Investing in property is a time-tested strategy for building tangible, long-term wealth. Returns are generated from two primary sources: rental income and capital appreciation, where a well-chosen asset increases in value over time. Success, however, is not accidental. It is the result of a clear, disciplined strategy aligned with your financial goals, risk appetite, and desired level of involvement.

Building Your International Property Investment Strategy

Before analysing markets or viewing listings, the first step is to define what a successful investment means for you. Buying property is not a one-size-fits-all endeavour. Your personal objectives will dictate every decision, from the choice of country to the specific type of flat or house you acquire. Your strategy is the compass that guides your capital.

The most successful investors do not find a property and then create a strategy to justify it. They establish a robust strategy first, which then leads them directly to the right asset class and location. This foundational planning prevents emotional decisions and ensures you only acquire assets that align with your financial blueprint.

First, Define Your Primary Investment Goal

Every property investment strategy ultimately targets one of two primary outcomes, or a hybrid of both. Clarifying your priority is a critical first step.

-

Cash Flow (Income): This strategy focuses on generating a regular, predictable income stream from rent. The objective is simple: monthly rental income must comfortably exceed all operational expenses (mortgage payments, taxes, insurance, maintenance). The surplus is your net cash flow.

-

Capital Appreciation (Growth): This strategy involves acquiring property in a location where economic fundamentals suggest values are set to rise significantly. The principal aim is not monthly income, but realising a substantial profit from selling the asset in the future.

For example, a two-bedroom flat in a high-demand area of Manchester could generate a strong rental yield, providing immediate cash flow for an income-focused investor. Conversely, an off-plan apartment in a regeneration zone in Lisbon might offer a lower initial yield but holds significant potential for capital growth as the district matures.

A well-balanced portfolio often incorporates both. A new investor might prioritise a high-yield property to build a financial buffer, whereas a more experienced investor may be better positioned to target a growth-focused asset with a longer-term horizon.

Core Investment Strategies Explored

Once your primary goal is defined, you can select a specific strategy. Each carries distinct risks, management requirements, and return profiles.

Buy-to-Let for Consistent Returns

The classic buy-to-let model is the cornerstone of many property portfolios. It involves purchasing a property to let to long-term tenants, typically on agreements of six months or more. This is an income-focused strategy designed to produce predictable monthly cash flow.

Its appeal lies in its stability. Long-term tenancies reduce void periods and the administrative burden of sourcing new tenants. According to UK government data, the private rented sector has nearly doubled in size since the early 2000s, demonstrating sustained tenant demand. This makes it a popular entry point for anyone new to buying property as an investment.

Capital Growth for Long-Term Wealth

A capital growth strategy requires investing in markets exhibiting strong indicators of future price appreciation. This growth is often driven by major infrastructure projects, positive demographic trends, or a robust local economy. While rental income is a secondary consideration, it should ideally cover holding costs.

This approach demands rigorous market analysis and due diligence. You are not just buying a physical asset; you are investing in a location's economic future. For those seeking to delve deeper, our guides on property investment provide a comprehensive look at market selection.

Short-Term Lets for High Yield Potential

Short-term or holiday lets involve renting a property on a nightly or weekly basis to tourists and business travellers. In prime locations, this strategy can generate significantly higher yields than a standard buy-to-let.

However, this model is far more operationally intensive. Management involves constant guest communication, cleaning schedules, and active marketing. Occupancy rates can be highly seasonal, and local regulations are often stringent. A holiday let in the Algarve or a city-break apartment in Prague can be highly profitable, but it must be operated as a professional hospitality business.

How to Pinpoint Profitable Investment Markets Worldwide

The success of a global property investor is contingent upon one critical factor: location selection. Moving beyond obvious tourist hubs and over-promoted postcodes requires a practical framework for analysing markets with professional rigour. The key is to interpret the economic signals that drive sustainable growth.

Effective market analysis begins with leading indicators—economic drivers that signal future growth and demand. These include infrastructure investment, local employment trends, and sustained population growth. A new transport link or the arrival of a major corporate headquarters can fundamentally transform a neighbourhood’s investment prospects.

