To successfully buy an investment property, you must begin with a clear, data-driven strategy. This process is about more than browsing property listings; it is about aligning your financial objectives—whether capital growth, steady rental income, or portfolio diversification—with the right market and asset class.

This is a significant financial commitment. A structured, analytical approach from the outset is non-negotiable for long-term success.

Building Your Property Investment Strategy

Investing in property has been a proven path to long-term wealth creation, but success is rarely accidental. It hinges on creating a robust strategy that aligns with your financial position and investment objectives.

Before engaging an estate agent, you must define your criteria for success. A well-defined strategy acts as your roadmap, guiding every decision, from market selection to financing structure. This planning phase is crucial, whether you are a first-time buyer or a seasoned global investor expanding your portfolio.

To provide a foundational understanding of how different properties perform, here is a comparison of primary investment types.

Quick Comparison: Key Investment Property Types

| Property Type | Potential Rental Yield | Capital Growth Prospect | Typical Management Effort |

|---|---|---|---|

| Residential Buy-to-Let | 4-7% | Moderate to High | Low to Medium |

| HMO (House in Multiple Occupation) | 8-12%+ | Moderate | High |

| Holiday Let / Short-Term Rental | 5-10%+ (Seasonal) | High | High |

| Commercial Property | 6-8% | Low to Moderate | Low (with long leases) |

This table illustrates the trade-offs. An HMO may offer superior yields but requires significantly more management than a standard buy-to-let. Understanding these distinctions is the first step in building a strategy that meets your specific requirements.

Defining Your Core Objectives

First, what is the primary goal? Are you targeting rapid capital appreciation by investing in emerging locations? Is the main objective a consistent rental income to supplement your earnings? Or are you focused on diversification, spreading risk across different geographical markets?

To achieve focus, consider these fundamental goals:

- Capital Growth: This strategy involves targeting neighbourhoods with planned infrastructure projects or regeneration schemes where property values are projected to rise significantly over the long term. An example would be investing along a new high-speed rail corridor.

- Rental Yield: Here, you would target properties in locations with strong, consistent tenant demand—such as university cities or central business districts—to maximise annual rental returns. Manchester, with its large student population, is a classic example.

- A Balanced Portfolio: This approach combines both growth and yield strategies. For instance, you might acquire a stable, high-yield property in an established market alongside a higher-risk, high-growth asset in an emerging market.

