Most investors start with the wrong question. They ask, “Can foreigners buy property in this country?” That sounds sensible, but it's often the least useful part of the analysis.

A market can look open on paper and still be awkward, expensive, or strategically risky in practice. Another market can look restrictive, yet still offer workable access through leaseholds, local entities, or regulated investment vehicles. The primary work sits in the gap between legal permission and commercial viability.

That gap matters because property returns aren't created by legal title alone. They come from what you can buy, how you can hold it, what compliance it triggers, how easily you can finance it, and whether you can sell it later without frightening off the next buyer.

For serious investors, foreign ownership restrictions by country should never be read as a simple traffic-light list. They should be read as a market access map.

Beyond Can You Buy Understanding the Real Rules

The weakest property screens in cross-border investing often start with a legally correct answer. “Yes, foreigners can buy” sounds useful, but it tells you almost nothing about access, execution, or exit.

A serious investor needs a narrower set of questions: which assets are restricted, which legal structures remain available, and what tax or compliance burden comes attached? Those three variables shape pricing power, financing options, holding costs, and resale liquidity. They belong in underwriting from day one, not in a lawyer's memo after terms are agreed.

Three filters decide whether a market is investable

The first filter is the asset itself. A jurisdiction may allow foreign ownership of a city apartment while limiting farmland, shoreline plots, low-density housing stock, or land near strategic infrastructure. That distinction affects more than legal eligibility. It changes what inventory you can buy, who your future buyers are, and whether redevelopment upside is available.

The second filter is the holding structure. Direct title, a local company, a regulated fund, a nominee, or a long lease can all produce different outcomes on tax, financing, liability, and inheritance. Formal access through the wrong structure can still be poor access if local banks refuse to lend against it or if the next buyer discounts it.

The third filter is transactional friction. Anti-money-laundering checks, foreign investment approvals, beneficial ownership disclosures, exchange controls, and registration procedures all consume time and money. In some markets, those frictions matter as much as the title rules because they affect cash timing and repatriation. For investors dealing with South African flows, practical guidance on strategies for FX compliance in SA can be more useful than a generic ownership summary.

This is the point many country lists miss.

The legal answer and the investable answer often diverge. The World Bank's investment policy work makes the same distinction in a different form: formal openness does not eliminate entry conditions, approvals, or sector-specific limits that change how foreign capital can participate in an asset class (World Bank investment policy resources).

Why headline guidance misprices risk

The UK shows why a binary framework fails. Foreign buyers can acquire property there, but that headline misses the operational issues that matter to investors: asset-level due diligence, disclosure rules, tax treatment, and the growing relevance of national security review around sensitive land or infrastructure-linked transactions. An investor buying central London residential stock faces a very different risk profile from one assembling land near strategic assets, even within the same legal system.

Australia makes the same point from a different angle. International capital often views it as open because institutions are strong and demand is deep. In practice, access is highly conditional by buyer type and asset type, which is why a market brief on foreign property investment in Australia is useful. The main question is not whether entry is possible. It is which version of entry remains commercially sensible after approvals, taxes, and use restrictions are accounted for.

Practical rule: assess foreign ownership restrictions as a market-access problem. Start with the asset, then the structure, then the friction. That sequence gets you closer to actual ROI than any simple yes-or-no country list.

