At its core, overseas rental income is the profit generated from a property you own in one country while residing in another. This strategy is a powerful method for diversifying an investment portfolio, but it operates under a different set of rules than domestic buy-to-let. Investors must navigate different tax laws, currency fluctuations, and foreign legal systems.

Understanding Your Overseas Rental Income Potential

Investing in property abroad can be a compelling move for discerning investors seeking to expand beyond their home market. The primary driver is often diversification; holding assets in different economies is a classic hedge against localised downturns. In the UK alone, the number of buy-to-let mortgages has held steady at approximately 2 million, according to UK Finance, demonstrating the enduring appeal of property as an asset class.

This strategy opens the door to markets with higher growth potential or more attractive rental yields than might be found domestically. An emerging European city, for example, could offer superior returns compared to a mature, high-cost market like London. This geographic arbitrage is a key component of building a resilient, global property portfolio.

Key Drivers for International Investment

Investors are typically drawn to overseas property for several powerful reasons:

- Higher Rental Yields: Certain international markets deliver fundamentally better rental returns than domestic options, providing a significant boost to monthly cash flow.

- Capital Appreciation: Targeting areas with strong economic growth can lead to substantial increases in a property's value over the long term.

- Portfolio Diversification: Spreading investments across different countries and currencies reduces risk and exposure to any single economy's performance.

However, generating overseas rental income presents a unique set of challenges. It is imperative to understand cross-border tax obligations, manage currency risk when repatriating profits, and navigate foreign property laws. These are critical hurdles that demand meticulous planning.

Navigating the Complexities

The path to successful international property investment is paved with thorough due diligence. While the promise of higher returns is strong, it is balanced by complexities not encountered in a domestic market.

A sudden shift in exchange rates, for example, could significantly reduce net profit when rental income is converted back into your home currency. Likewise, every country has its own regulations for tenancy rights, maintenance obligations, and tax reporting.

To properly evaluate any opportunity, you must first know how to determine a property's investment potential with these international factors in mind. This guide will provide the foundational knowledge needed to address these challenges effectively.

Calculating Your True Return on Investment

The headline rental figure in an advertisement is rarely the amount that reaches your bank account. To gain a true sense of an investment's potential, one must look past top-line numbers and understand the metrics that truly matter. It begins with understanding the critical difference between gross and net yields.

Gross figures offer a quick first impression, but net figures tell the real story. Relying solely on gross yield is one of the most common errors new investors make, and it can lead to unwelcome financial surprises.

