If you already own property, you know where the friction sits. New acquisitions need serious capital. Exits take time. One vacancy, one planning issue, or one poor letting decision can drag on results far longer than the original underwriting suggested.

That’s usually the point where investors start asking a better question. Not “Should I stop buying property?” but “How do I add property exposure without adding another building, another financing process, and another management headache?” That’s where understanding what is a real estate investment trust becomes useful.

A REIT lets you invest in property through shares rather than deeds. You’re still taking a view on rents, occupancy, asset quality, debt levels, and management. But you’re doing it through a listed structure that can be bought and sold far more easily than a flat, warehouse, or office block. For investors who’ve only worked through direct ownership, it often feels less like leaving property behind and more like adding a more liquid layer to the same playbook.

If you're still building your base knowledge before moving into listed real estate, this guide on real estate investments for beginners is a helpful starting point.

An Introduction to REITs for Property Investors

Direct property gives you control. You choose the asset, negotiate the purchase, shape the refurbishment plan, pick the tenant profile, and decide when to refinance or sell. That control can be valuable, but it comes with concentration risk and operational drag.

A REIT is often the tool investors use when they want property income without owning a single address outright. Instead of buying one asset in one city, you buy into a managed portfolio of income-producing real estate. In practice, that can mean exposure to logistics, offices, residential blocks, healthcare assets, retail parks, or specialist sectors that would be hard to access alone.

Three points matter immediately for a direct investor:

- Liquidity matters: you can usually sell listed REIT shares far faster than you can sell a physical property.

- Diversification changes the risk profile: one REIT may hold many assets across locations and tenant types.

- Management is outsourced: you don’t handle repairs, lettings, voids, contractor disputes, or day-to-day operations.

Practical rule: Treat REITs as property exposure with stock market pricing, not as a substitute for cash.

That last point is where many first-time REIT investors misjudge the product. A good REIT can own strong assets and still see its share price move sharply when rates rise, sentiment turns, or equity markets sell off. So the right comparison isn’t “REIT versus property” in the abstract. It’s “listed property with daily pricing” versus “private property with slower price discovery”.

For global investors, REITs also open markets that are difficult to enter directly. Buying one apartment abroad is one thing. Building diversified exposure across several major cities and sectors is something else entirely. REITs solve that access problem neatly, especially when you want broad exposure before committing to direct acquisitions in a new market.

The Core Concept of a Real Estate Investment Trust

A real estate investment trust, or REIT, is best understood as a pooled property vehicle. Think of it as a fund-like structure for real estate. Investors buy shares. The REIT uses that pooled capital to own, operate, and sometimes develop income-producing properties.

Instead of you buying one asset directly, the REIT management team acquires and manages a portfolio. Your return usually comes from two places. First, distributions paid out from rental income. Second, changes in the market value of the shares.

How the structure works in practice

A straightforward way to think about it is this:

- Investors contribute capital by buying shares.

- The REIT acquires property assets or property-related interests.

- Properties generate rental income through leases.

- Management handles operations such as financing, leasing, asset management, and disposals.

- Income is distributed to shareholders under the rules of the relevant REIT regime.

That’s why REITs appeal to investors who understand property economics but don’t want every return tied to one roof, one tenant, or one local council area.

If you already think in terms of rents, yields, occupancy, and capital values, you’re not learning a completely new asset class. You’re learning a new wrapper around familiar underlying drivers. This broader guide on how to make money in property helps place REIT income alongside other property strategies.

What a REIT gives you that direct ownership often doesn’t

The strongest REIT advantage isn’t magic. It’s scale and access.

A listed REIT can hold assets that most individual investors won’t buy directly, such as major logistics estates, central business district offices, healthcare portfolios, or institutional-grade residential blocks. It also brings in specialist teams to manage leases, refinancing, redevelopment, and tenant relationships.

That solves several practical problems:

- Entry barriers fall: you don’t need to fund an entire commercial acquisition yourself.

- Professional management takes over: leasing and capital allocation sit with the operating team.

- Trading is simpler: you buy and sell shares through a brokerage account rather than through a legal completion process.

- Geographic reach improves: you can access markets where direct ownership may be complex, costly, or operationally awkward.

A REIT is property ownership separated from property administration.

That doesn’t mean every REIT is automatically good. Some own excellent assets and allocate capital well. Others overpay, overborrow, or drift into weak sectors. The structure is useful, but the underlying real estate and the quality of management still determine outcomes.

