Embarking on property investment can seem daunting, but the fundamental principle is straightforward: acquiring an asset designed to generate returns in two primary ways. Firstly, it produces a regular rental income. Secondly, its value should appreciate over the long term. Unlike the volatility of the stock market, property offers a tangible asset that has historically proven to be a reliable vehicle for wealth creation.

This guide provides a practical, step-by-step framework for starting your investment journey, focusing on core principles applicable to global investors.

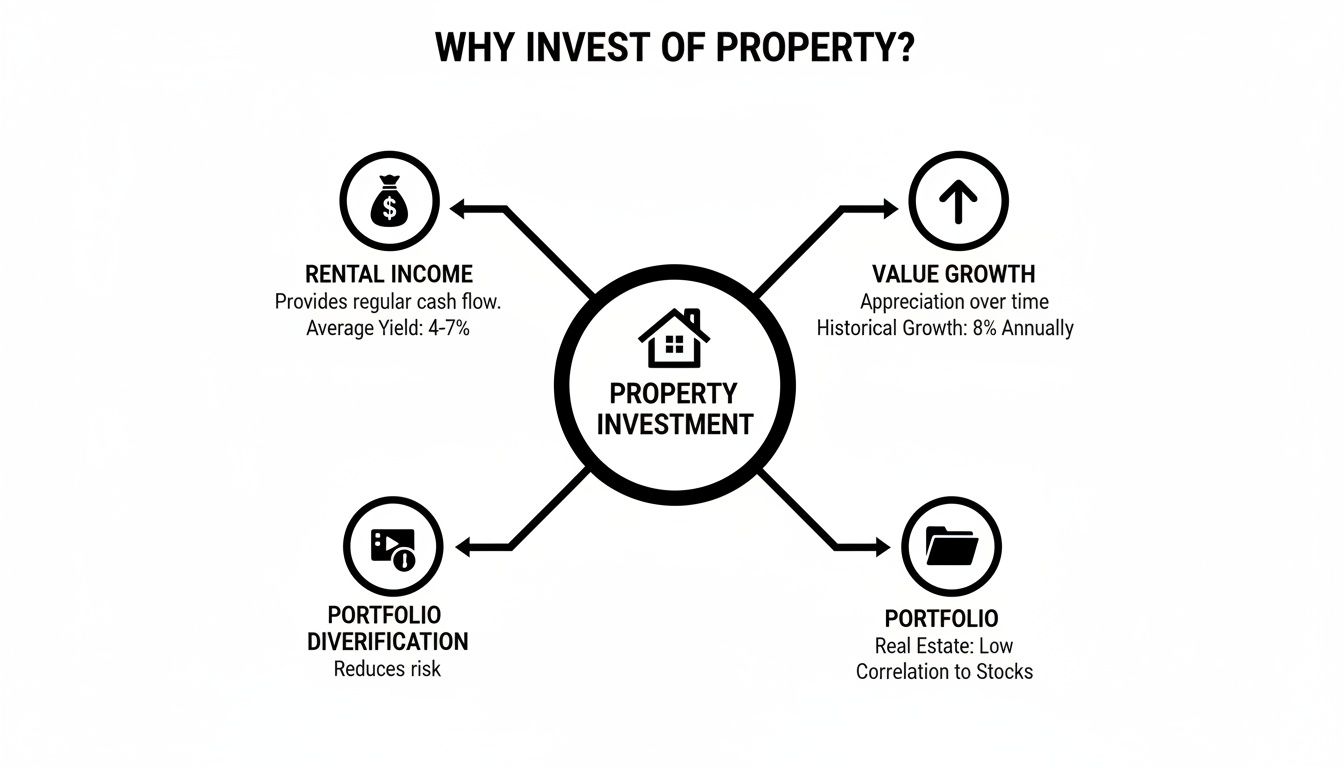

Starting Your Property Investment Journey

For generations, property has been a dependable path to long-term financial security, built upon a dual-stream return model.

The first stream is rental income—the consistent cash flow generated from tenants. In many established economies, such as the UK, structural housing shortages underpin robust rental demand. Data from bodies like the Office for National Statistics (ONS) often shows private rental prices on a sustained upward trend, which is a positive indicator for landlords.

The second is capital appreciation, the term for a property's increase in value over time. While all markets experience cycles, well-located property has a strong history of long-term growth. This combination of immediate income and future wealth creation is what distinguishes property from other asset classes.

Establishing Your Core Principles

Successful property investing is not about "get-rich-quick" schemes or attempting to time the market perfectly. It is a long-term strategy centred on building a resilient portfolio. The key is to acquire high-quality assets in locations with strong fundamentals—such as growing job markets, excellent transport infrastructure, and positive demographic trends.