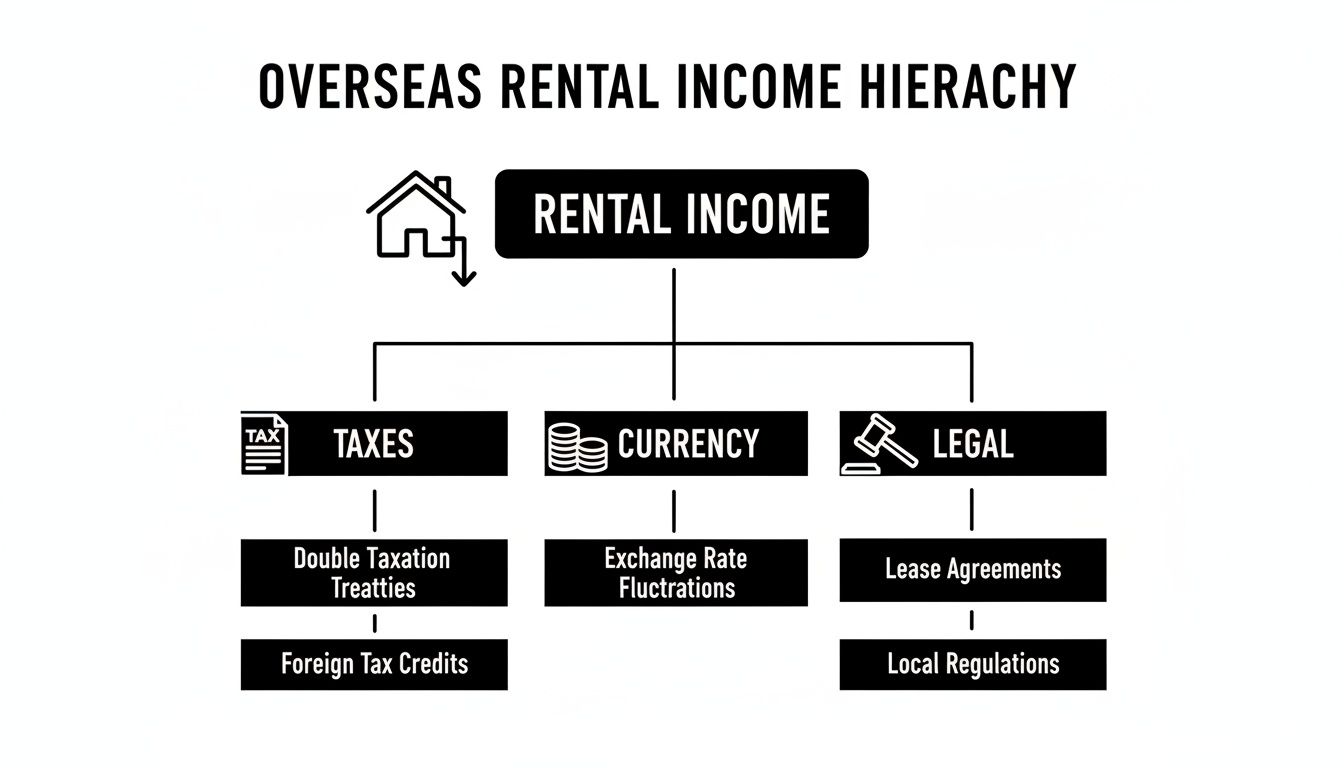

This diagram illustrates how gross rental income is reduced by the three main pillars of international property investment: local taxes, currency movements, and legal costs.

Each of these can take a significant portion of your final profit, which is why detailed analysis is essential before making an offer.

Gross Rental Yield: The Starting Point

Gross rental yield is the simplest calculation. It is a useful first filter for quickly comparing different properties or markets, giving a snapshot of potential income relative to the purchase price.

The formula is straightforward:

Gross Rental Yield (%) = (Total Annual Rental Income / Property Purchase Price) x 100

For instance, a flat in Lisbon purchased for €300,000 and renting for €1,500 per month (€18,000 annually) has a gross yield of 6%. This is a solid starting point, but the figure ignores all real-world operational costs.

Net Rental Yield: The Metric That Matters

This is the most crucial metric. Net rental yield provides a far more accurate picture of an investment's financial health because it accounts for all operational costs. Calculating this figure correctly is the key to understanding your true return.

To work it out, first sum all annual running costs and subtract them from your gross income. These costs almost always include:

- Property Management Fees: Typically a percentage of the rent, often between 8-12%.

- Maintenance and Repairs: A sensible rule of thumb is to budget 1% of the property's value each year.

- Local Property Taxes: These vary hugely between countries, so thorough research is vital.

- Landlord Insurance: Essential for protecting your asset against unforeseen events.

- Service Charges or HOA Fees: Common in apartment buildings to cover communal upkeep.

- Vacancy Periods (Voids): It is prudent to budget for at least one month of vacancy per year.

Once these costs are understood, calculating your net yield is simple. The table below provides a real-world example to show just how different the gross and net figures can be.

For a more detailed analysis of these calculations, consult our full guide on how to calculate return on investment (ROI) for real estate, which breaks down the concepts further.

Gross vs Net Rental Yield Calculation Example (Property in Manchester, UK)

This table shows a side-by-side comparison for a typical buy-to-let property in Manchester, highlighting how operational costs dramatically alter the final yield.

| Metric | Calculation/Value | Notes |

|---|---|---|

| Purchase Price | £200,000 | The total price paid for the property. |

| Monthly Rent | £1,000 | The income received from the tenant. |

| Annual Gross Rent | £12,000 | (£1,000 x 12 months). |

| Gross Rental Yield | 6.0% | (£12,000 / £200,000) x 100. |

| Annual Running Costs | £3,440 | See breakdown below. |

| Management Fees (10%) | £1,200 | A typical agent fee. |

| Maintenance (1%) | £2,000 | A conservative annual buffer for repairs. |

| Insurance | £240 | Standard landlord insurance policy. |

| Annual Net Rent | £8,560 | (£12,000 – £3,440). |

| Net Rental Yield | 4.28% | (£8,560 / £200,000) x 100. |

As demonstrated, the 6.0% gross yield appeared attractive, but the true return is closer to 4.28% once necessary costs are factored in. This is the figure that should inform investment decisions.

Calculating Cash Flow: Your Take-Home Profit

After calculating your net rental income, the final step is to determine your cash flow. This is the actual money remaining after all bills, including mortgage payments, have been paid.

Cash flow is the ultimate test of an investment's month-to-month viability. It is the difference between your net rental income and your mortgage payment.