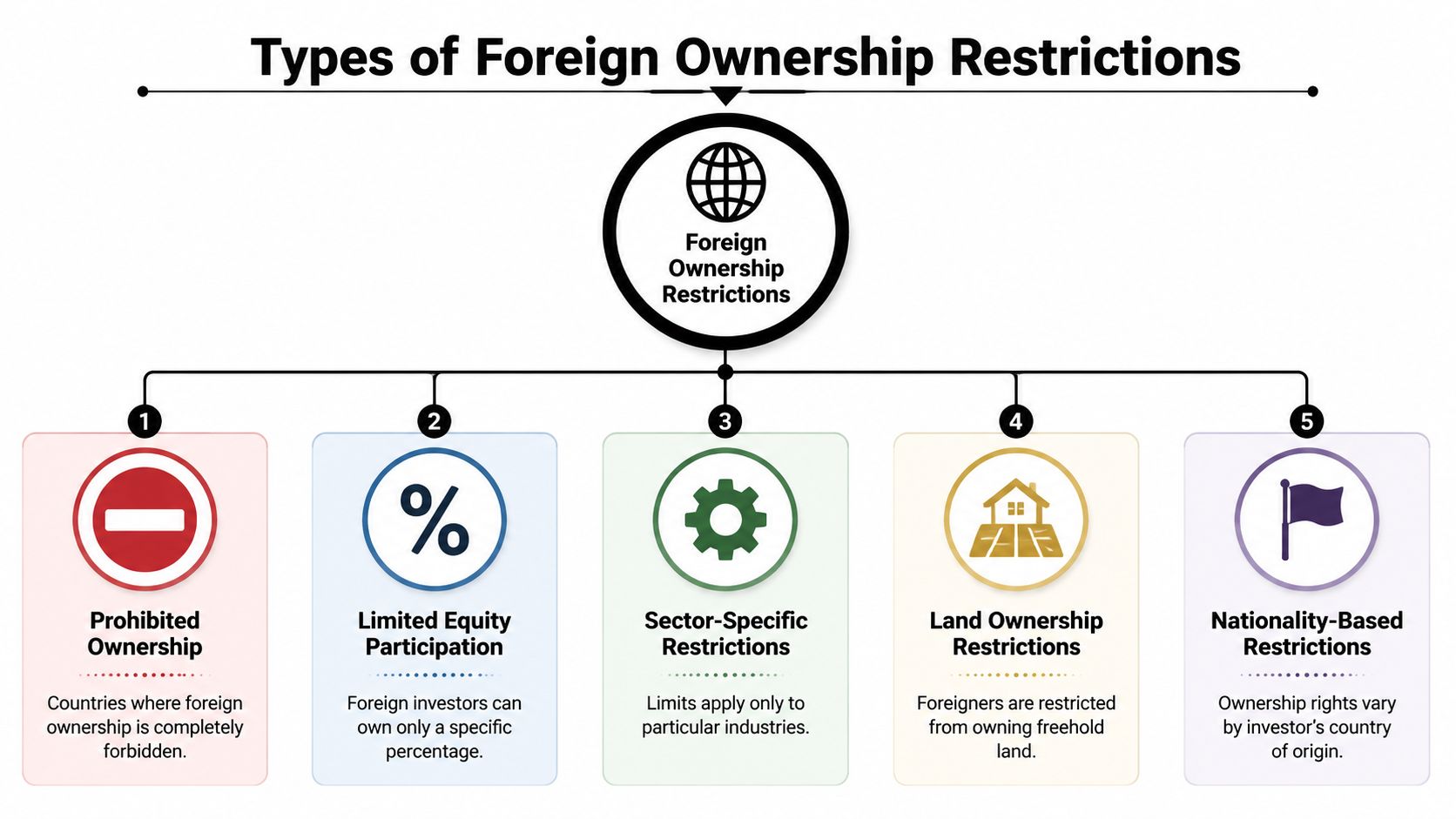

The Main Types of Foreign Ownership Restrictions

Foreign ownership restrictions by country usually fall into a handful of recurring categories. Once you know the categories, the legal language becomes easier to decode.

Prohibited ownership and limited equity

The hardest restriction is the direct ban. That's where foreign investors can't own certain property, or can't own it in the same way as citizens. This often appears in land law rather than corporate law.

A softer version is the equity cap. Investors can participate, but only up to a defined ownership share or through a joint venture. In property terms, that tends to matter more for development companies, strategic land, or mixed-use projects linked to regulated sectors than for a standard flat purchase.

Sector and land-specific controls

Some jurisdictions don't care much about a city-centre apartment, but care a great deal about farmland, coastal land, natural resources, or sites near infrastructure. That distinction is becoming more important than country-level yes-or-no guidance.

