For the global property investor, the Norwegian market presents a unique landscape where high living standards and a robust economy create both challenges and opportunities. This guide provides a data-driven analysis of the Norway cost of living, focusing on the metrics that matter for calculating risk, returns, and long-term asset growth.

Norway's reputation for being expensive is well-founded. However, this high-cost environment underpins its appeal for property investors, translating directly into market stability, low political risk, and sustained demand for quality housing from a high-earning population.

Understanding Norway's High-Cost, High-Reward Landscape

For property investors, the Norwegian market is a compelling, if capital-intensive, proposition. The high cost of living is intrinsically linked to the country’s high wages, comprehensive social welfare system, and exceptional quality of life. These are the fundamental drivers that guarantee long-term demand for quality housing.

This guide provides a detailed breakdown of the financial commitment required, setting the stage for crafting a successful investment strategy in one of Europe's most stable markets. It examines how factors like housing, utilities, inflation, and significant price differentials between established markets like Oslo and emerging ones like Stavanger directly impact an investor's bottom line.

Key Financial Realities for Investors

Data paints a clear picture of the premium attached to living in Norway. According to economic bodies, overall consumer prices are roughly 26.9% higher than in the United States and significantly above the UK average, a figure that reflects the country's robust economy and superior public services.

To understand the financial capacity of potential tenants, here is a baseline for average monthly costs, excluding rent.

Average Monthly Expenses in Norway (Excluding Rent)

| Household Type | Estimated Monthly Cost (NOK) |

|---|---|

| Single Person | 13,423.8 NOK |

| Family of Four | 48,389.8 NOK |

These figures provide a solid baseline for understanding the financial landscape your future tenants navigate.

An important takeaway for international investors is that while consumer prices are high, rental costs in Norway are, on average, 21.6% lower than in the United States, according to recent comparative data. This presents an interesting arbitrage opportunity.

This disparity indicates that while the capital outlay for property and general living expenses is high, potential rental yields can be more favourable than in some comparable Western markets. You can find more of the data behind these living expenses and explore the nuances in a detailed breakdown on Econumo's page covering the general Cost Of Living.

Regional Cost Variations

The cost of living in Norway is not uniform. Major cities have distinctly different cost structures, a crucial factor for investors analysing potential rental markets and projecting cash flow. Understanding these regional differences is fundamental to identifying where investment capital will work hardest and which tenant demographics offer the most stable returns.

- Oslo: As the capital and an established market, it has the highest cost of living index at 93.9, making it the most expensive city for residents and investors.

- Bergen: A major coastal and cultural hub, Bergen’s index sits at 89.6.

- Stavanger: A key city for the energy sector, Stavanger is an emerging market for investors, offering a slightly more affordable alternative with an index of 86.9.

These local variations are the first step toward building a viable investment strategy. The following sections provide a more granular analysis of these costs.

Breaking Down Housing and Utility Costs for Investors

In Norway, as in any market, housing is the largest single expense in most household budgets. For a property investor, a firm grasp of these costs is the foundation of a successful investment. The market presents two distinct opportunities: the high-cost, high-demand city centres, and the more affordable suburbs and smaller towns that offer their own unique advantages.

For a buy-to-let investment, analysis must go beyond surface-level numbers. A detailed breakdown of rental prices and running costs is essential for calculating net yield and forecasting cash flow. Without this, one is investing blind.

Analysing Rental Prices in Key Hubs

Rental prices across Norway’s main cities are a direct reflection of their economic strength and desirability. As the capital and business engine, Oslo naturally commands the highest rents, creating a premium market that demands significant capital but can deliver strong, stable returns.

- Oslo: A one-bedroom flat in a central district can command between 12,000 to 15,000 NOK per month. A family-sized home in a desirable area will be considerably more.

- Bergen and Stavanger: As key coastal and energy hubs, these cities have robust rental markets. Rents for a similar one-bedroom flat are roughly 10-20% lower than in Oslo, offering a more accessible entry point for some investors.