Monthly Cash Flow = Net Monthly Rental Income – Monthly Mortgage Payment

A positive number indicates the property is self-sustaining and generating a surplus. A negative number means you must supplement it from your own funds to break even.

Local market conditions are paramount. For example, ONS data for 2024 shows UK rents reached record highs. However, regional differences are substantial; higher rents in London and the South East are balanced by more modest figures in areas like the North East, illustrating how location dictates potential cash flow.

Navigating International Tax Obligations

Earning rental income from an overseas property introduces a new level of complexity: international tax.

Failure to manage this correctly can be a costly mistake, potentially leading to significant penalties that erode profits. The most immediate hurdle is dual taxation: the risk of being taxed on the same income in two different countries.

This occurs because the country where the property is located (the source country) will almost certainly tax the income generated within its borders. Simultaneously, your country of residence will typically tax you on your worldwide income. Without specific legal frameworks, you would be taxed twice.

How Double Taxation Treaties Provide Relief

Fortunately, most countries have mechanisms to prevent this. The key instrument is the Double Taxation Treaty (DTT), a formal agreement between two nations that determines which country has taxing rights and how to avoid double taxation.

These treaties do not eliminate tax. Instead, they provide a system for relief, most commonly through a foreign tax credit. This allows you to subtract the tax already paid in the property's country from the tax owed in your home country.

Key Takeaway: A Double Taxation Treaty does not erase your tax bill. It ensures that tax paid in one country can be offset against the tax due in another, so you are not penalised for investing across borders.

For example, a UK resident with a flat in Spain will first file a return and pay income tax to the Spanish authorities. When declaring that same rental income on their UK tax return, they can claim a credit for the amount paid to Spain, directly reducing their final UK tax liability.

You can understand property taxes in greater detail with our comprehensive guide for a deeper analysis of these mechanics.

Your Reporting Duties: Home and Away

Proper compliance means managing two distinct sets of reporting obligations each year.

- Host Country Filing: As a non-resident landlord, you will almost always be required to file an annual tax return in the country where your property is located. This return will outline your rental income and the specific expenses that country’s tax laws permit you to deduct.

- Home Country Declaration: You must also declare all your overseas rental income on your domestic tax return. This is the crucial step where you claim your foreign tax credit to prevent being double-taxed.

Meticulous record-keeping of all income and expenditure is non-negotiable. This documentation serves as proof for completing both tax returns accurately and substantiating every deduction claimed.

A Comparison of Tax Regimes: UK, Spain, and USA

Tax rules, particularly regarding deductible expenses, vary significantly between countries. A brief comparison of popular markets demonstrates the importance of local knowledge.

- United Kingdom: The UK allows deductions for most day-to-day running costs, such as letting agent fees, maintenance, and insurance. However, a major change in recent years means mortgage interest relief for individual landlords is now provided as a 20% tax credit, which is less generous than a full deduction for higher-rate taxpayers.

- Spain: For non-resident landlords from other EU/EEA countries, the rules are quite favourable, allowing a wide range of deductions similar to a Spanish resident. However, for landlords from outside the EU, including post-Brexit UK investors, the regime is much harsher. They face a flat tax on their gross rental income with no deductions allowed.

- United States: The US tax system permits a broad set of deductions, including mortgage interest, property taxes, and maintenance. Crucially, it also offers a powerful non-cash deduction called depreciation. For foreign properties owned by US taxpayers, the building's value can be depreciated over 30 years, which can significantly reduce taxable income each year.

The UK remains a significant market for property investors. The latest Gov.uk statistics show that total property income declared by unincorporated landlords remains a substantial part of the economy, highlighting the scale of the rental market and why tax compliance is so important. You can find out more about the UK's property rental income landscape on Gov.uk.

These differences underscore a golden rule of global investing: always seek professional tax advice. An accountant with expertise in both your home and host country's tax laws is not a luxury—it is essential for compliance and financial optimisation.

Managing Currency Risk to Protect Your Profits

Earning rent from an overseas property involves entering the global currency market. The value of your overseas rental income is not fixed; it fluctuates daily with exchange rates, creating a significant and often overlooked risk to your net returns. A sudden fall in the local currency’s value can erode profits when you repatriate them.

This currency risk is, of course, a double-edged sword. A favourable shift can boost returns, but an adverse one can erase a large portion of your cash flow. A 5% drop in the Euro against the Pound, for instance, means that €1,500 in rent from a Spanish property is worth considerably less when it arrives in your UK bank account. Managing this volatility is a necessity for any serious global investor.

Practical Strategies to Mitigate Currency Volatility

Investors are not powerless against these fluctuations. Smart investors use established strategies to shield their income from market instability and create more predictable returns.

