Investing in property abroad is a sound strategy for portfolio diversification, generating rental income while accessing high-growth international markets. However, it is a fundamentally different undertaking from a domestic purchase. Investors must navigate currency risk, unfamiliar legal systems, and the complexities of managing an asset from a distance. A well-executed strategy can yield substantial rewards, whereas a poorly planned one can result in significant financial loss.

Why Look Beyond Your Domestic Market?

For many investors, the primary appeal of purchasing a rental property overseas is the potential for superior returns. As property prices in mature markets like the UK have escalated, rental yields have often compressed. In contrast, many international locations offer a more favourable balance between affordable property prices and strong, consistent rental demand.

This strategy extends beyond chasing higher yields; it is a prudent method of risk mitigation. By diversifying assets geographically, a portfolio is insulated from localised economic downturns. A slump in one country's property market can be offset by stability or growth in another. Economic data consistently shows that different housing markets respond uniquely to the same global financial pressures.

What Drives Global Property Investors?

Successful international property investment is underpinned by clear, strategic objectives. While the concept of a holiday home that finances itself is appealing, a purely investment-led approach typically produces stronger financial outcomes.

The primary drivers for experienced global investors include:

- Higher Rental Yields: Many emerging markets and even established European cities offer gross rental yields that significantly outperform those in capital cities such as London.

- Capital Growth Potential: Investing in an area with a growing economy, new infrastructure projects, and a rising population can lead to substantial long-term capital appreciation.

- Portfolio Diversification: Spreading investments across different countries and currencies is a classic wealth preservation strategy, providing a buffer against domestic economic or political instability.

- Lifestyle & Retirement Goals: For some, an overseas property is a hybrid investment. It serves as a future retirement location or a family holiday home that generates income when not in personal use.

Establishing these fundamentals is the first step. For detailed analysis of specific strategies and markets, you can explore a wide range of articles on global property investment. This guide will outline the practical steps to transform an overseas ambition into a profitable reality.

Finding And Analysing Profitable Overseas Markets

Selecting the right market is the foundation of a successful overseas investment. This process requires a methodical analysis of economic fundamentals, landlord-friendly regulations, and genuine rental demand, rather than relying on a location's holiday appeal. Correctly executing this stage establishes the basis for your entire buy-to-let abroad strategy.

Differentiating Gross And Net Rental Yields

The first metric investors often focus on is rental yield, but it is crucial to distinguish between gross and net figures. Gross yield is the total annual rent divided by the purchase price. While simple to calculate, it can be misleading as it provides no insight into actual profitability.

Net yield reveals the true performance of the asset. This is the figure calculated after deducting all operational costs, including property management fees, maintenance, insurance, and local property taxes.

For example, a property in an emerging market may advertise an impressive 8% gross yield. However, if high management fees and local taxes reduce this to a 3% net yield, it could be less profitable than a property in an established market showing a 5% gross yield that delivers a 4% net yield.

Investment decisions must always be based on the projected net yield. This figure reflects the true return on your investment and prevents distraction by superficially attractive but ultimately unprofitable opportunities.