A common error for new investors is being swayed by a property's cosmetic appeal or underestimating the true operational costs. A successful strategy is founded on rigorous research and meticulous financial planning, not an emotional response to a modern kitchen.

This disciplined mindset protects against speculation and helps avoid common pitfalls. For a deeper analysis of these foundational concepts, our detailed beginner's guide to real estate investing is an excellent resource.

Aligning Goals with Strategy

Before analysing any property listing, you must define your objectives. Your personal financial goals are the blueprint for your investment strategy.

-

Seeking regular income? If your aim is to supplement your salary or build a pension, a high rental yield strategy is optimal. This often involves targeting properties in university towns or regional cities where acquisition costs are lower relative to rental income.

-

Prioritising long-term growth? If your goal is significant wealth creation over a decade or more, your focus should be on capital growth. This may lead you to areas with major regeneration projects or planned infrastructure improvements, even if initial rental income is more modest.

Defining your objectives at the outset makes subsequent decisions—from market selection to property choice—far more streamlined and effective.

Learning the Language of Property Investment

To make informed decisions, you must understand the key financial metrics. A handful of core calculations will allow you to cut through marketing hype, assess the viability of a deal, and distinguish a sound investment from a potential liability.

Think of these numbers as your analytical toolkit. Mastering them will enable you to evaluate any property, in any market, with confidence.

The diagram below illustrates how the distinct benefits of property investment work together to build wealth over time.

This blend of short-term income and long-term value appreciation makes property a robust asset for both novice and experienced investors. Now, let’s dissect the core metrics you will use.

Key Property Investment Metrics Explained

This quick-reference table outlines the essential financial terms. Familiarity with these concepts provides a significant advantage when analysing investment opportunities.

| Metric | What It Measures | Why It Matters for Beginners |

|---|---|---|

| Rental Yield | The annual rental income as a percentage of the property's value. | A simple, effective tool for comparing the income potential of different properties. |

| Cash Flow | The net income remaining each month after all operating expenses are paid. | This determines if the property is self-sustaining or requires additional capital from you. |

| Capital Growth | The increase in the property’s market value over time. | The primary driver of long-term wealth, realised upon sale or refinancing. |

| Loan-to-Value (LTV) | The mortgage amount as a percentage of the property’s appraised value. | A key risk metric for lenders; a lower LTV often secures more favourable mortgage terms. |

| ROI | The total return on the actual capital you have invested. | The definitive measure of how effectively your invested cash is performing. |

This table serves as your financial checklist. Let's explore each concept in more detail.

Getting to Grips with Rental Yield

One of the most common metrics is rental yield. It measures the annual rental income relative to the property's cost, providing a quick comparison of income-generating potential.

There are two types, but only one gives a true picture of performance:

- Gross Yield: This is a preliminary calculation. It is the total annual rent divided by the purchase price. For example, a £200,000 property generating £12,000 in annual rent has a gross yield of 6%.

- Net Yield: This is the critical figure. It is the annual rent minus all operational costs—including mortgage interest, insurance, management fees, and maintenance—divided by the purchase price. This provides a far more accurate reflection of profitability.

Always prioritise the net yield. A property may advertise a high gross yield, but if it is burdened with high service charges or frequent repairs, your actual returns can be significantly eroded.

Cash Flow vs. Capital Growth: The Two Engines of Return

While yield is a useful indicator, your investment strategy will be driven by two primary forces: cash flow and capital growth. Understanding their interplay is fundamental.

Cash Flow is the net amount of cash an investment generates each month after all expenses have been paid. Positive cash flow indicates a surplus, while negative cash flow means you must cover a shortfall.

Capital Growth is the appreciation in the property’s value over time. This is where substantial wealth is often built, but it is illiquid until the property is sold or refinanced.

A balanced portfolio often incorporates both. A high-yielding property in a regional city might provide excellent monthly cash flow. In contrast, an apartment in a prime urban area might offer lower cash flow but superior potential for long-term capital growth.

Understanding Your Financing

Lenders use the Loan-to-Value (LTV) ratio to assess their risk. This is the mortgage size as a percentage of the property’s market value. A £150,000 mortgage on a £200,000 property represents a 75% LTV.

A lower LTV (i.e., a larger deposit) reduces the lender's risk and can result in better interest rates. For most buy-to-let mortgages, lenders typically require a minimum deposit of 25%, corresponding to a maximum LTV of 75%.

