At its core, making money from property investment rests on two fundamental pillars: generating consistent rental income from tenants and securing long-term capital appreciation as the property's value grows. It is this dual-income approach that enables investors to build both reliable cash flow and substantial long-term wealth, transforming physical assets into powerful financial instruments.

Building Your Property Investment Foundation

Successful property investment is a business discipline, not a get-rich-quick scheme. The key is to build a strategy founded on the principles that drive returns. Before committing capital, it is essential to understand the two fundamental engines of profit.

The Twin Pillars of Profit: Income and Growth

The first pillar is rental income. This is the predictable cash flow that covers your mortgage, maintenance, and other operational costs. Any surplus at the end of the financial year represents your net profit. It provides the liquidity to sustain and expand a portfolio.

The second, and often more powerful, pillar is capital appreciation—the increase in a property's market value over time. This is where significant, long-term wealth is created. Established markets like the UK provide a clear example of this principle. According to ONS data, while the average UK house price was just £1,891 in 1952, it has demonstrated a resilient long-term upward trend, showcasing how patient investment can generate substantial returns.

Takeaway: A robust portfolio balances both cash flow from rental income and capital growth. Over-reliance on one creates vulnerability. A market downturn can erode capital values, whilst a rental void can eliminate income. A dual focus creates a more resilient investment strategy.

Understanding Leverage and Market Cycles

Prudent investors utilise leverage to enhance their returns. A buy-to-let mortgage allows an investor to control a high-value asset with a comparatively small deposit, typically around 25% in the UK market. When the property’s value increases, this leverage magnifies the return on the initial cash invested.

However, leverage is a double-edged sword; it amplifies risk just as it amplifies reward. A downturn in property values can lead to negative equity, where the loan exceeds the asset's worth. This makes a clear understanding of property market cycles—phases of growth, stagnation, and correction—essential. Experienced investors do not attempt to time the market perfectly. Instead, they focus on acquiring well-chosen properties in areas with strong economic fundamentals, such as job growth, infrastructure investment, and population trends.

A critical first step is mastering the financial analysis of a deal. Learning more about understanding property viability will equip you to make sound initial decisions. For those looking to scale, our guide on how to build a portfolio of properties provides practical next steps.

Mastering Rental Income for Consistent Cash Flow

For most investors, learning how to make money in property is synonymous with generating a reliable monthly income. This cash flow services debt and covers operational costs, but more importantly, it is the financial fuel that enables portfolio expansion over time.

You have two primary routes: the stability of traditional long-term tenancies or the higher-yield potential of short-term lets. Long-term rentals, typically governed by an Assured Shorthold Tenancy (AST) in England and Wales, form the bedrock of most buy-to-let portfolios. Tenants usually commit for 12 months or more, providing a predictable income stream and simplifying day-to-day management.

In contrast, short-term or holiday lets can generate a significantly higher gross income, particularly in tourist destinations or major business hubs. This comes with a trade-off: you are operating a hospitality business. This entails constant marketing, guest communication, frequent cleaning, and higher utility bills. The income is also more seasonal and far less predictable than a long-term tenancy.