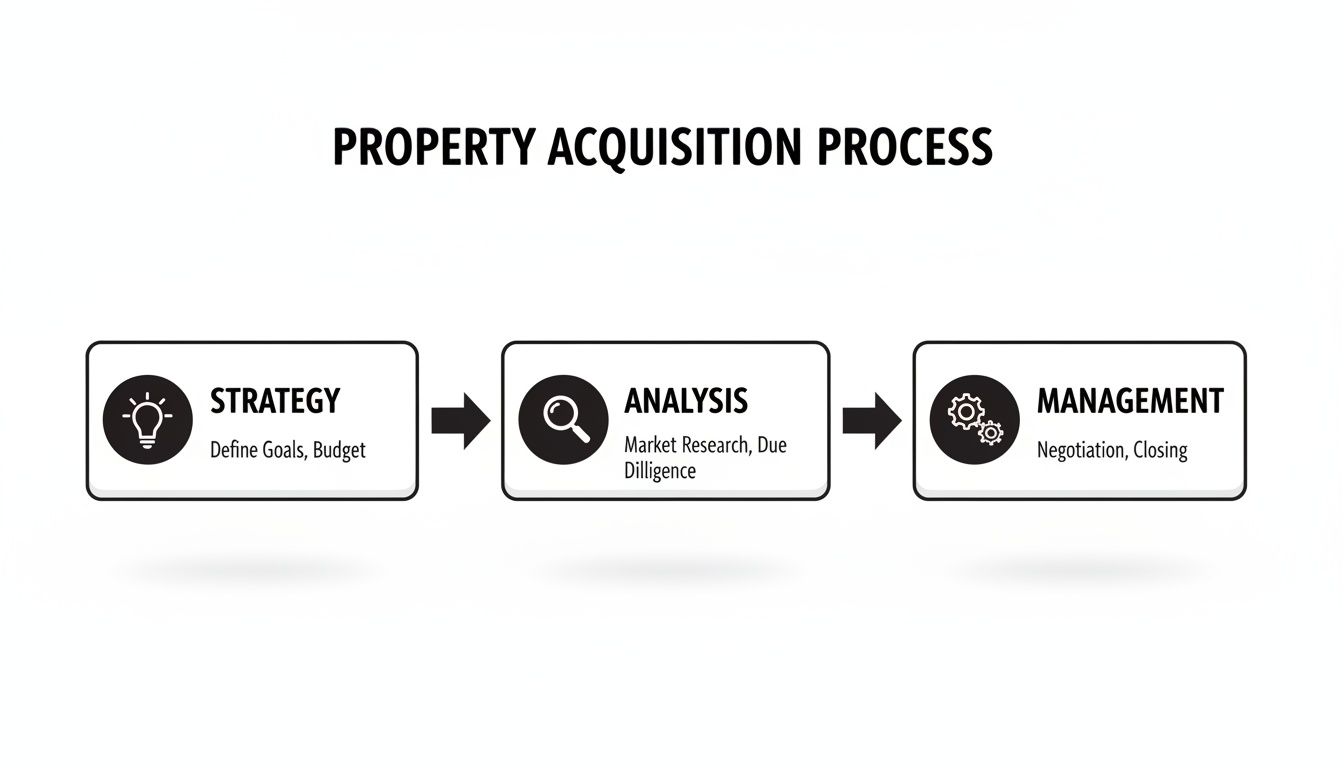

Clarity on these objectives makes your property search efficient and targeted. The following visual breaks down the core stages of a successful property acquisition.

As the flowchart demonstrates, a sound strategy underpins the entire process, leading to diligent analysis and, ultimately, effective long-term management. For any investor, understanding how these stages connect is the first step toward making a sound purchase.

For a deeper analysis of different investment approaches, explore our comprehensive guides on property investment.

Finding and Analysing Profitable Property Markets

Once your strategy is defined, the work of identifying a suitable market begins. Correct location selection can drive returns for years. An incorrect choice can lead to stagnant growth and persistent management challenges.

Successful investors do not rely on intuition or media hype. They analyse data, combining a macroeconomic overview with micro-level, localised understanding to build a robust investment case for a specific city or neighbourhood.

The Macro View: Understanding Economic Drivers

Before considering specific postcodes, you must assess the economic health of the wider city or region. A strong, growing economy is the engine that drives both property appreciation and rental demand.

Key indicators to examine include:

- GDP and Employment Growth: A thriving economy creates jobs, attracting new residents who require housing. Look for cities with a diverse employment base—a mix of technology, healthcare, education, and logistics is more resilient than a town reliant on a single industry.

- Population Trends: Is the city's population growing or declining? Official data from sources like the ONS in the UK can reveal migration patterns. A city attracting young professionals and skilled talent is a positive signal.

- Infrastructure Investment: Major infrastructure projects signal future growth. New rail links, expanded airports, or significant regeneration schemes can transform an area's appeal, often unlocking value in previously overlooked locations.

Established Hubs vs Emerging Markets

Your strategy will determine whether you target an established hub or an emerging market. An established city like London offers stability, a proven rental market, and relatively low risk. Its global status and diverse economy provide a deep, reliable tenant pool. The trade-off is that yields may be compressed and capital growth more moderate.

Conversely, an emerging market can offer higher growth potential. These are often areas benefiting from regeneration, new transport links, or inward investment. For example, cities in Poland have attracted significant foreign investment, offering lower entry prices and strong rental yields. The risks are higher, but so are the potential rewards. For a deeper dive, review our guide on the top emerging property investment markets.