The World Bank reports that nearly 80% of economies in its database restrict foreign companies from entering at least some sectors, and that foreign-owned company formation takes longer and requires more steps in 94% of economies through screening and related mechanisms, rather than through blanket bans alone, according to its global policy analysis. For investors, that means the permission may exist, but the route is rarely frictionless.

Screening and approval mechanisms

These are often mistaken for bans, but they're different. A screening regime allows the state to review, condition, delay, or block transactions that raise strategic concerns.

That matters because review risk affects pricing. If a deal may need approval, the buyer faces longer timelines, more legal work, and more execution uncertainty. Sellers may favour domestic bidders or buyers with cleaner regulatory profiles.

Residency, leasehold, and nationality rules

Some markets tie ownership rights to residency status. Others channel foreign demand into leasehold rather than freehold ownership. If you're comparing legal control, resale prospects, and financing options, the distinction between the two is fundamental. This breakdown of freehold vs leasehold is useful because many countries restrict foreigners less by excluding them entirely and more by limiting the form of title they can hold.

A final category is nationality-based targeting. The restriction doesn't apply to all foreigners equally. It applies differently depending on where the buyer is from, what entity they use, and whether the land has strategic sensitivity.

The headline rule tells you whether entry is possible. The category of restriction tells you whether the investment is bankable, scalable, and saleable.

Open Conditional and Restricted Markets A Comparison

The biggest mistake in cross-border property investing is treating market access as a yes-or-no question. Capital usually gets blocked, diluted, or delayed elsewhere. The core dividing line is threefold: what foreigners can buy, which legal structures still work, and how much transaction friction cuts into returns.

Foreign ownership regimes at a glance

| Country | Market Type | General Rule for Non-Residents | What actually shapes investor access |

|---|---|---|---|

| UK | Open | Broad access to property ownership | Few title barriers, but AML checks, beneficial ownership disclosure, and deal-specific scrutiny can slow execution |

| Australia | Conditional | Access is possible, subject to review and policy settings | Approval risk, asset-type limits, and rules that can change with housing policy |

| Canada | Conditional | Access varies by property type, location, and current policy | Temporary restrictions, provincial variation, and tax treatment affect feasibility |

| Switzerland | Restricted | Non-resident ownership is allowed only within narrow parameters in many cases | Permit controls, holiday-home rules, and location caps reduce scalability |

| Thailand | Restricted | Foreigners generally cannot own land directly | Leasehold, condominium quotas, and company structures determine actual control |

| UAE | Mixed | Ownership rights depend on the emirate and designated zones | Freehold areas, leasehold areas, and entity choice affect title, financing, and exit options |

This framework is meant for portfolio screening, not legal sign-off.

Open markets still carry execution risk

Open markets deserve less credit than they often get. They are easier to enter, but they still impose costs that matter to net returns.

In the UK, a foreign buyer can generally acquire residential or commercial property without a blanket ownership ban. The more relevant risks sit in source-of-funds checks, registration and disclosure obligations, tax treatment, and any review triggered by the nature of the asset or buyer. For an investor, that changes underwriting. Capital can be deployed, but the timetable may stretch, advisers' fees rise, and seller confidence weaken if compliance work drags.

That matters most for competitive deals. A bidder with avoidable diligence problems often loses before price becomes the deciding factor.

Conditional markets reward investors who read policy, not just statutes

Conditional markets are often the most misunderstood category because the law may permit entry while policy narrows the investable universe. Australia and Canada illustrate the point. Access exists, but not on equal terms across all assets, buyer profiles, and political cycles.

The practical consequence is concentration risk. If a government channels foreign demand away from existing housing, toward specific development outcomes, or into selected structures, investors have fewer assets that are both legal and economically attractive. A market can look open on paper and still produce weak deployment capacity in practice.

South Korea is a useful comparison because the rules are more open than many investors assume, yet local procedure, reporting, and financing realities still shape execution. This guide to buying a house in South Korea shows why formal permission is only the starting point.