- Use a Foreign Exchange (FX) Specialist: High-street banks are known for wide spreads and high fees on international transfers. FX specialists, by contrast, offer more competitive exchange rates and lower costs. This simple change can save a noticeable amount on every transaction.

- Set Up a Forward Contract: This is a powerful tool for locking in an exchange rate for a future date. For example, you could agree on a rate today for repatriating the next 12 months of rental income. This provides complete certainty over your returns, regardless of market movements.

- Maintain a Local Bank Account: Keeping a bank account in the country where your property is located is highly advantageous. It allows you to pay local expenses—such as management fees, taxes, and repairs—in the local currency. This strategy minimises the number of currency conversions, reducing both transaction costs and risk exposure.

By combining these methods, you can build a robust defence against currency risk. The goal is not to outsmart the market, but to remove its unpredictability from your financial planning, ensuring your investment remains profitable.

Repatriating Your Profits Effectively

Bringing profits home is the final step and requires careful planning. Repatriation is more than a simple bank transfer; you must consider fees, transfer limits, and legal reporting requirements.

Banks and money transfer services often impose daily or monthly limits on international transfers, which could be a hurdle when moving large sums. You also need to be aware of transfer fees, which can be a flat rate or a percentage. Researching the most cost-effective method is crucial. Understanding the rules around financing an investment property can also offer useful insights into handling large international capital flows.

Finally, remember that large international transfers can trigger reporting obligations in both the sending and receiving countries under anti-money laundering regulations. Always keep clear, organised records of these transactions to ensure full compliance.

Structuring Your Investment for Success

Owning a property thousands of miles away demands a solid operational and legal foundation. The structure you choose for your investment directly impacts your tax efficiency, liability, and administrative burden. This decision sets the tone for your entire overseas rental income journey.

A well-chosen structure can shield your personal assets and optimise your tax position, whereas a poor choice can lead to unnecessary costs and legal complications. Let’s explore the main ownership models and the practicalities of day-to-day management.

Choosing Your Ownership Model

One of the first major decisions is how to hold the property legally. You generally have two main options: holding it in your personal name or establishing a local limited company to act as the owner. Each has significant implications.

Holding a property in your personal name is the simplest route. The legal process is often more straightforward, and ongoing administrative costs are minimal. The downside is the lack of liability protection. If a tenant brings a lawsuit, your personal assets could be at risk.

Establishing a local limited company, often known as a Special Purpose Vehicle (SPV), creates a legal firewall between the property and your personal finances. This is a common strategy for seasoned investors, as it separates business liabilities from personal wealth. However, it involves higher setup and annual running costs, including accountancy fees and corporate filings.

The optimal choice often depends on the host country's specific legal and tax framework. In some jurisdictions, corporate ownership offers significant tax advantages on rental income and capital gains, which can easily outweigh the administrative costs.

Day-to-Day Property Management

With the ownership structure decided, the next challenge is managing the property from a distance. Again, there are two primary paths: self-management or hiring a professional property management firm. The right choice depends on your experience, local contacts, and desired level of involvement.

Self-management can maximise net rental income by avoiding management fees, which typically range from 8% to 12% of the monthly rent. This approach is only feasible for investors with a trusted network on the ground—such as family, friends, or reliable tradespeople—who can handle emergencies and routine maintenance. It requires significant time and effort, especially across different time zones.

Hiring a professional property management company is the more common route for overseas investors. They handle everything from finding tenants and collecting rent to managing maintenance and ensuring legal compliance, providing a genuinely passive investment experience. The fee is a deductible expense, and the peace of mind it offers is often invaluable.

Property Management Options Compared

This table breaks down the key differences between self-management and professional management to help you determine which approach best fits your investment style.

| Aspect | Self-Management | Professional Management |

|---|---|---|

| Cost | Lower direct costs (no management fees). | Higher costs (8-12% of rent) but predictable. |

| Time Commitment | High. Requires active involvement in all aspects. | Low. A passive, hands-off experience. |

| Local Knowledge | Requires an existing, reliable network. | Provides instant access to local expertise. |

| Legal Compliance | Responsibility falls entirely on you. | The firm ensures compliance with local tenancy laws. |

| Liability | Direct exposure to tenant issues and disputes. | Acts as a buffer between you and the tenant. |

When vetting a potential management partner, ensure they provide a comprehensive service. Ask critical questions about their tenant screening process, how they handle late payments, and their network of maintenance contractors. A reliable partner is the cornerstone of a successful overseas rental income stream.