A unique feature of the Norwegian rental market is the security deposit. Landlords typically require a deposit equal to three months' rent, which must be held in a joint account. This is a substantial upfront cost for tenants and shapes market dynamics. As explored in our guide on how property location impacts investment success, understanding these local nuances is vital.

The Hidden Costs in Norwegian Utilities

Beyond the headline rental figure, an astute investor must identify the "hidden" running costs that can erode net yield. In Norway, utilities are a significant and variable expense that cannot be ignored.

For buy-to-let investors, Norway's combination of high property values and moderate rental growth creates a market requiring careful calculation. Substantial utility bills, especially for seasonal heating, must be factored into net yield calculations to gain a true picture of an investment’s performance.

For a standard flat, monthly bills covering electricity, heating, water, and waste collection will typically fall between 1,500 and 2,500 NOK. The main variable is the seasonal swing in heating costs. Norway’s cold winters mean heating bills can easily double or even triple compared to the summer. This fluctuation must be built into any cash flow forecast to avoid negative surprises.

Calculating Net Yields Accurately

Gross rental yield—annual rent divided by property price—is a superficial metric. The real measure of a successful investment is the net rental yield, which accounts for all running costs.

To calculate net yield, all outgoings must be subtracted from the gross rental income. These always include:

- Utilities: Even if the tenant pays them, knowing the costs helps in setting a competitive rent. If utilities are included in the rent, the model must account for seasonal spikes.

- Maintenance and Repairs: A standard rule is to budget 1% of the property's value annually.

- Management Fees: Using a property manager typically costs 8-12% of the monthly rent.

- Property Taxes (Eiendomsskatt): This varies by municipality but is a recurring annual expense.

- Insurance: Essential for protecting the asset against damage and liability.

By meticulously tracking these costs, an investor can move from a vague gross yield to a precise net yield. This provides a clear, realistic picture of an investment's performance and the true return on capital. In a sophisticated market like Norway, this data-driven approach is the only way to invest with confidence.

How Inflation Trends Affect Your Investment Returns

A robust investment strategy must look beyond today's prices. For any global property investor considering Norway, understanding the country's economic climate is fundamental to long-term success. Inflation, in particular, acts as a silent partner: it can either erode returns or contribute to their growth, depending on how it is managed.

The Norway cost of living is tied directly to its inflation rate. For a landlord, rising inflation means the cost of everything from property maintenance and management fees to insurance premiums will increase. If rental income does not keep pace, net yield will shrink.

Understanding Recent Inflationary Pressures

The economic picture in early 2026 offered mixed signals. The country's annual inflation rate saw a temporary jump, hitting 3.6% in January 2026—its highest point in four months, according to Statistics Norway—before cooling to 2.70% by February. This short-term volatility directly affects the running costs of a rental property.

This inflationary pressure was most noticeable in categories that directly impact a landlord's balance sheet. Housing-related costs, which cover water, electricity, and fuel, climbed by 4.3% year-on-year in January. Simultaneously, transport costs, a key factor for both tenants and property managers, rose by 4.4%. For a closer look at the data, you can review the complete analysis on Trading Economics, which offers a deeper perspective on Norway's consumer price index movements.

Building Resilient Financial Models

The key to managing these fluctuations is to integrate them into financial models from the outset. While recent figures show volatility, long-term forecasts suggest a return to a more stable environment. Projections from major economic bodies point to Norway’s inflation normalising, trending towards roughly 2.40% annually by 2027 and 2.10% by 2028.

For an investor, these long-term projections are far more important than short-term spikes. They allow for the construction of a resilient financial model that anticipates cost increases and plans for sustainable rental growth, protecting net returns over the life of the investment.

This foresight enables smarter strategic decisions. For instance, one can factor in a projected 2-3% annual increase in the operational budget. This ensures cash flow remains positive even as the cost of maintenance and services rises. To refine these projections, our dedicated article explains in detail how to calculate your true return on investment (ROI) for real estate.

