Investing in European property offers access to some of the world's most stable and mature markets. It provides strong legal frameworks and consistent rental demand, but success is not guaranteed. It hinges on a clear strategy that balances risk with reward, whether you are drawn to the higher-yield potential of emerging markets or the security of established economies. This guide provides a practical framework for your investment journey, moving beyond general advice to deliver actionable insights.

Your Strategic Entry into the European Property Market

Before examining property listings, your first step is to define your investment objectives. Are you targeting long-term capital appreciation, steady monthly rental income, a holiday home that generates revenue, or a route to residency? Your answer is critical, as it immediately narrows the field of suitable markets. Each country presents a different risk and reward profile.

Established markets such as Germany and France represent the bedrock of European property investment. They offer reassuring economic and political stability, with data from bodies like Eurostat consistently showing transparent legal systems. This makes them lower-risk environments, but that security comes at a price—typically lower rental yields and higher acquisition costs.

Conversely, emerging markets, particularly in Central and Eastern Europe, can offer significantly higher returns. Countries like Poland or Hungary may deliver gross rental yields double those found in major Western European capitals. However, this potential for higher returns is balanced by increased risks, such as currency fluctuations and less mature legal frameworks for foreign investors.

Analysing Key Investment Factors

A successful investment is built on solid fundamentals, not market sentiment. Investors should analyse several core metrics:

- Economic Stability: Examine GDP growth, unemployment rates, and foreign direct investment trends. A country with a diverse, growing economy is better equipped to withstand economic shocks.

- Rental Yields vs. Capital Growth: You must decide whether your priority is immediate cash flow from rent (yield) or a long-term increase in the property's value (capital growth). High-yield areas do not always deliver the fastest price growth, and vice-versa.

- Foreign Ownership Laws: While most of Europe welcomes foreign buyers, some countries have specific restrictions or require additional legal processes. Understanding these rules is a non-negotiable first step.

A prudent investor never relies on market hype. Instead, focus on underlying fundamentals: Is the local population growing? Is the economy creating new jobs? These are the indicators that sustain a property market for the long term.