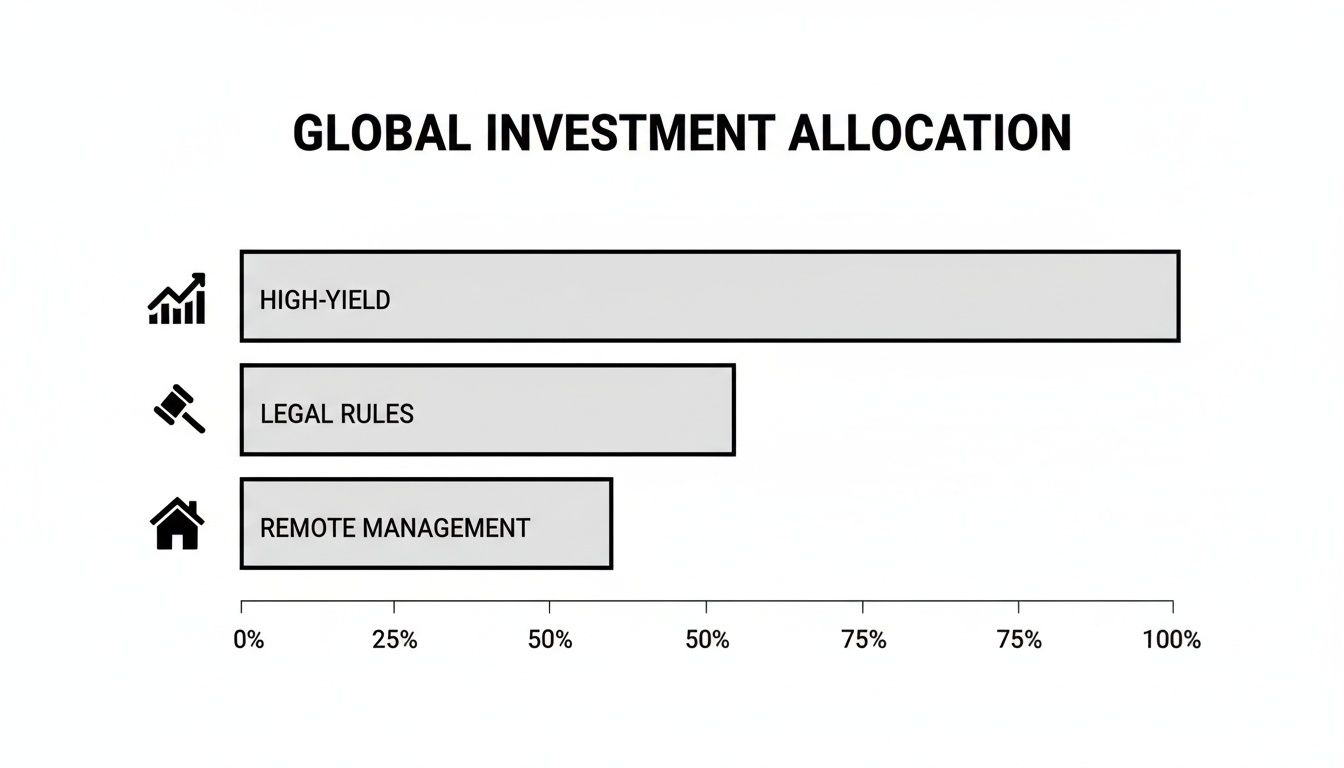

This chart illustrates how experienced investors typically prioritise their focus when evaluating a potential market to buy-to-let abroad.

As the data shows, while a high yield is the primary attraction, factors such as a stable legal framework and the feasibility of remote management are critical for building a sustainable, long-term investment.

Established Hubs Vs Emerging Hotspots

The choice between an established or emerging market fundamentally defines your risk and reward profile. Established markets offer stability and predictability, while emerging markets present the potential for higher growth alongside greater risk.

-

Established Markets (e.g., UK, Germany, France): These locations are characterised by political stability, transparent legal systems, and deep, liquid property markets. Capital growth may be slower, but rental demand is often highly consistent, supported by strong economies and major population centres. They are generally considered lower-risk investments.

-

Emerging Markets (e.g., parts of Southeast Asia, Eastern Europe): These can offer significantly higher rental yields and the potential for greater capital appreciation. However, they are accompanied by increased risks, such as currency volatility, political instability, and less transparent legal processes for foreign owners.

To provide a tangible example, the UK rental market remains a robust option for buy-to-let abroad investors. According to data from Hamptons, average gross yields on new purchases in England and Wales recently hit 6.2%. Major urban centres like Manchester, with its undersupply of housing and strong tenant demand, can deliver gross yields of 7-8%.

Market Comparison: Established vs Emerging Buy-To-Let Destinations

This table provides a comparative analysis of key investment metrics across popular and developing international property markets, illustrating the relationship between risk and potential returns.

| Country | Average Gross Rental Yield | Typical Capital Growth (Annual) | Key Risks | Investor Profile |

|---|---|---|---|---|

| UK (Established) | 5-7% | 2-4% | Regulatory changes, higher entry prices | Prefers stability, steady income, lower risk. |

| Germany (Established) | 3-4% | 3-5% | High transaction costs, tenant-friendly laws | Focused on long-term capital preservation and growth. |

| Portugal (Established) | 4-6% | 4-7% | Tourism dependency, evolving regulations | Seeks a blend of lifestyle and moderate growth. |

| Thailand (Emerging) | 5-8% | 3-6% | Foreign ownership restrictions, currency volatility | Amenable to higher risk for lifestyle and rental returns. |

| Georgia (Emerging) | 8-12% | 5-10% | Political instability, less mature legal system | High-risk tolerance, focused on yield and growth. |

This comparison highlights the classic investment trade-off: established markets offer security and predictability, whereas emerging markets provide the opportunity for higher returns but demand a greater appetite for risk. Your financial objectives and risk tolerance will determine the appropriate path.