The Dual Impact on Expenses and Tenant Affordability

Inflation not only raises an investor's expenses; it also impacts tenant affordability. This is a delicate balance that every successful landlord must manage.

- Operational Costs: As inflation drives up the price of materials and labour, the budget for repairs and general upkeep will need to grow. Likewise, property management fees will likely rise to cover their own increased costs.

- Tenant Affordability: Simultaneously, tenants face higher prices for daily essentials. Grocery bills, a core household expense, have risen with inflation, with a typical monthly shop now costing between 2,500 to 4,000 NOK per person.

This dynamic creates a natural tension. Rents must increase to cover rising costs, but tenants' ability to afford those increases is also under pressure. Setting rents too high risks longer vacancy periods; setting them too low erodes profit margins.

Understanding this balance is key to remaining competitive. By monitoring inflation trends and their impact on the Norway cost of living, investors can set rents that are both profitable and sustainable, forecast income growth with more accuracy, and make strategic decisions that protect returns against economic shifts.

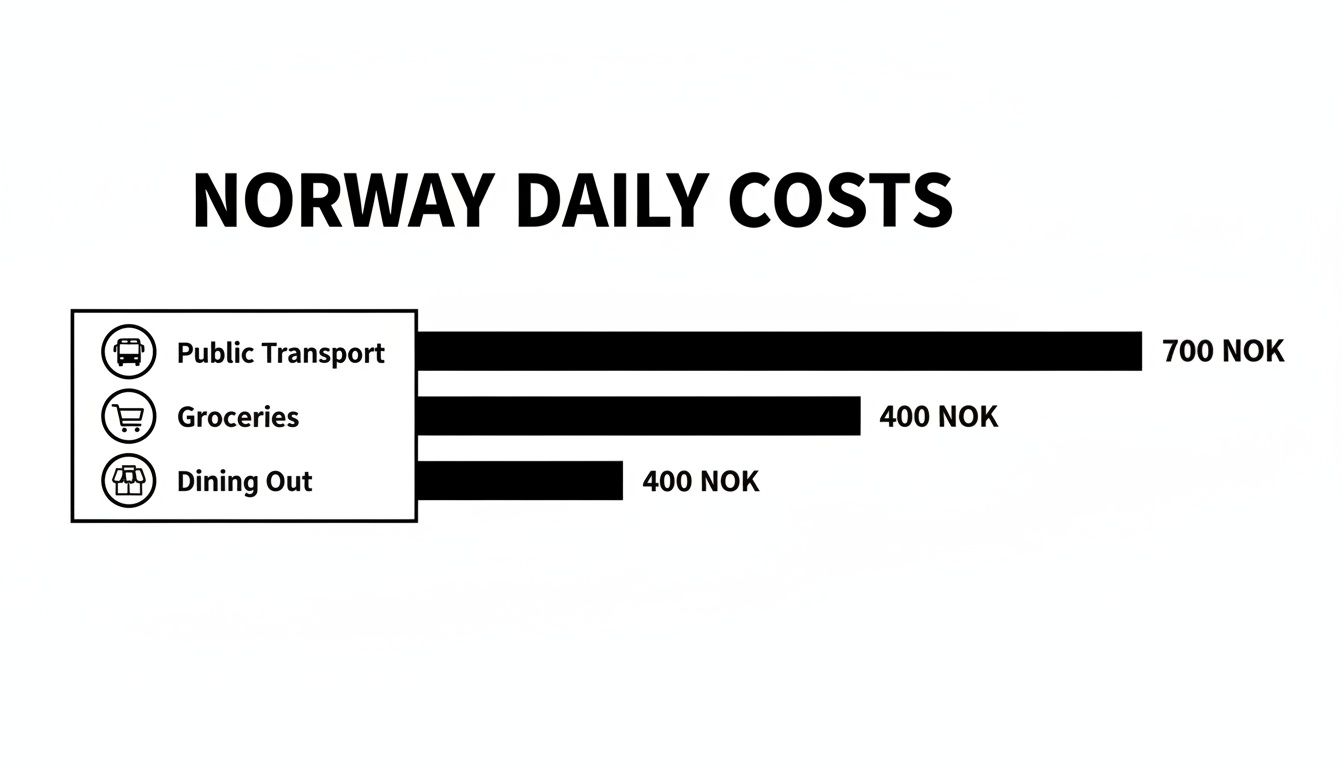

Analysing Daily Expenses to Understand Tenant Affordability

To truly understand a rental market, one must analyse the financial life of potential tenants. A property’s viability is not just its rental price, but how that rent fits within a household’s entire monthly budget. This holistic view of daily costs separates a strategic investor from a speculative one.

This deep dive into day-to-day spending provides a crucial read on tenant affordability. The Norway cost of living extends far beyond housing, and these other costs directly impact the amount a tenant can realistically pay in rent. This is a practical tool for setting the right price and minimising risk.

Transport Costs: A Key Differentiator

In Norway’s major cities, the choice between public transport and car ownership is a major financial decision for any household. Understanding this trade-off reveals the tangible value of a property’s location. A flat near a transport hub offers a direct monthly saving for a tenant.

Norway's public transport system is highly efficient. A monthly pass in a city like Oslo costs approximately 800 NOK. It is a fixed, predictable cost offering unlimited travel and a powerful alternative to the significant expense of car ownership.

Owning a car in Norway is a luxury, particularly in urban centres. The combination of high vehicle taxes, heavily taxed petrol, steep road tolls, and expensive city parking makes it one of the largest expenses a tenant can cut from their budget.