Takeaway: A common portfolio strategy involves balancing risk. Anchor a portfolio with a stable asset in an established market, then allocate a smaller portion of capital to a higher-growth emerging area to enhance overall returns.

The Micro Analysis: Analysing Local Fundamentals

Once you have identified a promising city, it is time to drill down to specific neighbourhoods. This is where you uncover true value. Key factors to analyse at a micro-level include:

- Transport Links: Proximity to a train station or major motorway is a significant advantage for most tenants.

- Local Amenities: Good schools are a key driver for family renters, increasing demand and values. Parks, shops, and leisure facilities all contribute to an area’s desirability.

- Local Demographics: Understand the local population. A neighbourhood of young professionals will demand different property types to one popular with students or families. Match your asset to the local demographic.

Calculating Your Potential Returns

To compare properties objectively, you must be comfortable with two key metrics: rental yield and Return on Investment (ROI).

Rental yield is a simple measure of a property's income potential. It is the annual rental income expressed as a percentage of the property’s value. For example, a £250,000 property generating £15,000 in annual rent has a gross yield of 6%.

ROI, however, is a more comprehensive metric. It provides a true picture of the return on your invested capital by accounting for all acquisition costs—the deposit, stamp duty, legal fees, and any refurbishment expenditure.

House prices across the UK have demonstrated steady long-term appreciation. According to the Office for National Statistics (ONS), average UK house prices showed consistent growth trends over the past decade. While short-term fluctuations occur, major property consultancies project cumulative growth in the coming five-year period, with certain regions expected to outperform, signalling robust capital appreciation potential. Explore more on these trends with the latest ONS house price index data.

Securing Finance for Your Investment Property

Arranging finance is often a primary challenge when buying an investment property, particularly for international buyers. A sound financing strategy shapes your returns for years to come. The first step is to understand your options to structure a deal that aligns with your objectives.

For most investors, the standard product is a buy-to-let (BTL) mortgage. This is a loan designed for properties intended for rental. The crucial difference from a standard residential mortgage is that lenders assess the application based on the property’s potential rental income, not solely on your personal salary.

Be prepared for stricter lending criteria. Lenders will almost always require a larger deposit, typically between 25% and 40% of the property’s value. This higher equity stake lowers their risk, a standard practice in established markets like the UK, Australia, and Canada.

Understanding Key Lending Metrics

To engage effectively with a lender, you must understand their terminology. Two of the most important metrics are the Loan-to-Value (LTV) ratio and the Interest Coverage Ratio (ICR).

The Loan-to-Value (LTV) ratio is the size of your mortgage as a percentage of the property’s value. If you buy a £200,000 property with a £50,000 deposit, your loan is £150,000, giving you an LTV of 75%. Generally, a lower LTV provides access to more favourable interest rates.

The Interest Coverage Ratio (ICR) is a stress test. Lenders use it to ensure the property's rental income can comfortably cover the mortgage interest payments. They typically require the monthly rent to be 125% to 145% of the monthly mortgage payment, calculated using a higher notional "stress" interest rate. This provides a buffer against rising rates or void periods.

Practical Example:

A property generates £1,000 per month in rent. A lender with a 125% ICR requires your monthly mortgage interest payment to be no more than £800 (£1,000 / 1.25). This calculation is central to their lending decision.

Financing Challenges for International Investors

If you are buying from overseas, expect additional scrutiny. Lenders may perceive non-resident investors as higher risk due to difficulties in verifying foreign income and credit histories. Consequently, you will likely face higher interest rates and be required to provide a larger deposit.

Securing a mortgage in principle (MIP) or pre-approval before making offers is a powerful step. It demonstrates to sellers and estate agents that you are a credible buyer with financing arranged, providing a significant advantage in a competitive market.