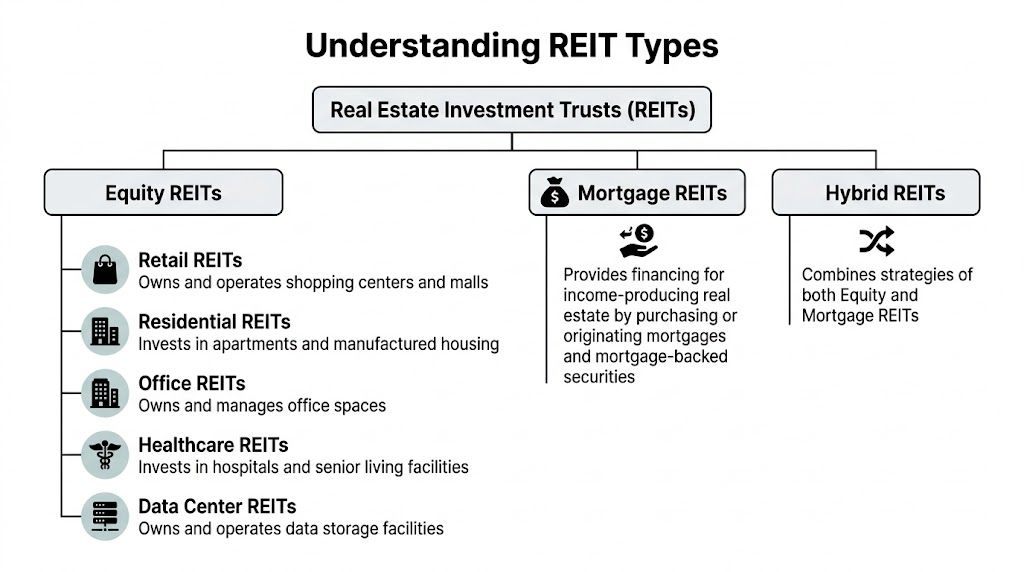

Understanding the Different Types of REITs

Type matters more than the REIT label itself. Two companies can both sit in the listed real estate bucket and still behave very differently in a portfolio. One may rise and fall with rents and occupancy. Another may be driven more by credit spreads, refinancing conditions, and the cost of debt.

For a global property investor, this distinction is even more important. The same label can cover different asset mixes across the US, UK, Australia, and Singapore. In one market, listed real estate may be heavy in data centres or logistics. In another, you may find more retail, office, or residential exposure. Start with how the vehicle makes cash, then look at the local market and tax framework.

Equity REITs

An equity REIT owns physical property and earns income mainly from rent. This is the closest listed equivalent to direct ownership. The difference is that you are buying a stake in a managed portfolio rather than one building.

Common equity REIT sectors include:

- Retail REITs: shopping centres, retail parks, and high street assets

- Residential REITs: apartments, build-to-rent portfolios, and similar housing stock

- Office REITs: business space in major employment centres

- Healthcare REITs: hospitals, clinics, and care-related property

- Industrial and logistics REITs: warehouses and distribution facilities

- Data centre REITs: specialised assets linked to digital infrastructure

Sector selection starts to matter. A warehouse REIT in Australia, a student housing REIT in the UK, and a suburban apartment REIT in the US may all look defensive on the surface, but tenant demand, lease length, rent review terms, and valuation drivers are not the same.

Mortgage REITs

A mortgage REIT, often called an mREIT, usually invests in property loans, mortgage securities, or other real estate debt instruments rather than owning buildings directly. Its income comes from financing margins and portfolio yield, not from collecting rent from tenants.

For an investor used to buying property outright, the practical comparison is simple. An equity REIT works more like a landlord. A mortgage REIT works more like a lender with property as the underlying exposure.

That changes the risk profile. Mortgage REITs are usually more sensitive to funding costs, credit losses, refinancing pressure, and shifts in rate expectations. They can produce attractive income in the right conditions, but they are a different proposition from owning a portfolio of offices, flats, or warehouses.

Hybrid REITs

A hybrid REIT combines direct property ownership with exposure to real estate debt. In practice, these can be harder to assess because the investor has to judge two engines at once. One part of the business depends on rents, occupancy, and asset management. The other depends on loan performance, financing spreads, and capital structure discipline.

That mixed model is not automatically a problem. It just demands clearer analysis.

If you cannot explain a REIT’s cash flow in one sentence, you should not buy it yet.

