You've found the asset. The numbers look workable. The estate agent is pushing for a quick reservation. Then the unfamiliar terms start arriving: title extract, notarial deed, beneficial owner declaration, source-of-funds pack, tax residency questions, lender conditions. At that point, most overseas buyers still think the lawyer is there to “handle the paperwork”.

That's the wrong mental model.

An international real estate lawyer is there to stop you buying the wrong asset, through the wrong structure, on the wrong terms, in the wrong jurisdictional sequence. In cross-border property, legal mistakes don't just slow a deal down. They can trap capital, trigger avoidable tax exposure, block registration, spook lenders, and make resale harder than the purchase.

A key problem is that many investors assume property law travels well. It doesn't. A process that feels routine in England can work very differently in Spain, Dubai, Florida, or Israel. Even the financing journey can change sharply when a buyer is non-resident. If you're weighing mortgage options in that market, these insights for foreign property buyers in Israel are useful because they show how quickly lending, documentation, and borrower status can reshape the transaction.

Practical buyers start legal work before they negotiate hard on price. They want to know whether the structure is financeable, taxable, registrable, and exit-friendly. If you're still comparing jurisdictions at a high level, a broader guide to buying property overseas helps frame the questions, but the legal brief has to come first.

Buying Property Abroad? Your First Call Should Be a Lawyer

A foreign purchase usually feels simple at the marketing stage. The brochure is clear, the projected rental use sounds straightforward, and the local sales team behaves as if the process is standard. It rarely is.

The first legal question isn't “can I buy it?” It's “what exactly am I buying, and under what enforceable rights?” In some markets, that means checking title and encumbrances. In others, it means checking whether the development approvals, community rules, lease restrictions, corporate ownership, or registration path line up with your intended use.

The cost of calling too late

The most expensive legal work is often remedial work. By the time a buyer has signed a reservation agreement, paid a deposit, or applied for finance through an unsuitable vehicle, the lawyer is no longer designing the transaction. They're trying to save it.

That distinction matters. A good international real estate lawyer reduces risk before you become committed. They test the asset, the seller, the ownership chain, the tax position, and the closing mechanics before your influence wanes.

Practical rule: In an overseas purchase, legal review should happen before you sign anything that puts money at risk.

Experienced investors take a different approach than first-timers. They don't treat legal fees as dead cost. They treat them as insurance against bad title, poor drafting, avoidable tax friction, and preventable delays at completion.

Why the specialist matters

A local generalist may be perfectly competent for ordinary domestic work. Cross-border deals need more than domestic competence. They need someone who can coordinate property law with tax, compliance, financing, and often private wealth planning.

That's especially true when the buyer is using a company, trust, family office structure, or offshore holding vehicle. Once those elements are in play, the transaction stops being simple conveyancing. It becomes a structured acquisition with multiple points of failure.

In practical terms, the right lawyer should be able to tell you:

- Whether your ownership structure fits the asset and your exit plan

- Whether the lender will accept that structure without additional conditions

- Whether your intended use is legally clean, including rental restrictions and planning concerns

- Whether the timing is wrong, even if the property itself is fine

That's why the first serious call should be legal, not sales, not mortgage, and not tax in isolation.

What an International Real Estate Lawyer Actually Does for You

Most investors underestimate the scope of the job. They think the lawyer checks title, reviews the contract, and attends closing. In a domestic purchase, that may be close enough. In a cross-border deal, it isn't.

Due diligence that goes beyond title

The first job is to verify what sits underneath the listing. Ownership, liens, planning position, building status, restrictions on use, and the legal identity of the seller all need testing. If the buyer is acquiring through a company, the lawyer also needs to check whether that vehicle creates downstream issues for tax, lender approval, or registration.

A weak diligence process often misses the things that don't appear in glossy marketing. Holiday-let restrictions. Incomplete permits. Occupancy issues. Unusual easements. Historic debts attached to the property or the ownership vehicle. These are the problems that destroy projected yield after completion.

