The best investment property is not a specific type of building or a location on a map. It is the one that is precisely aligned with your financial goals, risk tolerance, and personal ambitions.

It could be a high-yield flat in Manchester generating monthly cash flow, or a coastal villa in the Algarve that you use for holidays while it appreciates in value. The 'best' property is a strategic choice, not a universal answer.

Aligning Your Goals With the Right Property Strategy

Before reviewing property listings, the most critical step is to define what 'best' means for you. Property investment is not a one-size-fits-all endeavour. Your personal objectives will ultimately steer you towards the right market, property type, and investment strategy.

Are you seeking immediate monthly income to supplement your salary, or are you playing a longer game, content to wait for the property's value to increase over time?

The answer to that question is the bedrock of your investment journey. Each path comes with its own set of returns, risks, and management demands.

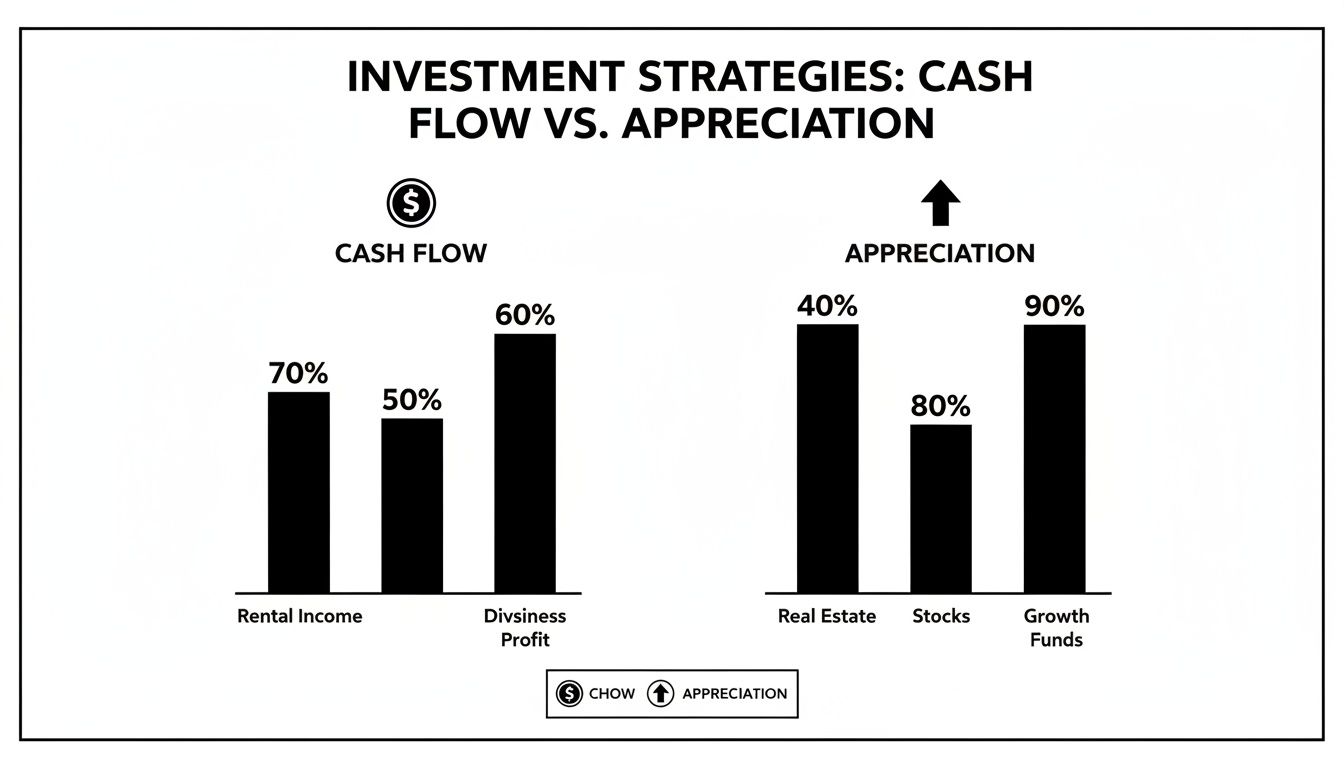

Cash Flow Versus Capital Growth

In property investment, most objectives fall into two core pillars: generating rental income (cash flow) or relying on the property’s value increasing over time (capital appreciation).

