A 23 percent wage shortfall still shapes Greek housing demand. Average annual pay has recovered from its post-crisis lows, but it remains well below the 2009 peak cited earlier. For an investor, that gap matters because rents in the local market are funded by current salaries, not by the story of macro recovery.

Greek property can screen as inexpensive beside Spain, Portugal, or major UK cities. That does not automatically create rental pricing power. In long-term residential markets, tenant budgets place a hard ceiling on achievable rent, and that ceiling rises slowly when wage growth is modest and household costs absorb a large share of income.

The practical question is not just what the average worker earns. It is how that income translates into rent tolerance, renewal risk, and arrears probability at neighbourhood level. A central Athens professional can support a different rent than a household in western suburbs or a worker in a tourism-led local economy with seasonal pay. Investors who price units against foreign buyer expectations rather than local earning capacity often overestimate sustainable yield.

This is also why income data should sit alongside acquisition due diligence. If you are reviewing the process of buying a home in Greece, the wage backdrop helps you judge whether a property is suited to domestic tenants, hybrid demand, or a strategy that depends heavily on short-let income.

Average income in Greece is useful because it clarifies three things quickly. How much pricing headroom the local rental market really has. How resilient cash flow may be if household budgets come under pressure. Which locations depend on local wages, and which can outperform because demand is supported by tourism, international tenants, or higher-income professional clusters.

Understanding Greek Incomes for Property Investment

A British investor looking at Greece can easily misread the market. One source cited by ADP reports that Greece's average full-time adjusted annual salary was €16,661 in 2022, while other sources place the 2024 figure closer to €18,470. ADP's point is the important one for investors: that headline wage level sits well below UK norms and doesn't by itself answer whether local incomes can support rents in Athens, Thessaloniki, or resort markets, as noted in ADP's discussion of pay in Athens and Greece.

That's the key reframing. The phrase average income Greece only becomes useful when you connect it to who your likely tenant is. A central Athens professional, a Thessaloniki family, and a seasonal island worker don't have the same rent tolerance, income stability, or renewal behaviour.

The number matters because rents come from wages

In domestic-led rental markets, wages drive three core outcomes:

- Affordability limits determine how far rents can rise before arrears or turnover increase.

- Tenant quality often reflects income stability rather than just income level.

- Yield durability depends on whether local households can keep paying through weaker economic periods.

A lot of international buyers focus on tourism because it appears to bypass local wage constraints. Sometimes it does. But many Greek submarkets still rely heavily on residents, students, local professionals, and mixed-use neighbourhood demand. In those areas, wage trends are not background noise. They're the base layer of your investment case.

Why Greece is attractive and complicated

Greece remains compelling because it combines lifestyle appeal, international buyer interest, and a long economic recovery that still leaves room for selective repricing. But it's also a market where investors need to distinguish between capital value opportunity and income reality.

Investor lens: If local earnings remain constrained, rent growth usually follows a slower path than sale-price narratives suggest.

That's especially relevant in 2026, when many buyers are comparing mature markets with more established income levels against Southern European markets where affordability is tighter and tenant demand can be more uneven. If you're assessing where Greece fits in a cross-border portfolio, it helps to pair wage analysis with local market rules, financing conditions, and ownership practicalities. A good starting point is this guide to buying a home in Greece.