In contrast, the costs associated with a car are both significant and variable:

- Fuel: Petrol prices are consistently among the highest in Europe.

- Insurance and Taxes: These annual fixed costs are substantial.

- Tolls and Parking: Frequent road tolls and city parking fees, especially in Oslo, can amount to thousands of kroner per year.

For an investor, this means a property with excellent transport links can be marketed as offering a more affordable lifestyle, a direct appeal to tenants focused on managing their monthly outgoings.

Groceries and Dining: A Window into Discretionary Income

Food is another large component of the Norway cost of living, offering a clear window into a tenant's disposable income. High import duties and agricultural protections mean grocery bills are noticeably higher than in the UK or many other European countries. A single person should budget 2,500 to 4,000 NOK a month on groceries.

For most Norwegians, dining out is a discretionary expense, not a routine. An inexpensive meal can cost 200 NOK, while a mid-range, three-course dinner for two will exceed 1,000 NOK, driven primarily by high labour costs.

This dynamic is critical for property investors. If a large portion of a tenant’s income is consumed by essentials like food and transport, they have less flexibility to absorb a high rent. For a more detailed look at evaluating these factors, explore our guide on how to determine a property's investment potential.

Healthcare and Leisure Costs

While Norway’s public healthcare system is tax-funded, there are some out-of-pocket costs. Residents pay for services until they hit an annual cap (recently around 2,040 NOK), after which most services are free. This low, predictable cost is a major benefit for residents and expatriate tenants, freeing up income that would be allocated to private health insurance in other countries.

Leisure costs are heavily shaped by Norway's outdoor culture. Many popular activities, like hiking, are free, offering a cost-effective way to enjoy the country's natural landscape. Understanding these cultural norms helps build a complete picture of the target tenant’s lifestyle, allowing for property pricing that maximises appeal and secures long-term occupancy.

Building Sample Tenant Budgets for Strategic Insights

Raw data must be translated into actionable intelligence. To move beyond broad statistics on the Norway cost of living, we can construct sample monthly budgets for typical tenant profiles.

This is not an academic exercise. Breaking down typical expenses is an effective method for understanding tenant spending power, judging rental affordability, and identifying which property types are in highest demand. These budgets help align a property with the tenant’s financial reality.

