This is a practical guide to Hong Kong's formidable real estate market. For any global property investor, Hong Kong housing represents an asset class defined by high capital values and persistent demand. This guide provides the clarity required to navigate this unique landscape and make informed decisions.

Understanding The Hong Kong Housing Market

For decades, the term "Hong Kong property" has been synonymous with premium prices and intense competition. It is best understood not as simple residential housing but as a high-value financial instrument, driven by a powerful and distinct set of fundamentals. An analysis of the core market mechanics is essential before committing capital.

At its heart, the market operates on a foundation of structural scarcity. The government's tight control over land supply has historically constrained new development, creating a long-term imbalance that supports property values. This dynamic makes the entire market exceptionally sensitive to shifts in demand and capital flows.

Core Investment Themes

A successful strategy requires a firm grasp of the key themes that shape returns. These factors influence everything from asset selection to long-term profitability and are the first step towards building a sound investment case for the Hong Kong housing market.

Key areas for analysis include:

- Demand and Affordability: Despite high prices, local and international demand remains a constant feature. This chronic housing shortage fuels a resilient rental market, particularly for the smaller, more affordable units that are in perpetual short supply.

- Government Policy: The Hong Kong government is known for market interventions, such as stamp duties, to manage speculation. The removal of punitive taxes for foreign buyers in 2024 marked a significant policy shift, improving market access for international capital.

- Economic Drivers: As a global financial hub, Hong Kong's economy is linked to global interest rates—primarily through the HKD-USD peg—and capital flows from mainland China. These macroeconomic forces create both opportunity and risk.

Takeaway: The market can be viewed as a system under pressure: limited land supply, constant demand, and a government that periodically adjusts regulatory controls. An investor's role is to understand these pressures, not just the physical asset.

Understanding key market indicators such as the absorption rate in real estate is vital for assessing market health. For broader context, examining overarching international property trends provides a useful global comparison.

This guide will break down these elements, providing a data-led analysis of price trends, rental yields, district profiles, and the practicalities of acquisition. The objective is to equip investors with the knowledge to make informed, long-term decisions in one of the world's most challenging and potentially rewarding property markets.

What Drives Hong Kong Property Prices

To analyse Hong Kong’s property market, one must understand the unique forces that shape it. Unlike many Western markets where prices largely follow the broader economy, Hong Kong is driven by three core levers: land supply, interest rates, and a deep, multi-layered demand structure.

Mastering these fundamentals is a prerequisite for any serious investor.

At the very heart of the city’s high property prices is a structural scarcity of land. The government acts as the ultimate landlord, controlling the release of new plots for development through a tightly managed auction system. This policy deliberately restricts the supply of new housing.

The result is a perpetual imbalance where demand consistently outstrips the supply of available homes. This engineered scarcity creates the market’s infamous ‘scarcity premium’—a primary reason why values have remained stubbornly high over the long term.

This controlled supply means even minor shifts in the economy or buyer sentiment can have an outsized impact on prices. When demand increases, developers must bid aggressively for the few available plots, a cost that is invariably passed on to the end buyer.

The Influence of Interest Rates and Capital Flows

Hong Kong's monetary policy is another critical component. The Hong Kong dollar is pegged to the US dollar, meaning local interest rates almost perfectly mirror those set by the U.S. Federal Reserve. For many years, this was a significant tailwind, as historically low global rates made borrowing cheap, fuelling a debt-driven property boom.

This peg, however, is a double-edged sword. It makes the market highly sensitive to monetary policy in Washington D.C. When US rates rise, borrowing costs in Hong Kong increase, which cools demand and places downward pressure on property values. Indeed, data from Hong Kong's Rating and Valuation Department showed that private home prices fell by over 15% from their 2021 peak by the end of 2023, largely due to aggressive rate hikes in the United States.

Takeaway: For investors, the direction of the US economy and its interest rate policy is as important to the Hong Kong housing market as local economic performance. This external factor introduces a layer of risk and volatility not present in markets with independent monetary control.

The third pillar is the immense, dual-pronged demand from both local residents and capital flows from mainland China. Locally, a strong cultural preference for home ownership, combined with limited housing options, ensures demand remains consistently robust.