Core Fundamentals For Market Analysis

Beyond yield calculations, due diligence must extend to the underlying economic drivers that sustain a rental market. A disciplined analysis helps investors avoid speculative bubbles and focus on long-term, tangible fundamentals.

Focus on cities with:

- Strong and Diverse Job Markets: A growing economy with multiple industries creates a steady stream of professional tenants who can afford consistent rental payments.

- Population Growth: Rising populations, driven by internal migration or immigration, directly fuel rental demand.

- Infrastructure Investment: Government spending on new transport links, schools, and public amenities increases an area's desirability and can stimulate property value appreciation.

- Landlord-Friendly Legislation: Research local tenancy laws. Some jurisdictions heavily favour tenants, making evictions difficult and costly, which adds a significant layer of risk to an investment.

A city like Manchester, for instance, exhibits many of these characteristics with its thriving technology sector and significant infrastructure projects. This contrasts with a purely tourist-driven coastal town in Spain, which might offer high seasonal returns but could suffer from long void periods and less stable demand.

To assist your evaluation, our guide on the best buy to let locations offers a detailed breakdown of top-performing cities worldwide. This methodical approach ensures your decision to buy-to-let abroad is based on solid data, not just lifestyle appeal.

Securing Finance For Your Overseas Property

Arranging finance is often the most significant challenge when you decide to buy to let abroad. Most domestic high-street banks are reluctant to lend on a property they cannot easily value or repossess. Lenders in the target country can be equally cautious about a non-resident borrower.

Understanding your financing options from the outset is critical. Be prepared for stricter lending criteria, larger deposit requirements, and more extensive paperwork than for a domestic purchase.

Your Primary Financing Avenues

When funding an overseas investment, there are generally three main routes. Each has distinct advantages and disadvantages, making it important to identify which aligns with your financial situation.

-

Remortgaging a Domestic Property: For many, this is the most straightforward path. Releasing equity from an existing property in your home country allows you to act as a cash buyer abroad, thereby avoiding the complexities of dealing with foreign lenders.

-

Using a Specialist International Mortgage Broker: These brokers possess the expertise and relationships with lenders that specialise in non-resident investors. They understand the niche products available and can navigate the regulatory requirements across different jurisdictions.

-

Applying to a Local Bank in the Target Country: This can be more challenging but is feasible, particularly if the bank has a dedicated international division. Expect to provide a substantial deposit and a large volume of translated and notarised documents.

Navigating Lender Requirements And Deposits

Regardless of the financing route, expect your application to undergo rigorous scrutiny. Lenders perceive a greater risk with non-residents and require a robust financial profile to demonstrate your ability to manage an overseas investment.

For a buy to let abroad mortgage, lenders will almost universally demand a larger deposit, typically in the range of 30-40% of the property’s value. This lower loan-to-value (LTV) ratio serves as their security against the risks associated with lending to a foreign national.

Key Takeaway: A significant deposit is a non-negotiable requirement for most overseas mortgage applications. Lenders view it as a critical indicator of your financial commitment and stability, facilitating loan approval.

You will also need to compile a comprehensive file of documents. The exact requirements vary by country, but generally include:

- Proof of Income: Your last three to six months of payslips and your most recent annual tax return.

- Proof of Deposit: Bank statements showing the funds are readily available.

- Credit History: A clean credit report from your home country.

- Valid Identification: Your passport and proof of your current residential address.

For example, a UK investor seeking a mortgage in Spain would need to provide a Spanish bank with all these documents, often officially translated. Similarly, an investor from Singapore buying in London must satisfy a UK lender’s stringent anti-money laundering checks and often meet a minimum income threshold, which Gov.uk guidance suggests is typically around £25,000, though some lenders require more. Our detailed guide offers more on the essentials of financing an investment property.