These metrics ultimately inform your overall Return on Investment (ROI), which measures the performance of a property relative to the amount of your own capital invested. To master this calculation, you can learn how to calculate ROI for real estate in our dedicated guide. Once you are proficient with these terms, you can analyse deals with professional rigour.

How To Buy Your First Investment Property Step By Step

This section provides a practical roadmap for acquiring your first investment property, breaking the process down into five clear, sequential stages.

Following this framework ensures all critical steps are covered, from initial financial preparation to final acquisition.

This step-by-step guide is designed to demystify the buying process, enabling you to proceed with a clear and confident plan.

Step 1: Prepare Your Finances

Before viewing properties, your first action should be to consult a mortgage broker. They will assess your financial position and help you secure an Agreement in Principle (AIP). An AIP is a conditional offer from a lender stating how much they are prepared to lend you.

This is a non-negotiable step. It demonstrates to estate agents and vendors that you are a credible buyer, providing a significant advantage in a competitive market. It also establishes a firm budget, preventing wasted time on unaffordable properties.

Step 2: Define Your Investment Criteria

With your budget confirmed, you can specify your search criteria. This involves making strategic decisions about the type of property you wish to acquire and the tenant profile you want to attract. These choices will directly influence your potential returns and management requirements.

Common strategies include:

- Student Lets: Typically located in university cities, these can offer high rental yields but often involve more intensive management and annual tenant turnover.

- Family Homes: Two or three-bedroom houses in suburban areas with good schools often attract long-term tenants, providing stable and reliable income.

- Young Professional Flats: Modern one or two-bedroom flats near city centres or transport hubs appeal to a mobile demographic and can offer a good balance of yield and capital growth.

Your decision should align with the investment goals you established earlier. For more detail on mortgage options, review our complete guide to financing your investment property.

Step 3: The Property Search And Viewings

Begin your search on major property portals, but also register directly with local estate agents in your target areas, as they often have access to properties before they are listed online.

During viewings, look beyond superficial aesthetics.

Focus on the fundamentals. Inspect for signs of damp, assess the condition of the roof, enquire about the age of the boiler, and check the windows. These are significant capital expenditure items that can severely impact your profitability.

Take your time during viewings. Ask direct questions about the property's history and the reason for the sale. A prudent investor learns to think like a surveyor, identifying potential issues before they become costly problems.

Step 4: Making An Offer And The Legal Process

Once you have identified a property where the financials are viable, it is time to make a strategic offer. Your offer should be based on the property’s condition, its true market value (supported by recent comparable sales data), and your own budget. An AIP and a chain-free position provide strong negotiating leverage.

Upon acceptance of your offer, the legal process, known as conveyancing, begins. You will need to appoint a solicitor to manage the legal documentation. Concurrently, you will submit your formal mortgage application and instruct a surveyor to conduct a thorough inspection. The surveyor's report is critical; if it uncovers significant defects, you can use it to renegotiate the price or withdraw from the purchase.

Step 5: Exchange And Completion

The final stages are the exchange of contracts and completion. Exchange is the point at which the transaction becomes legally binding. Both parties sign identical contracts, and you pay the deposit.

Completion is the day the remaining funds are transferred, legal ownership passes to you, and you receive the keys to your investment property. You are now officially a property investor. This structured approach, from finance to completion, removes ambiguity and empowers you to make logical, well-informed decisions.

Navigating Mortgages and Taxes for Your Investment

Securing appropriate financing and understanding tax obligations are fundamental to the profitability of your investment. The structure of your purchase will significantly impact your returns for years to come. This section outlines the essential mortgage and tax considerations for new investors.

Mastering these two areas will give you greater control, protect your profits, and help you avoid unforeseen financial burdens.

Understanding Buy-To-Let Mortgages

A mortgage for an investment property is assessed differently from a residential mortgage. Lenders providing buy-to-let (BTL) mortgages are primarily concerned with the property's potential rental income rather than your personal salary. A common requirement is that the projected monthly rent must cover the mortgage payment by at least 125%.

Two main types of mortgage products are available:

- Repayment Mortgage: Each monthly payment covers both the interest and a portion of the original loan capital. At the end of the term, the property is owned outright.

- Interest-Only Mortgage: Your monthly payment covers only the interest accrued on the loan. This results in lower monthly outgoings and improved cash flow, but the full loan amount remains due at the end of the term. The capital is typically repaid by selling the property or refinancing.

Many investors opt for interest-only mortgages to maximise monthly cash flow. This is a standard strategy, but it relies on the property appreciating in value to enable repayment of the loan.

