Entering the world of property investment is a significant financial step, but it remains one of the most reliable methods for building long-term wealth. The principle is straightforward: acquire an asset that generates a consistent rental income while simultaneously appreciating in value. This dual-stream return of cash flow and capital growth makes property a foundational component of many successful investment portfolios.

Starting Your UK Property Investment Journey

Embarking on a property investment journey in the United Kingdom offers a tangible opportunity to build substantial wealth. This is not about speculating on short-term market fluctuations; a robust property strategy is built on solid, long-term fundamentals.

Think of an investment property as planting a tree. The monthly rent is the fruit harvested each year—a consistent, reliable return. Simultaneously, the property's value, much like the tree itself, grows taller and stronger over the years. This increase in value is known as capital growth or appreciation.

Understanding the Two Pillars of Return

Every successful investor understands the two primary ways property generates wealth. Deciding which to prioritise will shape your entire investment strategy.

- Rental Income (Cash Flow): This is the net profit remaining from rental payments after all operational costs—mortgage, insurance, maintenance, and management fees—have been settled. It is the liquid income that provides an immediate, recurring return.

- Capital Growth (Appreciation): This refers to the increase in the property's market value over time. This return is realised only when the asset is sold for a profit.

For instance, an investor purchasing a flat in Manchester might focus on achieving a high rental yield for immediate cash flow. In contrast, an investor buying a house in an emerging London commuter town may be more focused on long-term capital appreciation. The UK market is sufficiently diverse to support both objectives. To explore these core concepts further, review our beginner’s guide to real estate investing.

The UK's property sector continues to demonstrate resilience. The market generated USD 121.7 billion in revenue in a recent year and is projected to reach USD 166.0 billion by 2030, according to industry analysis. These figures underscore the market's underlying strength and long-term potential for investors. You can learn more about UK real estate market growth on GrandViewResearch.com.

A successful entry into property investment is not about timing the market perfectly but about time in the market. By focusing on high-quality assets in areas with strong economic fundamentals, beginners can build a resilient portfolio that delivers returns for decades.

This foundational knowledge allows a transition from passive saving to active investing, enabling strategic decisions aligned with your financial goals. The key is to build confidence through education and create a clear, practical roadmap for the first acquisition.

How to Analyse a Property Investment

Successful property investment is driven by data, not emotion. Before committing capital, it is imperative to learn how to evaluate a potential acquisition with professional diligence. This involves looking beyond aesthetics to focus on the core financial metrics that reveal a property's true performance and potential. For any beginner, mastering these calculations is a critical first step.