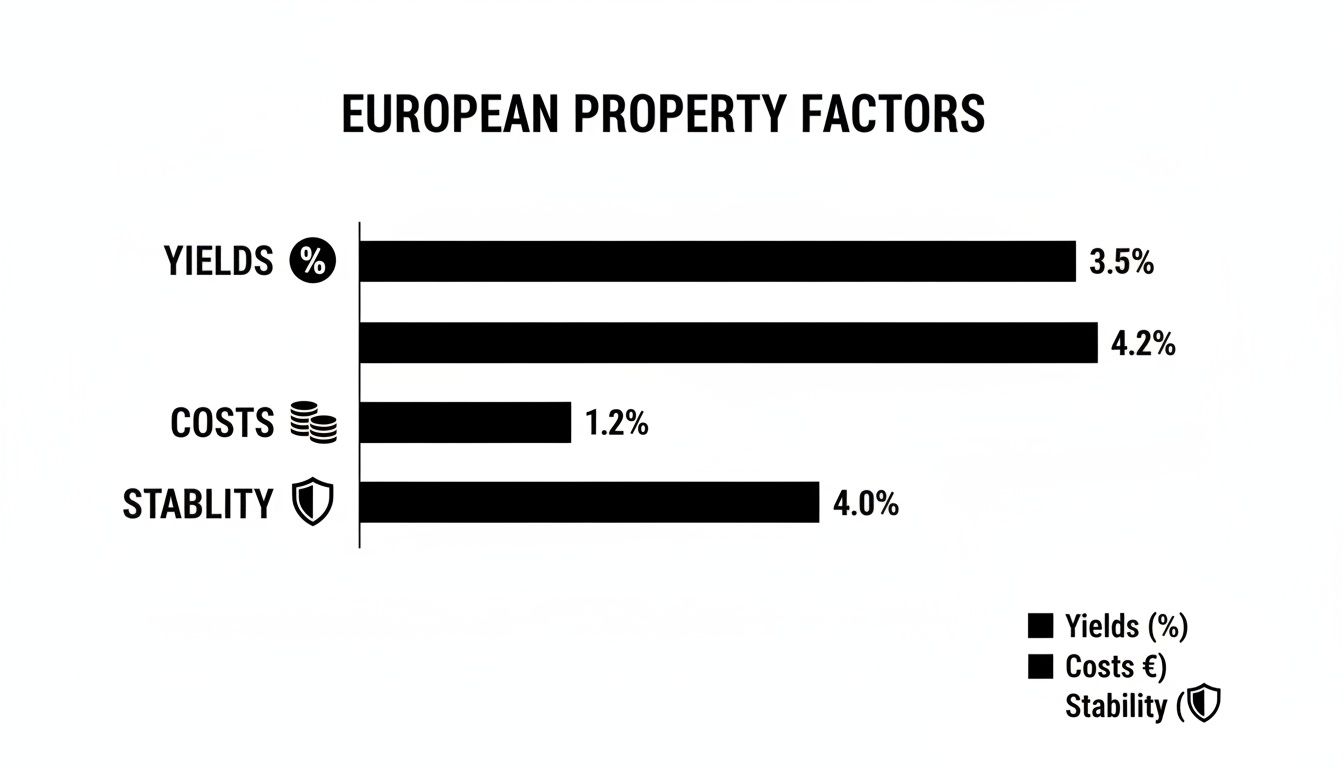

This chart provides a simplified snapshot of how yields, costs, and stability often interact across the continent.

As the visual suggests, there is often a classic trade-off. Higher yields can sometimes correlate with lower stability, while lower transaction costs can be found across various markets. This makes thorough due diligence on all three factors essential.

European Property Market Snapshot for Investors

This high-level comparison of key metrics across popular and emerging European destinations will help you to assess different market characteristics and narrow your search.

| Country | Average City Centre Yield (Gross) | Foreign Ownership Rules | Typical Transaction Costs (Buyer) | Market Stability |

|---|---|---|---|---|

| Portugal | 4.5% – 6.5% | Open, no major restrictions | 6% – 8% | Moderate-High |

| Spain | 4.0% – 6.0% | Open, no major restrictions | 10% – 14% | Moderate-High |

| Germany | 2.5% – 3.5% | Open, no major restrictions | 7% – 12% | Very High |

| France | 3.0% – 4.5% | Open, no major restrictions | 7% – 10% | Very High |

| Greece | 4.0% – 7.0% | Open (Golden Visa available) | 6% – 9% | Moderate |

| Poland | 5.0% – 7.5% | Open, permit needed for land | 4% – 6% | High |

This table is not a substitute for in-depth research but serves as a useful starting point. It immediately highlights key differences—for instance, the lower yields in the ultra-stable German market versus the more attractive income potential in recovering markets like Greece or growth hubs like Poland. Your task is to find the balance that best fits your personal investment goals.

How to Analyse and Select European Property Markets

When you buy property in Europe, the true potential is found in data, not in marketing brochures. A professional investor looks past surface-level sentiment and builds a solid case based on economic and demographic facts. This is not about chasing market trends; it is about making deliberate, data-backed decisions that serve your long-term objectives.

The analysis should begin with the macroeconomic health of a country or region. Credible sources like Eurostat and national statistics offices provide a wealth of information. Key signals to monitor include consistent GDP growth, falling unemployment rates, and significant public and private infrastructure investment. A city benefiting from new transport links, business parks, or university campuses is likely to experience sustained housing demand.

A country with a stable, growing economy is far better positioned to handle economic shocks, which protects your capital and ensures a steady supply of quality tenants.

Distinguishing Between Established and Emerging Markets

Not all markets within the same country are equal. A crucial part of intelligent analysis is comparing different regions to identify their unique risk and reward profiles. This approach helps to uncover pockets of value that other investors may overlook.

Consider Portugal, for example. Lisbon is a mature, established market that attracts significant foreign investment, resulting in high property prices and rents. While it offers a degree of security, its period of explosive capital growth may have passed.

In contrast, a region like the Algarve presents a different proposition. It contains pockets of emerging potential, particularly for holiday lets and retirement properties. Yields can be stronger, and the cost of entry is often much lower than in the capital. By comparing fundamentals—local employment trends, tourism figures, and planned infrastructure—you can decide which market truly aligns with your strategy. Our guide on the top 7 emerging property investment markets provides further ideas.

Calculating Realistic Rental Yields

A common error for new investors is focusing on the gross rental yield advertised by agents. This figure is often misleading as it ignores the real costs of property ownership. To understand your actual return on investment (ROI), it is imperative to calculate the net rental yield.

To do this, start with the annual rental income, then subtract all anticipated expenses:

- Property Management Fees: Typically between 8-12% of the monthly rent.

- Maintenance and Repairs: A prudent budget is 1% of the property’s value annually.

- Vacancy Periods (Voids): Realistically, your property might be empty for a month each year, so factor in an 8-10% vacancy rate.

- Insurance and Local Taxes: These vary significantly between countries and even municipalities, so research is essential.