Contract management that protects leverage

In international deals, the contract isn't a formality. It is your ultimate means of influence.

The lawyer's role here is to shape conditions, completion mechanics, default remedies, deposit protections, disclosure obligations, and timelines. In some transactions, the most important work is what gets removed from the contract. In others, it's what gets added before the buyer's money becomes exposed.

Language risk also matters. If any part of the transaction turns on translated paperwork, don't assume commercial translation is enough. A practical primer on when translated contracts are legally valid is worth reviewing because enforceability depends on more than readability.

A contract can be understandable and still fail to protect the buyer where local law, translation practice, and execution formalities aren't aligned.

Tax structuring before exchange

This is the area many investors leave too late. In the UK, the introduction of the Annual Tax on Enveloped Dwellings in 2013 and a 15% stamp duty land tax rate for certain residential purchases by non-natural persons in 2012 made specialist legal structuring far more important for overseas investors, as noted by CMS's international real estate practice overview. The same source also notes that its real estate practice spans over 800 lawyers in 40 countries, which tells you how often property work now crosses borders.

The practical lesson is simple. Structure first, acquire second.

If you buy in the wrong name and try to fix it later, the restructuring may be materially more expensive and less efficient. In UK practice, that's why experienced advisers treat conveyancing, ownership design, and tax advice as one stack of work rather than separate instructions. Buyers looking at family succession issues should also understand the wider exposure around inheritance tax on foreign property.

Compliance and execution

The final pillar is compliance. This includes identity checks, beneficial ownership evidence, source-of-funds documentation, lender conditions, and filing requirements. Cross-border transactions fail here more often than buyers expect because clients assume the funds are the only thing that matter. They aren't. The paper trail matters just as much.

A strong international real estate lawyer doesn't just answer legal questions. They sequence the whole deal so the legal, tax, and compliance work supports completion instead of colliding with it.

Why a Property Deal in Dubai Is Not Like One in London

Buyers often assume that all mature property markets operate on roughly the same legal logic. They don't. The legal culture behind the transaction changes how risk appears, how contracts function, and who controls the closing process.

A deal in London is typically driven by negotiated documents and solicitor-led coordination. A deal in Spain often leans more heavily on formalities, registries, and notarial procedure. Dubai adds another layer because market practice, master developer rules, freehold zones, and administrative process all influence the legal pathway.

Common Law and Civil Law feel different in practice

In Common Law systems such as England, the contract usually carries more of the commercial and legal detail. The lawyers negotiate hard because the contract has to do a lot of work.

In many Civil Law systems such as Spain, the notarial and registration framework plays a more visible role in formalising the transaction. That doesn't make it safer by default. It just means the pressure points are different. Buyers still need counsel to verify what the public records say, what they don't say, and how pre-signing obligations line up with the notarial closing.

Dubai deserves separate treatment because investors can assume it is “another freehold market” when it is not. The rights available, the administrative route, and the practical importance of local process can differ from both London and Madrid. If you're comparing that market in more detail, this guide on how to invest in Dubai real estate is a useful market primer.

Property law at a glance

| Legal Aspect | United Kingdom (Common Law) | Spain (Civil Law) | Dubai, UAE (Hybrid/Freehold Zones) |

|---|---|---|---|

| Contract emphasis | Detailed negotiated contract usually carries major risk allocation | Formal process and notarial completion are more central | Contract terms matter, but administrative and local procedural compliance are equally important |

| Role of notary | Limited compared with Civil Law systems | Central to completion formalities | Process depends on transaction type and local authority requirements |

| Title and registration | Lawyer-led diligence and registration sequencing are critical | Registry review and notarial execution play a larger role | Buyers must pay close attention to developer, land department, and zone-specific procedures |

| Buyer risk if unadvised | Hidden obligations in documents and structure | False comfort from formal process without full diligence | Misunderstanding ownership rights, restrictions, or closing mechanics |

Compliance now changes the transaction itself

Another mistake is treating compliance as post-offer admin. In some jurisdictions, compliance determines whether the deal can complete at all.