Mexico often fits the same analytical lesson from a different legal angle. Foreign participation is possible, but structure matters more in sensitive zones and coastal markets. Resources focused on simplifying Mexican real estate for expats are useful because they translate the legal wrapper into day-to-day ownership and closing risk.

Restricted markets can produce returns, but only if structure survives the exit

Restricted markets are not automatically unattractive. They are less forgiving.

In Switzerland, Thailand, and parts of the UAE, the issue is rarely just whether a foreign buyer can get exposure. The harder questions come later. Does the investor hold title, a long lease, or an interest through a local entity? Will a bank lend against that right? Can rental income be remitted efficiently? Will the next buyer accept the same structure without a pricing discount?

Those questions separate theoretical access from bankable access. A high headline yield loses value fast if the ownership form is hard to finance, difficult to transfer, or vulnerable to rule changes. In restricted markets, transactional friction is not a side issue. It is part of the asset.

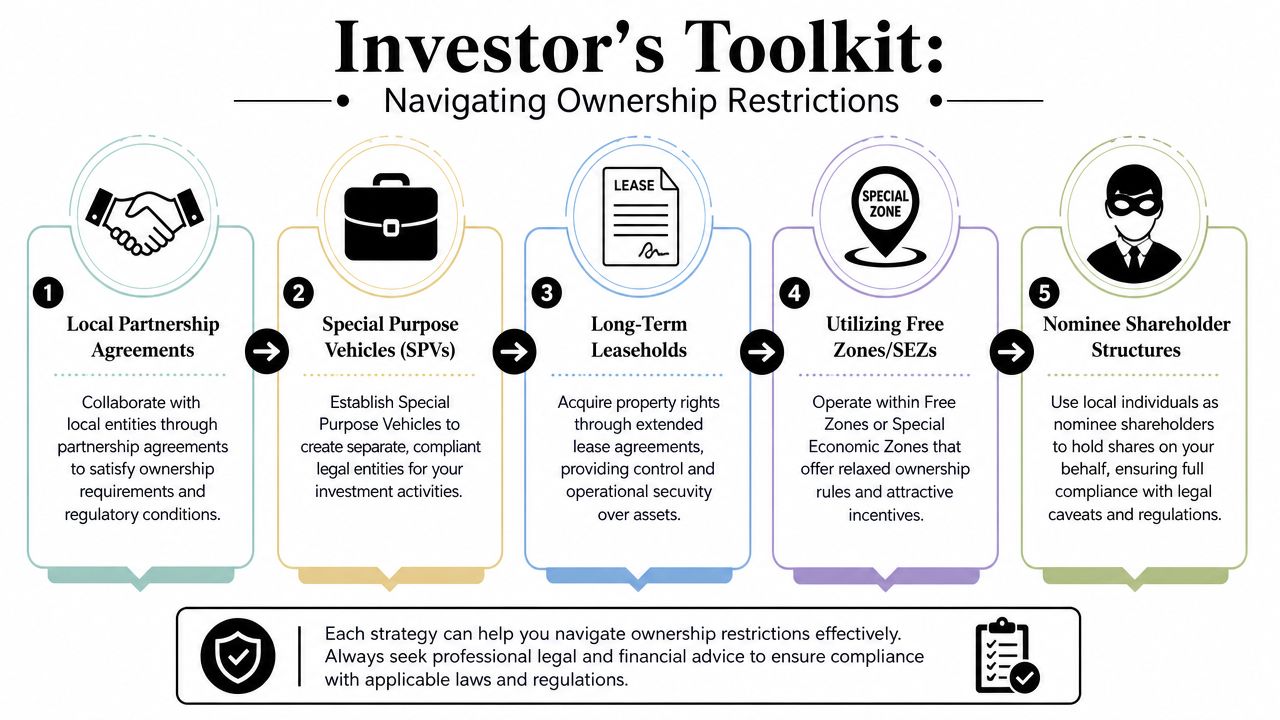

Navigating Restrictions The Investor's Practical Toolkit

Once a market moves from open to conditional or restricted, structure becomes the investment thesis. A weak structure can turn a good location into a bad deal.