Understanding Market Fundamentals

An accurate assessment of price trends and rental demand requires correct interpretation of official data. Credible sources like the UK's Office for National Statistics (ONS), Gov.uk, or national land registries offer invaluable, impartial insights. The objective is to identify long-term patterns in transaction volumes, average sale prices, and rental indices, not just short-term fluctuations.

Historical data provides crucial context. The UK property market, for example, saw residential prices peak in Q3 2007 before the global financial crisis. According to ONS data, average prices had risen sharply, creating a volatile cycle. While the market eventually stabilised, this history demonstrates both market cyclicality and resilience.

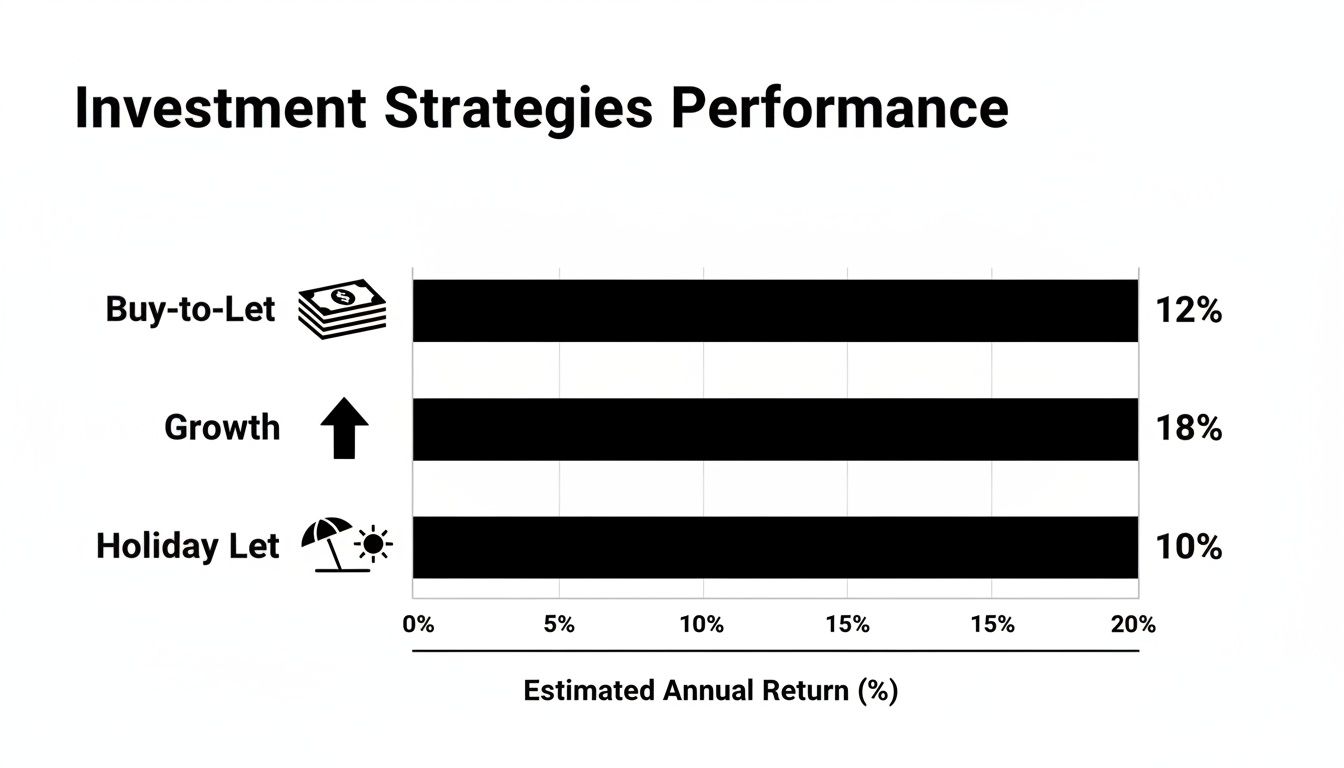

This chart illustrates the typical performance of different property investment strategies.