Simultaneously, Hong Kong has long served as a preferred safe haven for mainland Chinese investors seeking to diversify their assets, which intensifies competition for a finite number of properties. This combined pressure ensures a deep and resilient pool of buyers.

Market Responses To Extreme Prices

The intense pressure on affordability has given rise to unique market phenomena, most notably the trend of ‘nano-flats’. These are very small apartments, often under 200 sq. ft., designed to offer a lower entry price for first-time buyers and investors. While their development is debated, their existence is a direct and logical response to the city’s extreme land costs.

To place these factors in a global context, it is useful to compare them with other major cities.

- Hong Kong vs. London: London also has housing shortages, but its supply is not institutionally constrained in the same manner. Prices in London are more closely tied to UK economic performance and wage growth, as cited by ONS data. Hong Kong, by contrast, is far more influenced by its land policy and capital flows from mainland China.

- Hong Kong vs. Singapore: Singapore also features significant government involvement in its housing market, but with a different approach. The vast majority of Singaporeans live in public Housing & Development Board (HDB) flats, which creates a more stable and affordable environment for residents. This is a sharp contrast to Hong Kong’s predominantly private and exceptionally expensive market.

Ultimately, these drivers have created a market that has demonstrated remarkable resilience over decades. Despite periods of volatility, the underlying fundamentals of tight supply and deep-seated demand have historically provided a powerful floor under prices, supporting long-term capital growth.

Where To Invest: A Guide To Property Types And Districts

Moving from abstract market forces to tangible assets, an investor’s success in the Hong Kong housing market hinges on selecting the right property in the right location. For international buyers, the private market is the sole playing field. Understanding its distinct property types and district profiles is therefore essential before committing capital.

Hong Kong's property landscape is incredibly diverse, shaped by decades of extreme population density and high land values. The options range from small, high-yielding units to large luxury homes, with each serving a different tenant demographic and investment strategy.

Navigating Hong Kong Property Types

An investor's portfolio can be constructed from several key property archetypes. The most common options in the private market include:

- Nano-flats: These micro-apartments, typically under 200 sq. ft., are a market response to affordability pressures. Found in dense urban areas of Kowloon, they offer a lower entry price and can generate high rental yields, appealing to single professionals and students. Their potential for capital growth, however, may be more limited compared to larger units.

- Standard Apartments: The backbone of the market, these 1- to 3-bedroom flats are found in large private housing estates. They are the most common form of Hong Kong housing, sought after by local families and professional tenants. Their liquidity is high, making them a relatively safe, 'blue-chip' choice for long-term investment.

- Luxury Apartments: Concentrated in prime districts like Mid-Levels and West Kowloon, these properties offer expansive living spaces, premium facilities, and skyline views. They attract high-net-worth expatriates and senior executives, commanding high rents but requiring significant capital outlay.

- Detached Houses: The rarest and most exclusive property type, found in prestigious enclaves such as The Peak and the south side of Hong Kong Island. These are trophy assets, offering privacy and status. Their market is thin, and they are primarily vehicles for wealth preservation rather than rental income.