A lot of investors learn that too late. They focus on entry and neglect durability. The better approach is to decide first what legal exposure you need: title, use rights, development rights, rental income, or capital appreciation.

The following visual captures the core playbook.

Structures investors actually use

- Local company vehicle: A buyer incorporates locally and acquires through that entity. This can improve administrative fit, but it adds accounting, governance, tax filing, and beneficial ownership disclosure.

- Long-term leasehold: Useful where freehold is restricted. It can provide economic use without direct land title, but value at exit depends heavily on remaining lease term and enforceability.

- Fund or REIT exposure: This avoids many direct-acquisition issues. It also reduces control over asset selection and timing.

- Partnership with a domestic party: Sometimes necessary, often risky. Governance rights, dividend policy, deadlock clauses, and exit rights matter more than the headline share split.

- Nominee or layered holding arrangements: These may appear convenient, but they can create severe enforceability and beneficial ownership problems if local law, banks, or future buyers reject the structure.

The hidden cost is compliance friction

Often, a primary barrier for investors is not a legal ban but the compliance burden around a permitted deal. Analysis of recent US property bills points to a move towards nationality-based targeting and reporting requirements rather than universal prohibitions, creating hidden costs and liquidity risks even for allowed purchases, as discussed in this policy tracker on US property restriction bills.

That matters in practice because every extra filing, disclosure step, bank query, or approval condition affects timing and resale. A structure that gets you in the door may still be a poor investment if it scares lenders or narrows the future buyer pool.

A legally valid structure isn't enough. The structure also has to survive lender scrutiny, tax review, and an eventual sale process.

For buyers assessing Latin American routes into real estate, practical explainers such as simplifying Mexican real estate for expats are helpful because they show how local structures can differ sharply from what overseas investors expect.

A specialist international real estate lawyer should review structure before terms are agreed, not after money has been committed.

A short briefing on cross-border structuring is useful before moving into any transaction-level review:

Spotlight on Key Established Markets

The safest-looking markets often create the most expensive false confidence. In established jurisdictions, foreign buyers usually can buy. The harder question is what they can buy, through which structure, and with how much compliance drag on entry, financing, and exit.

That is the dividing line between markets that are merely open on paper and markets that are investable at target returns.

UK openness with reporting and screening

The UK remains one of the more accessible established markets for foreign capital. There is no general ban on overseas buyers acquiring residential or commercial property. The constraint sits in transparency and source-of-funds scrutiny. The Register of Overseas Entities at Companies House has reduced the privacy once associated with offshore holding structures, and anti-money-laundering checks can slow closings if ownership chains or funds flow are opaque.

For investors, the consequence is straightforward. The UK is open, but not frictionless. An overseas company can still hold the asset, yet disclosure, verification, and ongoing filing obligations now affect transaction timing and administrative cost. That matters most for buyers using layered entities, nominee arrangements, or capital coming from multiple jurisdictions.

This also affects resale. A structure that satisfies legal ownership rules but creates extra diligence work for the next buyer can narrow the purchaser pool and weaken pricing.

The United States as an asset-specific market

The United States is still described too often as a single open market. It functions more like a patchwork in which restrictions depend on asset type, location, and the identity of the ultimate buyer.

That shift is visible in state-level legislation focused on farmland, land near military sites, and property close to critical infrastructure, as tracked in this Multistate review of recent foreign ownership legislation. The practical point is not only political risk. It is underwriting risk. A logistics site, energy-adjacent parcel, or rural land acquisition can face a different approval and exit profile from a standard multifamily asset in a major city.

Lenders and future buyers respond to that distinction. If an asset sits in a category that may attract scrutiny, legal ownership may still be possible, but diligence costs rise, financing can tighten, and future liquidity becomes less certain.

In the US, market access is increasingly defined by what the asset is and where it sits, not just by whether a foreign buyer is allowed to own property in general.