Decoding Greek Pay What Investors Need to Know

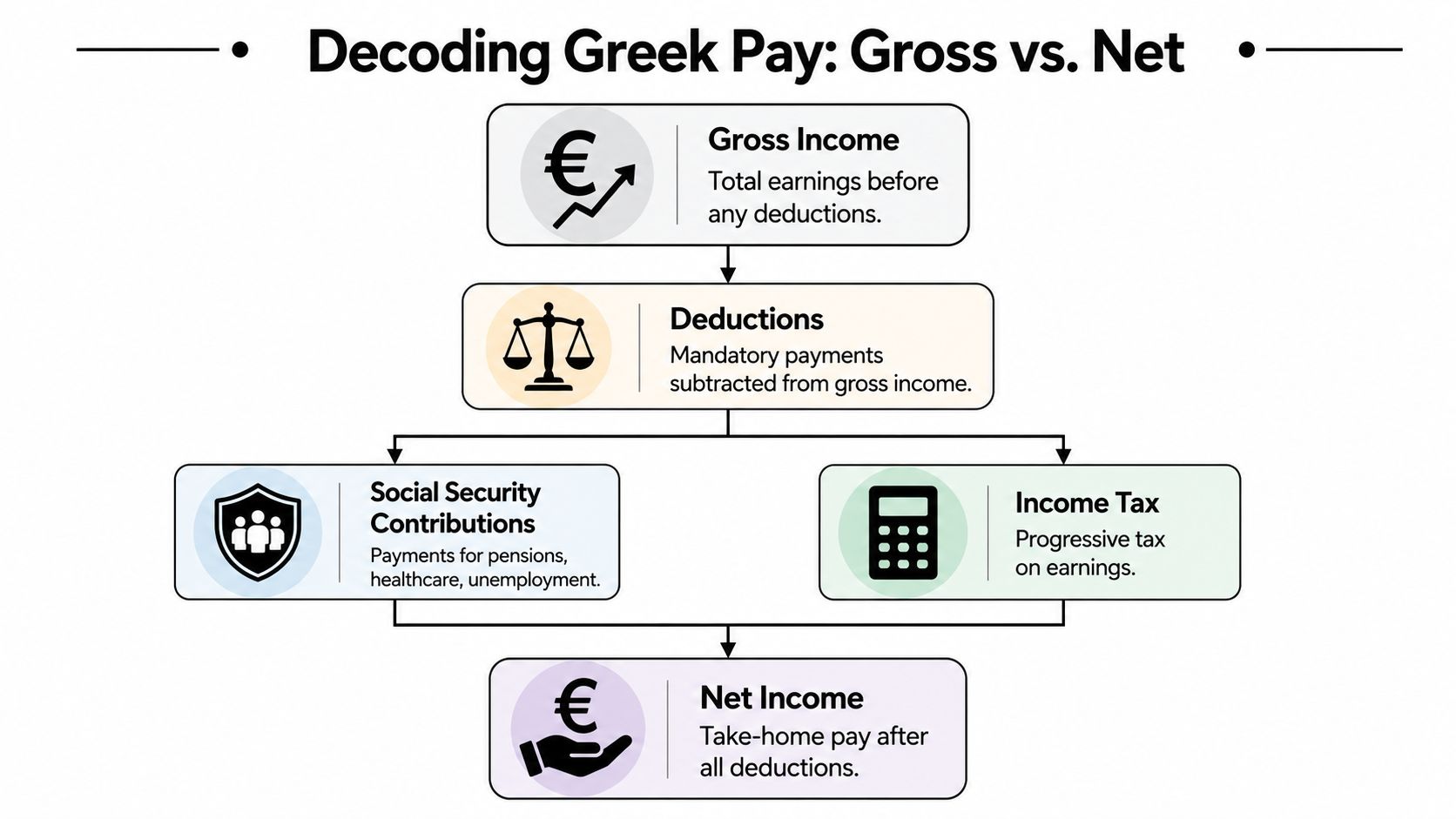

If you use income data carelessly, you'll overestimate what tenants can afford. The easiest way to avoid that is to separate four different ideas: gross income, net income, average income, and median income.

Think of salary like a pie. Gross income is the whole pie before anyone takes a slice. Net income is what's left on the plate after deductions. Average income is what you get if you add everyone's pie together and divide it equally. Median income is the pie size of the person standing in the middle of the line.

Gross versus net changes rent reality

For landlords, gross salary is not rent-paying capacity. Tenants pay rent from what arrives in their bank account, not from their pre-deduction contract figure.

That matters in Greece because even when headline salaries improve, a tenant's practical room for rent still depends on what remains after taxes, social contributions, and everyday essentials. Investors who anchor on gross pay often assume more headroom than households really have.