Key UK Property Taxes Explained

Property ownership comes with several tax liabilities. Failing to budget for these can turn a profitable investment into a financial drain.

The three main taxes you will encounter are:

- Stamp Duty Land Tax (SDLT): A one-off tax paid upon purchase. Investors buying an additional property pay a higher rate, which includes a surcharge on top of the standard SDLT bands. This is a significant upfront cost that must be factored into your budget.

- Income Tax: Profit generated from rental income is taxable. It is calculated by deducting allowable expenses (such as letting agent fees, insurance, and repairs) from your total rental income. The remaining profit is taxed at your personal income tax rate.

- Capital Gains Tax (CGT): This is payable upon the sale of the property on the profit made. The taxable gain is the difference between the sale price and the purchase price, less any deductible costs.

Navigating the complexities of property tax is essential for maximising returns. Recent legislative changes, particularly concerning mortgage interest relief, underscore the importance of correct investment structuring from the outset.

Structuring Your Investment for Tax Efficiency

A key initial decision is whether to purchase a property in your personal name or through a limited company, as the tax implications differ significantly.

Purchasing as an individual is straightforward, but higher-rate taxpayers can no longer deduct their full mortgage interest from rental income to reduce their tax liability. Instead, a tax credit equivalent to 20% of mortgage interest payments is provided.

Conversely, purchasing through a limited company allows the full mortgage interest to be treated as a deductible business expense. The company pays Corporation Tax on its profits, which can be lower than higher rates of Income Tax.

For a comprehensive analysis, you can learn more about how to understand property taxes in our detailed guide. It is always advisable to consult a qualified accountant to discuss your specific circumstances.

Finding the Right Market for Long-Term Success

In property investment, location is paramount. A well-renovated house in a declining area is a poor investment, whereas an average property in a thriving location can deliver excellent returns.

Successful investing requires looking beyond media headlines to analyse the fundamental drivers of growth in a specific city or region. This skill separates speculative gambling from strategic, long-term investments that build sustainable wealth.

Analysing the Key Drivers of Demand

Before examining individual properties, you must analyse the location. The long-term performance of your investment is directly tied to the economic and social health of the area. Strong tenant demand and capital growth are the results of specific local factors.

Focus your research on these core pillars:

- Major Employment Hubs: A diverse and growing job market is the most critical driver. Look for areas with major employers, new business investment, or strong sectors like technology, healthcare, and education. According to Gov.uk data, areas with significant public and private sector investment consistently see higher population growth.

- Transport and Infrastructure: New or improved transport links act as a powerful catalyst for price growth. A new railway line or regenerated station can dramatically reduce commute times, increasing an area's attractiveness and boosting property values.

- Population Trends: Is the local population growing? Data from bodies like the Office for National Statistics (ONS) can reveal which towns and cities are attracting new residents. A rising population increases competition for housing, driving up both rental and sale prices.

- Local Amenities: Never underestimate the importance of good schools, parks, shops, and restaurants. These elements transform a housing area into a desirable community, ensuring consistent tenant demand.

Established vs. Emerging Markets

Your choice of market will depend on your risk appetite and investment objectives. Markets can be broadly categorised as established or emerging, each offering a different risk-reward profile.

An emerging market may offer higher potential growth, but an established market provides the stability of proven demand. The optimal choice depends entirely on your personal strategy and risk tolerance.

For beginners, understanding this distinction is crucial for aligning your location choice with your financial goals from day one.

Established vs. Emerging Property Markets: A Comparison

The table below outlines the key differences between established property hubs and up-and-coming areas, helping you decide which market type aligns with your investment strategy.

| Characteristic | Established Markets (e.g., London, Manchester) | Emerging Markets (e.g., Regional Towns with Regeneration) |

|---|---|---|

| Capital Growth | Slower, more stable long-term growth. | Higher potential for rapid growth, but also more volatility. |

| Rental Yield | Typically lower due to high property prices. | Often higher, offering better initial cash flow. |

| Risk Profile | Lower risk, with a proven history of demand and liquidity. | Higher risk, as growth is often contingent on future projects. |

| Entry Price | High, requiring significant initial capital investment. | Lower, making it more accessible for first-time investors. |

The decision between the stability of an established city and the higher-yield potential of an emerging town depends on your objectives. There is no single correct answer—only the one that is right for your strategy.

Looking Beyond the Headlines

Choosing the right location requires thorough, objective research. Do not rely solely on media articles proclaiming the "next property hotspot." Instead, learn to interpret local data yourself.

Compare historical price growth, analyse average rental yields, and assess the pipeline of new housing supply. This deeper understanding of what makes a location a prime candidate for investment is explored further in our guide on the role of location in real estate investment success.