Australia as a conditional benchmark

Australia shows how a mature market can stay open to foreign capital while directing it toward preferred asset classes. The rules are clearer than in many jurisdictions, but they are also more interventionist. Foreign buyers often face review requirements through the Foreign Investment Review Board, and the outcome depends heavily on whether the property is new residential stock, existing housing, commercial real estate, or development land, as set out by the Australian Taxation Office guidance for foreign investors.

That structure changes the investment case in two ways. First, access is often easier for asset types aligned with housing supply or economic development goals. Second, taxes and application fees can materially change net yield, especially for residential strategies with thin operating margins.

Australia is a useful benchmark because it makes policy intent explicit. Investors comparing it with designated ownership models in the Gulf can see the contrast quickly. In Dubai, access often depends on buying in approved areas through a clearly defined foreign ownership framework, which is why many cross-border buyers review guides on how to invest in Dubai real estate alongside more tightly screened markets like Australia.

For serious investors, the lesson across all three markets is the same. A country can be institutionally strong and still impose enough friction, disclosure, asset screening, and tax cost to change the return profile materially.

Opportunities and Hurdles in Emerging Markets

Cheap entry prices do not create access. In many emerging markets, the harder question is whether the rights you buy can survive policy changes, administrative delay, and a difficult resale process.

That is why a simple country list gives investors false comfort. Market access usually depends on three variables. Which property types are restricted, which legal structures remain available, and how much transaction friction sits between headline yield and actual cash return.

Opportunity often sits inside narrow channels

Emerging markets rarely operate as fully open or fully closed systems. They tend to permit foreign capital through specific asset classes, geographies, or holding structures.

In the Gulf, designated ownership zones can make one district investable while the rest of the country remains off-limits or subject to different rights. In parts of Southeast Asia, foreign buyers may be blocked from direct land ownership but still gain exposure through long leases, strata or condominium titles, or locally incorporated vehicles. In parts of Eastern Europe and the Balkans, foreign investment policy may look permissive on paper, while title registration quality, planning enforcement, and court efficiency determine whether that access has practical value.

The investment implication is straightforward. The addressable market is usually smaller than the marketing narrative.

Policy risk often matters more than entry price

The primary risk in emerging markets is not legal complexity alone. It is legal complexity combined with shifting administrative practice.

A market may welcome foreign buyers during a capital-raising cycle and tighten rules once land values rise, political pressure builds, or strategic assets come into focus. Coastal parcels, border regions, logistics corridors, farmland, and sites near energy or transport infrastructure face this risk most often because they sit closer to national policy priorities.

Compare that with mature markets discussed earlier. In more institutionally stable jurisdictions, investors still face taxes, disclosure obligations, and compliance screening, but the rules are usually clearer and enforcement is more predictable. In many emerging markets, the opposite is true. Formal access may exist, yet approvals, title procedures, and exit rights can depend heavily on local implementation.

That changes underwriting. A higher nominal yield does not compensate for an ownership structure that banks will not finance, courts may not enforce quickly, or future buyers do not trust.

What investors should test before committing capital

A workable screen for emerging markets is stricter than a simple foreign-ownership check:

- Enforceability of title: Confirm that the ownership or lease right can be registered, defended, and transferred without relying on informal relationships.

- Quality of the access structure: Test whether the permitted route, such as leasehold, condo title, nominee risk, or a local company, holds up at refinance and resale.

- Exit liquidity: Ask who the next buyer is. If the structure narrows the buyer pool to cash investors or domestic insiders, the discount will show up on exit.

- Currency and repatriation controls: Rental income and sale proceeds matter less if conversion, remittance, or dividend extraction is slow or restricted.

- Administrative friction: Approvals, notarisation, licensing, local tax registration, and reporting duties can turn a legally open market into an operationally expensive one.

Investors who perform well in these markets do not pay for growth stories alone. They pay for enforceable rights, usable structures, and a transaction process that does not erode returns after closing.