A better underwriting habit is simple:

- Start with take-home pay, not advertised salary.

- Stress-test rent levels against ordinary living costs.

- Assume caution, especially in markets with a large share of middle-income households.

Average versus median tells you different things

Average income is useful for macro comparisons. It helps you compare Greece with the EU, or track recovery over time. But average figures can be pulled upward by higher earners in sectors or locations that don't represent the typical tenant.

Median income is usually the more practical concept for residential lettings because it reflects the middle household rather than the mathematical mean. In plain English, median tells you what a more typical tenant can manage.

We don't have a verified median figure to cite here, so it's better to make the point qualitatively: in a market with uneven regional and sectoral earnings, the median usually gives a stricter affordability signal than the average.

A landlord buying for long-let demand should care less about what the top earners can pay and more about what the middle of the market can sustain.

A practical rule for investors

Use the headline average as a market temperature check, then narrow to the specific tenant pool your asset targets. A compact flat near business districts may appeal to professionals with steadier income. A larger unit in a local suburban market may depend on households with much tighter monthly flexibility.

If you're comparing Greece with other buy-to-let markets, this primer on what makes a good rental yield is useful because yield without affordability support can prove fragile.

Greeces Income Landscape National Averages and EU Benchmarks

The core fact about Greece is straightforward. Pay has recovered, but not enough to erase the legacy of the crisis era.

The Greek Analyst reports that the average full-time adjusted salary per employee in Greece reached €17,000 in 2023, while the EU average stood at €38,000, as outlined in The Greek Analyst's salary review. Greek average pay was therefore less than half the EU benchmark. For investors comparing European residential markets, that single gap explains a lot about affordability pressure and rent sensitivity.

What the EU gap means in practice

A lower national pay base doesn't automatically make property a bad investment. It changes the kind of investment Greece is.

In higher-income EU markets, landlords may have more room to push rents on standard long lets because household incomes start from a stronger base. In Greece, that room is narrower. Tenants may still be reliable, and demand may still be healthy, but pricing power is usually more limited unless the property serves a niche with stronger earnings or non-local demand.

Here's the practical split:

| Market type | Income support for long-let rents | Investor implication |

|---|---|---|

| Established higher-income EU markets | Generally broader | More room for conventional rent growth assumptions |

| Greece and similar lower-income markets | More constrained | Stronger need for micro-location and tenant targeting |

That's why Greece often suits investors who are disciplined about entry price, conservative on rent growth, and selective about submarket demand drivers.

Comparing Greece with the rest of Europe

A lot of buyers compare Greece with Spain, Portugal, or other Southern European markets and assume they belong in the same investment bucket. That can be misleading. Similar climate or tourism appeal doesn't mean similar wage support.

When you compare countries, ask two questions:

- Is local income deep enough to support the long-let market without tourism?

- If not, what type of asset performs best under lower domestic purchasing power?

For professionals benchmarking European labour markets more broadly, this comprehensive guide for finance analysts is a useful comparative reference because it shows how salary expectations vary across roles and geographies. That kind of salary context helps when you're trying to assess whether a city can support premium urban rents.

The investor takeaway from national income data

Greece offers value, but it doesn't offer unlimited rent elasticity.

That's the distinction many overseas buyers miss. Lower income levels can support attractive acquisition cases, especially where pricing remains below richer EU capitals, but they also place a brake on how quickly domestic rents can move.

If you're weighing Greece against other lifestyle and relocation destinations, this overview of the best EU countries to live in helps frame the wider trade-off between affordability, quality of life, and economic depth.