As shown, different strategies yield varied returns, reinforcing the need to align market choice with specific financial objectives. A high-growth strategy demands a very different market environment from one suited to steady income generation.

Established vs. Emerging Markets

A common dilemma for global investors is choosing between the stability of an established market and the high-growth potential of an emerging one. Each offers a distinct risk-reward profile.

A direct comparison clarifies which path aligns with your investment thesis.

Established vs. Emerging Market Comparison for Property Investors

| Characteristic | Established Markets (e.g., UK, Germany) | Emerging Markets (e.g., Turkey, parts of Eastern Europe) |

|---|---|---|

| Growth Potential | Slower, more predictable capital growth. | Potential for rapid capital appreciation. |

| Rental Income | Stable, reliable rental income streams. | Often higher rental yields, but can be more volatile. |

| Risk Profile | Lower risk due to stable economies and legal systems. | Higher risk from currency fluctuations and political instability. |

| Liquidity | High liquidity; easier to buy and sell assets. | Lower liquidity; can be harder to exit the market quickly. |

| Legal Framework | Transparent and mature property ownership laws. | Legal frameworks can be less developed or subject to change. |

| Best For | Conservative investors prioritising capital preservation. | Investors with a higher risk appetite seeking strong returns. |

The choice ultimately depends on your personal risk tolerance and investment horizon. An investor seeking stable, reliable income might favour a flat in Berlin, whereas one targeting rapid growth might look to an up-and-coming district in Warsaw.

Your Market Vetting Checklist

Before committing to a location, conduct a systematic review to identify any potential red flags. A disciplined approach is essential when buying property as an investment from overseas.

- Economic Health: Is the local economy diverse and expanding? Review unemployment rates and major employers. A town reliant on a single industry presents a significant risk.

- Population Trends: Is the population growing? Expanding cities require more housing, which supports both rental demand and property values.

- Rental Yields & Demand: What are the average gross and net yields? Crucially, is there a structural undersupply of rental properties? Our detailed guide on the best buy-to-let locations offers further insight.

- Supply Pipeline: Are major new residential developments planned? An oversupply of new stock can suppress prices and rents.

- Landlord Regulations: Are local laws landlord-friendly? Familiarise yourself with tenancy laws, eviction procedures, and any rent control measures.

- Infrastructure Investment: Are new transport links, schools, or hospitals under construction? These are powerful indicators of future growth.

By combining macroeconomic analysis with this granular, on-the-ground research, you can look past market hype and identify locations with strong, long-term fundamentals. This disciplined method is key to building a resilient and profitable international property portfolio.

Mastering Finance, Taxes, and Legal Structures

Identifying a promising market is a critical step, but converting that opportunity into a profitable asset depends on mastering the financial and legal mechanics. Correctly structuring the finance, tax, and legal ownership is what separates a successful long-term investment from a costly error.

Many novice investors falter here. They focus on the property itself but underestimate the impact of these three elements on net returns. A professional approach requires a clear understanding of funding options, tax liabilities, and the most efficient legal structure to hold the asset. Every country has its own regulatory framework, making professional advice non-negotiable for any serious international investor.

Securing Your Investment Capital

A realistic funding strategy must be in place before you make an offer. For international buyers, the financing landscape can be more complex, but several established paths exist.

-

Non-Resident Mortgages: Many global banks and specialist lenders offer mortgages to foreign nationals. Expect stricter lending criteria, including a larger deposit (typically 30-40%), slightly higher interest rates, and rigorous checks on your income and credit history in your home country.

-

Releasing Equity: A common strategy is to remortgage an existing property to release equity. This allows you to purchase the international property with cash, circumventing the complexities of securing foreign finance.

-

Private Lenders and Bridging Loans: For non-standard properties or transactions requiring speed, private financing can be a solution. It comes at a significantly higher cost and is best used strategically to secure a deal before refinancing onto a conventional mortgage.

Your choice of funding directly impacts your cash flow and overall return. It is vital to model the costs of each option. For a deeper analysis, review our complete guide on financing an investment property.

