Expanding an investment portfolio into overseas property is a strategic decision to achieve diversification, pursue higher rental yields, and secure a lifestyle asset. This is not simply about acquiring a holiday home; it is a financial strategy aimed at building wealth in global markets. Success, however, hinges on a disciplined approach to managing unique risks, from currency fluctuations to unfamiliar foreign legal frameworks.

Why Invest in Property Beyond Your Borders?

Investing in property abroad is a calculated decision to strengthen one's financial position. By moving beyond the domestic market, investors can unlock opportunities that may not be available at home. The primary appeal is diversification. Spreading assets across different economies reduces exposure to a single market downturn. Should the UK property market, for example, experience a period of stagnation, a well-chosen asset in a growing European city or a popular US tourist destination can provide a critical buffer.

This strategy allows investors to tap into markets with different economic cycles, potentially capturing growth when the domestic market is flat. It also provides access to higher rental yields. For instance, while gross yields in major UK cities often sit between 3% and 4% according to ONS data, certain overseas locations can deliver significantly better returns due to lower property prices and strong rental demand.

Comparing Market Opportunities

The global property landscape offers a clear choice between established and emerging markets, each with a distinct risk-reward profile.

-

Established Markets: Locations such as Portugal, Spain, or major cities in the USA are considered stable. They offer transparent legal systems, proven tourist appeal, and high liquidity, which facilitates easier exit strategies. The trade-off is that their potential for rapid capital appreciation may be more moderate.

-

Emerging Markets: In contrast, destinations like parts of the UAE or Southeast Asia can offer the potential for significant capital growth and attractive rental yields. The compromise here is often higher political or economic risk, less legal transparency, and potential currency volatility.

An informed decision requires analysis that goes beyond marketing materials to examine the fundamental drivers of each market.

A successful international property portfolio is not built on speculation. It is built on rigorous analysis and a clear understanding of market fundamentals. The objective is to identify sustainable demand, whether from tourism, local renters, or broader economic growth.

Foundational Considerations for Global Investors

Before committing capital, every global investor must grasp several key factors. Currency risk is paramount; a 10% adverse movement in an exchange rate can dramatically alter the purchase cost or erode rental income when converted back to sterling.

Furthermore, legal and tax systems vary immensely between countries. Understanding property ownership structures—such as freehold versus leasehold—and tax obligations both in the foreign jurisdiction and in the UK is non-negotiable. This due diligence forms the bedrock of any successful venture into overseas property investment.

How to Evaluate International Property Markets

Selecting the right location is the single most critical decision when investing overseas. A successful investment is not based on glossy brochures or persuasive sales pitches; it is founded on a solid understanding of market fundamentals. This requires looking beyond superficial appeal to analyse the economic and political landscape that will support the property’s value over the long term.

A data-driven approach is essential. A country’s overall economic health provides the foundation for a stable property market, and key indicators offer a clear snapshot of its trajectory and potential risks.

A thorough analysis should include:

- Gross Domestic Product (GDP) Growth: Consistent GDP growth indicates a healthy, expanding economy. This typically translates into rising wages, increased housing demand, and genuine potential for capital appreciation.

- Political Stability: Stable governments and predictable legal frameworks are non-negotiable. Data from sources like the World Bank can offer objective insight into political risk, which directly impacts property rights and investor security.

- Local Employment Rates: Low unemployment and the presence of major employers signal a robust local economy. This is what sustains long-term rental demand and property values.

Calculating a Market's True Potential

Once the macroeconomic picture is clear, the focus should shift to property-specific metrics. These figures allow for objective comparison between locations and provide a realistic expectation of returns.

The most common starting point is the gross rental yield. This is calculated by dividing the total annual rent by the property’s purchase price, then multiplying by 100. For example, a £200,000 property generating £12,000 in annual rent has a gross yield of 6%.

This figure, however, can be misleading as it ignores expenses. The net rental yield provides a much more accurate picture of profitability by factoring in costs such as management fees, maintenance, insurance, and local property taxes.

The primary goal is to understand a market’s cash flow potential. A high gross yield may look attractive, but if local taxes and management fees are excessive, the net return could be disappointing. Always calculate both.

Another vital metric is the price-to-rent ratio, calculated by dividing the median house price by the median annual rent. A lower ratio suggests it is more favourable to buy than rent, indicating strong underlying demand for rental properties and a potentially healthier investment market.

Established vs Emerging Markets: A Comparison

The global property market presents a spectrum of opportunities, from the stability of established markets to the high-growth potential of emerging ones. Each carries a different risk and reward profile.

To illustrate this, let's compare a typical established market like Portugal's Algarve with a popular emerging market such as Dubai in the UAE.