Managing Currency Risk On Your Investment

A frequently overlooked factor is currency risk. If your mortgage repayments are in one currency (e.g., Euros) but your income is in another (e.g., Pounds Sterling), an adverse movement in the exchange rate can erode profits and increase monthly costs.

Prudent investors mitigate this by opening a local bank account in the country of purchase. Rental income is paid into this account in the local currency, and the mortgage and other local expenses are paid directly from it.

This creates a natural hedge, allowing you to repatriate profits only when the exchange rate is favourable, rather than being forced to make transfers monthly regardless of the rate.

Navigating Legal Structures And Tax Obligations

The legal structure through which you own your investment property is a critical decision that is often overlooked by new investors. This choice has profound implications for tax liability, personal liability, and future estate planning.

When you buy to let abroad, purchasing the property in your personal name is not always the most efficient strategy. Establishing the correct structure from the outset can yield significant tax savings and protect your other assets. It dictates how rental income is taxed and how profits are treated upon sale. Seeking specialist legal and tax advice specific to both your home country and your target location is essential before making an offer.

Choosing Your Ownership Structure

For most international buyers, the decision is between purchasing as an individual or establishing a corporate entity, such as a limited company. Each path has distinct advantages and disadvantages that vary between jurisdictions.

-

Buying as an Individual: This is the simplest and most direct method. The legal process is more straightforward, and there are no ongoing administrative costs associated with running a company. The primary drawback is that personal assets are not shielded from property-related liabilities.

-

Buying Through a Limited Company: This involves creating a dedicated legal entity, often a Special Purpose Vehicle (SPV), for the sole purpose of holding the property. This structure creates a "corporate veil" between your personal finances and the investment, limiting your liability. Critically, it can also provide significant tax advantages in markets like the UK.

The Rise Of The Limited Company Model In The UK

The UK serves as a compelling case study for the importance of ownership structure. Legislative changes to mortgage interest tax relief for individual landlords have reshaped the buy-to-let market.

Previously, individual landlords could deduct all mortgage interest from their rental income before calculating tax. Now, they receive only a basic-rate tax credit. Limited companies, however, were not affected by this change and can still offset 100% of their mortgage interest against profits before paying corporation tax. For many investors, this difference is the deciding factor in a deal's profitability.

The shift towards corporate ownership has been significant. According to Hamptons, in 2023, a record 50,000 new buy-to-let companies were incorporated in the UK. This trend reflects a strategic move by investors to optimise their tax position. You can read more about the growth of limited company BTLs on liquidexpatmortgages.com.

Performing Essential Legal Due diligence

Regardless of the chosen structure, thorough legal due diligence is non-negotiable. This process, conducted by your lawyer, ensures the property title is clean, there are no hidden encumbrances, and the seller has the legal right to transfer ownership. In many European countries, this is handled by a public notary.

Key checks include:

- Title Search (Verifying Ownership): Your legal representative will examine land registry records to confirm the seller is the legal owner and check for any liens or debts registered against the property.

- Planning Permission Checks: This confirms the property was built in accordance with local regulations and that any modifications have the required approvals.

- Understanding the Notary's Role: In civil law countries like Spain, France, and Germany, a notary plays a central, impartial role. They are responsible for drafting the final deed, ensuring the transaction complies with the law, and officially registering the sale.

Demystifying The International Tax Landscape

Tax is one of the most complex aspects of buying property abroad, and errors can be costly. You will have obligations in both the property's location and your country of residence, making professional advice essential.

The main taxes to be aware of are:

| Tax Type | Description | Example |

|---|---|---|

| Purchase Tax | A one-off tax paid upon acquisition of the property. | In the UK, this is Stamp Duty Land Tax (SDLT). For overseas investors, this can represent a significant portion of the purchase price. |

| Income Tax | An ongoing tax on the net rental income generated by the property. | Most countries tax this income at source. The applicable rates and deductible expenses vary widely. |

| Capital Gains Tax (CGT) | A tax on the profit realised when the property is sold for more than its acquisition cost. | This is calculated on the difference between the sale price and your original purchase price plus allowable costs. |

| Inheritance Tax | A potential tax liability for your heirs when the property is transferred to them. | The rules are highly specific to each country and your residency status. |

A primary concern for investors is double taxation—being taxed on the same income in two different countries. Double Taxation Treaties (DTTs) are bilateral agreements between countries designed to prevent this.