In the UK, the Register of Overseas Entities requires overseas companies owning UK land to disclose beneficial owners, and the Economic Crime and Corporate Transparency Act 2023 is expanding those rules, as outlined by Latham & Watkins' real estate practice note. Failure to comply can prevent registration of a sale. That means entity structure isn't a side issue. It can become the issue.

If an overseas buyer's structure can't satisfy local disclosure rules, the transaction can fail even when price, finance, and title all look acceptable.

That's why a specialist lawyer adds value country by country. In London, they may be protecting registrability and lender confidence. In Spain, they may be stress-testing the formal title path and usage rights. In Dubai, they may be making sure the buyer acquires the rights they think they're acquiring.

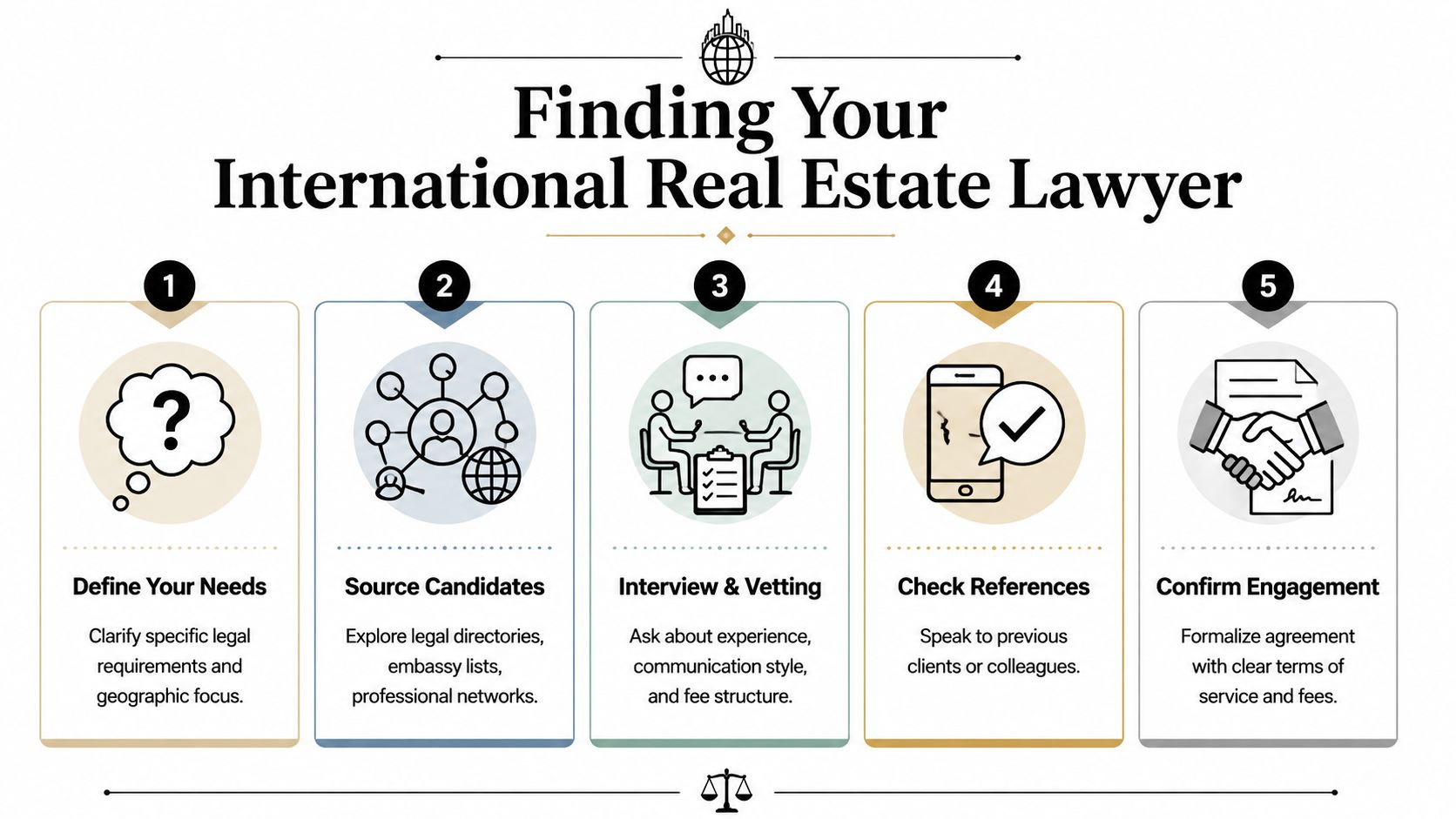

How to Find and Hire the Right International Lawyer

Most buyers ask the wrong first question. They ask, “Who is good in this city?” A better question is, “Who regularly handles my type of cross-border transaction in this city?”

The answer may not be the most visible name locally. It may be the firm that understands non-resident lending, family wealth structures, overseas entities, and investor timelines. In the UK, the Legal Services Act 2007, followed by key market changes from 2011, liberalised the legal market and encouraged multi-disciplinary firms that can coordinate conveyancing, tax, and planning advice. That matters for investors because property law now sits in a more competitive and integrated environment. The scale of the specialist field is also clear in the US, where IBISWorld projects 50,705 businesses and a market size of $26.2 billion in 2026 for real estate law firms, according to IBISWorld's industry report.

Start with fit, not reputation

A strong domestic conveyancer may be the wrong choice for a non-resident acquisition. The right lawyer should understand your nationality risk profile, ownership vehicle, financing route, intended use, and exit horizon.

Useful sourcing channels include:

- Professional directories and legal rankings that identify real estate and cross-border specialists

- Embassy or consular referral lists where available

- Referrals from private bankers, tax advisers, and relocation professionals