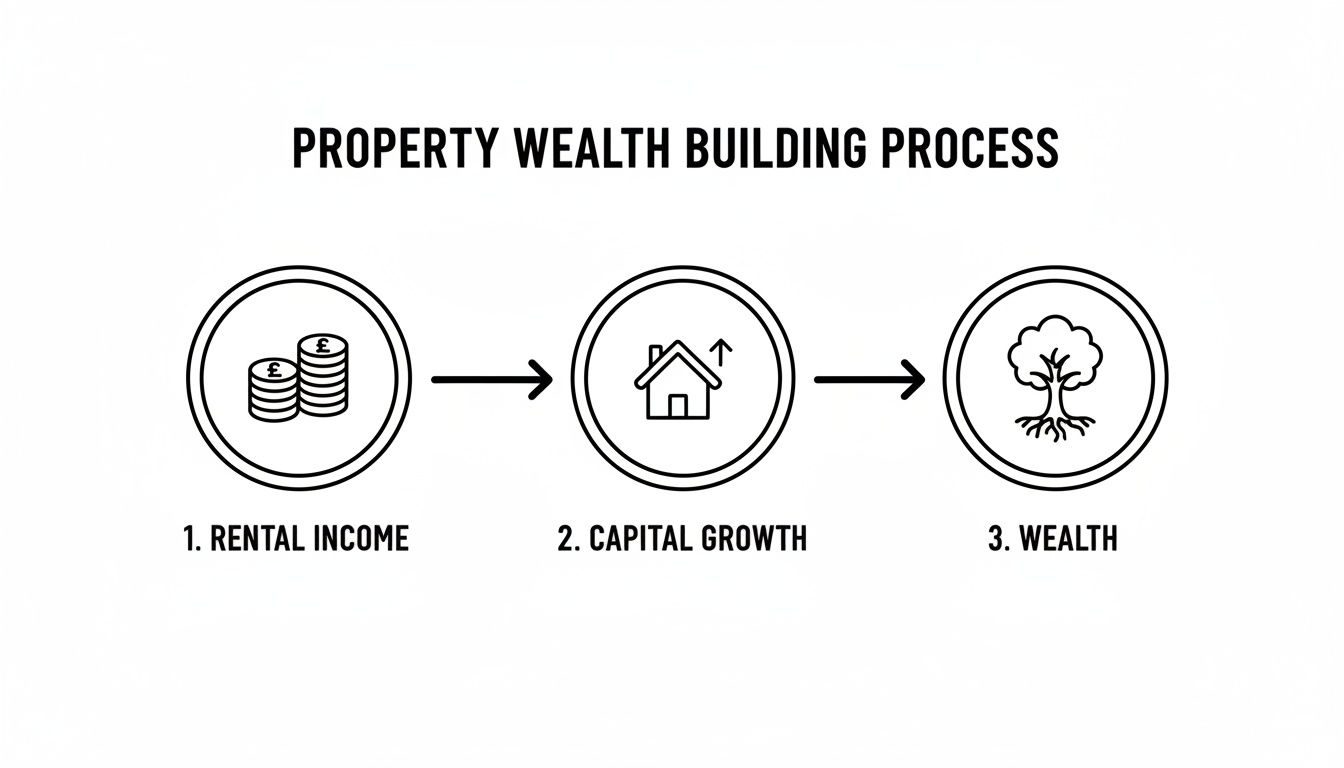

The two primary ways a property generates wealth are through ongoing rental income and long-term capital growth. This simple diagram shows how these two streams combine to build your portfolio over time.

As you can see, consistent rental income provides the cash flow to keep the investment running, while capital growth builds your net worth over the years, leading to substantial wealth.

Calculating Key Performance Metrics

Three fundamental metrics form the bedrock of investment analysis: rental yield, return on investment (ROI), and loan-to-value (LTV). Each provides a different perspective on the financial viability of a deal.

1. Rental Yield

This metric measures the annual rental income as a percentage of the property’s value. It serves as a high-level indicator to quickly compare the income-generating potential of different assets.

- Calculation: (Annual Rental Income / Property Value) x 100 = Gross Yield %

- Example: A £250,000 flat that rents for £1,250 per month (£15,000 per annum) has a gross yield of 6.0%. (£15,000 / £250,000) x 100.

2. Return on Investment (ROI)

ROI provides a more accurate measure of performance by comparing the net profit against the actual cash invested (deposit and acquisition costs). It reveals how effectively your capital is being deployed.

- Calculation: (Annual Net Profit / Total Cash Invested) x 100 = ROI %

- Example: For the same £250,000 flat, if your deposit and costs totalled £70,000 and your annual net profit (after mortgage, insurance, etc.) was £5,000, your ROI would be 7.14%. (£5,000 / £70,000) x 100.

Mastering these calculations is essential. You can explore further methods to determine a property's investment potential in our detailed guide.

Looking Beyond the Numbers at Market Fundamentals

While financial metrics are crucial, they only provide a partial view. The long-term success of a property investment is fundamentally linked to the economic health of its local market. A high yield in a declining area presents a significant risk. Investors must learn to identify indicators of sustainable growth.