Calculating Your True Rental Yield

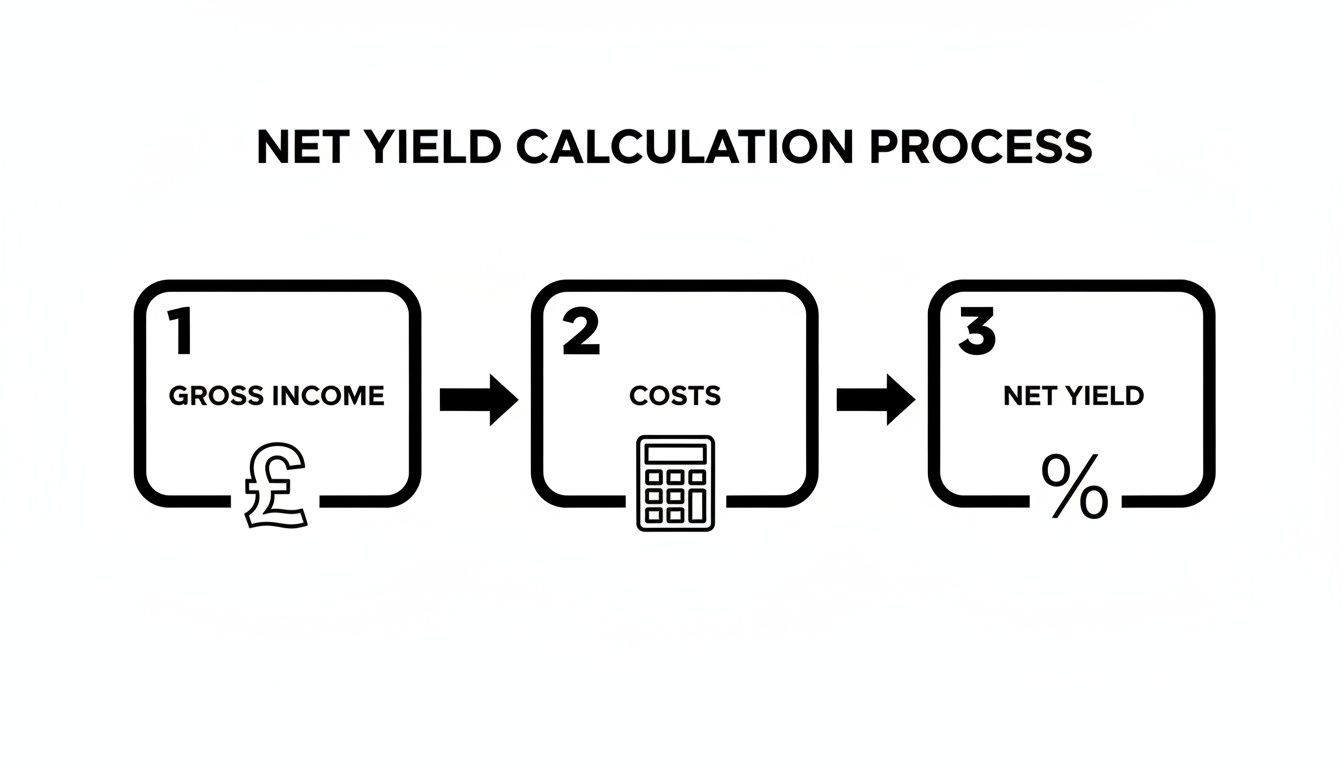

To accurately assess a property's performance, you must calculate the net rental yield. This metric reveals your true profitability by factoring in all operational costs. It is the single most important figure for any cash flow-focused investor.

The calculation is straightforward:

- Net Annual Rental Income: Your total annual rent minus all expenses (e.g., agent fees, insurance, maintenance, service charges, and an allowance for void periods).

- Net Yield Formula: (Net Annual Rental Income / Total Property Cost) x 100.

For example, a £250,000 property generating £15,000 per annum in rent (£1,250 pcm) appears to have a 6% gross yield. However, after deducting £4,000 for agent fees, repairs, insurance, and a one-month void period, your net income falls to £11,000. Your net yield is therefore 4.4%. This level of detail is explored in our guide on what rental yields really mean for your investment.

Identifying High-Yield Locations: UK vs. Global

Location is the primary determinant of rental yield. In established markets like the UK, investors have long found that rental yields in northern regions often outperform those in the more expensive south. Data consistently shows locations like the North West and Yorkshire offering stronger gross yields compared to the South East.

In emerging markets, rental yields can be substantially higher, often exceeding 8-10% in cities across Southeast Asia or Eastern Europe. However, these higher returns come with increased risks, including currency fluctuations, political instability, and less transparent legal frameworks. A balanced global portfolio might combine stable, lower-yield assets in established markets with a smaller allocation to higher-risk, higher-yield emerging markets.

Takeaway: A 5% net yield on a £200,000 property generates £10,000 of pre-tax income annually. Reinvesting this cash flow is how successful investors systematically scale their portfolios, using profits from one property to fund the deposit for the next.

Your Legal Duties as a Landlord

Maximising cash flow requires strict legal compliance to avoid fines that can eradicate profits. In the UK, every landlord has several non-negotiable statutory responsibilities, as outlined by sources like Gov.uk.

These duties are a fundamental part of operating a professional rental business and include:

- Gas Safety: Arranging an annual gas safety check by a Gas Safe registered engineer.

- Electrical Safety: Ensuring all electrical systems are inspected and tested by a qualified person at least every five years (EICR).

- Deposit Protection: Protecting a tenant’s deposit in a government-approved scheme within 30 days of receipt.

- Energy Performance: Providing tenants with an Energy Performance Certificate (EPC) with a minimum rating of 'E'.