A property optimised for cash flow is typically found in markets with strong rental demand and more accessible purchase prices. Consider a two-bedroom flat in a regional UK city like Liverpool or Glasgow, where it is not uncommon to find gross rental yields exceeding 7%. This strategy delivers a steady, predictable income stream, making it well-suited for investors looking to supplement their income or fund retirement.

Conversely, a strategy focused on capital growth might lead you to a different type of asset. You might target a property in an area with major infrastructure projects planned, or a prime district in a global city. The initial rental yield might be a modest 2-3%, but the real prize is the potential for the property's value to double over a decade. This is a classic long-term strategy for building wealth through equity.

Defining Your Personal and Financial Objectives

Your investment goals are deeply personal. They must reflect your financial situation, lifestyle, and what you ultimately want this asset to achieve for you. It is not just about the figures on a spreadsheet.

To clarify your aims, it is worth exploring the different essential rental property investment strategies available.

Common investor objectives include:

- Portfolio Diversification: Mitigating risk from traditional stocks and shares by adding a stable, tangible asset.

- Securing a Future Holiday Home: Buying in a location you love, such as the Algarve or Tuscany, that can generate rental income when not in use.

- Property-Linked Residency: Investigating markets that have historically offered residency permits to property investors, providing a foothold in another country.

- Hands-On vs. Passive Management: Deciding whether you want to be actively involved or prefer a hands-off investment managed by a professional firm.

Key Takeaway: A high-turnover holiday let in a tourist hotspot might offer higher returns but demands intensive management. In contrast, a long-term let to a family in a quiet suburb provides lower but far more consistent income with minimal day-to-day involvement.

For example, an investor with a higher risk tolerance and available capital might acquire an older property in an up-and-coming neighbourhood, planning a full renovation to force appreciation and boost its rental value. A more risk-averse investor, however, may prefer a new-build apartment with a rental guarantee from the developer, choosing security over the highest possible returns.

By clarifying your ambitions from the outset, you can filter out market noise and focus your search on opportunities that serve your long-term vision. This first step is, without doubt, the most important in finding the best investment property for you.

Once you have defined your investment goals, it is time to analyse potential markets. This is where the real work begins. Identifying a genuinely promising location is less about following headlines and more about delving into the data. This analytical rigour is what separates a strategic, wealth-building asset from a speculative punt.

Your focus should be on the numbers that drive long-term profit: rental yields, capital growth, and the economic fundamentals that create lasting tenant demand. It is this process that allows you to weigh up a prime, high-cost city like London against a regional powerhouse or an emerging international market.

Ultimately, property investment returns come from two main sources: immediate income and long-term appreciation.

As you can see, cash flow provides the income that makes the investment sustainable month-to-month, while appreciation builds your wealth over time. A strong investment often balances both.

Established Versus High-Growth Markets

A common decision for investors is the choice between the perceived safety of an established market and the higher potential returns of a growth area. A central London flat, for instance, is a prestigious asset in a global city, but entry costs are enormous and gross rental yields are often disappointingly low, sometimes dipping below 3-4%. Here, your strategy is almost entirely a bet on steady, long-term capital appreciation.

Now, contrast that with regional cities like Liverpool or Glasgow. It is a completely different scenario. Lower property prices mean your capital stretches much further. It is not unusual to find properties generating gross yields of 7-8% or more, delivering strong cash flow from day one. These areas are often undergoing major regeneration, which can also ignite impressive capital growth.

To provide a clearer picture, let's compare some key UK regions. The data highlights the classic trade-off between the high-cost, lower-yield southern markets and the more affordable, high-yield northern cities.