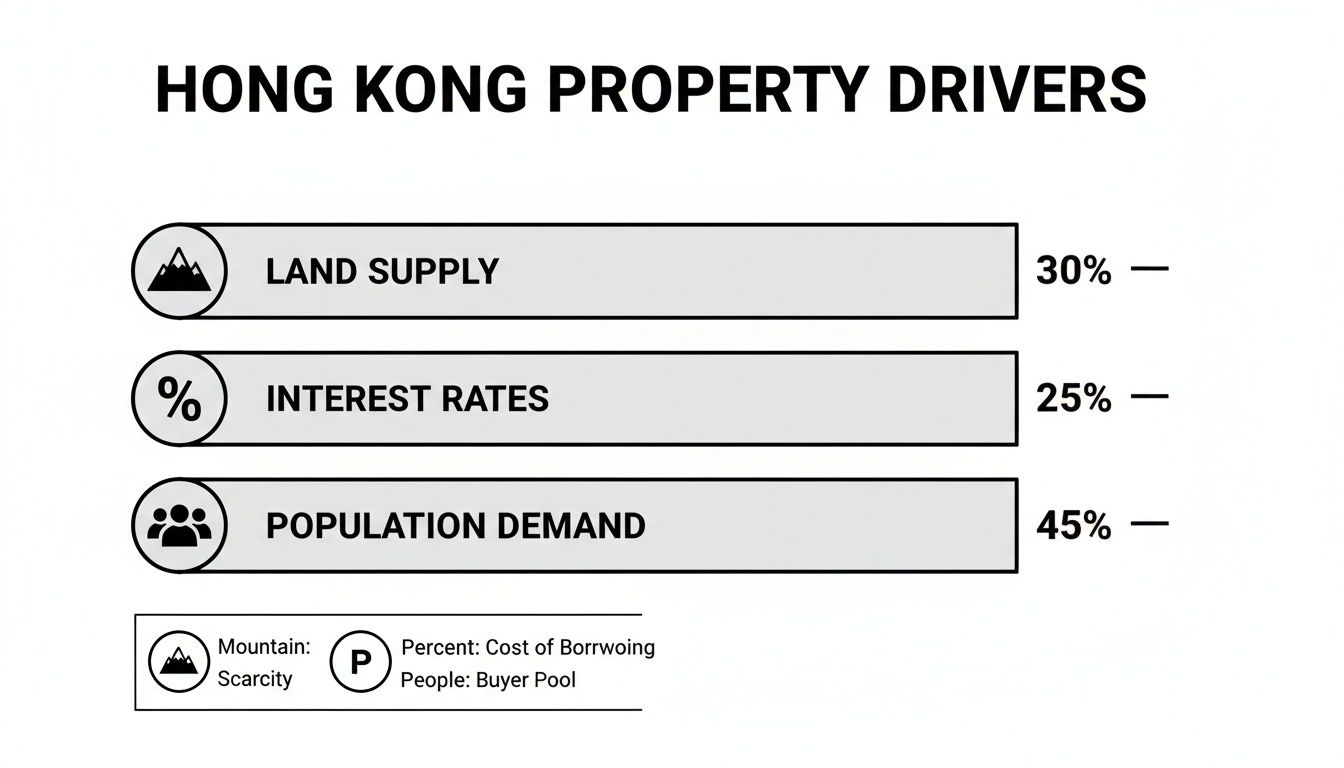

The following infographic breaks down the core drivers influencing property values across these types.

As the chart indicates, it is the unique combination of land constraints, interest rate sensitivity, and intense demand that shapes the market’s investment environment.

Hong Kong's Key Investment Zones

In Hong Kong, location is paramount. The territory can be broadly divided into three major zones, each with a distinct investment profile and risk-reward balance.

Takeaway: Think of these zones as different risk-and-return tiers. Hong Kong Island is the established blue-chip stock, Kowloon is the dynamic growth stock, and the New Territories represents the emerging market opportunity with higher potential upside.

Hong Kong Island: The Premium Core

This is the traditional heart of Hong Kong, home to the central business district, luxury retail, and the city’s most affluent residents. Districts such as Central, Mid-Levels, and Repulse Bay are considered prime real estate by any global standard.

Properties here are the most expensive but are also seen as the most resilient during market downturns. They offer prestige and stability, attracting top-tier corporate tenants. An investment here is a long-term play on capital preservation and steady, albeit modest, rental returns.

Kowloon: A Vibrant And Evolving Hub

Across the harbour, Kowloon is a densely populated, energetic district that blends old and new. Areas like Tsim Sha Tsui are major commercial and tourist hubs, while redeveloped zones like West Kowloon offer modern, high-end residential towers with excellent transport links.

Kowloon offers a wider range of property prices than the Island and is a popular choice for both local and expatriate renters. Investment here provides a balance of potential capital growth and solid rental demand, particularly in buildings near MTR stations. Understanding property ownership is vital; our guide on freehold and leasehold property is a valuable resource, as all land in Hong Kong is government leasehold.

The New Territories: The Growth Frontier

Stretching from Kowloon to the mainland border, the New Territories is the largest and most populous region. Historically more suburban, it is now a key growth area, with new towns like Sha Tin and Tseung Kwan O developing into self-contained urban centres.