Key factors to research include:

- Employment and Economy: A growing job market, driven by inward investment from major employers, is the engine of tenant demand.

- Infrastructure and Transport: New rail links, such as Crossrail or HS2, and major road improvements can substantially increase property values and rental desirability.

- Population Trends: Analyse demographic data from credible sources like the Office for National Statistics (ONS) to identify areas with population growth.

- Supply and Demand: Review local authority planning portals. A large pipeline of new-build developments could saturate the rental market and suppress yields.

Comparing Established and Emerging Markets

A practical way to understand these dynamics is to compare different locations. Consider an established market like London versus an emerging city such as Leeds or Liverpool.

In an established market like Central London, one might find lower rental yields (e.g., 3-4%) but expect more stable, long-term capital growth. Conversely, an emerging city in the North may offer much higher rental yields (6-8% or more) and greater potential for rapid appreciation as regeneration projects take hold, though potentially with higher volatility.

To better understand the performance of different UK property sectors, the table below summarises recent key indicators.

Key UK Property Market Indicators

| Metric/Sector | Performance Figure | Time Period |

|---|---|---|

| UK All Property Total Return | 8.1% | 12-Month Period |

| Industrial Sector Growth | 17.2% | 12-Month Period |

| Build-to-Rent (BTR) Growth | 9.5% | 12-Month Period |

| Average UK Rental Growth | 8.7% | Year-on-Year |

| Central London Office Yield | 4.5% | Q1 2024 |

Source: Data compiled from recent industry reports.

This data illustrates the diverse opportunities available, from the notable growth in industrial property to the steady performance of the residential rental market. It highlights why a macroeconomic perspective is essential.

Ultimately, your choice of location depends on your investment strategy. Whether you are seeking immediate cash flow or long-term wealth accumulation, a thorough analysis of both property-specific metrics and wider market fundamentals will empower you to make an informed decision aligned with your financial goals.

Choosing the Right Investment Strategy for You

There is no single "best" strategy in property investment. The optimal path depends on your financial objectives, available capital, and desired level of active involvement. For any beginner aiming to build a successful UK portfolio, understanding the most common approaches is a crucial first step.

Each strategy presents a different balance of risk, reward, and time commitment. A passive investor may prefer a simple, income-generating asset, whereas a hands-on investor will seek to actively create value. Let's examine the most popular models.

Classic Buy-to-Let (BTL)

The buy-to-let model is the traditional foundation of property investment and the most common starting point. The concept is simple: you purchase a property and let it to a tenant. The objective is to generate consistent monthly income that covers the mortgage and all other costs, leaving a net profit.

This strategy is ideal for investors prioritising steady, long-term returns. For example, acquiring a one-bedroom flat in a well-connected Birmingham suburb for £180,000 could generate £900 per month in rent. After mortgage payments and expenses, this provides a reliable income stream alongside gradual capital appreciation.

- Pros: Straightforward to understand, easier to finance, provides predictable cash flow.

- Cons: Returns can be modest, and appreciation is dependent on wider market movements.

- Ideal Investor: An individual with a long-term outlook seeking a relatively passive source of income.

Buy, Refurbish, Refinance (BRR)

The BRR strategy is suited to the more hands-on investor. It involves acquiring a property requiring modernisation, adding value through refurbishment, and then refinancing with a lender based on its new, higher valuation. This allows the investor to extract their initial capital to fund the next project, creating a powerful method for recycling capital.

Consider finding a dated two-bedroom terraced house in Leeds for £150,000. You invest £20,000 in a new kitchen, bathroom, and redecoration. Post-refurbishment, the property is revalued at £200,000. You could then refinance at 75% of the new value, releasing £150,000—your entire initial investment—to repeat the process.

The BRR model is a powerful method for 'forcing' appreciation rather than waiting for the market to deliver it. It accelerates portfolio growth but requires more knowledge, time, and a higher tolerance for the risks associated with renovation projects.