Listed versus non-traded structures

Most international investors begin with listed REITs because pricing is visible and dealing is straightforward. Non-listed and thinly traded structures require more caution. Valuations may be less frequent, exit routes can be narrower, and fee structures can be harder to compare. If you want a legal and investor-protection lens on that part of the market, this overview of a non traded real estate investment trust is worth reading before committing capital.

A useful way to assess any REIT is to ask which part of your direct property experience transfers. Investors coming from residential ownership often assume a residential REIT will behave like a scaled-up private portfolio. Sometimes it does. Sometimes it does not, especially once public market pricing, external management decisions, and country-specific tax treatment for overseas holders come into play. If you already understand the operating logic behind buy-to-rent investment, use that as your starting point, then adjust for the fact that listed real estate trades daily and can reprice faster than the buildings themselves.

The Mechanics and Rules That Govern REITs

A direct property investor usually asks the same question at this stage. What stops a listed landlord from calling itself a REIT and paying out whatever story suits the market?

The answer is the rulebook. A REIT sits inside a legal and tax framework that dictates what it can own, how much of its income it must distribute, and how investors are taxed on those payments. That framework is not identical across markets. The US, UK, Australia, and Singapore all use the REIT label, but the investor experience can differ materially once you factor in distribution rules, withholding tax, and listing requirements.

In the UK, a company must be UK-resident, listed on a recognised stock exchange, and focused on a qualifying property rental business to enter the REIT regime. It must also distribute at least 90% of the profits from that rental business as Property Income Distributions, usually called PIDs. In return, qualifying rental profits are generally exempt from corporation tax inside the REIT structure.

That payout rule shapes the investment case. REITs are often attractive for income because they pass through a large share of rental earnings. The trade-off is simple. Less cash stays inside the vehicle, so external funding, asset recycling, or equity issuance often plays a bigger role in growth than it would in a private portfolio with retained earnings.

The UK rules that matter in real life

The UK regime also tests what constitutes the business, not just what it calls itself. Broadly, the company needs most of its profits and asset value tied to qualifying property rental activity. Ownership concentration rules also matter. A structure that becomes too tightly held can run into problems with REIT status.

For investors, that matters because the wrapper affects behaviour. Management has less freedom to drift far from income-producing property, less freedom to hoard cash, and a stronger incentive to protect recurring rental income. If you come from direct real estate, that discipline is one of the main differences between owning a building privately and owning a quoted property vehicle through a REIT regime.

It also changes how you judge returns. A private investor may focus first on gross yield and a future sale price. A REIT investor still cares about both, but has to judge them through reported distributions, share pricing, and recurring cash flow. If you want a refresher on the property-side maths behind that comparison, this guide on how to calculate return on investment for property is a useful baseline before translating those numbers into listed real estate.

Debt levels, refinancing, and asset discipline

Borrowing is part of the model. REITs use debt to acquire assets, refinance maturing facilities, and manage capital more efficiently across a portfolio. That can improve returns in stable conditions. It also creates pressure when interest costs rise, lenders tighten terms, or asset values fall.

The analysis of listed REITs leans more practical than theoretical. A good management team protects the balance sheet before it protects the headline yield. That can mean selling assets into a weak market, issuing equity at an uncomfortable time, or slowing acquisitions even when brokers are pitching growth.

The patterns worth watching are usually clear:

- conservative debt levels relative to asset value

- staggered debt maturities rather than large near-term refinancing cliffs

- rental income that is diversified by tenant, sector, and lease expiry

- asset sales driven by capital discipline, not distress

- dividends covered by recurring cash flow rather than short-term balance sheet decisions

The warning signs are just as clear. An unusually high yield can reflect market concern, not generosity. Short debt maturities, weak occupancy, or heavy exposure to one tenant group can turn a normal rate cycle into a capital problem.

Investor lens: Read the dividend together with debt levels, refinancing timetable, asset quality, and management discipline.

Why global investors need to watch tax mechanics

Cross-border tax treatment is where many new REIT investors make poor comparisons with direct property. The quoted yield on screen is not the amount a non-resident necessarily receives in cash.

In the UK, PIDs can be subject to withholding tax, and the final outcome depends on your residence, treaty position, and how you hold the investment. The same issue appears in other major REIT markets, but with different rules. US REIT distributions can be treated differently from UK PIDs. Australian A-REIT income can carry its own tax characteristics. Singapore REITs are often approached differently again by foreign investors.