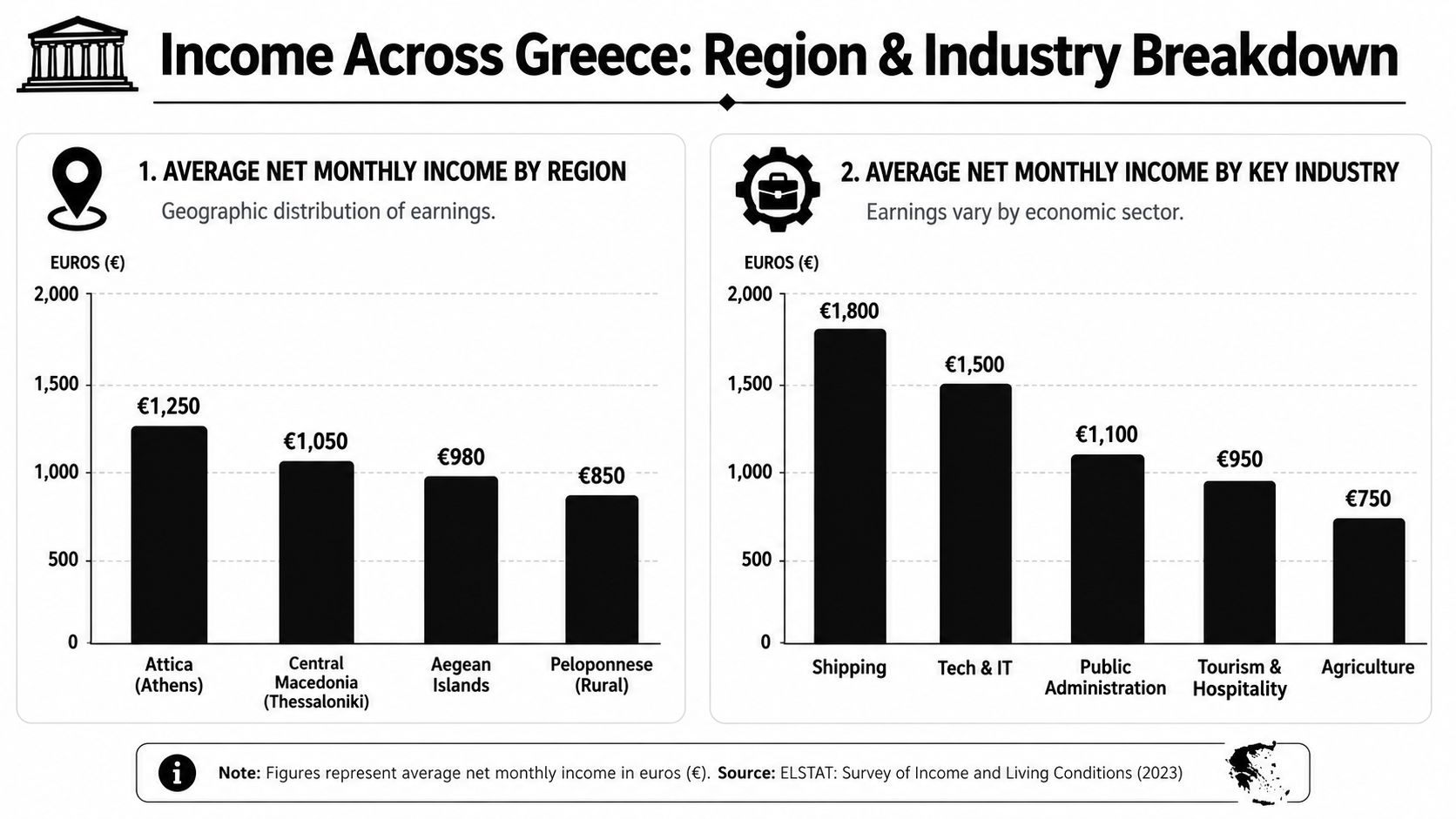

Where Is the Money Income by Region and Industry

National averages are only the starting point. In property, location decides income relevance. The tenant profile in central Athens isn't the same as the tenant profile in Thessaloniki, and neither behaves like a worker in a tourism-heavy island economy.

Regional and sector differences matter because they shape lease length, seasonality, and arrears risk. An investor buying one-bed flats for urban professionals should study a completely different demand base from someone buying a villa or small apartment in a resort-led market.