Market Snapshot: Established vs Emerging

| Metric | Established Market (e.g., Portugal) | Emerging Market (e.g., UAE) |

|---|---|---|

| Capital Growth | Slower, more predictable growth. | High potential for rapid appreciation. |

| Rental Yields | Often moderate (e.g., 3-5%). | Can be higher (e.g., 5-8%+). |

| Liquidity | High; easier to sell the property. | Can be lower; may take longer to exit. |

| Risk Profile | Lower political and economic risk. | Higher volatility and potential risk. |

| Legal Framework | Transparent and well-established. | Can be less developed or subject to change. |

Investing in a location like the Algarve offers a mature market with a proven tourism track record, providing reliable rental income and a stable legal system. The potential for dramatic capital growth may be limited, but the associated risk is much lower.

In contrast, a market like Dubai offers tax-free rental income and significant potential for capital appreciation, driven by strong economic growth. However, it is also more susceptible to global economic shifts and has a history of market volatility. For investors seeking dynamic opportunities, our analysis of the top 7 emerging property investment markets provides further insights.

Ultimately, the choice depends on an individual's risk appetite and long-term financial objectives.

Navigating Foreign Legal and Tax Rules

Acquiring property overseas involves more than finding a prime location and calculating potential returns. It means entering a different legal and tax system, and understanding the local rules is not just advisable—it is essential. A mistake in this area can lead to unexpected costs, legal complications, or, in the worst-case scenario, jeopardise ownership of the asset.

The first step is to understand the form of property ownership. In many countries with legal systems derived from English law, terms like freehold (outright ownership of the building and land) and leasehold (ownership for a fixed period) will be familiar. However, many other jurisdictions have different structures, such as strata titles or community ownership schemes. Each comes with its own rights and responsibilities. An independent local solicitor is an invaluable asset in navigating these systems and avoiding common pitfalls like defective property titles or restrictive local planning laws.

Understanding Your Tax Obligations

Tax obligations are an ongoing aspect of being an overseas landlord. If not planned for, they can significantly erode returns. Generally, investors will face four types of tax.

- Purchase Taxes: Similar to UK Stamp Duty Land Tax, most countries charge a one-off tax on property acquisition. This can be a substantial upfront cost, sometimes reaching 10% or more of the purchase price.

- Annual Property Taxes: These are equivalent to council tax and are paid yearly to local authorities. Calculation methods vary widely between countries and even municipalities.

- Rental Income Tax: It is almost certain that tax will be payable on rental income in the country where the property is located. As a UK resident, this income must also be declared to HMRC.

- Capital Gains Tax (CGT): Upon selling the property, CGT will likely be due on any profit made. This may be payable in both the foreign country and the UK.

The key is to understand the interplay between these taxes. The Double-Taxation Treaty between the UK and the investment country is a critical instrument designed to prevent the same income from being taxed twice.