Houses in Multiple Occupation (HMOs)

An HMO is a property let to at least three people from different households who share facilities like a kitchen and bathroom. Commonly found in university cities such as Manchester or Nottingham, HMOs can generate significantly higher rental yields than a standard BTL because individual rooms are let separately.

This increased cash flow, however, comes with greater management demands and stricter legal regulations, including mandatory licensing from the local housing authority. Managing multiple tenancies, higher tenant turnover, and potential interpersonal issues requires a professional and organised approach.

- Pros: Potentially the highest rental yields and cash flow of any residential strategy.

- Cons: Management-intensive, complex regulations, higher setup costs.

- Ideal Investor: A hands-on investor focused on maximising cash flow, prepared for the additional operational duties.

Another approach is purchasing new-build properties directly from developers. For those seeking a hands-off asset with minimal initial maintenance, it is worth exploring the pros and cons of buying off-plan properties as part of your research. Ultimately, the best strategy for a beginner aligns with their personal circumstances, risk appetite, and financial objectives.

Securing Finance for Your First Investment

Arranging finance is the step that transitions an aspiring investor into a property owner. While this process can appear daunting for a first-timer, it becomes more manageable once the different funding mechanisms are understood. The optimal financing route depends on your strategy, personal financial situation, and the target property.

For most beginners, the journey starts with a mortgage. However, an investment property loan is a fundamentally different product from a residential mortgage on your own home.

Residential vs Buy-to-Let Mortgages

A standard residential mortgage assessment is centred on the borrower. Lenders focus almost exclusively on your personal income and credit history to determine affordability based on your salary.

A buy-to-let (BTL) mortgage is a specialist loan for landlords. The lender's primary focus shifts from the borrower's personal income to the property's income-generating potential. While your personal financial standing remains relevant, the key criterion is whether the property's rental income can comfortably cover the mortgage payments with a sufficient surplus.

Lenders typically require the projected rental income to be at least 125% to 145% of the monthly mortgage payment. This is calculated using a 'stressed' interest rate, which is higher than the actual rate, to ensure the loan remains affordable if interest rates rise or the property experiences a short void period.

Another significant difference is the deposit, or loan-to-value (LTV) ratio. A residential mortgage may be secured with a deposit as low as 5-10%, whereas a BTL mortgage requires a much larger capital contribution.

- Deposit: Expect to provide a minimum deposit of 25% of the property's purchase price.

- Interest Rates: BTL mortgage rates are almost always higher than residential rates to reflect the greater perceived risk.

- Loan Type: Many investors opt for an interest-only BTL mortgage. Monthly payments cover only the interest, which lowers outgoings and maximises cash flow. The principal loan amount is repaid in full upon the eventual sale of the property.

Considerations for International Investors

Securing a UK mortgage as a non-resident presents additional complexities but is entirely feasible. UK lenders are generally more cautious with overseas applicants due to the difficulty in verifying foreign credit histories and income streams.

Expect stricter lending criteria, typically including a larger deposit (often 30-40%), slightly higher interest rates, and more rigorous anti-money laundering checks. A specialist mortgage broker with experience in handling international clients is invaluable in this scenario, as they have relationships with lenders who understand the nuances of overseas applications.

For a deeper analysis, our in-depth guide offers a detailed look at financing an investment property as a global buyer.

Alternative Funding Options

Beyond traditional mortgages, other financing tools can be effective for certain strategies.

Bridging loans are short-term, high-interest loans designed to 'bridge' a funding gap. They are frequently used by investors employing a 'Buy, Refurbish, Refinance' strategy. For example, a bridging loan can be used to purchase an unmortgageable property, fund the renovations to bring it up to standard, and then be repaid with a conventional BTL mortgage once the works are complete.

Whichever route you choose, a strong application is paramount. A clean credit history, a clear business plan for the property, and a substantial deposit are the cornerstones of securing optimal finance for your first investment.