Once you have deducted these costs from your gross rent, divide the result by the total purchase price (including all transaction costs) and multiply by 100. This is your net yield—a far more accurate measure of the property's performance.

An investment that appears attractive with a 7% gross yield might only deliver a 3.5% net yield after all costs are considered. Performing these calculations properly prevents unpleasant surprises and ensures your cash flow projections are based on reality.

Understanding Supply, Demand, and Regulations

Ultimately, market fundamentals are driven by the balance of housing supply and demand. You must identify demographic shifts that signal growing demand, such as a rising population, an influx of young professionals, or an expanding university. These are all powerful indicators of a healthy rental market.

Local regulations can also significantly impact an investment. Some cities, like Berlin, have introduced forms of rent control that can limit your rental income and growth potential. Conversely, other areas may offer tax incentives for renovating older properties, which could boost your returns.

The UK residential market provides a clear case study. The 'Living' sector—encompassing build-to-rent and standard residential homes—posted an impressive 8.8% total return over a recent 12-month period, according to a major real estate services firm. This performance was driven not by soaring house prices, but by powerful rental growth, which the Office for National Statistics reported at 8.1% in the private rented sector. This figure outpaced both headline inflation and house price growth, demonstrating the profitability of a market with strong demand and constrained supply.

Understanding the Legal and Financial Framework

Successfully buying property in Europe requires an understanding of each country’s unique legal and financial systems. While the bureaucracy may seem intimidating, it is manageable with knowledge of the key players and processes. Your success when you buy property in Europe will almost always depend on the quality of the professional team you assemble on the ground.

Notaries vs. Solicitors: A Critical Distinction

A primary hurdle for investors is understanding the different roles of legal professionals. In common law countries like the UK and Ireland, your solicitor works exclusively for you, providing advice, conducting checks, and protecting your interests.

In most of mainland Europe, a different system applies. Countries like France, Spain, and Germany operate under a civil law system where a notary (a notaire in France or Notar in Germany) is a quasi-public official. Their primary duty is to the state, ensuring the transaction is legally sound and all taxes are paid. They do not act as your personal advocate.

This is a crucial distinction. A French notaire will execute the deed of sale but will not offer the same protective advice as a British solicitor. It is therefore highly recommended that international buyers in civil law countries hire their own independent lawyer or avocat to review contracts and represent their interests.

Securing Finance as a Non-Resident

There are several routes to finance your European property purchase, each with distinct advantages and disadvantages. The main options are buying with cash, obtaining a local mortgage, or financing through an international lender. A cash purchase is the simplest but may not be the most efficient use of capital.

Obtaining a local mortgage as a non-resident is possible, particularly in markets like Spain and Portugal that are accustomed to foreign buyers. However, be prepared for stricter lending criteria than a local applicant would face.

- Loan-to-Value (LTV) Ratios: You will require a larger deposit. While a resident might secure a mortgage for 80% of the property’s value, non-residents are typically offered between 60-70%. This means having a 30-40% deposit available.

- Documentation: Lenders will require extensive proof of income from your home country, recent bank statements, tax returns, and a strong credit history. Expect to have all documents officially translated.

- Interest Rates: Rates may be slightly higher for non-residents, as lenders perceive this as an additional risk. It is advisable to shop around, ideally using a specialist mortgage broker who deals with international clients.

For example, German banks are known for lending to expatriates, but the terms improve significantly if you hold a permanent residence permit. A non-EU citizen without residency may find their borrowing is capped at 60% of the property’s value.

Understanding the True Cost of Taxes

The agreed purchase price is just the beginning of your financial commitment. A complex web of taxes—at purchase, annually, and on sale—can significantly impact your net return. Overlooking these is one of the most common and costly mistakes for first-time international investors.

The initial tax is the property transfer tax, often known as Stamp Duty. This varies wildly. In Spain, the Impuesto de Transmisiones Patrimoniales can range from 6% to 11%, while Germany’s equivalent, the Grunderwerbssteuer, is between 3.5% and 6.5%.

Your budget must account for total acquisition costs, not just the property price. As a rule of thumb, set aside an additional 10-15% of the purchase price to cover all taxes, notary fees, and legal expenses.

Once you own the property, you will be liable for annual property taxes. In Portugal, this is the Imposto Municipal sobre Imóveis (IMI), and in Spain, the Impuesto sobre Bienes Inmuebles (IBI). Data from bodies like the OECD shows that France and the UK have some of Europe's highest recurring property taxes relative to GDP.

