prioritise strong, consistent cash flow and robust rental growth.

Recognising this divide is the first step toward building a sound London investment strategy. For investors focused on maximising rental income, the most compelling opportunities are found not in the prestigious heart of the city, but in its well-connected and rapidly developing outer boroughs. You can explore this further by reading our guide on the average price of a flat in London.

Calculating Your True Return: Gross Versus Net Yield

Before analysing specific postcodes, it is vital to understand how to measure the true return on an investment. Many investors fixate on the gross rental yield, a simple calculation showing annual rent as a percentage of the property’s purchase price. This figure represents a property’s total potential income before costs.

However, for serious investors, the only figure that truly matters is the net rental yield. This metric reflects your actual profit after all operational expenses have been deducted. It is the real return, offering an honest assessment of a property's financial performance. The gap between gross and net yield in London can be substantial; relying only on the headline figure can lead to inaccurate projections.

The Costs That Shape Your Net Yield

The difference between an advertised gross yield and your real return is determined by operating costs. These are the unavoidable expenses of owning and letting a property in London. Accurately forecasting them is fundamental to any sound investment analysis.

Key operational costs for a London buy-to-let property include:

- Service Charges: A significant expense for leasehold properties (which covers most flats in London). This fee covers the maintenance of communal areas, buildings insurance, and often includes a contribution to a ‘sinking fund’ for major future works. Government data suggests this can average over £2,300 per year.

- Letting Agent Fees: A full-service agent will typically charge between 15% and 20% of the monthly rent, plus VAT. This fee covers tenant sourcing, rent collection, and day-to-day management.

- Maintenance and Repairs: A prudent approach is to budget around 0.5% of the property’s value annually. This fund should cover routine jobs as well as unexpected costs, such as a boiler replacement or a leak.

- Void Periods: No property is occupied 100% of the time. Budgeting for three to four weeks of vacancy per year (approximately 8% of annual rent) is a realistic provision for the time between tenancies.

- Landlord Insurance: This is separate from the buildings insurance covered by the service charge. It protects your contents, covers liability, and can provide rent-loss protection, typically costing £200 to £400 annually.

A Worked Example: Gross vs. Net Yield

Let’s apply these principles to a one-bedroom flat in an Outer London borough.

Purchase Price: £400,000

Monthly Rent: £1,800

Annual Rent: £21,600 (£1,800 x 12)

Gross Yield Calculation:

(Annual Rent / Purchase Price) x 100

(£21,600 / £400,000) x 100 = 5.4% Gross Yield

Now, let’s calculate the net yield by subtracting typical annual costs:

- Service Charge: £2,300

- Letting Agent Fees (15% + VAT): £3,888

- Maintenance Fund (0.5%): £2,000

- Void Period (3 weeks rent): £1,246

- Landlord Insurance: £300

Total Annual Costs: £9,734

Net Annual Income: £21,600 (Annual Rent) – £9,734 (Total Costs) = £11,866

Net Yield Calculation:

(Net Annual Income / Purchase Price) x 100

(£11,866 / £400,000) x 100 = 2.97% Net Yield

As this example demonstrates, the real return is significantly lower than the headline figure. This foundational knowledge empowers investors to look past marketing claims and accurately assess the true potential of any London property. To assist with your own calculations, use our simple rental yield calculator to model different scenarios.

Where to Find the Best Rental Yields in London

For investors seeking strong rental income, the strategy is clear: look beyond the glamour of Prime Central London. While postcodes in Kensington or Mayfair offer prestige, their high property prices compress gross yields to a modest 2.5% to 4.0%. The most compelling opportunities for robust, regular income lie in the city’s dynamic outer boroughs.

These well-connected, regenerating areas consistently deliver superior cash flow. The formula is simple: target postcodes where relatively affordable property prices meet strong, consistent tenant demand. This data-led approach is how you pinpoint where your capital will work hardest.