For Houses in Multiple Occupation (HMOs), you must also adhere to specific HMO fire safety regulations. Failure to meet these legal requirements can lead to severe penalties, invalidate your insurance, and place your entire investment at risk.

Adding Value Through Renovation and Development

Beyond collecting rent, actively creating value through renovation is one of the most powerful ways to accelerate returns. This hands-on approach involves identifying a property's latent potential and executing a plan to unlock it—effectively manufacturing equity rather than waiting for market forces to deliver it.

Two core strategies dominate this space: the short-term 'flip' and the more advanced BRRRR method.

The most critical step is acquiring the right property. You are looking for a structurally sound but cosmetically dated asset—the type of property most buyers overlook. This could be a house with an old kitchen, an inefficient layout, or simply worn-out finishes. Your goal is to find the "worst house on the best street," where targeted, cost-effective improvements can deliver a significant uplift in value.

The 'Flipping' Strategy: Buy, Renovate, Sell

The classic 'flipping' model is simple in theory: you buy a property, renovate it quickly, and sell it for a profit. Success hinges on rigorous financial planning. Your profit is what remains after accounting for every associated cost.

A successful flip requires a meticulous budget covering:

- Acquisition Costs: Purchase price, Stamp Duty Land Tax (SDLT), solicitor fees, and survey costs.

- Renovation Costs: A detailed breakdown of materials and labour, plus a contingency of 15-20% for unforeseen issues.

- Holding Costs: Mortgage payments, insurance, and utility bills for the project's duration.

- Selling Costs: Estate agent fees, legal fees for the sale, and Capital Gains Tax on the profit.

Forgetting any one of these can turn a profitable project into a loss. Many novice investors are caught out by underestimating renovation timelines or failing to budget for the tax liability.

The BRRRR Method: A Strategy for Scale

A more advanced strategy is the Buy, Refurbish, Refinance, Rent (BRRRR) method. This approach is designed to recycle your initial investment capital, enabling you to build a portfolio much faster than traditional methods. Instead of selling for a one-off profit, you retain the asset as a cash-flowing rental.

The cycle is as follows:

- Buy: Purchase an undervalued property, often using cash or bridging finance for speed.

- Refurbish: Renovate the property to a high standard, significantly increasing its market value.

- Refinance: Obtain a new valuation and take out a buy-to-let mortgage based on the new, higher value. This allows you to withdraw your initial deposit and refurbishment funds.

- Rent: Let the property to a tenant, with the rental income covering the new mortgage and generating a monthly profit.

- Repeat: Use the extracted capital to fund the next BRRRR project.

Takeaway: The power of BRRRR is its ability to recycle the same pot of money. You are effectively using your deposit from one deal to fund the next, all while building a portfolio of income-generating assets.

A Real-World BRRRR Example

Let's apply numbers to this strategy. Imagine you buy a dated two-bedroom terrace house in a strong rental area for £120,000.

- Purchase & Refurb: You use £50,000 of your own cash. This covers a £30,000 deposit and £20,000 for a full refurbishment.

- Post-Refurbishment Value: After the work, a chartered surveyor re-values the property at £190,000.

- Refinance: You apply for a buy-to-let mortgage at 75% Loan-to-Value (LTV) on the new valuation. The lender provides £142,500 (£190,000 x 0.75).

- Recycle Capital: This £142,500 pays off initial borrowing. Having invested £50,000 cash, after refinancing you can withdraw most or all of it to use for your next deposit.

The result is that you now own a £190,000 asset generating rental income, and you have your initial capital back, ready to repeat the process. This is precisely how sophisticated investors scale their portfolios with speed. The principles of adding value are universal, and unique opportunities exist globally. For the adventurous, the famous houses in Sicily for one euro represent an extreme but fascinating case of value-add potential.

This visual illustrates the flow for calculating net yield, which is crucial for both BRRRR and standard rental strategies.

The key insight is that gross income is merely a starting point. It is the net yield, after all costs are deducted, that truly defines an investment's profitability.

Alternative Ways to Invest in Property

Not everyone has the time, capital, or inclination to become a hands-on landlord. Fortunately, direct ownership is not the only way to generate wealth from real estate.

For investors seeking a more passive route, lower entry costs, or portfolio diversification, a range of other strategies provide exposure to the property market. These indirect approaches open property investing to a much wider audience, each with its own risk and reward profile.