This chart provides a snapshot of how daily and monthly expenses accumulate.

It is clear how core costs like transport and groceries quickly consume a monthly budget, explaining why tenants are sensitive to rental prices.

Single Professional in Oslo (Established Market)

Oslo attracts young professionals in sectors like tech and finance. This demographic prioritises convenience, seeking proximity to work, social life, and transport hubs. Smaller, centrally located apartments are therefore extremely desirable.

A typical monthly budget might appear as follows:

- Rent (1-bed flat, central): 14,000 NOK

- Utilities (heating, electricity, internet): 2,000 NOK

- Groceries: 4,000 NOK

- Public Transport (monthly pass): 800 NOK

- Health & Personal Care: 500 NOK

- Leisure & Dining Out: 2,500 NOK

With essential outgoings easily exceeding 23,800 NOK per month, it is clear that rental prices must be competitive. The best tenants will seek a property that leaves them with disposable income.

Couple in Bergen (Established Market)

Bergen’s economy is driven by shipping, aquaculture, and tourism. It is a popular city for professional couples who are often seeking more space than a single person but remain cost-conscious.

For an investor, this demographic is ideal. They represent a stable, dual-income tenant base often seeking two-bedroom flats that offer a balance between city access and extra living space. Properties in neighbourhoods just outside the immediate centre are often a perfect fit.

Their combined budget reflects shared expenses and different priorities:

- Rent (2-bed flat): 16,000 NOK

- Utilities: 2,500 NOK

- Groceries: 6,500 NOK

- Transport (one monthly pass, occasional car use): 1,500 NOK

- Health & Personal Care: 800 NOK

- Leisure & Dining Out: 3,500 NOK

A total monthly spend of around 30,800 NOK shows that even with two incomes, the high Norway cost of living keeps affordability central to their decision-making.

Family of Four in Stavanger (Emerging Market)

Stavanger is the centre of Norway’s energy industry and a hub for families, including a large international expatriate community. For this demographic, priorities shift to space, good schools, and family-friendly amenities, often over city-centre proximity. This makes it an interesting emerging market for family-focused investment.

A family’s budget is driven by childcare costs and the need for a larger home.

The following table provides a side-by-side comparison of regional differences.

Sample Monthly Budgets Across Norwegian Cities (2026)

| Expense Category | Single in Oslo (NOK) | Couple in Bergen (NOK) | Family in Stavanger (NOK) |

|---|---|---|---|

| Rent | 14,000 | 16,000 | 20,000 |

| Utilities | 2,000 | 2,500 | 3,500 |

| Groceries | 4,000 | 6,500 | 10,000 |

| Transport | 800 | 1,500 | 3,000 |

| Childcare/Activities | 0 | 0 | 4,000 |

| Other | 3,000 | 4,300 | 4,500 |

| Total Estimated Monthly Spend | 23,800 | 30,800 | 45,000 |

For a family in Stavanger, total expenses can realistically reach 45,000 NOK per month. This valuable data shows precisely why three-bedroom homes near parks and schools are in such high demand, even at a premium rent.

Ultimately, these budgets prove a fundamental rule of property investment: the most effective strategy is to align the property type with the specific needs and financial capacity of a well-defined tenant profile.

Forming Your Norwegian Property Investment Strategy

After analysing the cost of living data, the final step is to translate it into a coherent investment strategy. The figures indicate that this market rewards patient capital and a focus on long-term growth, rather than the high-yield, short-term cash flow found in more speculative locations.

Norway’s property market is shaped by its remarkable economic stability, high wages, and exceptional quality of life. These fundamentals create deep, consistent demand for quality housing. However, they are accompanied by high running costs and taxes. A successful strategy must balance the opportunity of steady rental income with these significant overheads.