Understanding Your Tax and Legal Duties

A profitable property investor is a compliant one. While the UK's tax and legal framework can seem complex, understanding the fundamentals from the outset is essential for long-term success. This protects your investment, optimises returns, and ensures you operate within the law.

The primary taxes you will encounter are Stamp Duty Land Tax (SDLT), Income Tax, and Capital Gains Tax (CGT). Each applies at a different stage of your investment journey.

Key Property Taxes Explained

Stamp Duty Land Tax (SDLT) is payable upon the acquisition of property in England and Northern Ireland. As an investor purchasing an additional home, you will be subject to a higher rate.

A 3% surcharge applies on top of the standard SDLT rates for any additional residential property purchase. This is a significant upfront cost that must be factored into your financial analysis when evaluating a potential deal.

Income Tax is levied on your rental profits, not the gross rent collected. This is a critical distinction. HMRC allows you to deduct certain allowable expenses from your rental income to determine your taxable profit, making meticulous record-keeping essential.

Capital Gains Tax (CGT) becomes relevant when you sell an investment property for more than its acquisition cost. You are taxed on the gain—the profit—not the total sale price. All individuals have an annual CGT allowance, and any gains realised below this threshold are tax-free.

For a deeper dive into these financial responsibilities, our guide can help you fully understand property taxes for investors.

Reducing Your Tax Bill Legally

Prudent investors minimise their tax liability by claiming all allowable expenses. These are costs incurred 'wholly and exclusively' for the purpose of letting the property.

Common allowable expenses include:

- Letting agent and management fees: Costs for professional tenant-finding and property management services.

- Maintenance and repairs: Costs for maintaining the property (e.g., fixing a leak), but not for capital improvements (e.g., building an extension).

- Landlord insurance: Premiums for buildings, contents, and public liability cover.

- Accountancy fees: Costs for professional financial and tax advisory services.

- Direct costs: Ground rent, service charges, and utility bills paid by the landlord.

Maintaining detailed records and receipts for every expense is non-negotiable. This documentation serves as evidence for your tax return and is vital in the event of an enquiry from HMRC.

Your Legal Duties as a Landlord

Beyond taxation, you have a legal duty of care to your tenants. Non-compliance can result in substantial fines or legal action, making these responsibilities a top priority.

Key legal obligations include:

- Gas Safety: An annual inspection of all gas appliances by a Gas Safe registered engineer, with a copy of the certificate provided to the tenant.

- Electrical Safety: An Electrical Installation Condition Report (EICR) conducted by a qualified electrician at least every five years.

- Energy Performance Certificate (EPC): The property must have an EPC rating of 'E' or higher to be legally let. A copy must be given to tenants.

- Tenancy Deposit Protection: Tenant deposits must be protected in a government-approved scheme within 30 days of receipt.

By mastering these tax and legal fundamentals from the start, you build your property investment business on a solid, sustainable, and profitable foundation.

Managing Risk and Growing Your Portfolio

Successful property investing is not about avoiding risk, but managing it intelligently. For a beginner, understanding potential challenges from the outset is what differentiates a sustainable, growing portfolio from a high-stress liability.

Common operational risks include periods without a tenant ('void' periods), unexpected repair costs, and rent arrears. A strategic investor plans for these eventualities rather than hoping they do not occur.

Building Your Financial Defence

A robust financial buffer is your primary defence against unforeseen costs. It is non-negotiable. Prudent investors maintain a separate contingency fund, ring-fenced from personal savings, specifically for their property portfolio.

This fund should cover a minimum of three to six months of all property-related outgoings, including mortgage payments. It functions as a crucial buffer for your cash flow. If a boiler fails or a tenant departs unexpectedly, this reserve allows you to manage the situation without financial distress, protecting both your investment and your credit rating.

Furthermore, comprehensive landlord insurance is essential. A good policy covers more than just the building itself; it can include loss of rent and legal expenses, providing a vital safety net.