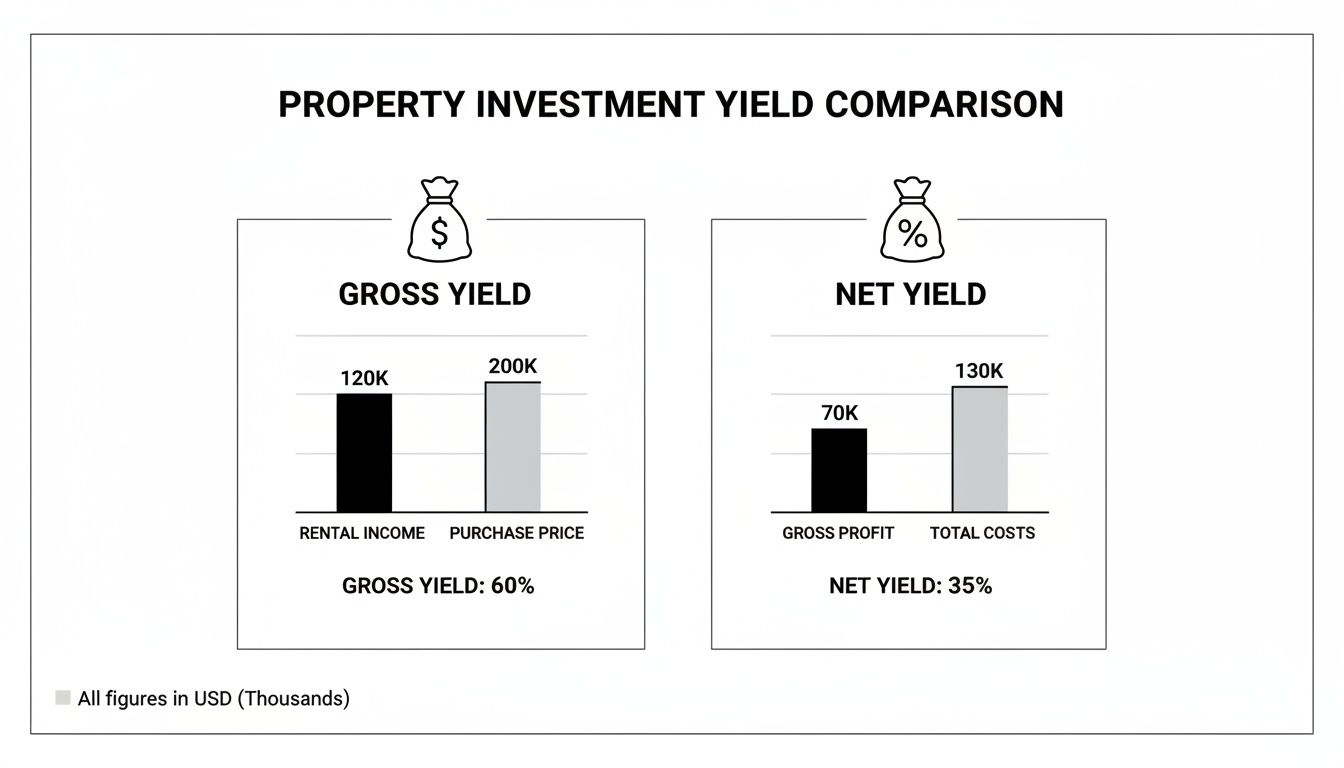

It is also crucial to look past the headline 'gross yield' and focus on the 'net yield'—the return that actually lands in your bank account. This visual makes that distinction clear.

As you can see, your true profit is only revealed after accounting for all operational costs. It is a vital calculation for properly assessing any London investment.

The Anatomy of a High-Yield Area

What transforms these outer boroughs into such compelling prospects for yield-focused investors? It is not a single factor but a combination of forces creating the ideal environment for landlords.

- Regeneration and Investment: Areas like Stratford and Tottenham have been revitalised by billions in public and private funding, creating new homes, amenities, and public spaces. This wave of investment attracts new tenants and supports long-term rental growth.

- Transport Connectivity: The Elizabeth Line has been a game-changer for postcodes like Abbey Wood and Woolwich. By slashing commute times to central London and Heathrow, it has made these areas vastly more desirable for renters.

- Relative Affordability: This is the primary driver. With average property prices in many of these areas still below £400,000, investors can acquire assets for a fraction of the cost of central locations while still commanding strong rents.