This region offers the most accessible entry point into the Hong Kong housing market. It is particularly popular with local families due to its larger living spaces and community-oriented environment. Major infrastructure projects and proximity to the Greater Bay Area are fuelling long-term growth prospects, making it an attractive zone for investors seeking capital appreciation.

To help compare these zones, we have broken down their investment profiles in the table below.

Hong Kong District Investment Profile Comparison

| District | Primary Market | Average Price / Sq. Ft. (Private) | Typical Rental Yield | Key Investor Appeal |

|---|---|---|---|---|

| Mid-Levels (HK Island) | Luxury & Expat | HK$23,000 – $30,000+ | 1.8% – 2.5% | Capital preservation, prestige, and stable corporate tenants. |

| West Kowloon | High-End & Professional | HK$20,000 – $28,000 | 2.2% – 3.0% | Modern infrastructure, growth potential, strong transport links. |

| Sha Tin (New Territories) | Local & Family | HK$14,000 – $18,000 | 2.5% – 3.5% | Affordability, strong local demand, future growth prospects. |

This comparison highlights the clear trade-offs between stability, yield, and growth. A premium location like Mid-Levels offers robust security, while an area like Sha Tin presents a more accessible entry point with the potential for higher yields and long-term capital growth driven by ongoing development. Your choice will depend on your personal investment strategy and risk appetite.

Calculating Your Return: Rental Yields Versus Capital Growth

For any property investment, the primary question concerns return. For the Hong Kong housing market, it is crucial to understand that this is a market that historically rewards patient capital through long-term appreciation, not high monthly rental income.

For investors accustomed to emerging markets offering rental yields of 8-10%, Hong Kong will be a different proposition. Gross rental yields for residential property here typically hover in a modest range of 1.5% to 2.5%. To an investor familiar with markets in the UK or parts of Southeast Asia, this figure can appear low.

The reason for this compressed yield is simple arithmetic. Over the past two decades, property values in Hong Kong have risen at a much faster pace than rents. This has created a significant gap, meaning that even with high absolute rental prices, the annual income represents a small fraction of a property's capital value.

Understanding Capital Growth Potential

While rental yields are modest, the story for capital growth is entirely different. Historically, Hong Kong has delivered phenomenal long-term appreciation. Although the market experiences periods of sharp volatility, its core drivers—a structural shortage of land and deep-seated demand—have consistently pushed asset prices higher over time.

An investor who purchased a flat in Central in the early 2000s would have seen its value multiply many times over, far eclipsing the modest annual rent collected. This is the fundamental investment thesis for Hong Kong: accept a low annual cash flow in exchange for the potential of significant capital gains over a 10-to-20-year horizon. It is a strategy built for wealth creation through asset appreciation, not immediate income.

How To Calculate Your Net Rental Yield

To obtain a realistic picture of actual returns, one must look beyond the gross figure and calculate the net rental yield. This is the metric that accounts for the various costs of owning and letting a property in Hong Kong.

Takeaway: Your net yield is the true measure of an investment's annual performance. It reflects the income remaining after all necessary expenses have been paid, providing a clear view of the property's cash flow reality.

The calculation is straightforward:

Net Rental Yield = [(Annual Rental Income – Annual Operating Costs) / Total Property Cost] x 100

Essential costs to factor in include:

- Management Fees: A professional property manager typically charges around 5% of the monthly rent.

- Government Rates: This is a property tax paid quarterly, calculated at 5% of the property's estimated annual rental value.

- Property Tax: Levied on the owner at a standard rate of 15% on the net assessable value (which is the annual rent minus rates and a 20% statutory allowance for repairs).

- Vacancy Periods: It is prudent to budget for at least one month of vacancy per year, which equates to an 8.3% reduction in potential annual income.

- Repairs and Maintenance: A sensible budget for unforeseen repairs is essential for maintaining the asset and its appeal to tenants.

Once these outgoings are tallied, a 2.5% gross yield can quickly compress to a net yield closer to 1.5% or less. Understanding how to calculate cap rate is a vital skill for any serious property investor.

This low-yield, high-growth model is not suitable for everyone. It demands a long-term view and a financial position that does not rely on immediate rental cash flow. For a detailed breakdown, our guide on how to calculate return on investment property provides further analysis. Ultimately, an investor must decide if this financial profile aligns with their own goals and risk appetite.