For a more detailed look at lender requirements, our guide offers a full breakdown on financing an investment property.

Structuring Your Purchase: Individual vs Limited Company

A crucial decision is whether to purchase the property in your personal name or through a limited company, often a Special Purpose Vehicle (SPV). This choice has significant tax and legal implications.

- Individual Ownership: This is the simpler administrative route. However, in the UK, tax relief on mortgage interest for individual landlords is restricted, which can significantly reduce profitability for higher-rate taxpayers.

- Limited Company (SPV) Ownership: Buying through an SPV allows you to deduct 100% of mortgage interest as a business expense before corporation tax is calculated. This is a significant tax efficiency. It also provides limited liability, separating your personal assets from your investment portfolio.

While establishing and managing an SPV involves more administration and potentially higher mortgage rates, the long-term tax benefits often make it the optimal structure for serious investors building a portfolio. Professional tax advice is essential to determine the right structure for your circumstances.

Navigating Legal and Tax Obligations

Once you move from market analysis to acquisition, the legal and tax aspects become paramount. While not the most glamorous part of investing, errors here can turn a profitable deal into a costly liability. For anyone looking to buy an investment property, especially across borders, a firm grasp of your obligations is essential.

This domain is best approached by separating it into two parts: the legal process and your tax strategy. Engaging qualified local professionals—a solicitor and a tax advisor—is not a suggestion; it is a fundamental step to protect your investment.

The Essential Legal Process

Your first step should be to appoint a reputable solicitor or conveyancer with expertise in investment property. Their role is to conduct legal due diligence, confirming the property is a legitimate and unencumbered purchase. This is a corner you must never cut.

Their responsibilities include:

- Title Searches: Verifying the seller has the legal right to sell the property and checking for any hidden claims or debts registered against it.

- Contract Review: Scrutinising the purchase agreement to protect your interests, clarify legal terminology, and flag any unusual clauses.

- Local Authority Searches: Checking for planning permissions, building regulations, or local land charges that could impact the property's value or your future plans for it.

The process varies significantly by jurisdiction. In the UK, the "exchange of contracts" makes the deal legally binding, with completion occurring later. Other countries may use a notary system where the entire transaction is finalised in a single meeting. Understanding these differences is vital.

Foreign Ownership Restrictions

When investing internationally, you must investigate local rules on foreign ownership. Some countries, such as the UK and Portugal, are very open to overseas investors. Others, like Switzerland or parts of Thailand, have strict restrictions.

Investor Pitfall: A common error is underestimating the complexities of leasehold property. In England, a leasehold purchase means you own the building for a fixed term, but not the land it stands on. Failing to check the remaining lease term or underestimating ground rent and service charges is an expensive mistake.

Understanding Your Tax Obligations

A robust tax plan is as important as finding the right property. The taxes you pay directly impact your net returns, so they must be factored in from the start. While specifics vary, you will generally encounter a similar set of taxes.

Property investors typically face three main types of tax:

- Transactional Taxes: Paid upon purchase. In the UK, this is Stamp Duty Land Tax (SDLT), tiered by value with a surcharge for additional properties.

- Ongoing Taxes: Income tax paid on your net rental profit (rental income minus allowable expenses).

- Capital Gains Tax (CGT): Tax paid on the profit realised when you sell the property.

Getting this wrong can lead to significant financial penalties. A professional tax advisor can provide a detailed breakdown of how these taxes apply to your situation.

The UK market exemplifies a liquid, though highly regulated, environment. According to industry data, new property listings and sales transactions show consistent activity, indicating a market where investors can enter and exit with confidence. Find more details on the UK's active property market here.

For international investors, double taxation is a key concern. Fortunately, many countries have Double Taxation Treaties (DTTs) to prevent income being taxed in both your home country and the investment country. A tax advisor can explain how the relevant treaty applies to you, ensuring you meet your legal obligations efficiently. This planning is fundamental to building a global property portfolio.