For the yield-focused investor, a property in East Ham or Woolwich presents a clear advantage. The lower capital outlay means the rent generated represents a much larger proportion of the initial investment, directly boosting the gross yield.

Top 5 London Postcodes for Rental Yield

To provide a clearer picture, we have analysed the latest data to identify the postcodes currently leading the pack for rental yields. These are thriving communities benefiting from investment, transport links, and growing appeal among London's renters.

This table provides a data-led comparison of London's highest-yielding postcodes, offering actionable insights for investors.

| Postcode/Area | Average Gross Yield (%) | Average Property Price (£) | Average Monthly Rent (£) |

|---|---|---|---|

| E6 (East Ham) | 6.0% | £411,000 | £2,055 |

| SE28 (Thamesmead) | 5.9% | £315,000 | £1,550 |

| E15 (Stratford) | 5.8% | £450,000 | £2,175 |

| SE2 (Abbey Wood) | 5.8% | £380,000 | £1,850 |

| N17 (Tottenham) | 5.8% | £430,000 | £2,080 |

The pattern is clear: London's highest rental yields are found where affordability and major infrastructure investment intersect. Recent analysis confirms this, with East Ham (E6) standing out with an average gross yield of 6.0%, driven by average monthly rents of £2,055 and impressive five-year price growth of 22%.

Close behind, areas like Thamesmead (SE28), Stratford (E15), Abbey Wood (SE2), and Tottenham (N17) all deliver strong yields around 5.8%. These are not speculative bets but calculated investments based on the fundamental drivers of the city's growth.

By focusing your search on these postcodes, you align your strategy with London's future, positioning your portfolio for strong and sustainable rental income. For more ideas on where to invest, check out our guide on the best buy-to-let locations to consider.

Understanding the Forces Driving the London Rental Market

What makes the London rental market so resilient and dynamic? While headline yields are a useful starting point, a true understanding of the rental yield London offers requires a deeper look at the powerful economic and social currents that shape it. These long-term fundamentals provide market stability and fuel impressive rental growth.

The market is defined by a simple but powerful principle: a severe, chronic imbalance between the supply of homes and the demand from tenants. For decades, the number of new properties built in the capital has fallen far short of what is needed for its growing population, creating a fiercely competitive rental landscape.

This is not a recent phenomenon. Government data and market analysis consistently show that for every single rental property that becomes available, there are dozens of prospective tenants competing for it. This relentless pressure on limited housing stock is the primary engine behind London's robust rental performance.

The Unshakeable Pillars of Tenant Demand

This relentless demand for rental properties is driven by several key factors that converge to attract a diverse and continuous stream of tenants from across the globe.

- A Global Economic Powerhouse: London is a world-leading centre for finance, technology, law, and the creative industries. This creates a vast jobs market that constantly attracts highly skilled professionals, who almost always choose to rent, at least upon arrival.

- Population Growth: The city’s population continues to expand, fuelled by migration from other parts of the UK and from overseas. According to ONS data, this steady growth ensures a constant flow of new households seeking accommodation.

- World-Class Education: Home to some of the world's top universities, London attracts tens of thousands of international students annually. This creates a substantial and reliable pool of tenants, particularly for smaller flats and Houses in Multiple Occupation (HMOs).

This constant demographic and economic pull means tenant demand in London is not just high—it is structurally embedded in the city's DNA. To grasp the dynamics that will affect your investments, understanding this wider landscape is key, as detailed in A Letting Agent's Guide to the Rental Market London 2026.

Rent Inflation: The Investor's Secret Weapon

The direct result of this supply-demand imbalance is powerful rent inflation, and this is where London truly sets itself apart. While its headline gross yields may trail some regional UK cities, the rate at which rents increase often delivers a far superior total return over the long term.

For example, while the UK-wide gross yield average may be higher, London's rent inflation is significantly stronger. ONS data shows London's rents surged by 11.5% year-over-year to December 2024, far outpacing the 5.4% seen in other regions, as rental supply sits well below its historic peak. Discover more insights about these rental yield trends on Global Property Guide.

For a long-term investor, a 5.5% yield with 10% annual rent growth is far more valuable than a 7% yield with flat rents. This growth compounds over time, significantly boosting your cash flow and the underlying value of your asset.