Finally, consider your exit strategy from day one. When you eventually sell, any profit is likely to be subject to Capital Gains Tax. Rates and exemptions vary widely; in Germany, for instance, you can be exempt from this tax if you have owned the property for more than ten years. Understanding these long-term implications from the outset is essential for accurate return forecasting.

Executing The Purchase From Offer To Ownership

Once your due diligence is complete and you have found the right property, it is time to move from analysis to action. The process to buy property in Europe is not uniform; it varies significantly between civil law and common law jurisdictions. Navigating this correctly is crucial for a smooth transaction.

Most of mainland Europe, including popular investment destinations like Spain, France, and Germany, operates under a civil law system. This framework places great importance on a state-appointed notary. In contrast, the UK and Ireland use a common law system, where solicitors for the buyer and seller manage the process.

The Preliminary Contract Stage

Regardless of where you are buying in Europe, the first major legal step after an offer is accepted is signing a preliminary contract. This document secures the deal and sets out the terms for the final sale. The name varies by country, but its function is consistent.

In France, you will sign a compromis de vente. This is a legally binding agreement that includes a ten-day cooling-off period. In Spain, it is the contrato de arras, a private contract where a deposit of typically 10% is paid. If you withdraw without a valid legal reason, you forfeit this deposit.

It is vital that these contracts include contingency clauses (clauses suspensives in French). These are your safety nets, allowing you to withdraw without penalty if certain conditions are not met, such as securing a mortgage, obtaining a satisfactory building survey, or confirming planning permissions.

Tailoring Your Negotiation Strategy

Negotiating property prices requires cultural awareness as much as financial acumen. In some markets, a low offer is a standard opening gambit. In others, it can be viewed as an insult and end negotiations.

- Southern Europe (Spain, Italy, Greece): There is generally more flexibility. It is common to offer 5-10% below the asking price, particularly for properties that have been on the market for some time.

- Northern Europe (Germany, Netherlands): These markets are more rigid. Properties are usually priced close to their market value, so a lowball offer is unlikely to succeed. In competitive city markets, you may even have to offer the asking price or slightly more.

Let your market analysis guide your strategy. Is it a buyer’s or a seller’s market? How long has the property been listed? This data, not emotion, should inform your offer.

A successful negotiation is not just about securing the lowest price; it is about agreeing on terms that work for all parties. Consider negotiating other points, such as the inclusion of furniture or an adjustment to the completion date.

The Closing Process And Transfer Of Ownership

The final stage is the closing, or completion. This is when the property legally becomes yours. The process culminates in a final meeting, which in civil law countries almost always takes place at the notary’s office.

During this meeting, the final deed of sale (acte de vente in France or escritura pública de compraventa in Spain) is read aloud before being signed by all parties. You will transfer the remaining balance of the purchase price, plus all taxes and fees. The notary handles the collection of these funds and payment to the relevant authorities.

Once the funds have cleared and the deed is signed, you will receive the keys. The final step is for the notary to register the sale with the official Land Registry (Grundbuch in Germany, Registro de la Propiedad in Spain). This registration is the definitive proof of your ownership, concluding your journey to becoming a European property owner.

From Offer to Keys: Your Post-Purchase Strategy for Maximum Returns

Receiving the keys to your European property is a significant milestone, but it is only the beginning of your investment journey. The work of transforming that asset into a high-performing investment starts now.

Effective management is what separates a passive, underperforming property from a profitable one. This phase determines your cash flow, long-term capital growth, and ultimate success. Your first major decision is the management model.

Selecting Your Property Management Model

This choice depends on your time, location, and desired level of involvement. For the hands-on investor, self-management offers total control and saves on fees. It can work if you live nearby, speak the language, and are familiar with local tenancy laws. For most international investors, however, time zones and distance make this impractical.

A good compromise is hiring a local property manager. This is often an individual who handles day-to-day tasks—collecting rent, arranging minor repairs—for a fee of around 5-8% of the monthly rent. It is a cost-effective way to get on-the-ground support.

The most common route for overseas investors is a full-service management agency. They handle everything from marketing and tenant vetting to legal compliance and maintenance. You will pay more, typically 10-15% of rental income, but in return you receive a genuinely passive ownership experience.

When vetting managers or agencies, do not just consider the fees. Ask for references, review their portfolio of similar properties, and ensure they have a transparent system for reporting income and expenses. This diligence is crucial for a successful partnership.

Rental Strategies: Long-Term vs. Short-Term Lets

Your rental strategy must align with your goals and the property’s location. The two main options are long-term residential lets and short-term holiday rentals, each with distinct advantages and disadvantages.