So the practical test is not, "Which REIT market offers the highest yield?" It is, "After local tax, home-country tax, treaty relief, and dealing costs, which market gives me the cleanest income and the exposure I want?" For a global property investor, that question matters as much as the buildings themselves.

Key Metrics for Analysing a REIT Investment

A listed REIT can own excellent buildings and still be a poor investment at the wrong price or with the wrong balance sheet. Direct property investors already know the principle. Asset quality, cash flow, debt, and entry price have to line up. The difference is that a REIT reports those moving parts through company accounts rather than a single asset appraisal.

FFO and AFFO

Start with cash earnings, not headline profit.

Traditional net income is a weak guide for property because accounting depreciation can reduce reported earnings even while the underlying real estate remains income-producing and, in some periods, rises in value. REIT analysis therefore starts with Funds From Operations (FFO) and then moves to Adjusted Funds From Operations (AFFO).

In practical terms:

- FFO strips out some of the accounting noise and gets closer to recurring operating performance.

- AFFO adjusts further for recurring capital expenditure, leasing costs, and other items that affect the cash available for distribution.

For a direct landlord, the comparison is straightforward. FFO is closer to property operating profit than statutory earnings. AFFO is closer to asking, after the recurring spend needed to keep rents coming in, how much cash is left for owners.

The trade-off matters. Some REITs look cheap on FFO but less attractive on AFFO because their assets need heavy ongoing capital spend to hold occupancy and rent levels.

NAV and discounts

Net Asset Value (NAV) is the estimated value of the property portfolio and other assets, less debt and liabilities. It is the listed market version of asking what the equity in the portfolio is worth after lenders are paid.

That number helps, but it should never be treated as a final answer. Private real estate valuations are periodic and appraisal-based. Listed markets reprice daily. In stressed periods, a REIT can trade at a wide discount to NAV because equity investors expect weaker rents, lower values, or dilutive refinancing before those pressures fully show up in appraised values.

A premium to NAV can also be rational. Investors may be paying for better management, stronger development capability, lower funding costs, or access to sectors where private buyers struggle to build scale. This is common in higher-quality platforms in markets such as the US, Australia, and Singapore, where governance, sector specialization, and capital access can materially affect returns.

A discount to NAV is only interesting if the assets are sound, debt is manageable, and management has realistic options to close the gap.

Dividend yield and payout cover

A dividend yield is simple to calculate and easy to misuse. In listed property, a high yield often signals risk before it signals value.

The better question is whether the dividend is covered by recurring cash flow. If distributions are running ahead of AFFO, or if management is relying on asset sales and new debt to maintain the payout, the headline yield can mislead. Direct property investors already apply this logic to a building with a strong passing rent but looming refurbishment costs or major lease expiry. The same discipline applies here.

Check four things together:

- Dividend cover from AFFO or equivalent recurring cash flow

- Lease expiry profile and tenant concentration

- Near-term debt maturities and interest-rate exposure

- Management's record on capital allocation

The utility of global comparison is evident. A 6 percent yield from a US REIT, a UK REIT, an Australian A-REIT, and a Singapore REIT does not mean the same thing once you account for sector mix, debt structure, withholding tax, and the local rules governing distributions. For non-resident investors, the cash that reaches your account may differ materially from the quoted yield on screen.

Debt metrics that matter

Property investors tend to spot asset risk quickly and underweight financing risk until the cycle turns. With REITs, debt deserves equal attention.

Focus on loan-to-value, interest cover, and the debt maturity schedule. A REIT with a moderate debt level but a heavy refinancing wall in the next 12 to 24 months can be more exposed than one with slightly higher debt and well-staggered maturities. The same applies across jurisdictions, although the funding markets differ. US REITs often have deeper unsecured debt access. Smaller vehicles in other markets may rely more heavily on bank lines or secured financing against individual assets.

If you are used to underwriting direct property returns, it helps to revisit the basic maths behind how to calculate return on investment property before comparing listed vehicles. REIT analysis uses different labels, but the underlying questions remain familiar: what cash comes in, what capital has to stay in the asset base, what debt sits ahead of you, and what return is left for equity.

Tax should stay in view as well. Investors comparing REIT income with direct ownership often focus on yield first and tax second, which can distort the decision. If direct real estate is part of the same portfolio review, understanding investment property tax benefits can help frame the trade-off between listed income and the deductions sometimes available through direct ownership.

REITs Versus Direct Property Investment A Practical Comparison

Most investors don’t need to choose one camp forever. The better question is what role each format plays inside a portfolio.