UK Regional Yield and Growth Comparison

| Region | Example Postcode | Average Gross Yield (%) | Average Property Price (£) | 3-Year Price Growth (%) |

|---|---|---|---|---|

| North East | TS1 (Middlesbrough) | 10.5 | 70,000 | 25 |

| North West | L7 (Liverpool) | 9.1 | 120,000 | 28 |

| Yorkshire | BD1 (Bradford) | 9.7 | 65,000 | 22 |

| London | SW1 (Westminster) | 3.2 | 1,250,000 | 8 |

| South East | GU1 (Guildford) | 4.1 | 550,000 | 15 |

Note: Data is illustrative and subject to market changes. Always conduct current, localised research.

As the table shows, areas in the North West of England are standout performers for investors prioritising income. Some postcodes are delivering average yields well above 10%, with strong price growth to boot. This powerful mix of high yields and capital growth is exceptionally rare and highly sought after.

Key Takeaway: A core part of your analysis is balancing the high entry costs and lower yields of prime markets against the attractive income potential and growth prospects of regional powerhouses. Neither is inherently 'better'; they simply serve different strategies.

The Key Metrics to Master

To analyse any market professionally, you must become comfortable with fundamental data. Look past glossy sales brochures and dig into the numbers that reveal a market’s true health.

Your research framework should always include:

- Gross and Net Rental Yields: Gross yield (annual rent / property price) is a quick check, but net yield is what truly matters. It is your profit after all costs are paid.

- Historical and Projected Capital Growth: Examine official house price indices from sources like the ONS or local land registries. Is growth driven by a strong economy, or is it a speculative bubble?

- Vacancy Rates: Low vacancy rates, ideally below 5%, are a clear sign of strong, consistent tenant demand. High or rising vacancy rates are a major red flag.

- Local Economic Drivers: What powers the local economy? You want to see a diverse mix of employers, university populations, major infrastructure projects, and population growth. A town reliant on a single industry is a much riskier investment.

Sourcing Reliable Data

Good analysis depends entirely on good data. Never rely solely on the sales pitch from an estate agent. Instead, build your case using official and independent sources.

Your go-to list should include:

- Government Statistics Bodies: For the UK, the Office for National Statistics (ONS) and Gov.uk provide robust, unbiased data on house prices, rental inflation, and economic trends.

- Local Housing Authorities: These are excellent for insights into local development plans, upcoming licensing rules, and population forecasts.

- Major Economic Bodies: Reports from central banks and major financial institutions give you a high-level view of a country's economic health.

- On-the-Ground Intelligence: This is crucial. Speak to local letting agents (not sales agents). They will give you the unvarnished truth on tenant demand, achievable rents, and which postcodes are genuinely popular.

By systematically gathering and examining this data, you can see past the hype and make an informed decision based on solid fundamentals. This diligent approach is essential whether you're trying to decide where to buy investment property in the UK or assessing opportunities further afield.

Mastering the Numbers to Calculate Your True Return

A property can appear attractive in a brochure or during a viewing, but if the figures do not stand up to scrutiny, it can quickly become a financial liability rather than an asset. Finding the best investment property is less about gut feeling and more about cold, hard mathematics. This is where you look past the marketing and determine if a deal genuinely has the potential to build wealth.

Learning a few key calculations is non-negotiable for any serious investor. These metrics provide a universal language for comparing properties, whether you are looking in Birmingham or Berlin. Once you know your numbers, you will have the confidence to walk away from a bad deal and act decisively on a good one.

Gross Rental Yield: The First Quick Check

Gross rental yield is the figure you will see quoted most often. It is a fast, simple way to get an initial sense of a property’s income potential by comparing its annual rent to its purchase price.

Formula: (Annual Rental Income / Property Purchase Price) x 100 = Gross Yield %

For example, a property bought for £200,000 that generates £12,000 a year in rent (£1,000 per month) has a gross rental yield of 6%. It is a useful starting point, but it's dangerously incomplete because it ignores all running costs.

Net Rental Yield: The Number That Really Matters

This is where the real analysis begins. Net yield shows you the actual profit you are making after all the property’s running costs are subtracted from the rent. It presents a much more honest picture of how the investment will perform.