How To Buy Property In Hong Kong As A Foreigner

Acquiring property in Hong Kong as a foreigner is a well-established process with clear rules. This section breaks down the legal and financial journey into a straightforward plan for non-resident investors.

For years, significant tax hurdles made it costly for overseas buyers. This changed in early 2024. In a major policy shift, the government scrapped all extra stamp duties that applied to non-permanent residents and foreign purchasers. This move places international buyers on the same financial footing as locals, signalling a clear welcome to external capital.

Understanding The Costs of Entry

Even with the recent tax changes, stamp duty remains a key part of the budget. The primary tax is the Ad Valorem Stamp Duty (AVD), which operates on a sliding scale based on the property’s price. For example, a property valued at HK$10 million would attract an AVD of 3.75%.

It is also crucial to be aware of the Special Stamp Duty (SSD). This tax is designed to discourage short-term speculation. If you sell a property within 24 months of purchase, the SSD applies. The rate is 20% for a sale within six months, 15% for a sale between six and 12 months, and 10% if sold between 12 and 24 months. The policy reinforces the view that Hong Kong property is best treated as a long-term investment.

Takeaway: The 2024 decision to scrap extra stamp duties for foreigners is the single most important policy change for international investors in a decade. It removes a significant financial barrier, allowing a focus on the fundamental quality of the asset.

Beyond taxes, standard transaction costs include:

- Legal Fees: Expect to pay between 0.075% to 0.125% of the purchase price for your solicitor’s work on due diligence and conveyancing.

- Estate Agent’s Commission: This is typically 1% of the purchase price, paid to the agent representing you.

Securing Financing As A Non-Resident

Securing a mortgage in Hong Kong as a non-resident is possible, but banks are noticeably more cautious. While local residents can often borrow up to 70% of a property’s value (Loan-to-Value or LTV), foreign buyers should plan for a lower LTV, typically around 50-60%. This necessitates a larger down payment of at least 40%.

Furthermore, all banks apply a strict mortgage stress test. They will verify if you could still afford the monthly repayments if interest rates were to rise by 2%. To pass, you must provide robust proof of income, such as tax returns and employment contracts. This system is designed to ensure borrowers are not over-leveraged. For those new to international purchases, a broader guide on how to buy property abroad can shed more light on common financial hurdles.

The Step-by-Step Purchase Process

Once financing is arranged, the purchase follows a clear, legally defined path. The Hong Kong system is known for being efficient and transparent, offering solid protection for both buyer and seller.

- Engage an Agent and Make an Offer: A good estate agent is key to sourcing properties and negotiating the price. Once a figure is agreed, you will sign a preliminary contract.

- Sign the Provisional Agreement: This is a preliminary but legally binding agreement. Upon signing, you pay an initial deposit, usually 3-5% of the purchase price.

- Appoint a Solicitor and Conduct Due Diligence: Your solicitor begins work, conducting essential checks on the property’s title to ensure it is clean and free from legal encumbrances.

- Sign the Formal Agreement: Within 14 days, you sign the formal sale and purchase agreement. At this stage, a further deposit is paid to bring the total to 10% of the purchase price.

- Completion: On the agreed completion date, typically 30 to 60 days later, the remaining 90% of the price is transferred. The keys and the property’s legal title are then officially handed over.

Risks And Strategic Outlook

A prudent investment in the Hong Kong housing market requires understanding the risks as clearly as the potential rewards. While the city’s property has an established reputation for long-term growth, it is not immune to significant headwinds. A forward-looking strategy must balance these challenges against the core strengths that underpin the market.

The primary risks are a mix of geopolitics, economics, and demographics. Beijing’s growing influence is now a permanent feature of the landscape, introducing a layer of political uncertainty that can sway market sentiment.

At the same time, the local economy is tied to global finance, mainly through the HKD-USD currency peg. This makes Hong Kong highly sensitive to interest rate decisions made by the US Federal Reserve. This was demonstrated in 2022-2023, when rising US rates directly increased borrowing costs in Hong Kong, cooling demand and putting downward pressure on prices.