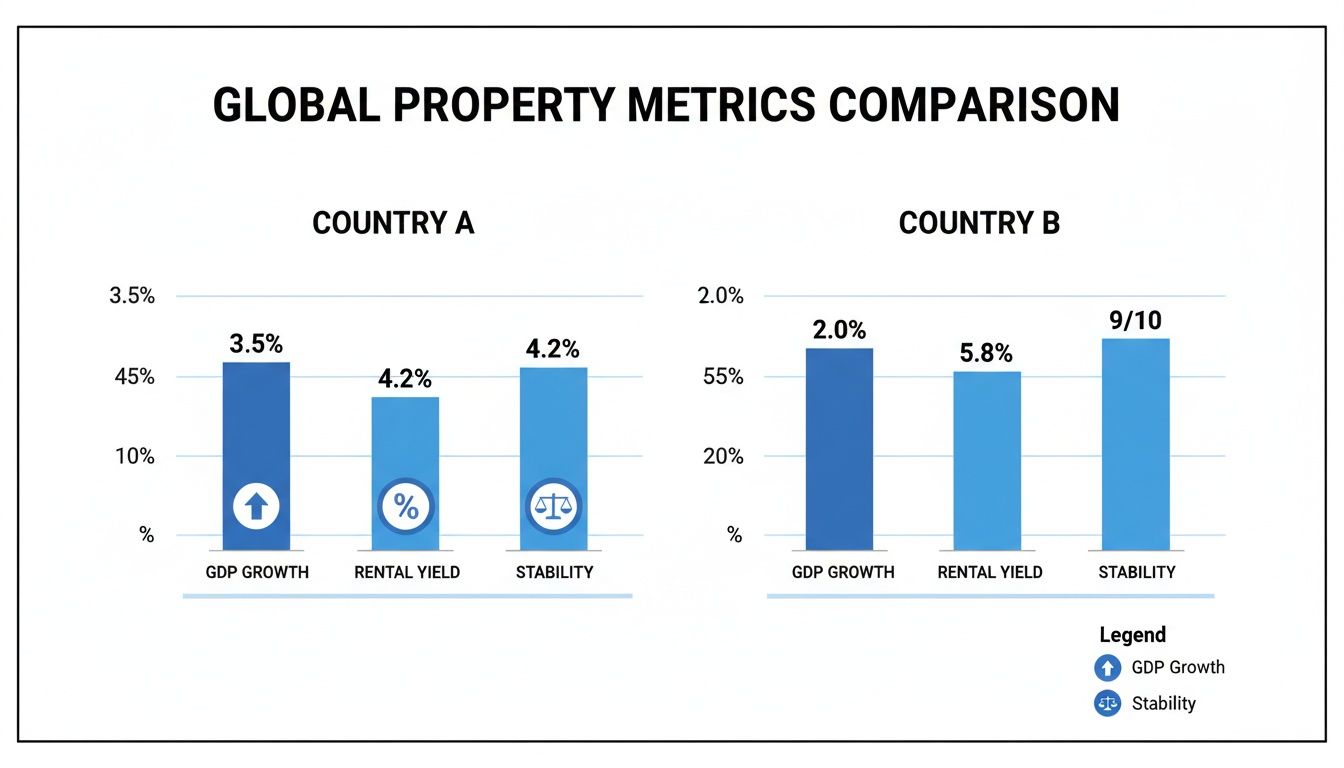

The chart below illustrates how different economic and stability metrics combine when evaluating a potential market.

It serves as a reminder that a comprehensive assessment—from GDP growth to rental yields and political stability—is required to form a true picture of a country’s investment climate.

Staying Compliant and Tax-Efficient

The complexity of international tax law makes professional advice a necessity, not a luxury. A stable and transparent legal framework is one reason the UK remains a popular destination for international investors, as it provides a sense of security for global capital.

To ensure compliance and tax efficiency, it is vital to ask the right questions from the outset. Before making an offer, legal and tax advisors should clarify the following:

- What are the total estimated acquisition costs, including all taxes and fees?

- How is the annual property tax calculated, and are there any applicable exemptions?

- What is the local tax rate on rental income, and which expenses are deductible?

- How does the relevant Double-Taxation Treaty apply to rental income and future capital gains?

Addressing these points from the start is fundamental. For a more detailed examination of this topic, refer to our guide on how to understand property taxes when investing abroad.

Financing Your Overseas Property Purchase

Once a promising overseas property has been identified, the next critical step is financing the purchase. Arranging finance for an international acquisition is significantly different from a domestic transaction, involving different regulations, lenders, and risks. However, with careful planning, it is a process that many investors navigate successfully.

The first major decision is the funding route.

Most investors choose one of two paths: seeking a mortgage from a local lender in the country of purchase or releasing equity from a UK property to become a cash buyer abroad. Each approach has distinct advantages and disadvantages.

Securing a Mortgage Abroad

Arranging a mortgage with a bank in the target country may seem the most direct method, but it presents several challenges. From a foreign lender’s perspective, a non-resident applicant represents a higher risk, which is reflected in their lending terms.

Investors pursuing this route should be prepared for:

- Larger Deposits: Non-resident buyers are typically required to provide a deposit of 30-50% of the property’s value, substantially higher than the 5-10% common in the UK market.

- Stricter Affordability Checks: Lenders will conduct rigorous due diligence, scrutinising global income and outgoings and demanding extensive, often translated, documentation such as proof of income, tax returns, and bank statements.

- Higher Interest Rates: To compensate for the perceived additional risk, the interest rate offered will likely be higher than that available to a local resident.

Engaging an independent mortgage broker in the target country who specialises in non-resident applications is highly recommended. Their existing relationships and knowledge of documentation requirements can save considerable time and effort.

Using Your UK Property to Fund the Purchase

An alternative strategy is to remortgage a UK property to release equity—the difference between the property's value and the outstanding mortgage—to fund the overseas purchase outright. This approach has the significant advantage of positioning the investor as a cash buyer abroad, which can strengthen their negotiating position and accelerate the transaction process by removing the need for foreign lender approval.

The primary risk is the increased debt secured against the UK property. It is imperative to ensure that the rental income from the overseas asset will comfortably cover the increased UK mortgage payments.