To calculate this, you first need to sum your annual operating expenses. These will almost always include:

- Maintenance and Repairs: A good rule of thumb is to budget 1% of the property’s value each year, or about 5-10% of your rental income.

- Letting Agent Fees: Full management services typically cost between 8% and 15% of the monthly rent.

- Insurance: Landlord insurance is essential, covering the building, liability, and sometimes contents.

- Service Charges and Ground Rent: These are common costs for leasehold properties such as flats.

- Void Periods: Prudent investors always budget for at least one month of vacancy each year as a contingency.

Once you have a total for your annual costs, the calculation is simple.

Formula: [(Annual Rental Income – Annual Operating Costs) / Property Purchase Price] x 100 = Net Yield %

This is the true measure of a property's income-generating power. If you want a deeper dive into these numbers, our full guide on how to calculate return on investment for a property is an excellent resource.

Key Takeaway: Never make an investment decision based on gross yield alone. It is the net yield that determines your monthly cash flow and the long-term sustainability of your investment.

Today's economic climate brings this into sharp focus. For instance, recent rental inflation in the UK has created fertile ground for investors. According to the ONS, private rents surged by 9.0% in the 12 months to February 2024. For anyone considering a buy-to-let, this upward pressure directly boosts potential yields. You can learn more about the latest UK private rent and house price findings from the ONS.

Net Operating Income and Return On Investment

Closely tied to net yield is your Net Operating Income (NOI). This is your gross rent minus all operating expenses, but critically, it excludes mortgage payments. Lenders look closely at NOI to assess if a property can generate enough income to cover its debt, so it is a crucial figure for obtaining financing.

The final and arguably most important metric is your Return on Investment (ROI), sometimes called the cash-on-cash return. This tells you the exact return you are making on the actual cash you have put into the deal—not the total property value.

Formula: (Annual Net Cash Flow / Total Cash Invested) x 100 = ROI %

Here, 'Total Cash Invested' is everything you paid out of pocket: your deposit, Stamp Duty, legal fees, and any initial refurbishment costs. 'Annual Net Cash Flow' is your net rental income after you have made your mortgage payments.

Let’s run the numbers on a real-world example: a two-bedroom flat in Birmingham.

| Metric | Amount |

|---|---|

| Purchase Price | £220,000 |

| Deposit (25%) | £55,000 |

| Stamp Duty & Fees | £8,000 |

| Total Cash Invested | £63,000 |

| Annual Rent (£1,100/month) | £13,200 |

| Annual Operating Costs | – £3,200 |

| Annual Mortgage Payments | – £7,500 |

| Annual Net Cash Flow | £2,500 |

Now for the ROI calculation: (£2,500 / £63,000) x 100 = 3.97% ROI.

This is the number that tells you what your invested capital is actually earning you each year. It provides a true apples-to-apples comparison of this property deal against any other investment, from shares to bonds, helping you decide where your money will work hardest for you.

Navigating Foreign Ownership Rules and Taxes

Investing in international property is exciting, but it is the legal and financial due diligence that separates a sound investment from a costly mistake. Finding the best investment property on a global stage means understanding local regulations. These are not minor details; they can fundamentally alter the security and profitability of your investment.

The rules for foreign investors vary wildly from one country to the next. In many EU nations, for instance, a citizen buying in Spain or Portugal will find the process feels almost identical to buying at home. This makes cross-border investing within the bloc incredibly accessible.

Further afield, however, you can encounter significant roadblocks. In parts of Southeast Asia, you will find that buying freehold land as a foreigner is often not permitted. Investors there typically have to navigate more complex structures, such as setting up a local company or signing long-term leasehold agreements, which adds extra layers of cost and risk.

Understanding the Tax Implications

Beyond ownership, tax is the single biggest factor that will impact your net returns. Gaining a firm grasp of property income tax rates for non-residents is non-negotiable. You must account for taxes at every level—local, national, and international—to avoid unwelcome surprises.