Mastering Due Diligence and Negotiation

You have completed your market analysis, arranged financing, and identified a promising property. The next phase, due diligence, is what separates a calculated, profitable investment from an expensive mistake.

This is a comprehensive investigation into the property's physical, legal, and financial condition. Skipping steps here can expose you to unforeseen repair costs, unresolved legal issues, or the realisation that the valuation is insupportable. Thorough due diligence provides the factual basis for effective negotiation.

Your Essential Due diligence Checklist

Before making a binding offer, a structured checklist is your primary risk management tool. Each item provides a piece of the puzzle, helping you build a complete picture of the asset.

Your non-negotiable checks should include:

- Commissioning a Professional Survey: A chartered surveyor can identify structural issues an untrained eye would miss, such as subsidence, damp, or roof defects. The survey fee is a small price to pay to avoid major future expenditure.

- Verifying the Legal Title: Your solicitor will confirm the seller's legal right to sell and uncover any restrictions, covenants, or charges that could limit your use of the property.

- Checking Local Planning: Review the local council’s planning portal. Is a new industrial estate planned nearby? This could negatively impact value. Conversely, a new train station could provide a significant uplift.

- Reviewing Service Charge and Lease Details: For a flat (apartment), obtain the full service charge history and scrutinise the lease. A short lease (under 80 years) is a major red flag, making the property difficult to mortgage and expensive to extend.

Arriving at an Accurate Valuation

Overpaying is a cardinal sin in property investment. The best way to avoid this is by conducting a comparative market analysis (CMA). This involves analysing recent sale prices of genuinely similar properties in the immediate vicinity—compare size, condition, and exact location.

Your goal is to build a valuation supported by hard data, independent of the seller's asking price. This evidence is invaluable during negotiation. It is also crucial to determine a property's investment potential beyond the purchase price to understand the full financial picture.

Rental yields remain a cornerstone of UK property investment. According to ONS data, average UK private rents have shown consistent year-on-year growth, highlighting the reliability of UK property as an income-generating asset.

The Art of Strategic Negotiation

With your due diligence complete, you are negotiating from a position of strength. Your opening offer should be confident and justified by your research, while leaving room for manoeuvre. Never lead with your final price.

Takeaway: Negotiation is a dialogue, not a conflict. The objective is to reach a mutually agreeable price. A successful outcome secures the property on favourable terms while maintaining a professional relationship.

Consider a real-world scenario: your survey reveals the property requires a new roof at an estimated cost of £10,000. This is not a problem; it is a powerful negotiating tool. You can present the relevant section of the surveyor's report to the agent and revise your offer downwards, demonstrating your new price is based on facts, not arbitrary haggling.

If you enter a competitive bidding situation, remain objective. Set your maximum price based on your return calculations and be prepared to adhere to it. The most prudent move is sometimes to walk away from an overpriced deal.

Managing Your Property for Long-Term Success

Acquiring the keys to your new investment property is a milestone, but it marks the beginning of the journey, not the end. Subsequent effective management is what transforms a physical asset into a profitable, passive investment.

Your management approach will directly influence cash flow, protect the property's long-term value, and determine your own time commitment. The fundamental choice is whether to self-manage or to engage a professional letting agent.

Self-Management vs. Professional Letting Agents

The DIY route can be appealing for maximising net income by avoiding agency fees. It provides full control over tenant selection and repairs. However, this control is accompanied by significant legal and practical responsibilities.

If you are considering this path, a thorough understanding of your legal obligations as a landlord is non-negotiable. In the UK, for example, this includes:

- Deposit Protection: You are legally required to protect the tenant's deposit in a government-approved scheme.

- Safety Certificates: You must ensure the property has a valid Gas Safety Certificate, an Electrical Installation Condition Report (EICR), and an Energy Performance Certificate (EPC).