Key Takeaway: Becoming a 'cash buyer' overseas provides greater negotiating power and simplifies the purchase. However, this strategy increases leverage on UK assets, a risk that must be carefully managed.

This approach can be particularly effective when the UK property market is stable. Current forecasts from bodies such as Savills and Knight Frank point to modest growth, with an easing of mortgage rates bringing buyers back to the market. Data from Rightmove has also shown a surge in US interest, with enquiries at their highest since 2017. You can read more about this in the UK property price forecast for 2025 at 10acre.co.uk.

Managing Currency Risk

Regardless of the financing method, currency risk is an unavoidable factor. The agreed purchase price is effectively a moving target from the moment an offer is accepted until the funds are transferred. An adverse 5% shift in the GBP/EUR exchange rate on a €300,000 property could increase the sterling cost by approximately £12,000.

This volatility affects not only the purchase price but also long-term mortgage payments and rental income. Prudent strategies to manage this risk include:

- Using a Specialist Currency Broker: These firms typically offer more competitive exchange rates and lower fees than high street banks.

- Securing a Forward Contract: This financial instrument allows you to lock in an exchange rate today for a future transaction. This removes uncertainty from the final purchase cost.

A robust financing plan is the foundation of any successful overseas property investment. For a more detailed look at the strategies involved, please see our complete guide on financing an investment property.

Choosing Your Investment Strategy

With financing arranged and a target market identified, the next step is to define how the investment will generate returns. A successful venture into investing in overseas property depends on a clear, well-executed strategy. The optimal approach is determined by financial goals, risk appetite, and the time an investor can realistically commit to managing an asset from a distance.

For most international investors, the choice is between two primary models: securing long-term tenants for a steady income stream, or entering the more demanding but potentially lucrative short-term holiday let market. Each path has a distinct income potential, cost structure, and management workload.

Long-Term Rentals For Stable Returns

The traditional buy-to-let model is often viewed as the more conservative, hands-off approach. It involves finding a tenant on a long-term contract, typically for six months or more, creating a predictable source of monthly income. This stability is the model’s greatest strength, making it easier to forecast cash flow and cover ongoing costs like mortgage payments and service charges.

Success, however, depends on securing reliable, properly vetted tenants. It also requires an understanding of local tenancy laws, which can be complex and, in some jurisdictions, highly tenant-friendly. Furthermore, rental income is determined by the local market rate, which may cap potential returns compared to the more dynamic holiday let market.

Short-Term Holiday Lets For Higher Yields

In tourist destinations, short-term holiday lets offer the potential for significantly higher rental yields. By letting a property on a nightly or weekly basis through platforms like Airbnb or Booking.com, investors can command premium rates during peak season, often generating more income in a few months than a long-term rental would over a full year.

This higher reward comes with greater risk and a much larger management burden. Occupancy is not guaranteed; it fluctuates with seasons, local events, and wider travel trends, which can lead to costly void periods. Managing a holiday let is akin to running a small hospitality business, involving constant marketing, guest communication, cleaning, and maintenance. Additionally, many regions are introducing stricter regulations and higher taxes on short-term rentals, which can impact profitability.

The core difference lies in the balance between income stability and income potential. A long-term let provides a reliable baseline, whereas a holiday let offers the chance for superior returns at the cost of consistency and hands-on management.

Comparing The Two Strategies

A side-by-side comparison of the key financial and operational differences is essential for making an informed decision.

| Factor | Long-Term Rental | Short-Term Holiday Let |

|---|---|---|

| Income Potential | Stable and predictable, but capped by local market rates. | High potential for superior yields, especially in peak season. |

| Occupancy Rate | High and consistent, often 95-100% during a tenancy. | Variable and seasonal, a good year might average 60-80%. |

| Running Costs | Lower (e.g., agent fees of 8-12% of rent). | Higher (e.g., platform fees, cleaning, utilities, marketing). |

| Management | Largely passive; a local agent can handle most tasks. | Active and demanding; requires constant guest management. |

| Wear and Tear | Generally lower with one long-term, vetted tenant. | Higher due to frequent guest turnover. |

The characteristics of a particular market often dictate the more logical strategy. For example, despite recent fiscal headwinds, UK property investment volumes remain resilient, with income returns driving performance. Forecasts show promising annual returns, particularly in the industrial and retail sectors, with continued cross-border capital inflows from the US, Canada, and Australia. This underlying stability can support both rental models. You can discover more insights in Aberdeen Investments' UK real estate market outlook.

Ultimately, the best strategy aligns with your circumstances. For a passive investment with minimal involvement, a long-term rental managed by a reputable local agent is likely the better fit. For those with the time and entrepreneurial drive to actively manage a property for maximum returns, a holiday let in a prime tourist location could be highly rewarding. For a deeper dive into foundational concepts, check out our beginner's guide to real estate investing.