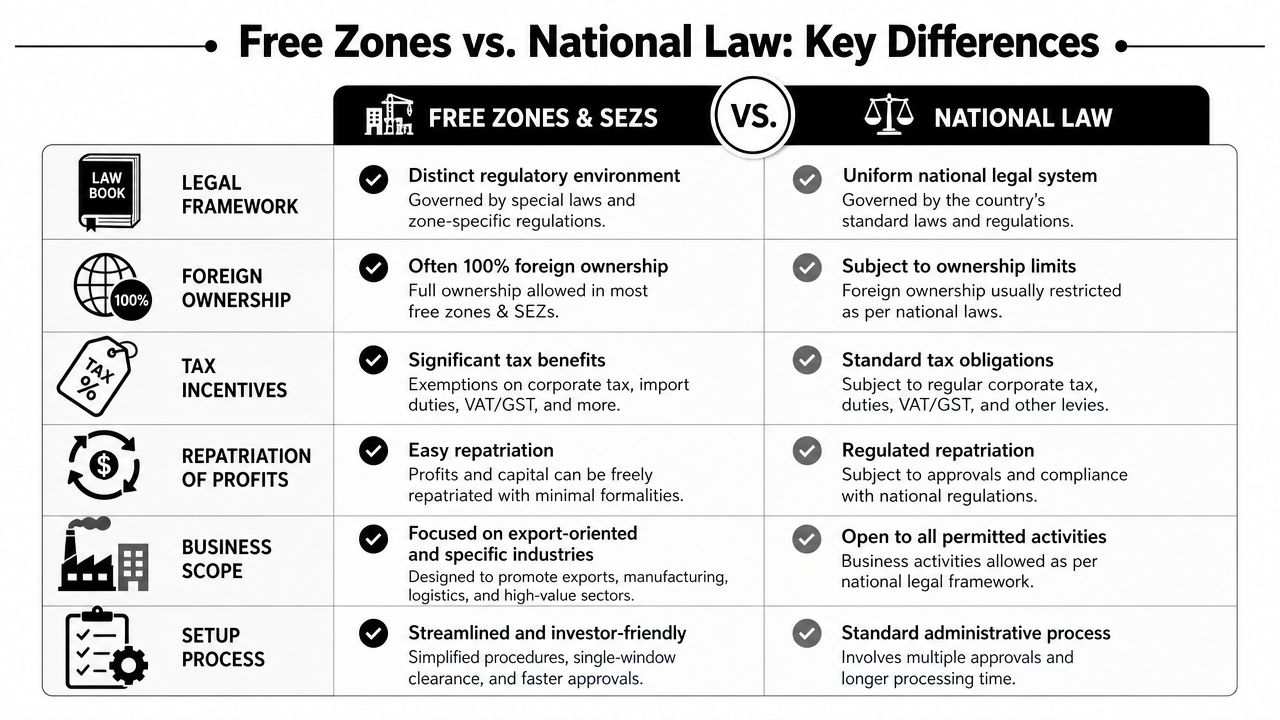

The Role of Free Zones and Special Economic Zones

Free zones and special economic zones can change the investment equation completely. They create carved-out legal environments inside countries that may otherwise be more restrictive.

For foreign buyers, that matters because the zone, not just the country, can determine what ownership rights are available.

Why zones attract foreign capital

A free zone typically aims to reduce friction. It may offer clearer setup rules, greater foreign ownership rights, more predictable administration, and easier profit repatriation than the wider domestic regime.

For property investors, the attraction is straightforward:

- Clearer foreign access: The zone may permit ownership rights that are harder to secure elsewhere in the country.

- Administrative efficiency: Transaction processes can be more standardised.

- Commercial alignment: Zones are often designed for internationally mobile capital and internationally familiar structures.

Where investors get caught out

Zones are not a shortcut around diligence.

The most common mistake is assuming the zone's benefits apply to all asset types in all locations. They usually don't. A zone may permit stronger rights, but only for specific property classes, uses, or district boundaries. Tax treatment can also vary depending on whether income is generated inside the zone framework or outside it.

Buyers should read zone rules as a separate legal system with its own boundaries, not as a generic signal that the whole country is open.