Balancing Growth with Cash Flow

The Norwegian market is not for short-term speculators; it is for investors with a long-term horizon. The focus should be on properties in areas with solid fundamentals—growing populations, stable employment, excellent infrastructure—that are positioned for steady appreciation over a five to ten-year period.

While gross rental yields may appear modest compared to emerging markets, the low-risk environment provides security. Financial models must reflect this, prioritising asset value and predictable income over aggressive, high-risk returns. As part of this strategy, different rental models can be explored, including short-term leasing apartments, which present their own set of returns and challenges.

The core of a successful Norwegian investment is meticulous due diligence and precise cash flow modelling. This means going beyond simple yield calculations to account for seasonal cost spikes, particularly winter heating bills, and factoring in all taxes and management fees.

This level of detail is not optional. A small miscalculation in running costs can quickly erode net returns, turning a seemingly solid investment into a financial drain. For a wider perspective, our guide on investing in overseas property offers valuable context for building a diversified portfolio.

Strategic Takeaways for Investors

The decision to invest in Norway depends on an investor's risk appetite and long-term goals. The market demands significant capital and a long-term outlook but offers unparalleled stability in return.

Key strategic takeaways include:

- Prioritise Capital Growth: View a Norwegian property primarily as a long-term growth asset, not a high-yield cash-flow generator.

- Model Costs Meticulously: Create detailed financial forecasts that account for all operational costs, including seasonal utility swings, property taxes, and maintenance.

- Select Locations Strategically: Pinpoint areas with strong economic drivers and tenant demand, such as Oslo, Bergen, or Stavanger. Match the property type to the specific tenant profile.

By adopting this disciplined, data-driven approach, investors can make a confident, well-informed decision that ensures a Norwegian property investment aligns with their global portfolio goals.

Frequently Asked Questions About Investing in Norway

When evaluating a new market like Norway, several practical questions arise. This section addresses common queries from investors and expatriates to provide a clear, real-world picture of the costs and financial realities.

How Much Savings Should I Have Before Moving to Norway?

Arriving in Norway with a substantial financial cushion is essential. For a single person, a minimum of three to six months of living expenses is recommended. This equates to roughly 45,000 to 90,000 NOK (approximately £3,500 to £7,000).

This buffer is a practical fund to cover the large three-month rental deposit required by landlords, the first month's rent, and other initial setup costs associated with relocating to a new country.

Is It Cheaper to Live in Norway Than the UK?

As a general rule, daily life in Norway is more expensive than in the UK. Data consistently shows that consumer prices—particularly for groceries, transport, and dining—are noticeably higher.

For a property investor, the comparison is more nuanced. While operational costs may be higher, rental prices in a major city like Oslo can be on par with, or even slightly less than, those in London.

This creates an interesting dynamic for landlords. The entry point for rent can appear more accessible to tenants compared to other prime European capitals, even if the investor's own operational costs are higher.

What Are the Highest and Lowest Cost Cities in Norway?

Oslo consistently ranks as Norway's most expensive city. As the country's main economic engine, the capital commands the highest prices for both housing and daily living. Other major hubs like Bergen and Trondheim follow closely.

For investors seeking more affordable entry points, it is prudent to look beyond the top three. Smaller cities and towns, such as Drammen or Kristiansand, can offer a lower cost of living and more accessible property prices, providing solid alternative markets with less competition than the capital.

Can You Negotiate Rent Prices in Norway?

In high-demand areas, particularly central Oslo, the rental market is highly competitive, leaving almost no room for negotiation. Desirable properties are often leased within days, with landlords choosing from multiple qualified applicants.

However, in less crowded markets or for longer-term leases, some negotiation may be possible. A landlord is more likely to consider a modest discount for a tenant offering a multi-year commitment, a stable income, and excellent references. A significant price reduction remains very uncommon.

Ready to explore global property markets with confidence? At World Property Investor, we provide the in-depth guides and data-driven analysis you need to make informed decisions. Visit us at https://www.worldpropertyinvestor.com to find your next investment opportunity.