- Investor communities and expat groups, used carefully and only as a starting point

A broad investment checklist on tips for investment property can help you frame your buying criteria before you interview counsel.

Ask questions that expose real experience

The interview should test execution, not charm. Ask specific questions about transactions like yours.

Try questions such as:

- Have you acted for buyers from my country into this market before?

- What usually causes delay for non-resident buyers here?

- How do you coordinate with local tax, lending, and notarial professionals?

- Have you handled purchases through companies, trusts, or overseas entities in this jurisdiction?

- What part of my proposed structure concerns you most?

The quality of the answers tells you more than testimonials ever will. A serious lawyer will identify friction points early. They won't promise a “smooth process” without first understanding the facts.

Here's a useful discussion on what buyers often overlook when choosing representation:

What good hiring looks like

Good hiring decisions usually share the same features:

- Clear scope with deliverables listed in writing

- Named lead lawyer rather than a vague team promise

- Transparent fee basis and likely exclusions

- Defined communication rhythm so you know who updates whom and when

- Willingness to challenge the deal if something doesn't stack up

The best instruction letters aren't long. They're precise. They define who is advising on title, tax coordination, compliance, financing conditions, and completion mechanics.

If a firm can't explain where its role starts and stops, expect confusion later.

Understanding Legal Fees and Managing Costs

Legal fees only feel expensive when you compare them to the wrong benchmark. Many buyers compare them with estate agency fees or mortgage costs. The correct comparison is with the cost of a defective transaction.

The three fee models you'll usually see

For standard residential work, firms often use a fixed fee. This is easiest to budget for, but only if the scope is narrow and clearly defined. A fixed fee should state what it covers, what triggers extra charges, and whether company work, lender work, tax input, or post-completion filings sit outside the quote.