Gaining Control with Property Lease Options

A property lease option is a sophisticated strategy that allows an investor to secure control over a property today, with the right—but not the obligation—to purchase it later at a pre-agreed price. The investor pays a small upfront 'option fee' for this right, typically 1-5% of the agreed purchase price.

This structure is highly effective for investors with limited capital. You do not need to secure a mortgage or provide a large deposit to get started, yet you can benefit from any capital growth during the option period, which typically runs for three to five years. The investor often manages the property during this time, renting it out and collecting the income.

Imagine a property with a current market value of £200,000. You could negotiate a lease option with a £5,000 fee (2.5%) and a locked-in purchase price of £210,000, exercisable within three years. If the market value climbs to £250,000, you can exercise your option to buy for £210,000, creating £40,000 of instant equity.

Liquid Property Investing with REITs

For those wanting property market exposure with the liquidity of shares, Real Estate Investment Trusts (REITs) are an excellent solution. A REIT is a company that owns, operates, and finances a large portfolio of income-producing real estate, such as shopping centres, office blocks, warehouses, or large-scale residential complexes.

When you buy shares in a REIT, you are acquiring a small fraction of this vast, diversified portfolio. This immediately spreads your risk across different property types and geographical locations. In the UK and many other jurisdictions, REITs are legally required to distribute at least 90% of their tax-exempt rental profits to shareholders as dividends, providing a regular income stream.

Takeaway: REITs offer a unique combination of liquidity and diversification. Unlike physical property, which can take months to sell, REIT shares can be bought and sold instantly on a stock exchange.

The trade-off is a lack of control; you cannot influence which properties are bought or how they are managed. REIT share prices can also be influenced by broader stock market sentiment, not just the performance of the underlying property assets.

Pooling Capital with Property Crowdfunding

Property crowdfunding bridges the gap between direct ownership and a passive REIT investment. It allows a group of investors to pool their capital online to fund a specific property deal, be it a buy-to-let investment or a development project. The entry point can be as low as a few hundred pounds.

This model offers more choice than a REIT, as you select the exact projects you wish to back based on strategy, location, and forecast returns. You typically become a shareholder in a Special Purpose Vehicle (SPV)—a limited company created solely to own that asset. The crowdfunding platform handles all management.

The upsides are a low cost of entry, easy diversification, and a hands-off experience. However, it is vital to scrutinise the fee structure, as initial and ongoing management charges will impact your net returns. Your capital is also illiquid, locked into the project for a fixed term (usually 2-5 years) with no easy exit. For those interested in a hands-on but high-yield strategy, consider learning how to start an Airbnb business as an alternative.

Navigating UK Property Taxes And Finance

A firm grasp of finance and tax is non-negotiable for making money in property. This framework protects profits and ensures your strategy is sustainable.

For most, the journey begins with finance. A buy-to-let mortgage is the standard tool for leveraging capital, but the choice between repayment and interest-only has a significant impact on cash flow.

Choosing Your Mortgage Strategy

With a repayment mortgage, each monthly payment covers both the interest and a portion of the original loan. At the end of the term, you own the property outright. This is a lower-risk, forced-savings approach but results in higher monthly payments and therefore lower cash flow.

An interest-only mortgage requires you to cover only the interest each month, leaving the capital loan untouched. This leads to far lower monthly outgoings and maximises rental profit, which is why it is preferred by many professional investors. The strategy relies on capital appreciation to cover the original loan when the property is eventually sold or refinanced.

Lenders use two key metrics to assess affordability: the rental income (which must typically cover the mortgage payment by 125-145%) and the Loan-to-Value (LTV) ratio. A 75% LTV is standard, requiring a 25% deposit.

Takeaway: A higher LTV allows capital to be spread across more properties but increases risk. A lower LTV creates a larger safety buffer against house price falls and interest rate rises but ties up more cash in a single asset.

Understanding Key Property Taxes

Once you generate income or realise a capital gain, tax becomes the next critical factor. In the UK, every property investor must account for a specific set of taxes.

-

Stamp Duty Land Tax (SDLT): This tax is paid upon acquisition. Investors purchasing an additional property pay standard SDLT rates plus a 3% surcharge. It is a major upfront cost that must be factored into every deal analysis.

-

Income Tax: Profit from rent is subject to Income Tax. Your profit is your total rental income minus allowable running costs. The rate you pay depends on your personal income tax band.