From One Property to a Portfolio

Once your first investment is operating smoothly and your risk management strategy is in place, the next logical step is growth. Scaling from a single property to a portfolio requires a shift in mindset—from managing a single asset to balancing multiple income streams and risks.

Diversification is the cornerstone of this phase. Just as a prudent equity investor would not allocate all their capital to a single stock, relying on one property in one location creates concentrated risk.

A common error for new investors is to buy only in familiar locations. While local knowledge provides comfort, a strategic portfolio is built on data. Diversifying across different regions and property types mitigates risk and allows you to capitalise on growth wherever it occurs.

The Power of Regional Diversification

Expanding your portfolio across different parts of the UK can protect against localised market downturns and unlock new opportunities. For instance, if the rental market in one city softens, strong performance in another can balance your overall returns.

Official data from the Office for National Statistics (ONS) demonstrates how significantly performance can vary by region. In a recent 12-month period, average private rents rose across the UK, but at different rates:

- England reached an average of £1,410 (a 5.5% increase)

- Wales reached £815 (a 7.1% increase)

- Scotland saw rents climb to £1,004 (a 3.4% increase)

This rental growth occurred alongside a 3.0% overall rise in UK house prices, as reported by Gov.uk, showing how rental income and capital gains can work in tandem. You can explore further detail by reviewing the UK private rent and house price trends on ONS.gov.uk.

This data underscores why looking beyond your local area is so critical. A strategic investor might hold a high-yielding flat in a northern city while also owning a house in a southern commuter town poised for long-term capital growth. This balanced approach creates a more resilient and profitable portfolio over time.

Common Questions from New Property Investors

Entering the property investment market invariably raises several key questions. Obtaining clear, practical answers from the outset facilitates confident action and avoids analysis paralysis. Here are the most common queries from new investors, answered concisely.

How Much Money Do I Realistically Need to Start?

This varies by market, but a sound budget should account for a 25% deposit for a buy-to-let mortgage. For a £200,000 property, this equates to a £50,000 deposit.

This figure, however, does not represent the total initial capital required. You must also budget for acquisition costs, including Stamp Duty Land Tax, legal fees, and surveys, which typically amount to an additional 3-5% of the purchase price. Furthermore, prudent investors maintain a separate cash reserve—equivalent to three to six months of mortgage payments and running costs—to manage unforeseen expenses.

Should I Use a Letting Agent or Manage It Myself?

This decision involves a trade-off between your time, expertise, and proximity to the investment property.

Self-management can save the 10-15% of monthly rent typically charged by agents, but the workload should not be underestimated. You become responsible for tenant screening, handling maintenance calls at all hours, and ensuring compliance with evolving legislation. It is a significant commitment.

For most beginners, particularly those investing from a distance, a reputable letting agent is an invaluable asset. They manage the day-to-day operations, professionalise the tenancy process, and ensure legal compliance, freeing you to focus on strategic activities, such as identifying your next investment.

Is a New-Build or an Older Property a Better Investment?

Neither option is inherently superior; the optimal choice depends on your investment strategy. Each has distinct advantages.

-

New-Build Properties: These typically attract high-quality tenants and have fewer initial maintenance issues and better energy efficiency. The disadvantage is that you often pay a price premium, which can limit immediate capital growth and leave little scope for adding value through refurbishment.

-

Older Properties: These can offer better value in established locations and provide the opportunity to "force appreciation" through renovation. The trade-off is the higher risk of maintenance costs, which must be factored into your financial forecasts.

Your choice should reflect your goals. If you seek a hands-off, income-focused asset, a new-build may be suitable. If you are looking for a project to actively add value, an older property is likely the more strategic choice.

At World Property Investor, we provide the data-driven guides and market analysis you need to compare international markets and invest with confidence. Explore our expert insights at https://www.worldpropertyinvestor.com.