For more complex cross-border matters, firms may charge hourly rates. That's common when the deal involves bespoke structuring, difficult negotiations, regulatory problems, or a disputed issue. Hourly billing isn't bad in itself. It becomes problematic when the firm can't estimate likely time bands or identify the cost drivers.

In some larger or commercial matters, you may see value-linked or percentage-based pricing. That can make sense where the work is highly transactional and the asset value materially changes the risk and drafting burden. Retail investors should read these proposals carefully because the percentage headline often says less than the exclusions.

What should appear in the engagement letter

A clean quote should separate legal fees from disbursements. Those are third-party costs such as registration charges, notarial fees, filing charges, translations, corporate searches, and certification costs.

Ask for these items in writing:

- Scope of work so you know exactly what the lawyer is doing

- Assumptions such as single buyer, no title defects, no lender complications

- Exclusions including tax opinions, litigation, immigration, or company formation if relevant

- Disbursement policy covering what will be billed at cost

- Fee triggers for extra work such as delayed completion, revised structure, or seller default

Where buyers go wrong on cost control

The common mistake is trying to save money by splitting advice too aggressively. One firm handles conveyancing, another handles tax, and nobody owns the transaction as a whole. That usually creates duplicated questions, slower decisions, and gaps in accountability.

Another mistake is treating legal budget as a fixed number before the structure is settled. Cost planning should follow risk planning. If you're buying through a company, borrowing cross-border, or expecting future succession planning, the legal budget should reflect that complexity from the start.

Cheap legal work is often expensive later.

Red Flags to Watch for When Buying Property Abroad

The danger signs usually show up early. Buyers miss them because they want the deal to work.

Red flags that relate to the property

Some warnings sit with the asset itself.

- Unclear ownership. If the seller can't produce a clean title story, stop. Ambiguity around ownership, charges, rights of way, or occupancy usually gets more expensive, not less.

- Missing approvals or patchy records. If permits, plans, licences, or historical documents are incomplete, assume there is legal risk until proved otherwise.

- Usage claims that sound too easy. If a sales agent says holiday lets, subdivision, refurbishment, or residency-linked use is “no problem”, get that checked independently.

If you're evaluating tenure risk in markets where the distinction matters, this guide on freehold vs leasehold is a useful starting point.

Red flags that relate to people and process

The most serious transaction failures often come from conduct, not bricks and mortar.

- Pressure to sign immediately. Urgency is a classic way to stop proper review.

- One adviser acting for both sides. Conflicts of interest are manageable only when they're explicit, limited, and legitimately acceptable. In many investor situations, they're a reason to walk away.

- Unusual payment instructions. Requests for cash, offshore redirection, informal side payments, or undocumented adjustments should trigger immediate caution.

Red flags that relate to compliance

Cross-border buyers sometimes think compliance is a box-ticking exercise. It isn't. In UK transactions involving overseas buyers, firms and lenders must satisfy anti-money-laundering and source-of-funds obligations. A lawyer who is slow to manage that KYC process can cause significant delays or even a lender's refusal to proceed, as described in Pillsbury's overview of international real estate work.

That's a useful warning beyond the UK as well. If your lawyer isn't organised on compliance, every other part of the deal can become irrelevant.

A disorganised legal team can lose a perfectly good property for a buyer who had the money, the intent, and the lender, but not the documentation in the right form at the right time.

What to do when you spot one

Don't negotiate against a red flag with optimism. Escalate it into a written legal question. Ask what evidence resolves it, who supplies that evidence, and what happens if it cannot be resolved before exchange or completion.

If the answers stay vague, you already have your answer.

World Property Investor helps buyers compare jurisdictions, understand market fundamentals, and avoid predictable mistakes before capital is committed. If you're researching where to buy next, visit World Property Investor for in-depth country guides, tax and ownership explainers, and practical resources for international property investors.