Comparing Global Rental Yields And Markets

Before analysing potential overseas rental income, it is essential to understand the fundamental differences between global property markets. At a high level, they fall into two categories: established markets, known for stability, and emerging markets, which offer higher growth potential but with greater risk.

Your choice depends on your investment strategy and objectives.

Established Markets: The Appeal of Stability

Markets such as London, Berlin, or New York are mature and predictable, with robust legal systems, high liquidity, and a consistent pool of tenants. Capital growth may be slower and steadier, but rental income is highly reliable.

These locations attract investors who prioritise wealth preservation and steady, long-term cash flow over speculative gains. The trade-off is that high property prices typically result in lower net rental yields, often in the 2.5% to 4% range.

Stable markets are supported by strong economic fundamentals, such as consistent GDP growth and rising populations, which sustain housing demand. The UK property market is a classic example of this resilience.

ONS data shows a clear and steady rise in UK rents, reflecting market stability. In England, average private rents increased by 8.9% in the 12 months to April 2024. This consistent, data-backed growth offers reassurance to conservative investors. You can examine these private rental market trends from the ONS for more detail.

Emerging Markets: The Quest for Higher Yields

Emerging markets in locations like Portugal, parts of Eastern Europe, or Southeast Asia offer a different risk-reward profile. These regions often feature rapidly growing economies, a surge in foreign investment, and a rising middle class—all drivers of a property boom.

The main attraction is the potential for significantly higher rental yields, often ranging from 5% to over 8%. This is because property prices remain low relative to the rent they can command. Lisbon, for instance, has seen a huge influx of interest due to its quality of life and investment-led visa programmes, causing rental demand to soar.

However, higher reward comes with greater risk. These markets can be volatile, and investors must consider potential downsides:

- Political and Economic Instability: Sudden changes in government policy can impact property rights and deter investors.

- Currency Fluctuations: Currencies in developing nations can be volatile, which can either boost or reduce the value of repatriated profits.

- Legal Ambiguity: Property laws may be less developed or transparent, requiring more thorough due diligence.

Choosing between these market types is a critical first step. If your goal is a stable, passive income stream, a property in a major German city could be ideal. If you have a higher risk tolerance and are seeking strong growth, our guide on the best buy-to-let locations globally might point you toward a high-potential emerging market.

A balanced portfolio, incorporating both established and emerging markets, is often the most prudent approach.

Frequently Asked Questions

Investing in overseas property can raise many questions. Below are clear, straightforward answers to the most common queries from international investors, designed to provide clarity and confidence.

How Should I Legally Own My Overseas Property?

This is one of the first major decisions, with long-term consequences. The simplest route is to buy in your personal name. It is quick and inexpensive but offers no liability protection. In a legal dispute, your personal assets could be at risk.

A more professional approach is to establish a local limited company or Special Purpose Vehicle (SPV). This creates a legal firewall between your investment and personal finances. While it costs more to set up and maintain, the liability protection and potential tax advantages make it the preferred method for serious investors. Local laws vary, so professional advice is essential.

How Can I Manage Tenants and Repairs From Afar?

Managing a property from a distance can be challenging. Self-management is possible if you have a reliable contact on the ground, but for most investors, a professional property management company is the prudent choice.

These firms act as your local representatives, handling everything from tenant screening and rent collection to maintenance issues. Their fee, typically 8-12% of the monthly rent, is a tax-deductible expense that provides invaluable peace of mind. A good manager protects your asset and ensures a smooth income flow.

What Happens If My Property Is Vacant For a Long Period?

Vacancy—or a "void period"—is an unavoidable aspect of being a landlord. When the property is empty, income ceases but costs continue. You remain liable for the mortgage, insurance, service charges, and local taxes. It is therefore crucial to build a buffer for vacancies into your financial forecasts; assuming one month of vacancy per year is a safe starting point.

A strong property manager is your best defence against long void periods. They will market the property effectively, price it correctly, and secure reliable, long-term tenants. Maintaining the property in excellent condition also reduces the time it sits empty between tenancies.

Do I Still Have To Report Income If The Property Makes a Loss?

Yes, absolutely. You are required to report your rental activity to the tax authorities in both your home country and the host country, even if you incur a loss for the year. While it may seem like unnecessary administration, there is often a benefit: most tax systems allow you to carry forward those losses to offset profits in future years, which can significantly reduce your future tax liability. Meticulous record-keeping is non-negotiable for compliance.

At World Property Investor, we provide the in-depth guides and market analysis you need to make informed decisions. From understanding local tax laws to comparing rental yields in the world's top markets, our resources are designed to help you invest with confidence. Explore our global property investment guides to start your journey.