Direct property is concentrated, operational, and controllable. REITs are diversified, liquid, and market-priced every day. Neither is automatically superior. Each solves a different problem.

Where REITs usually win

REITs tend to be stronger when you want broad exposure without operational friction. You can enter or exit more easily. You can diversify across assets and cities more quickly. And you don’t need to handle tenant management, refurbishment scheduling, or local compliance yourself.

For an international investor, that last point is especially useful. Direct ownership in another country often means legal coordination, tax filings, bank setup, and trusted local operators. Listed property removes much of that administrative burden.

Where direct property still has the edge

Direct ownership gives you decision-making power. You choose the financing methods, the refurbishment scope, the letting strategy, the timing of the sale, and the jurisdiction. Skilled operators can create value through work, not just through market movement.

There’s also a tax angle. Many investors prefer direct property because they can plan around depreciation rules, financing structures, and local deductions. If Australia is part of your portfolio review, this note on investment property tax benefits is a useful supplement because tax treatment often affects net returns more than headline yield does.

REITs vs Direct Property At a Glance

| Factor | Real Estate Investment Trusts (REITs) | Direct Property Investment |

|---|---|---|

| Liquidity | Usually easier to buy and sell through the market | Typically slower to exit |

| Diversification | Exposure to multiple assets and often multiple tenants | Often concentrated in one or a small number of properties |

| Management effort | Day-to-day operations handled by the REIT team | Owner or local manager handles operations |

| Entry cost | Usually lower capital barrier | Usually higher capital requirement |

| Control | Limited direct control over asset decisions | Full control over acquisition, management, and sale |

| Pricing | Repriced by the market continuously | Repriced less frequently and often less transparently |

| Financing exposure | Embedded at company level | Structured by the owner per asset or portfolio |

| Transaction process | Brokerage-based | Legal, financing, and conveyancing process |

Direct property rewards operating skill. REITs reward portfolio selection and discipline.

That difference is why many experienced investors use both. They keep direct assets where they have local knowledge or operational advantage, then use listed real estate to add sectors or countries that would be cumbersome to access physically. If you're thinking in terms of overall asset mix rather than isolated deals, this guide on how to build a portfolio of properties helps frame the decision properly.

How to Invest in REITs A Global Perspective

You own an office block in London and a warehouse in Sydney. You understand leases, refinancing risk, tenant quality, and local regulation. The shift with REITs is not learning real estate from scratch. It is learning how those same property risks show up inside a listed vehicle, under a specific country regime, with public market pricing layered on top.

For that reason, the first decision is usually not sector. It is vehicle choice. Buy individual REITs if you want targeted exposure and are willing to assess management, capital allocation, and balance sheet discipline company by company. Use a REIT ETF if the goal is broad access to listed property in one market or across several markets, with less single-name risk and less need to monitor every earnings call.

Neither route is necessarily better. A concentrated investor who knows logistics assets well may prefer a handful of operators in the US, Singapore, or Australia. An investor using REITs to complement a direct property portfolio often gets a cleaner result from a diversified fund first, then adds specialist names where conviction is high.

A practical process before buying

A disciplined cross-border process usually starts with the market, not the ticker.

Choose the jurisdiction first

The label "REIT" does not mean the same thing everywhere. The US, UK, Australia, and Singapore all offer listed real estate exposure, but the tax rules, distribution treatment, debt culture, and market depth differ enough to affect returns.Decide what role the position plays in the portfolio

Income, inflation linkage, geographic diversification, sector access, and liquidity are different objectives. A Singapore REIT bought for yield solves a different problem from a US data centre REIT bought for growth.Check tax treatment before you buy

Cross-border investors often focus on the quoted yield and ignore what arrives after withholding tax, treaty relief, and local tax filing. Net income is what matters.Review debt and refinancing exposure

In direct property, you would not buy first and ask about debt maturity later. Apply the same standard here. Short debt duration and weak interest cover can change the investment case quickly.Assess the underlying assets, then the manager

Good management can improve a strong portfolio. It rarely rescues poor assets bought at the wrong price.

How major REIT markets differ in practice

The UK works well for investors who want a familiar legal environment, established listed names, and transparent disclosure. The practical issue for non-residents is often not property quality but distribution treatment. UK property income distributions can be attractive on paper and less attractive after withholding if your ownership structure does not use treaty relief efficiently.