Athens and Thessaloniki are not interchangeable

Athens, especially the wider Attica area, tends to offer the broadest pool of higher-skilled employment, white-collar demand, and mixed domestic plus international tenant traffic. That usually makes it the most flexible market for long-term rentals. Not every Athens district is equal, but the city has more ways to generate demand.

Thessaloniki is different. It can still work well for investors, especially where universities, professional services, and transport links support occupancy, but tenant budgets are often tighter and rent ceilings can be lower. In practice, that means pricing discipline matters more.

A simple comparison helps:

- Athens often suits smaller, well-located units aimed at professionals, students, and expats.

- Thessaloniki can reward value-driven acquisitions where rent is realistic and operating costs are controlled.

- Tourist islands may offer stronger seasonal upside but weaker annual income consistency.

Industry matters as much as postcode

The source material around Greek incomes repeatedly points to labour-market structure as a core issue. Pay varies with sector concentration, part-time work, and the weight of tourism and services in the economy. For an investor, that means the same apartment can have very different tenant risk depending on who rents it.

A tenant employed in tech, shipping, or a stable professional role may offer predictable payment patterns. A tenant tied to seasonal hospitality work may deliver strong income during parts of the year and much thinner resilience outside peak periods.

This distinction is easier to see in local market selection than in national statistics.

The regional picture becomes clearer when you visualise it. This video gives helpful local context on how Greek areas differ in character and appeal.

The regional investment lens

Use income geography to match asset type to demand source.

- Urban long lets work best where year-round employment is diverse.

- Family housing needs neighbourhoods where incomes are stable enough for renewal, not just initial occupancy.

- Holiday-led stock requires a separate underwriting model because domestic wages may be less relevant than visitor demand.

The best Greek property strategy isn't “buy where prices look cheap”. It's “buy where the local income base matches the rental model”.

That's why established urban districts and emerging secondary areas shouldn't be judged by the same template. One may offer stability; the other may offer upside, but only with a different risk tolerance.

The Real-World Impact on Disposable Income

Nominal wage growth helps, but landlords don't collect rent from nominal growth. They collect it from disposable income.

Trading Economics reports that average annual wages rose to an estimated $32,257 in 2024 from $31,597.68 in 2023, as shown in Trading Economics' Greece wage data. The investment question isn't whether wages rose. It's whether households felt materially less strained after paying for housing, food, and energy.

Why disposable income is the real rental metric

For long-let investors, the most useful affordability test is brutally simple. After essential spending, does the tenant still have enough margin to pay rent on time and absorb small shocks?

If the answer is tight, three things usually follow:

- Rent increases face resistance sooner than foreign buyers expect.

- Tenant turnover can rise if households search for cheaper options.

- Arrears risk becomes more cyclical, even if employment remains intact.

Average income in Greece needs interpretation rather than repetition. A rising wage line can coexist with a household sector that still feels constrained.

Affordability pressure changes landlord behaviour

Investors often treat Greece as a low-cost market and assume that lower entry prices automatically produce better landlord economics. That's incomplete. Lower acquisition costs can help, but rent collection still depends on tenant cash flow.

A more grounded approach is to underwrite with conservative assumptions:

| Investor question | Conservative answer |

|---|---|

| Can tenants absorb aggressive annual rent rises? | Often not without stronger local income support |

| Are prime urban pockets insulated? | Sometimes, but only where tenant demand is deeper |

| Do lower costs eliminate affordability risk? | No. Affordability is about income left after essentials |

That's why local taxation, ownership costs, and compliance matter as much as wages. If you're modelling net returns, this guide to taxation in Greece helps frame what reaches your bottom line.

Domestic demand resilience is the hidden variable

Practical rule: In a lower-income market, stability often beats ambition. A rent that renews is better than a rent that only looks good at listing stage.

Investors focused on domestic tenants should therefore treat disposable income as the main risk control. If a submarket depends on households with thin monthly flexibility, pricing should be modest, tenant screening should be tighter, and void assumptions should be more cautious.