A DTT specifies which country has the primary right to tax your income and outlines how your home country must provide credit for tax already paid abroad. Ignoring these treaties is a common error that can lead to a substantially higher tax burden.

Managing Your International Property From Afar

Owning an investment property from a significant distance makes self-management practically unfeasible. The key to a successful buy-to-let abroad venture is appointing a reliable, professional local property manager. This agent acts as your local representative, handling everything from tenant vetting to emergency maintenance.

Selecting the right agent is a critical decision. A proficient manager protects your asset and ensures consistent income flow; an incompetent one can quickly turn a promising investment into a financial liability. This step should not be rushed.

Vetting Your Property Management Partner

Before signing any contract, you must conduct a thorough interview process with potential agents. Treat this as hiring a key employee, as they will be integral to your investment's success. A reputable agent will welcome detailed questions and provide clear, direct answers.

A practical checklist of questions includes:

- Fee Structure: What is the exact management fee (typically 10-15% of monthly rent)? Are there additional charges for tenant placement, inspections, or arranging repairs? Obtain a full schedule of fees in writing.

- Tenant Sourcing: What is their process for finding and screening tenants? Look for evidence of credit checks, employment verification, and references from previous landlords.

- Maintenance Procedures: How are routine maintenance and emergencies handled? Do they have a network of vetted local tradespeople, and what is the expenditure limit before requiring your authorisation?

- Financial Reporting: What type of financial statements will be provided, and at what frequency? You require clear, monthly reports detailing rental income and a breakdown of all associated costs.

Your objective is to find an agent who communicates proactively and operates with full transparency. Vague responses regarding fees or an inadequate tenant-vetting process are significant red flags.

The global appeal of certain markets means competition for high-quality agents can be intense. The UK, for example, has seen a substantial influx of overseas buy-to-let investment. Research from Hamptons shows that foreign-owned rental companies now account for one in five new landlord company incorporations. For more on this trend, see their report on the rise of international landlords.

Long-Term Lets Versus Short-Term Holiday Rentals

Your management requirements will differ significantly depending on your rental strategy. The day-to-day operations for a long-term residential let are distinct from those of a short-term holiday rental, each with its own risk and reward profile.

Long-Term Lets offer stability and predictable income streams via fixed-term contracts (often 12 months or more). Management is less intensive, focusing on rent collection, periodic inspections, and occasional repairs. This is often the preferred route for investors seeking passive income with minimal operational involvement.

Short-Term Holiday Lets can generate much higher weekly or nightly rates, particularly in tourist destinations. However, this increased income comes with far more intensive management demands, including constant marketing, booking management, guest communication, frequent cleaning, and compliance with local regulations, which are becoming increasingly strict in cities like Barcelona, Lisbon, and Paris.

Calculating The True Net Yield

To make an informed decision, you must calculate the true net yield for both strategies, factoring in all associated costs.

Consider a two-bedroom apartment in the Algarve, Portugal, purchased for €250,000.

| Cost/Income Item | Long-Term Let (Annual) | Short-Term Let (Annual) |

|---|---|---|

| Gross Rental Income | €14,400 (€1,200/month) | €24,000 (80% occupancy @ €100/night) |

| Management Fees | – €1,728 (12%) | – €6,000 (25%) |

| Cleaning & Laundry | – €200 (end of tenancy) | – €3,600 |

| Utilities & Subscriptions | – €0 (tenant pays) | – €1,800 (Wi-Fi, TV, etc.) |

| Maintenance & Repairs | – €600 | – €1,200 (higher wear and tear) |

| Total Annual Costs | €2,528 | €12,600 |

| Net Income | €11,872 | €11,400 |

| Net Yield | 4.75% | 4.56% |

In this example, the short-term let’s higher gross income is significantly eroded by greater operational costs, resulting in a slightly lower net yield than the more stable long-term option. This analysis underscores the importance of looking beyond headline figures to identify the strategy that aligns with your financial goals and operational capacity.

Planning Your Exit Strategy To Maximise Returns

Every successful investment begins with the end in mind. A well-defined exit strategy is not an afterthought; it should be an integral part of your plan before a purchase contract is signed. Deciding when and how to sell your overseas property is as critical as selecting the right market.