You will need to investigate several key tax liabilities:

- Income Tax on Rent: This is what you will pay on your rental earnings in the country where the property is located. Rates can differ significantly, and you must know which running costs are tax-deductible.

- Capital Gains Tax (CGT): When you eventually sell for a profit, most governments will claim a share. The CGT rate, along with any allowances or exemptions, must be factored into your profit forecasts from day one.

- Local Property Taxes: These are the equivalent of council tax. They are an ongoing annual cost and can vary hugely, even between neighbouring towns in the same country.

It is also essential to understand Double Taxation Agreements (DTAs). These are treaties between countries designed to prevent you from being taxed twice on the same income—once where you invested, and again where you reside. Specialist advice is almost always required here.

Local Tenancy Laws and Regulations

The regulations governing landlords and tenants are another critical piece of your research. These laws shape your rights and responsibilities, affecting everything from how you can increase rent to the process for evicting a non-paying tenant. In some jurisdictions, tenant protections are so strong that an eviction can become a long, drawn-out, and expensive process.

Short-term let regulations have also become a significant factor. Cities like London, Paris, and Barcelona have introduced strict rules to manage the impact of holiday lets on their local housing stock. London's 90-day rule, for example, caps the number of nights you can rent out a property on platforms like Airbnb without specific planning permission. Ignoring these rules can lead to substantial fines.

Key Takeaway: A deal that looks fantastic on a spreadsheet can quickly unravel if restrictive tenancy laws or short-term let caps prevent you from earning the planned income.

Even in a familiar market like the UK, the financial landscape is always shifting. According to Gov.uk data, unincorporated landlords saw a strong rebound in rental income, with the average reaching £19,400 per landlord in the 2023-2024 tax year. That is a 15% increase from 2019-2020 levels. It demonstrates the resilience of a good buy-to-let, even with higher taxes. Before you proceed, our guide on how to buy property abroad provides a solid foundation for your research.

Final Due Diligence and Making a Confident Offer

You have analysed the numbers, compared markets, and finally, a property has risen to the top of your list. On paper, it looks like a strong contender. The location fits your strategy, and the figures appear to stack up.

Now comes the most critical step before you commit your capital: rigorous due diligence. This is your final opportunity to look beyond the fresh coat of paint and uncover any hidden issues that could turn a great investment into a financial liability.

Whether you are on the ground or thousands of miles away, this is a non-negotiable part of the process. It is a deep dive into the building’s physical health, its legal standing, and the real-world factors that will ultimately make or break it for tenants.

The Physical Inspection Checklist

A professional survey is essential, but conducting your own initial walkthrough (physically or virtually) helps you spot major red flags early. Think of it as your first line of defence against expensive surprises.

Focus on the big-ticket items that are most costly to fix:

- Structural Integrity: Look for large cracks in the walls, especially on the exterior. Uneven floors, or doors and windows that stick, can be signs of subsidence. These are serious warning signs.

- Roof and Damp: Check for missing tiles, broken guttering, or water stains on the ceilings. A musty smell, peeling wallpaper, or dark patches on walls often indicate damp, which can be expensive to resolve.

- Utilities and Services: Test everything possible. Run the taps, check the boiler and radiators, and test the light switches. Note the age of the fuse box and boiler—an old system is a significant future capital expense.

- Value-Add Potential: Beyond looking for problems, search for opportunities. Could a simple cosmetic update—a modern kitchen or new flooring—dramatically increase the rental value? Is there space to reconfigure the layout or convert a loft to add another bedroom?

Assembling Your Local Power Team

No investor, particularly an international one, can succeed alone. You need a reliable "power team" of local professionals on the ground. They provide the specialised knowledge and boots-on-the-ground expertise that you cannot obtain from a distance.

Your team should include:

- A Specialist Solicitor or Conveyancer: They will handle all legal checks, from title searches to contract reviews, ensuring the property is free from legal issues.

- An Independent Mortgage Broker: If you require financing, a broker who specialises in buy-to-let or foreign national mortgages is invaluable. They have access to lenders and products you will not find on your own.