Long-term lets offer stability and predictable income. They are ideal if you seek consistent cash flow with less hands-on management. This model works best in cities with strong local economies and a large pool of professional tenants. The UK market, for example, is seeing a significant institutional shift, with build-to-rent completions rising 17% year-on-year according to industry reports, highlighting the robustness of the long-term rental market.

Short-term holiday lets, on the other hand, can generate much higher income during peak season, especially in hotspots like the Algarve or the Greek islands. However, this comes with higher vacancy rates, more intensive management, and a growing web of local regulations. Cities like Lisbon and Barcelona have introduced licensing rules to manage tourism's impact, adding complexity for owners.

Securing Tenants and Planning Your Exit

Attracting reliable tenants begins with professional marketing. Use high-quality photographs and list your property on major local portals. When you receive applications, always conduct credit and reference checks.

Crucially, ensure your tenancy agreement is legally compliant for that specific country. It is always worth paying a local lawyer to draft or review it; this small cost can prevent significant problems later.

Finally, a savvy investor always considers their exit strategy. This does not mean planning to sell immediately, but you should continuously monitor the market. Keep an eye on local price trends, new infrastructure projects, and economic forecasts. By understanding these fundamentals, you will know when the time is right to sell and realise your capital gains, completing a successful investment cycle.

Common Questions on Buying European Property

Entering the European property market raises several key questions, particularly for investors from outside the continent. Understanding the realities of obtaining a mortgage, navigating post-Brexit rules, and finding trustworthy professionals on the ground is crucial. Let's address some of the most common queries.

Can Non-Residents Get A Mortgage In Europe?

Yes, absolutely—but be prepared for a different process. European lenders view non-resident borrowers as a higher risk and therefore apply stricter criteria.

Expect to provide a larger deposit, often between 30-50% of the property's value. You will also need to supply comprehensive documentation, including professionally translated proof of income, international credit reports, and several months of bank statements from your home country.

Countries like Spain and Portugal are experienced in dealing with foreign buyers, and their banks are generally more accommodating. However, it is strongly advised to work with a specialist mortgage broker. They have the right contacts and understand the specific paperwork each lender requires from foreign nationals, which can save considerable time and stress.

What Has Changed for UK Buyers in the EU After Brexit?

The legal process of buying property has not fundamentally changed. The UK's common law system was always distinct from the civil law systems prevalent across mainland Europe. The most significant change relates to residency rights.

UK citizens are now treated as other non-EU nationals. This means purchasing a property no longer grants any automatic right to live there. Your stays in the Schengen Area are limited to 90 days within any 180-day period. For longer stays, you must apply for a long-stay visa or a formal residency permit.

Transaction costs and property taxes are determined by the country where the property is located, so your nationality does not affect these.

For context, UK house prices have remained resilient. Data from the ONS shows that average private rents in the UK increased by 9.2% in the 12 months to March 2024, demonstrating the ongoing strength of the rental market. You can find more detailed figures in the ONS report on private rent and house prices in the UK.

Which Countries Offer Golden Visas?

Several European countries offer residency-by-investment programmes, often called 'Golden Visas'. These are designed to grant residency to non-EU citizens who make a significant investment and can be an excellent option for investors seeking more than just a holiday home.

Popular options include:

- Spain: Requires a real estate investment of at least €500,000.

- Greece: Offers one of the most accessible programmes, with a minimum investment starting from €250,000 in some areas.

- Portugal: The well-known Golden Visa has been revised. It no longer applies to direct residential property purchases in major cities like Lisbon and Porto, but routes remain available through fund investments or commercial real estate.

These programmes are complex, and the rules change frequently. It is essential to seek specialist legal and financial advice from a firm that focuses on investment migration before committing. They will have up-to-date knowledge of the latest regulations.

How Can I Find Reliable Professionals Abroad?

Your success depends on the quality of your team on the ground. You cannot afford to cut corners when finding a trustworthy estate agent and an independent lawyer.

A good starting point is seeking recommendations on established expatriate forums or in international property investor networks. People are often willing to share both good and bad experiences.

For estate agents, check if they belong to a recognised professional body like the AIPP (Association of International Property Professionals). For a lawyer, ensure they are completely independent—never use one recommended by the seller or the agent. They should be fluent in English, specialise in property transactions for foreign buyers, and provide a clear, written breakdown of their fees before you engage them.

At World Property Investor, we provide the in-depth guides and market analysis you need to make informed decisions. Explore our resources to find your next global property investment with confidence. https://www.worldpropertyinvestor.com