Timing the sale to align with market cycles can dramatically impact final returns. Selling during a downturn can erase years of capital growth, whereas exiting at the peak of a seller’s market maximises profit. This requires monitoring local economic indicators, interest rate trends, and housing supply data in your chosen country.

Understanding The Costs Of Selling

When you sell, the headline price is only part of the equation. You must account for several significant costs that will be deducted from your final profit. Understanding these expenses upfront provides a realistic picture of your net gain.

Common selling costs include:

- Estate Agent Commissions: These fees vary significantly by country, typically ranging from 2% to 6% of the sale price.

- Legal and Notary Fees: Essential for the conveyancing process, these can add another 1% to 2% to the total cost.

- Capital Gains Tax (CGT): This is the tax levied on the profit made from the sale.

Navigating Capital Gains Tax Abroad

Capital Gains Tax is often the single largest cost faced when selling a buy to let abroad. The rules are highly specific to each jurisdiction and nearly always depend on your personal tax residency status. CGT is generally calculated on the difference between your sale price and your original purchase price, less allowable expenses such as legal fees and major improvement costs.

The variation between countries is substantial. In Germany, for instance, a property sold after a holding period of more than ten years is exempt from CGT. If sold within that ten-year window, the profit is subject to your personal income tax rate, which could be as high as 45%. In the UK, non-residents pay CGT on gains from residential property but may be entitled to an annual tax-free allowance.

A crucial part of your exit plan involves understanding how CGT is applied in your investment country and whether a Double Taxation Treaty with your home country will provide relief. This knowledge helps determine the optimal holding period for your asset.

Exploring Alternative Exit Strategies

A straightforward sale is not the only option. Depending on your long-term financial goals, other strategies may be more suitable.

One popular approach is to refinance the property after significant equity has been built. This allows you to release capital for further investment without selling the asset, which continues to generate rental income and potential capital appreciation.

Another long-term consideration is passing the property to heirs, which requires careful planning around local inheritance laws and taxes.

Ultimately, a profitable exit is the result of strategic planning. To ensure your calculations are accurate, our guide can help you calculate your total return on investment for real estate by factoring in all potential costs and gains.

Common Questions About Buying To Let Abroad

Entering the international property market inevitably raises questions. Securing clear, practical answers is essential for investing with confidence. Here are some of the most common queries from investors.

What Are The Biggest Hidden Costs?

Beyond the purchase price, you must budget for legal fees, property registration taxes (e.g., Stamp Duty in the UK), notary fees, and currency conversion costs.

Ongoing expenses include property management fees, typically 10-15% of the monthly rent. Additionally, you will be liable for annual property taxes, insurance, and service charges for apartments.

In total, these additional costs can easily add 10-15% to your initial capital outlay. Factoring these in from the start is essential for an accurate net yield calculation.

Is It Better To Buy In My Name Or A Company?

This depends on the country of investment and your personal tax circumstances. In the UK, using a limited company has become the standard structure for professional investors. It allows for the offsetting of 100% of mortgage interest against rental income for tax purposes—a significant advantage individual owners no longer receive. A company also provides liability protection.

The trade-off is the administrative cost and compliance requirements of running a company. It is vital to obtain professional tax and legal advice to determine the optimal structure for your specific situation before making an offer.

Choosing the right ownership structure is a strategic decision, not an afterthought. The tax implications between personal and corporate ownership can be the difference between a profitable investment and a financial burden.

How Can I Manage Currency Risk?

Currency fluctuations can significantly impact your returns. If your rental income is in Euros but your mortgage is in Pounds Sterling, a shift in the exchange rate can increase your monthly payments and reduce your profit margin.

Experienced investors mitigate this by opening a local bank account in the country where the property is located. Rent is paid into this account and used to cover the mortgage and other local expenses. This creates a natural hedge, allowing you to repatriate profits only when the exchange rate is favourable.

For the initial purchase, using a specialist currency exchange service instead of a high-street bank can also result in substantial savings.

At World Property Investor, we provide the data-driven guides and market analysis you need to invest with confidence. Explore our resources to find your next opportunity at https://www.worldpropertyinvestor.com.