- A Reputable Letting Agent: Speak to a few local letting agents (not the agent selling the property). They will give you an honest assessment of achievable rents, tenant demand, and the features tenants in that specific area truly want.

Key Takeaway: Your power team is your most important asset when investing from abroad. Their local knowledge protects your interests and helps you navigate the complexities of a foreign market with confidence.

Making a Confident and Strategic Offer

With your checks complete and your finances arranged, you are ready to make an offer. Do not simply choose a number at random. Your offer should be strategic, backed by your market research, recent comparable sales, and the property’s true condition.

If your survey revealed issues that need fixing, use professional quotes to justify a lower offer. Remember, a strong offer is not just about the price. Demonstrate that you are organised. Highlighting that your solicitor and financing are ready can make your offer far more attractive, even if it is not the highest on the table.

For flats or apartments, it is also crucial to understand the ownership structure. You can familiarise yourself by reading our detailed guide on the distinctions between freehold vs leasehold ownership.

Once your offer is accepted, your solicitor will take the lead. By being thorough in your checks and strategic with your offer, you can move forward to secure the best investment property for your portfolio, free from last-minute surprises.

Frequently Asked Questions

When considering property investment, especially across different countries, many of the same questions arise. Here are direct, practical answers to the queries we hear most often from investors trying to find the best investment property for their goals.

What is a good rental yield for an investment property?

A "good" yield depends entirely on the market and your strategy. There is no single magic number.

In prime global cities like London or Paris, investors often accept gross yields of 3-4%. Their focus is not on monthly income; they are acquiring a 'trophy asset' and relying on steady, long-term capital appreciation to deliver their main return.

However, if your goal is to generate meaningful income, you should aim higher. For investors targeting UK regional cities like Liverpool or Manchester, a gross yield of 6-8% or more should be the target.

Practical Takeaway: As a general rule, a net yield (after all costs are paid) of at least 4-5% is a solid benchmark. This typically indicates the property is generating positive cash flow and can withstand minor market fluctuations.

Should I focus on capital growth or rental income?

This is not a trick question—the right answer is whichever aligns with your personal financial goals and timeline.

If your primary objective is to generate passive income now, perhaps to supplement your salary or fund retirement, then a high-yield property is the clear choice. Your focus should be on markets where the price-to-rent ratio is firmly in your favour.

Conversely, if you have a longer time horizon and do not need the monthly cash, prioritising capital growth makes more sense. This could lead you to buy in an area undergoing major regeneration or with significant infrastructure projects planned, betting on a substantial rise in value over time. The most resilient portfolios often contain a mix of both.

How much deposit do I need for a buy-to-let mortgage as a foreign investor?

When applying for a buy-to-let mortgage as a non-resident or an expatriate, you should be prepared for a much larger deposit than a local buyer. Most lenders will require a down payment of at least 25-40% of the property's price.

The final figure will depend on several key factors:

- The lender’s own criteria and risk appetite.

- Your country of residence and its financial regulations.

- Your personal financial situation and credit history.

It is absolutely crucial to work with a mortgage broker who specialises in financing for expatriates and foreign nationals. They have access to a network of specialist lenders and products you simply will not find on the high street.

Is it better to invest in a new-build or an older property?

Both new-builds and older properties offer compelling, but very different, advantages for an investor.

New-build properties are attractive because they usually come with builders' warranties, require very little initial maintenance, and have high energy efficiency ratings—something tenants increasingly seek. The trade-off is that you often pay a premium, and initial capital growth can be slower as the "new-build shine" wears off.

Older, existing properties often have more character and are located in well-established neighbourhoods. They also present clear opportunities to add value through renovation, a strategy known as "forcing appreciation" that can create instant equity. The risk is unexpected maintenance costs, which makes a thorough survey and a healthy contingency budget essential.

At World Property Investor, we provide the in-depth guides and data-driven analysis you need to confidently compare global markets. Explore our resources to find your next investment at https://www.worldpropertyinvestor.com.