Navigating the Complex World of Property Taxes

Tax is one of the largest costs for a property investor, impacting the transaction at purchase, during ownership, and upon sale. Tax regimes vary enormously between countries, and sometimes even between regions or cities.

The primary taxes to consider are:

-

Transaction Taxes: A tax levied upon purchase. In the UK, this is Stamp Duty Land Tax (SDLT), with rates tiered according to the property's value. Spain has a similar tax, the Impuesto de Transmisiones Patrimoniales (ITP).

-

Income Tax: Rental income is almost always taxable. The key is to determine where it must be declared—in the property's jurisdiction, your country of residence, or both. Double-taxation treaties often exist to prevent the same income being taxed twice.

-

Capital Gains Tax (CGT): When you sell a property for a profit, the gain is usually subject to CGT. Rates and allowances differ significantly. The UK, for example, has a specific CGT allowance, and the rate is linked to your income tax band, whereas other countries may apply a flat rate.

Real-World Example: A Spanish Buy-to-Let

An investor buys a flat in Valencia, Spain, for €200,000. They immediately face the ITP transfer tax, around 10% in that region (€20,000). If they generate €12,000 in annual rental income, a non-EU resident must pay non-resident income tax (IRNR) at a flat rate of 24% on the gross income. Upon selling, any profit is liable for Spanish capital gains tax. This illustrates how taxes erode returns at every stage.

Choosing the Right Ownership Structure

One of the most critical strategic decisions is how you legally own the property. This choice has significant implications for your tax liability, personal asset protection, and inheritance planning.

For most individual investors, the choice is between two primary options:

-

Personal Name: Purchasing as an individual is the simplest method, with lower administrative costs. The main drawback is that all profits are taxed as personal income, and you are personally liable for any debts associated with the property.

-

Limited Company / Special Purpose Vehicle (SPV): Establishing a company specifically to hold property has become a popular strategy, particularly in jurisdictions like the UK. While it involves setup and annual running costs, it offers distinct advantages. Corporation tax rates are often lower than higher-rate personal income tax, and it creates a legal separation between your personal assets and your investment portfolio. For higher-rate taxpayers building a portfolio, this structure is often more tax-efficient.

The optimal structure depends on your personal financial circumstances, long-term objectives, and the specific tax laws of both your home country and the investment location. Consulting with a cross-border tax advisor and a solicitor is not merely advisable—it is essential.

Running the Numbers and Conducting Due Diligence

Once you have identified a promising market and a specific property, the analytical work begins. To move from an online listing to a profitable asset requires a forensic level of scrutiny. This is the due diligence phase, where you must look beyond professional photography and verify every claim, assumption, and financial projection.

Successful investors are disciplined at this stage. They set aside emotion and place the property under a microscope to uncover hidden defects, calculate its true operational costs, and confirm its genuine investment potential. This process is about capital protection and ensuring you are making a fully informed decision.

Performing a Comparative Market Analysis

Before making an offer, you must ascertain whether the asking price reflects fair market value. This is achieved through a Comparative Market Analysis (CMA), a methodical process of comparing your target property to similar properties that have recently sold in the immediate area.

You are looking for "comparables"—properties that are as closely matched as possible in terms of:

- Location and postcode

- Property type (e.g., flat, terraced house)

- Number of bedrooms and bathrooms

- Square footage or overall size

- Condition and age

By analysing the final sale prices of at least three to five comparable properties, you can establish an evidence-based valuation. This protects you from overpaying and provides a strong, data-backed position for negotiation.

Physical Inspections and Building Surveys

Regardless of how a property appears online, a professional physical inspection is non-negotiable, particularly for an overseas investor. You should engage a chartered surveyor to conduct a thorough building survey. Their report is your primary defence against discovering costly, hidden defects after purchase.

Key areas a surveyor will investigate include the building's structural integrity, the condition of the roof, signs of damp, the state of the electrical and plumbing systems, and any indicators of subsidence. For an international investor, this independent assessment provides essential on-the-ground intelligence that cannot be gained remotely.

A detailed survey may cost several hundred pounds, but it can save you tens of thousands. If a survey uncovers significant issues like a failing roof or rising damp, it does not automatically disqualify the property. Instead, it becomes a critical tool for renegotiating the purchase price.