- Right to Rent Checks: You have a duty to verify that every tenant has the legal right to rent in the UK, as mandated by the Home Office.

This is where a professional letting agent adds value. They manage these complexities, making them the default choice for most international investors or those with limited time. A good agent acts as a buffer between you and the tenant, managing day-to-day issues and ensuring legal compliance.

Takeaway: A good letting agent does more than collect rent. They are your on-the-ground asset manager, tasked with protecting your investment, minimising void periods, and resolving issues before they escalate.

What to Expect from a Letting Agent

When you buy an investment property as a remote landlord, the quality of your letting agent is paramount. Their services typically come in two forms: a basic ‘tenant-find’ service or a comprehensive ‘full management’ package.

For most serious investors, full management is the logical choice. It typically includes:

- Tenant Sourcing and Vetting: Marketing the property, conducting viewings, and carrying out thorough background checks on applicants.

- Rent Collection: Ensuring timely rent payment and professionally managing any arrears.

- Maintenance and Repairs: Coordinating with trusted local contractors for all maintenance, from minor repairs to emergency call-outs.

- Inspections and Compliance: Conducting regular property inspections and ensuring all safety certificates and legal paperwork remain current.

Fees for full management usually range between 10% and 15% of the monthly rent. While this is a notable expense, the professional oversight and peace of mind it provides can be invaluable, especially when the goal is long-term, passive income.

Frequently Asked Questions

Entering the world of property investment, particularly on a global scale, raises practical questions where strategy meets real-world application. This section addresses common queries from investors to provide clarity.

How Much Deposit is Required for a Buy-to-Let Mortgage?

For a standard buy-to-let mortgage in an established market like the UK, lenders require a larger deposit than for a primary residence. You should expect to provide between 25% and 40% of the property's value.

For international investors, these requirements can be stricter, as some lenders perceive overseas buyers as higher risk. It is advisable to confirm specific criteria with lenders in your target country early in your planning.

Should I Buy with Cash or Use a Mortgage?

This is a strategic decision with significant trade-offs. Using a mortgage provides leverage, allowing you to control a more valuable asset with a smaller capital outlay. This can amplify your returns (but also amplifies risk).

A cash purchase means you have no mortgage costs, maximising monthly profit. It also makes you an attractive buyer, strengthening your negotiating position. The downside is that it ties up a large amount of capital in a single asset, limiting your ability to diversify.

Takeaway: There is no single correct answer. The choice depends on your risk tolerance and objectives. Leverage can help you build a portfolio faster, while a cash purchase provides maximum security and cash flow from day one.

What Are the Primary Risks of Investing Abroad?

Investing outside your home country opens up significant opportunities but also introduces unique risks that require careful management. The main risks to monitor are:

- Currency Fluctuations: Significant movements in exchange rates can impact your rental income and capital gains when converted back to your home currency.

- Unfamiliar Legal and Tax Systems: Every country has its own property laws and tax regulations. Navigating these without expert local advice is a recipe for costly errors.

- Remote Management: The practicalities of managing a property from a distance can be challenging. A reliable local letting agent is not a luxury—it is an essential requirement.

- Market Stability: You must be comfortable with the political and economic climate of the investment country. Instability can negatively affect property values and tenant demand.

Is It Better to Invest Through a Limited Company?

This has become a popular strategy, particularly for investors in jurisdictions like the UK. Purchasing property through a limited company (an SPV) can be highly tax-efficient. The primary advantage is that the company can offset 100% of the mortgage interest against rental income before paying corporation tax.

An SPV also provides limited liability protection, keeping your personal assets separate from your property portfolio. The trade-offs include more administration and the possibility of higher mortgage fees and interest rates. It is vital to obtain professional tax advice to determine if this structure is suitable for your personal circumstances.

At World Property Investor, we provide the data-driven guides and market analysis you need to navigate the global property market with confidence. Explore our resources to find your next investment opportunity. Find out more at World Property Investor.