A second mistake is overestimating liquidity. A free-zone asset may be attractive to the right buyer cohort, but narrower legal eligibility can also narrow resale demand. Investors need to ask who the next buyer is likely to be, what financing they can obtain, and whether the ownership format remains attractive at exit.

Your Due Diligence Checklist and Finding Legal Counsel

Foreign ownership restrictions by country are only the starting point. True protection comes from transaction-specific due diligence carried out before the contract locks you in.

That means independent legal review, tax review, and title verification. Not informal reassurance from a broker, developer, seller, or “recommended local contact”.

The checklist that matters

- Verify ownership rights: Confirm whether you're acquiring freehold, leasehold, shares in a holding vehicle, or only contractual use rights.

- Check the asset category: Make sure the land type or property use doesn't trigger special restrictions.

- Map the approvals: Identify every consent, filing, identity check, and disclosure requirement before exchange.

- Review tax and reporting: A legally possible deal can still produce weak returns if taxes and reporting burdens are heavy.

- Stress-test the exit: Ask how a future buyer, lender, and regulator will view the same structure.

- Confirm source-of-funds evidence: Banking friction can delay or derail completion even when title is clear.

How to choose legal counsel

Use a lawyer who represents you alone and has handled foreign-buyer transactions in that jurisdiction. If the only lawyer in the room was introduced by the seller, your interests may already be diluted.

Ask direct questions:

| Question | Why it matters |

|---|---|

| Have you advised foreign buyers on this asset type? | Restrictions often vary by land class and use |

| Who checks title and planning compliance? | Responsibility must be explicit |

| Have you handled overseas entity or beneficial ownership filings? | Compliance failures can block completion |

| What commonly goes wrong in exits? | Good counsel should think beyond acquisition |

Hire the lawyer before the negotiation becomes expensive. Once a deposit is committed, bad structure becomes harder to fix.

Frequently Asked Questions on Global Property Ownership

Does buying property give me residency or citizenship

Usually, no. Investors often assume property ownership automatically opens the door to residency rights. In many markets, property purchase and immigration status are separate legal tracks. Even where a country promotes investment migration, the qualifying route may depend on programme rules rather than ordinary property ownership.

Do restrictions apply only to residential property

No. In many jurisdictions, the most sensitive rules attach to commercially strategic property rather than ordinary housing. Farmland, logistics sites, energy-linked land, infrastructure-adjacent plots, and development land often attract more scrutiny than standard residential stock.

Can I borrow from a local bank as a foreign buyer

Sometimes, but restrictions often spill into financing. Banks care about title quality, borrower identity, source of funds, and enforceability of security. If your ownership structure is unusual, a lender may offer less debt, demand more documentation, or refuse the deal altogether.

Is leasehold always inferior to freehold

Not automatically. Leasehold can work well if the term is long, rights are clear, renewal risk is understood, and the local resale market accepts the structure. It becomes problematic when lenders avoid it, buyers discount it heavily, or key contractual protections are weak.

What happens on death or inheritance

That depends on local succession law, your ownership vehicle, and whether the asset is held personally or through a company. Cross-border inheritance can become complicated fast. Investors should review succession issues before purchase, not after.

Are company structures always safer than personal ownership

No. A company can improve flexibility, privacy, or compliance fit in some markets. In others, it creates extra filings, extra tax complexity, and more beneficial ownership exposure. The right answer depends on the jurisdiction and your intended hold period.

How do restrictions affect resale value

They can reduce the buyer pool, increase legal costs, and lengthen the transaction timetable. That doesn't always destroy value, but it can compress it. The more specialised the ownership route, the more important exit analysis becomes.

What's the biggest mistake foreign investors make

They confuse legal possibility with commercial practicality. The legal answer may be yes. The investment answer can still be no.

World Property Investor helps buyers compare overseas markets with practical, data-led research on ownership rules, taxes, yields, and buying process. If you're weighing where to deploy capital next, explore World Property Investor for country guides, market analysis, and step-by-step support on international property investment.