In contrast, if a property sits in a location supported by professional demand, education hubs, or international occupiers, the rent may have more resilience. But that resilience comes from tenant mix, not from the national average alone.

What Greek Incomes Mean for Your Property Strategy

Income growth in Greece has improved the backdrop for housing demand, but the investment implication is narrower than many buyers assume. For a landlord, the question is not whether wages are rising in absolute terms. It is whether a specific tenant base in a specific submarket can support rent, renew reliably, and absorb normal cost increases without arrears.

As noted earlier, average pay has recovered only gradually from pre-crisis levels. That matters because slow wage repair usually produces selective pricing power, not broad pricing power. In practice, this means landlords can often raise rents in supply-constrained micro-locations, near employment hubs, or in neighbourhoods with stronger professional demand. Outside those pockets, asking rents that stretch beyond local budgets tend to show up later as longer voids, more negotiation, or weaker tenant retention.

What that means for asset selection

Properties that match the middle of the market usually offer the clearest risk-adjusted case.

That often includes:

- Smaller urban apartments with monthly rents that sit within ordinary household budgets

- Units near transport, universities, or office districts where demand is recurring rather than speculative

- Layouts that suit more than one tenant profile, such as young professionals, couples, or students sharing space

The logic is simple. In a market where income growth is real but constrained, broad usability matters more than aspirational positioning. A flat that can be leased to several tenant groups gives you more protection if one slice of demand softens.

Larger homes and premium stock can still perform well. They just depend on a narrower occupier pool, which raises reletting risk if the local income base is not deep enough.

Pricing power depends on tenant mix

Investors often treat Greece as a yield story first and an affordability story second. The order should usually be reversed.

Rent growth is easier to defend where at least one support exists:

- Tenants earn above the local norm

- Demand is supported by international, corporate, or education-linked occupiers

- Competing rental supply is limited at the same price point

If those supports are absent, headline yield can be misleading. A high initial rent only works if it is collectible and repeatable. For long-let buyers, the practical rules around tenant demand, lease structure, and operating realities in renting houses in Greece are directly relevant to underwriting.

Strategy should reflect investor type

Greek income data is most useful when it shapes the style of deal you pursue.

An income-sensitive, cash-flow-focused buyer will usually prefer liquid urban stock with steady domestic demand. A more cyclical investor may accept narrower affordability if the asset has a clear tourism or repositioning angle. The right choice depends less on the national average and more on whether your strategy depends on local salaries, external demand, or a mix of both. PadPulse's investor analysis is a useful reference point because it separates these approaches in a way that fits Greece well.

The broader conclusion is straightforward. Greece rewards investors who price for what tenants can sustain, not for what a listing portal suggests should be possible.

Key Takeaways for Global Investors

The phrase average income Greece is useful only if you treat it as an investment signal, not trivia. Income data tells you where rent growth may stall, where tenant quality may hold up, and which locations can support a conventional long-let strategy.

The best way to use it is as a filter for risk.

- Focus on affordability, not headlines. Wage growth has improved the backdrop, but domestic rent ceilings still depend on what households can pay after essentials.

- Match property type to income profile. Smaller, flexible units in stronger urban locations usually align better with constrained local budgets than oversized or highly aspirational stock.

- Separate tourism demand from local demand. A resort market can perform well, but it should be analysed differently from an Athens or Thessaloniki long-let purchase.

- Assume gradualism. Greece's wage recovery supports a constructive long-term view, but not a reckless rent-growth thesis.

Investors who think carefully about their own style tend to make better location choices. For a useful framework on how different buyer profiles approach deals, PadPulse's investor analysis is worth reading because it helps clarify whether you're buying for stability, yield, value-add, or cyclical upside.

Greece can work very well in a global portfolio. It just works best for investors who respect the limits that local incomes place on rental ambition.

If you're comparing Greece with other international markets, World Property Investor offers in-depth country guides, rental yield analysis, tax breakdowns, and practical buying advice to help you assess where the numbers support the story, and where they don't.