The US offers the broadest menu. If you want self-storage, manufactured housing, cell towers, healthcare, timber, or highly specialised logistics, you will usually find more choice there than in other listed markets. The trade-off is complexity. Non-US investors need to understand withholding, account setup, and how US tax rules interact with their home jurisdiction before treating the headline dividend as spendable income.

Australia has a long track record in listed property and tends to be well understood by institutional investors in the region. It can suit investors who want exposure to a market with strong pension participation and established real estate management platforms. The caution point is structure. Australian listed property vehicles do not map neatly onto UK or US assumptions on distributions, tax, or earnings presentation.

Singapore attracts many international investors for a simpler reason. It offers liquid access to Asian real estate through vehicles that are often income-focused and widely followed by yield buyers. That can be useful, but it also means popular names can trade more on yield sentiment than on changes in underlying property value.

Developed versus emerging REIT markets

Established REIT markets usually give you deeper liquidity, better research coverage, and a wider spread of sectors. That matters if you may need to reallocate quickly or build a position over time without moving the price too much.

Emerging markets can still be worthwhile. They may offer access to urbanisation, new logistics corridors, or sectors that are earlier in their institutional development. The trade-off is familiar to any direct investor who has bought outside a core market. Legal structure matters more. Governance matters more. Exit risk matters more.

I usually treat emerging market REIT exposure as something to earn into, not rush into. Start with position sizing discipline, assume less liquidity than the screen suggests, and give extra weight to sponsor quality and local financing conditions.

This short video gives a useful additional lens on how REIT structures work for investors evaluating listed real estate internationally.

What tends to work best

The investors who use REITs well usually keep the process simple and repeatable:

- Start with the objective. Decide whether you want income, diversification, liquidity, or access to a market you would not buy directly.

- Prefer broad exposure before stock picking. Build the country or regional allocation first. Add individual REITs only when you have a clear reason.

- Focus on net yield, not stated yield. Withholding tax and treaty mechanics can turn an attractive distribution into a mediocre one.

- Stay close to balance sheet risk. Public market pricing can hide property risk for a while, then reprice it fast.

- Use country differences to your advantage. The US may offer specialist sector access, the UK legal familiarity, Australia institutional depth, and Singapore liquid Asian exposure.

For a global property investor, that is the main attraction of REITs. They let you add countries, sectors, and operating platforms that would be slow, expensive, or tax-inefficient to access through direct ownership alone. The best results usually come from treating them as part of the property portfolio, not as a separate equity trade.

Frequently Asked Questions for International REIT Investors

How do rising interest rates affect REITs

Rates matter in two ways. First, they affect borrowing costs. Second, they affect how investors value future income streams. A REIT with heavy refinancing needs and weak rental growth can struggle when rates rise. A REIT with strong leases, conservative debt, and pricing power usually holds up better.

Can I invest only in residential REITs

Yes, in many markets you can target residential exposure specifically. That may include apartments, build-to-rent portfolios, student housing, or other housing-related formats. The key is not to assume “residential” means low risk. You still need to review tenant demand, local regulation, lease structure, and funding.

Are green and specialist REITs becoming more important

Yes, and this is one of the more meaningful shifts in listed real estate. Verified data notes that British Land reported ESG-compliant portfolios outperforming by 12% in rental growth, and that the FTSE EPRA/NAREIT UK Index indicated 65% of assets under management were in sustainable properties in 2026, up 22% since Q1 2025 (green-certified REIT trend data). For investors, that matters because sustainability upgrades increasingly affect tenant demand, leasing resilience, and future capital expenditure.

How are REIT dividends taxed for non-residents

It depends on the market, the legal form of the distribution, and your treaty position. In the UK, PIDs require particular attention because withholding treatment can reduce the amount you receive if you don’t reclaim correctly. The same principle applies elsewhere. Always check local rules, your residence-country treatment, and whether the income sits best in a personal account, company, pension wrapper, or other structure.

The biggest REIT mistake international investors make isn't choosing the wrong building type. It's ignoring how cross-border tax changes the return they actually keep.

Should I choose REITs instead of direct property

Usually, no. For most serious investors, this isn’t an either-or decision. Direct property remains useful when you have local knowledge, operating skill, or clear value-add plans. REITs are useful when you want liquidity, diversification, and access to markets or sectors that are harder to own directly.

World Property Investor helps you compare property markets, assess yields, understand taxes, and research where listed and direct real estate fit best in a global portfolio. Explore more market guides and investment analysis at World Property Investor.