Your Essential Due Diligence Checklist

Thorough due diligence is the most effective defence against costly errors when investing in overseas property. This checklist serves as a final inspection before capital commitment, consolidating the key principles of this guide into a practical, step-by-step process.

This final phase is not about questioning the market choice, but about verifying every detail of the specific property. Rushing this stage is a false economy that can lead to significant financial and legal complications.

Legal and Physical Verification

Before any funds are transferred, an independent lawyer must conduct a thorough legal review. This is non-negotiable. Their role is to confirm the property is exactly as the seller represents it.

Key legal checks include:

- Verifying the Property Title: Confirming the seller possesses the legal right to sell and that the title deed is free from disputes.

- Checking for Encumbrances: Searching local land registries for any outstanding debts, mortgages, or legal claims (liens) attached to the property, which could become the buyer's responsibility.

- Reviewing Planning Permissions: Ensuring the property complies with all local zoning and planning regulations, which is critical for rental or alteration plans.

In parallel with legal checks, the property's physical condition must be scrutinised. Never rely solely on a report from the seller or their agent. Commissioning an independent building survey is crucial for uncovering hidden structural issues—from faulty wiring to damp—that could require expensive repairs.

Financial and Contractual Finalisation

Once legal and physical checks are complete, the focus shifts to securing the financial arrangements and finalising contracts. This step ensures funding is secure and all agreements are watertight before signing.

Your final due diligence is the critical bridge between finding a promising investment and securely owning a profitable asset. It's the disciplined process that turns a good opportunity into a great investment.

The final financial checklist should cover:

- Securing a Formal Mortgage Offer: If using finance, this means obtaining the binding, written offer from the lender.

- Arranging Property Insurance: Ensuring adequate building and contents insurance is in place from the day of completion.

- Opening a Local Bank Account: This is often essential for paying local taxes, utility bills, and receiving rental income efficiently.

- Final Contract Review: Your independent solicitor must review every clause of the final purchase contract, explaining all obligations and ensuring your interests are protected before you sign.

Methodically working through these steps ensures a comprehensive understanding of the asset being acquired. To further refine your evaluation process, read our guide on how to determine a property's investment potential with greater accuracy.

Your Questions Answered

Venturing into international property investment naturally raises practical questions. Below are answers to some of the most common queries from investors beginning their journey.

How Much Deposit Will I Need for a Property Abroad?

Deposit requirements for non-residents are almost always higher than in the UK. Foreign lenders perceive non-resident buyers as a greater risk and therefore require a larger upfront commitment.

As a general rule, investors should budget for a deposit of between 30% and 50% of the property's value. This is a significant capital outlay that must be considered early in the research process. The most effective first step is to consult a local mortgage broker who specialises in financing for foreign buyers to obtain accurate figures for your target country.

Can I Use My UK Pension to Buy an Overseas Property?

While it is technically possible to use a Self-Invested Personal Pension (SIPP) to purchase certain types of property, for a residential home abroad, the answer is almost certainly no. This is an exceptionally complex area fraught with risk.

HMRC has extremely strict rules regarding pension investments. Acquiring a residential property that you, your family, or any connected person could potentially use is almost always prohibited and can trigger punitive tax charges of up to 55% of the funds used. Commercial property may be treated differently, but this is a specialist investment field.

Before considering this path, it is imperative to seek independent financial advice from a qualified professional specialising in pension investments. The financial consequences of an error are severe.

What Are the Biggest Hidden Costs of Buying Overseas?

The purchase price is only the starting point. A prudent investor will budget for an additional 10% to 15% on top of the property price to cover associated costs. Failing to account for these can invalidate return-on-investment calculations.

Your budget should include provisions for:

- Transactional Costs: These include legal fees, notary charges, property registration fees, and local purchase taxes (the equivalent of Stamp Duty).

- Professional and Financing Fees: This covers mortgage arrangement fees, currency exchange costs, and a professional building survey—which should never be skipped.

- Ongoing Ownership Costs: After acquisition, costs continue. These include annual property taxes, community fees (for shared facilities like pools), landlord insurance, and property management fees, which typically range from 10% to 20% of rental income.

It is also advisable to establish a separate contingency fund for unexpected repairs. A boiler failure or a roof leak can occur anywhere, and being prepared is a core part of responsible property ownership.

At World Property Investor, we provide the in-depth guides and data-driven analysis you need to navigate the global property market with confidence. Explore our resources to find your next investment opportunity. Learn more at World Property Investor.