Market Fundamentals And Potential Upside

Despite these risks, Hong Kong is built on incredibly resilient fundamentals. Its position as a top-tier global financial hub remains secure, continuing to attract international talent and capital.

The city also plays a key role in China's Greater Bay Area initiative, a long-term economic project designed to integrate Hong Kong with major mainland cities. This strategic role is expected to drive economic integration and support property demand for years to come.

The most powerful fundamental, however, remains the severe, structural undersupply of housing. Data from Hong Kong's Housing Bureau shows the average waiting time for public rental housing is still years long, forcing a large portion of the population into the private market. This chronic shortage creates a solid foundation for rental demand, especially for smaller, more affordable flats.

Takeaway: The core investment thesis remains unchanged: you are buying into a market defined by extreme scarcity. While economic cycles and political shifts will cause short-term volatility, the fundamental imbalance between supply and demand provides powerful long-term support for property values.

Actionable Investment Recommendations

Weighing the risks and opportunities, a clear, fundamentals-first strategy emerges. This is not a market for short-term speculation; success demands patience and a long-term perspective.

- Focus on High-Demand, Smaller Units: The most stable segment of the rental market is, and will likely remain, smaller apartments (one or two bedrooms) in urban areas with excellent transport links. These properties are aimed at the deep, consistent demand from young professionals and small families. They offer the best combination of rental stability and liquidity.

- Explore Emerging Districts: While prime districts on Hong Kong Island are safe bets, the best growth potential often lies in up-and-coming areas undergoing infrastructure upgrades. Consider locations in the New Territories, especially those along new MTR lines or near the mainland border. These areas are well-positioned to benefit from population growth and integration with the Greater Bay Area.

- Adopt a Long-Term Horizon: The Hong Kong housing market is cyclical and famously volatile. Attempting to time the market is a high-risk strategy. A successful approach requires a minimum investment horizon of 10+ years. This provides the capacity to ride out inevitable downturns and capture the long-term capital growth that has historically defined this market.

Ultimately, investing in Hong Kong property is a strategic play on capital growth more than immediate rental income. By focusing on high-demand properties in growth areas and committing to a long-term hold, investors can position themselves to navigate the risks and reap the potential rewards of one of the world's most dynamic real estate markets.

Frequently Asked Questions About Hong Kong Property

When analysing a market as unique as Hong Kong, questions are natural. The regulations, financing norms, and even property ownership structures can differ from what many investors are accustomed to. Here are clear answers to common queries from international investors.

Are There Restrictions On Foreigners Buying Property?

No, there are no restrictions—foreigners are completely free to buy property in Hong Kong.

In a significant policy change in early 2024, the government abolished the substantial stamp duties that previously applied to non-permanent residents and overseas buyers. This has levelled the playing field, placing international investors on the same footing as local buyers and making direct ownership far more accessible.

What Is The Typical Deposit For A Foreigner's Mortgage?

While securing a mortgage as a non-resident is standard practice, you will require a larger down payment. Hong Kong banks are generally more conservative when lending to foreign buyers.

You should be prepared to put down a deposit of at least 40% to 50% of the property’s value. The Loan-to-Value (LTV) ratios are stricter for non-residents compared to the 70% LTV (or higher) that local buyers can often access.

How Important Is The HKD-USD Peg For Property Investors?

It is critically important. The Hong Kong dollar is pegged to the US dollar, which means Hong Kong's interest rates must follow the policy moves of the US Federal Reserve.

When US rates rise, borrowing costs in Hong Kong inevitably climb. This can cool the property market by making mortgages more expensive, which directly impacts affordability and, in turn, asset prices.

How Is Property Owned In Hong Kong?

This is a fundamental difference from markets like the UK or US. Unlike freehold ownership, all land in Hong Kong is ultimately owned by the government and sold on a leasehold basis.

When you purchase a property, you are acquiring the right to use it for the remainder of the government's land lease term. These leases are typically long (often 50 years or more) and can be renewed, but it is a core feature of the market that every investor must understand from the outset.

At World Property Investor, we provide the in-depth analysis and data you need to make confident investment decisions across the globe. Explore our guides and start building your international portfolio today at https://www.worldpropertyinvestor.com.