Essential Legal Due Diligence

While the surveyor inspects the physical asset, your solicitor will conduct vital legal checks to ensure the property has a clean and marketable title. This legal due diligence is fundamental to protecting your investment from future complications.

These checks typically include:

- Title Search: This confirms the seller is the legal owner and has the right to sell. Critically, it uncovers any liens, debts, or legal claims registered against the title that could become your liability.

- Planning Permissions: Your solicitor will review local planning records to verify that any extensions or alterations to the property were completed with the correct legal permissions. Unauthorised works can become a major liability.

- Local Searches: This involves checking with the local authority for any planned developments, such as new roads or zoning changes, that could negatively impact the property's value or the quality of life for your tenants.

Calculating Your True Return on Investment

Finally, you must run the numbers to forecast your true net yield and potential return on investment. This analysis goes far beyond simply looking at the potential rent. Affordability is a key metric; data from bodies like Schroders shows that the ratio of UK house prices to average earnings has been historically high, indicating a risk of market overvaluation that demands careful financial modelling.

While recent UK House Price Index data published by the ONS shows average prices, factors such as stamp duty and regulations can compress investor returns. You can explore more insights on UK house price affordability from Schroders.

To get an accurate forecast, you must project all potential income and subtract all anticipated costs.

- Projected Rental Income: Research the local market to establish a realistic monthly rent. Do not rely solely on the agent's estimate; verify it against comparable online listings.

- Running Costs: Factor in all expenses. This includes mortgage payments, insurance, property management fees (typically 10-15% of rent), a maintenance budget (a common estimate is 1% of the property’s value annually), and potential void periods between tenancies.

Only by subtracting these comprehensive costs from your income can you calculate your true net yield. You can learn more about how to calculate your return on investment for real estate in our detailed guide. This final calculation confirms whether the property truly aligns with the financial goals set at the outset.

Managing Your Property and Planning Your Exit

Acquiring the keys to your investment property is a significant milestone, but it marks the halfway point of the investment lifecycle. The distinction between a high-performing asset and one that consumes your time and capital lies in what follows: proactive management and a pre-defined exit strategy.

This is the operational reality of property ownership, particularly for overseas investors. Effective management transforms a physical building into a reliable financial asset. It protects the property's value, ensures consistent rental income, and maintains legal compliance. Neglecting this phase can lead to returns being eroded by tenant issues, prolonged vacancies, and unforeseen repairs.

Self-Management vs Professional Agency

An early decision is whether to manage the property yourself or engage a professional agency. Each path has major implications for your time, costs, and peace of mind.

Self-management offers maximum control and avoids agency fees, which typically range from 10-15% of the monthly rent. However, this is only a viable option if you live in close proximity, possess a thorough understanding of local tenancy law, and have a network of reliable tradespeople. The workload can be substantial, from tenant vetting and rent collection to handling emergency maintenance calls.

For most international investors, hiring a professional management company is the default and most prudent choice. They handle all day-to-day operations, ensuring your asset is properly maintained and legally compliant.

A reputable management agency should handle:

- Tenant Sourcing and Vetting: Marketing the property, conducting viewings, and performing comprehensive background and credit checks.

- Rent Collection and Financials: Ensuring timely rent payment and providing clear, regular financial statements.

- Maintenance and Repairs: Utilising their network of vetted contractors to resolve issues efficiently, thereby protecting the property's condition.

- Legal Compliance: Staying current with landlord-tenant legislation, managing deposit protection schemes, and handling eviction processes if necessary.

A high-quality local partner is invaluable. When vetting agencies, request references from other overseas clients, check online reviews, and confirm their accreditation with a recognised professional body in that country.

Defining Your Exit Strategy from Day One

Your exit strategy should not be an afterthought; it is an integral part of your investment plan from the beginning. Knowing how and when you intend to liquidate your investment influences the type of property you buy and the market you enter. Your strategy should be flexible enough to adapt to market conditions but clear enough to guide your decisions.

For most property investors, there are two primary exit routes.