By focusing on these long-term fundamentals—jobs, transport, demographics, and amenities—you can build a reliable framework to assess any market and make an educated decision that maximises your investment's potential for success.

How to Manage Your Property and Mitigate Common Risks

Acquiring your first investment property is a significant achievement, but effective management is what transforms it into a profitable, passive asset rather than a source of stress.

Your first major decision is determining your management approach. This choice will directly impact your time, stress levels, and financial returns. There are two primary options.

Self-Management vs Hiring an Agent

Self-management provides complete control and saves on agent fees, which typically range from 10-15% of the rental income. However, it means you are responsible for all aspects of management, including marketing the property, vetting tenants, handling maintenance issues, and collecting rent. This can be a viable option if you live locally and have the necessary time and expertise.

Conversely, hiring a letting agent creates a more passive investment. A reputable agent manages all tenant relations and ensures the property remains legally compliant. For most beginners, and particularly for those investing remotely, this is often the most prudent approach. It professionalises the operation and frees up your time.

Understanding Your Legal Duties

Being a landlord in the UK involves significant legal responsibilities designed to ensure tenant safety. Non-compliance can result in substantial fines or legal action.

Key duties include:

- Gas Safety: An annual inspection of all gas appliances by a Gas Safe registered engineer is mandatory. A copy of the safety certificate must be provided to the tenant.

- Electrical Safety: An Electrical Installation Condition Report (EICR) is required every five years to certify that the property's electrical systems are safe.

- Deposit Protection: Any tenancy deposit must be registered with a government-approved scheme within 30 days of receipt.

Proactive risk management is the cornerstone of sustainable property investing. It’s not about avoiding problems entirely—it’s about having a plan in place so that when they inevitably arise, they are manageable events, not financial crises.

Proactive Risk Management

Successful investors anticipate and plan for potential challenges. The two most significant risks are unexpected costs and periods of vacancy.

First, a dedicated maintenance fund is essential. A sound practice is to allocate 1-2% of the property’s value annually for repairs and upkeep. This financial buffer prevents unforeseen expenses, such as a boiler failure, from derailing your investment.

Second, you must budget for void periods—the time between tenancies when the property is unoccupied. Factoring in at least one month of vacancy per year ensures you can cover the mortgage and other fixed costs even without rental income.

Finally, comprehensive landlord insurance is non-negotiable. It provides a financial safety net against risks such as property damage, loss of rent, and liability claims.

Common Questions About Property Investing

Even with a clear strategy, questions will arise. This is a normal part of the learning process.

Here are concise, practical answers to some of the most frequently asked questions from new investors.

How Much Money Do I Need to Start?

There is no single figure, but the primary initial cost is the deposit. For a typical buy-to-let mortgage in the UK, lenders generally require a minimum deposit of 25% of the property's value. For a £200,000 property, this would be £50,000.

However, you must also budget for acquisition costs. These include Stamp Duty Land Tax (which includes a surcharge for additional properties), legal fees, and survey costs. A prudent estimate is an additional 5-7% of the purchase price for these expenses.

Therefore, for a £200,000 property, you would realistically need between £60,000 and £64,000 in available capital.

Is It Better to Buy with Cash or a Mortgage?

The majority of experienced investors use mortgages. This strategy, known as leveraging, is powerful. It allows you to control a high-value asset with a relatively small amount of your own capital, enabling you to build a more diversified portfolio more quickly. When successful, it significantly enhances your Return on Investment (ROI).

Purchasing with cash eliminates mortgage payments, resulting in excellent monthly cash flow and a simplified buying process. The drawback is that a large amount of capital is tied up in a single asset, limiting your capacity for diversification and expansion.

For most beginners, leveraging with a sensible mortgage is the recommended approach as it multiplies your investment power. However, it is crucial to remember that leverage also amplifies risk if property values decline or interest rates rise.

Should I Manage the Property Myself or Hire an Agent?

This decision involves a trade-off between your time and expertise versus your money.

Self-management saves the typical letting agent fee of 10-15% of the monthly rent. However, it requires you to manage all responsibilities, from finding tenants and handling emergency maintenance calls to ensuring full legal compliance.

For most new investors, especially those purchasing outside their local area, appointing a reputable letting agent is a wise decision. It professionalises the entire process, ensures legal compliance, and transforms your property into a genuinely passive investment.

At World Property Investor, we provide the data-driven guides and market analysis you need to compare opportunities and make confident decisions across the globe. Explore our resources to find your next investment at https://www.worldpropertyinvestor.com.