-

Capital Gains Tax (CGT): When you sell an investment property that has increased in value, the profit ('gain') is subject to CGT. Higher and additional-rate taxpayers currently pay 24% on gains from residential property in the UK. For a deeper dive, explore our guide on what Capital Gains Tax on property involves.

Individual Ownership vs Limited Company

A critical decision for any UK investor is whether to own property personally or through a limited company (SPV). This choice has profound tax implications, primarily due to a tax rule known as Section 24.

For individual landlords, Section 24 removed the ability to deduct mortgage interest as a business expense. Instead, they receive a tax credit equivalent to 20% of their mortgage interest payments. This means higher-rate (40%) and additional-rate (45%) taxpayers no longer receive full tax relief on their largest cost, which can significantly reduce net profits.

A limited company, however, can still deduct 100% of its mortgage interest from its rental income before calculating its Corporation Tax bill. This makes the company structure far more tax-efficient for higher-rate taxpayers. It is not a universal solution; this structure involves more administration, accountancy fees, and often slightly higher mortgage rates.

Takeaway: There is no single correct answer. The decision requires careful financial modelling with a qualified property tax advisor to determine which structure delivers the best net return for your specific circumstances and long-term goals.

Answering Key Questions for Property Investors

Every investor faces the same core questions. Obtaining clear, practical answers is what separates a well-planned investment from a costly error. Here, we address some of the most common queries.

How Much Capital Do I Need to Start in UK Property?

The required starting capital varies significantly based on location and strategy. For a traditional buy-to-let mortgage, lenders typically require a deposit of at least 25% of the property’s value. In more affordable regions of the UK, this could mean a deposit of £25,000 to £40,000 for an entry-level rental property.

The deposit is only the first cost. You must also budget for acquisition costs, including Stamp Duty Land Tax (with the 3% second-home surcharge), solicitor fees, and survey costs. Together, these can add another 5-7% of the purchase price to your upfront cash requirement. Alternative routes like REITs or property crowdfunding allow market entry with as little as a few hundred pounds, without the need for mortgages or tenants.

Is It Better to Buy in a Limited Company or My Personal Name?

This decision depends entirely on your personal financial circumstances, specifically your income tax bracket. For higher-rate taxpayers in the UK, using a limited company is often far more tax-efficient.

The reason is Section 24: a limited company can deduct 100% of its mortgage interest before paying Corporation Tax. In contrast, individual landlords only receive a 20% tax credit on mortgage interest costs. This severely impacts profitability for anyone paying tax at 40% or 45%.

Takeaway: A limited company is not a panacea. It involves more administration and potentially higher mortgage rates. Extracting profits is also more complex. Bespoke advice from a property-specialist accountant is essential to model the financial outcomes of each structure.

Long-Term Rentals or Holiday Lets: Which Is More Profitable?

Both models can be highly profitable but they are fundamentally different business operations suited to different investor profiles and risk appetites.

Short-term lets can generate a higher gross income, particularly in prime tourist locations. However, this comes at the cost of being far more management-intensive, with higher operational costs (cleaning, utilities) and increasing local regulation.

Long-term rentals offer a more predictable and stable income stream with significantly less hands-on management. While gross yields are typically lower than a holiday let, the net profit is often more consistent and passive. For most investors focused on building scalable, long-term wealth, the traditional buy-to-let model remains the most stable foundation.

What Are the Biggest Risks I Need to Plan For?

Every investor must have a contingency plan. The primary risks to prepare for include:

- Market Downturns: A fall in property prices can erode equity and lead to negative equity.

- Interest Rate Hikes: A sharp rise in mortgage rates can compress profit margins or turn a profitable investment into a loss-maker.

- Void Periods: An empty property generates no income but continues to incur costs.

- Unexpected Costs: Major repairs, such as a boiler failure or roof leak, can severely impact cash flow.

- Problem Tenants: Dealing with rent arrears or property damage is both costly and stressful.

These risks cannot be eliminated, but they can be managed. This involves thorough due diligence before purchasing, maintaining a cash reserve for emergencies, considering fixed-rate mortgages to control costs, and implementing robust tenant screening processes. Diversifying a portfolio across different locations or property types is another proven risk-mitigation strategy.

At World Property Investor, we provide the data-driven guides and market analysis you need to navigate these questions and invest with confidence. Explore our expert insights to find the best places to buy property around the world. Visit World Property Investor to start your research today.