Selling for Capital Growth

This involves selling the property after a period of appreciation to realise a capital gain. The holding period might be five, ten, or twenty years, depending on your financial goals and market performance. This approach is best suited to properties in areas with strong economic growth prospects, new infrastructure, and positive demographic trends.

When planning a sale, you must factor in costs such as capital gains tax, estate agent fees, and legal expenses, all of which will reduce your net profit. The UK, for instance, remains a top European market attracting global investors. While regional buy-to-let yields are strong—with sources reporting averages of 5.89% in the North West and 5.77% in the West Midlands—the long-term trajectory of house prices also underscores its appeal for capital growth.

Holding for Long-Term Income

The alternative is to hold the property indefinitely, using it to generate a steady income stream, perhaps as part of a retirement plan. Here, the priority is high, sustainable rental yields and strong tenant demand, rather than speculative growth. Properties best suited for this are typically located in stable, established rental markets with low vacancy rates. Even with this strategy, it is prudent to review the property’s performance periodically to ensure it continues to meet your financial targets.

Ultimately, your exit plan connects back to your original investment goals. For investors considering new-builds, it is worth exploring the pros and cons of buying off-plan properties as part of that initial strategy. By planning your exit from day one, you maintain control over the investment's entire lifecycle, enabling you to act decisively when the time is right.

Common Questions About Property Investment

Embarking on property investment, especially in international markets, raises a common set of questions. Here are clear, practical answers to the most frequent queries from global investors, designed to provide clarity as you proceed.

What Is a Good Rental Yield for an Investment Property?

There is no single figure that defines a "good" rental yield; it is entirely dependent on the specific market and associated risk.

In a mature, prime city like London or Berlin, a gross yield of 3-4% is often considered solid. The lower yield is compensated by the prospect of strong, reliable capital growth and exceptionally high tenant demand. Investors are essentially trading higher cash flow for lower risk and long-term stability.

Conversely, in regional UK cities like Manchester or emerging hotspots such as Lisbon, sophisticated investors may target yields of 6-8% or higher. This stronger cash flow is the return for accepting potentially slower or more volatile capital growth.

As a general rule, a gross yield exceeding 5% warrants further investigation. However, the most critical metric is always the net yield—the return after all expenses, including taxes, maintenance, and potential void periods, have been deducted.

Can I Invest in Property Abroad Without Visiting?

Yes, it is entirely feasible to invest from overseas in the modern market, but success is contingent on the quality of your professional team. You must appoint trusted, independent experts to act as your representatives on the ground.

Your core team should include:

- A Sourcing Agent: A local specialist who understands your investment criteria and can vet properties on your behalf.

- An Independent Solicitor: A legal professional who represents your interests exclusively, conducting thorough due diligence on the property title and contracts.

- A Chartered Surveyor: A qualified professional who will perform a comprehensive physical inspection to identify any defects not visible remotely.

High-definition virtual tours and video conferencing have simplified remote viewings. The critical element is to rigorously vet every professional you engage. Verify their credentials, request references from their past overseas clients, and never simply accept the team recommended by a developer or selling agent.

Investing from a distance demands a heightened level of due diligence. The quality of your professional team directly correlates with the security of your investment. Trust is valuable, but verification is essential.

What Are the Biggest Risks for Overseas Property Investors?

Beyond standard market risks like an economic downturn, international investors face a unique set of challenges.

Currency fluctuation is a primary risk. An adverse movement in the exchange rate can significantly erode your rental income or your final profit when repatriating funds to your home currency.

Sudden legal or tax changes in the investment jurisdiction can also impact returns with little warning. This risk is typically greater in emerging markets compared to more established, stable economies.

Finally, poor local management is a common pitfall, leading to extended void periods, property deterioration, and costly operational issues. These risks can be mitigated through meticulous planning, expert professional advice, currency hedging strategies, and the careful selection of a top-tier property management agency from the outset.

Ready to find your next global property investment? The experts at World Property Investor provide the in-depth market analysis and practical guides you need to invest with confidence. Explore our insights at https://www.worldpropertyinvestor.com.