Understanding this dynamic is crucial. A London property investment should not be viewed as a static income source, but as a growing asset class. By investing in London, you are tapping into a market defined by scarcity and sustained demand—a proven formula for long-term rental income growth. This core strength provides a buffer against economic headwinds and makes the city a cornerstone for any serious global property portfolio.

Navigating UK Taxes and Regulations as a Global Investor

Investing in London property from overseas can be highly rewarding, but the difference between a successful investment and a stressful one often lies in understanding the UK’s tax regulations before you purchase.

While professional tax advice is essential, this guide outlines the key financial responsibilities you will face. This provides a foundation for ensuring your rental yield London calculations are grounded in reality.

As an overseas landlord, any profit generated from your London rental property is subject to UK Income Tax. The amount payable depends on where your profits fall within the UK's tax bands after deducting all allowable expenses. Some non-residents may be eligible for a tax-free Personal Allowance, but this depends on factors such as citizenship, so it is vital to verify.

The Non-resident Landlord Scheme

One of the first systems you will encounter is the Non-resident Landlord Scheme (NRLS). This is a mechanism used by the UK government to ensure tax is collected on rental income from landlords living abroad.

Under this scheme, your letting agent (or your tenant, if you self-manage) is legally required to deduct basic rate tax from your rent before it is paid to you. They then remit this money directly to HM Revenue & Customs (HMRC).

It is possible to mitigate this. You can apply to HMRC for approval to receive your rent in full. If granted, you then become responsible for declaring the income and paying the tax yourself through a Self Assessment tax return.

Key Taxes for Overseas Investors

Beyond income tax, several other significant taxes will directly impact your bottom line. Budgeting for these from the outset is non-negotiable for an accurate picture of your potential returns.

Stamp Duty Land Tax (SDLT): This is the tax paid upon purchasing a property in England. As an overseas buyer, you will pay the standard SDLT rates plus an additional 2% surcharge. If it is a second home, a further surcharge applies, making this a substantial upfront cost.

Capital Gains Tax (CGT): When you sell your London property, any profit made—the 'gain'—will likely be subject to UK Capital Gains Tax. This applies to all non-residents selling UK residential property, with the rate dependent on the size of the gain and your income level.

Inheritance Tax (IHT): This is a critical consideration often overlooked by overseas investors. UK-sited assets, including property, fall under UK Inheritance Tax rules regardless of your domicile. The current rate is 40% on the value of the asset above a certain threshold.

While these regulations may seem complex, they are a standard part of the process. The key is to build these costs into your financial models from the very beginning. This ensures your net yield calculations are realistic and your investment remains profitable after all liabilities are met.

Grasping these financial responsibilities is a cornerstone of sound property investing. If you are new to this journey, it is always wise to begin with the basics. Our guide on beginner property investment strategies is an excellent place to build that solid foundation.

Putting It All Together: A Practical London Investment Strategy

Understanding the data is one thing; turning it into a profitable investment is another. Let's move beyond theory and build a clear, actionable roadmap for navigating London’s complex but rewarding property market.

The core principle is refreshingly straightforward: chase cash flow in high-yielding outer boroughs, buy near transport hubs and regeneration zones, and never rely solely on a gross yield figure. This disciplined approach separates hopeful speculators from savvy investors who make decisions based on real returns.

For a deeper look into the core principles of buy-to-let, our guide on tips for property investment provides more valuable insights.

Your Core Investment Thesis Summarised

A winning London strategy is not about chasing the highest possible headline yield. It is about securing a sustainable return from a resilient asset that balances rental income, growth potential, and risk.

Your entire approach can be built on these three pillars:

- Target the Outer Boroughs: As established, the strongest rental yields are consistently found in areas like Barking, Woolwich, and Tottenham. These locations offer the ideal formula for cash flow: affordable purchase prices combined with powerful, unwavering rental demand.

- Follow the Infrastructure: Prioritise properties within walking distance of key transport links. The Elizabeth Line, Overground, and DLR are tenant magnets, dramatically reducing void periods and supporting rental growth for years to come.

- Calculate Net Yield Relentlessly: You must run the numbers. A tempting 6% gross yield can easily reduce to 3% or less once service charges, agent fees, and maintenance are deducted. Your final decision must be based on this net figure—it is the only number that truly matters.

A Final Worked Example: Investing in East Ham (E6)

Let's apply these principles to a real-world example in a high-yield hotspot like East Ham. This is how you move from an attractive headline figure to a realistic annual return.

Property: A two-bedroom flat in East Ham (E6)

Purchase Price: £411,000

Monthly Rent: £2,055 (Annual Rent: £24,660)

Gross Yield: (£24,660 / £411,000) x 100 = 6.0%

Now for the crucial part—the net calculation. This is where the profit is truly found.

Annual Operating Costs:

- Service Charge & Ground Rent: £2,500

- Letting Agent Fees (15% + VAT): £4,439

- Maintenance Fund (0.5% of value): £2,055

- Void Period (3 weeks): £1,422

- Landlord Insurance: £300

- Total Annual Costs: £10,716

Net Annual Income: £24,660 – £10,716 = £13,944

Final Net Yield: (£13,944 / £411,000) x 100 = 3.39%

This final figure of 3.39% is your realistic, actionable number. Of course, a vital part of protecting your income is keeping the property occupied. Learning how to effectively market your rental properties is a key skill for attracting high-quality tenants and minimising vacancies.

While London’s yields may appear modest next to some global markets, its rare combination of powerful rental growth and proven resilience makes it a compelling proposition. For the discerning global investor, it offers a formidable engine for long-term wealth creation within a diversified portfolio.

Answering Your Key Investment Questions

When assessing a market as large and complex as London, it is easy to become lost in the noise. To help you cut through it, we have addressed some of the most common questions from global investors seeking to understand the opportunities.

Is a 5% Rental Yield Good for London?

A gross yield of 5% is a solid benchmark for London and a realistic target for a well-chosen property. While you may see higher headline figures in other UK cities, a 5% return in the capital often comes with something more valuable: stronger long-term rental growth and greater potential for capital appreciation.

This resilience is driven by London’s powerful economy, constant international appeal, and a chronic housing shortage that maintains high tenant demand.

For a quick assessment, a 5.5% gross yield is considered genuinely ‘good’ by most local investors, as it provides a healthy buffer against London’s higher running costs. A yield of 6% or more is widely seen as an excellent return for this market.

Which Property Types Offer the Best Yields?

In London, smaller properties consistently deliver the best rental yields. One and two-bedroom flats are the workhorses of the city’s buy-to-let market for good reason. Their purchase prices are more accessible, yet they command strong rents from a huge pool of young professionals, couples, and international students.

- One and Two-Bedroom Flats: These properties offer the optimal balance between purchase price and rental income. They align perfectly with tenant demand and are generally the easiest to let and manage.

- Larger Family Homes: While the total monthly rent is higher, the much larger initial investment pushes the gross yield down. These properties are typically better suited for long-term capital growth rather than immediate monthly cash flow.

Can I Get a UK Mortgage as an International Investor?

Yes, it is entirely possible for international investors to secure a UK mortgage, but the process is stricter than for UK residents. Lenders will require a clean credit history, a stable income, and a clear, verifiable source of funds for your deposit.

The most significant difference is the deposit requirement. While a UK resident might obtain a buy-to-let mortgage with a 25% deposit, non-resident investors should be prepared to provide a larger amount—often between 30% and 40% of the property’s value.

How Much Tax Do I Pay on Rental Income as a Non-resident?

As a non-resident landlord, your rental profits are subject to UK Income Tax. This is calculated after deducting all allowable expenses. Under the Non-resident Landlord Scheme (NRLS), your letting agent is legally required to withhold tax at the basic rate from your rent.

However, you can apply to HMRC for approval to receive the rent in full and handle your own tax affairs via an annual Self Assessment tax return.

You also need to factor in Stamp Duty Land Tax (which includes a 2% surcharge for overseas buyers) at the point of purchase, and potentially Capital Gains Tax when you eventually sell. It is always advisable to seek professional tax advice tailored to your personal circumstances before you invest.

At World Property Investor, we provide the in-depth analysis and data you need to make confident investment decisions across the globe. Visit World Property Investor to explore our full range of guides and market reports.