For global investors seeking opportunities beyond the saturated, high-cost Western markets, Vietnam has become a focal point. This is not a speculative punt on an emerging economy; finding a property to buy in Vietnam presents a chance to engage with one of Southeast Asia's most dynamic real estate narratives, underpinned by robust economic fundamentals.

Why Vietnam Is on the Investor Radar for 2026

For those weary of the low yields and stagnant growth characterising many developed nations, Vietnam represents a fundamental alternative. The potential here is not speculative; it is built on a foundation of consistent GDP growth, significant foreign investment, and a young, aspirational populace.

The economic data is compelling. According to sources like the World Bank, Vietnam's GDP growth has consistently outpaced its regional peers for years. This has been amplified by a substantial influx of Foreign Direct Investment (FDI), as global corporations such as Samsung and Apple relocate their supply chains and manufacturing operations to the country. This activity generates employment, raises incomes, and attracts a steady stream of expatriates—all requiring accommodation.

The Power of a Rising Middle Class

Perhaps the most crucial driver is the rapid expansion of Vietnam's domestic middle class. As household incomes rise, so does the aspiration for homeownership and an improved quality of life. This creates powerful, organic demand for property that provides a stable floor for the market, particularly in major urban centres.

This is not merely theoretical. In 2024, the residential sector recorded over 47,000 property transactions with a 72% absorption rate for new projects, as reported by local real estate bodies. This was supported by a 19% increase in foreign investment into real estate, demonstrating confidence from both local and international buyers. Deeper analysis of price trends is available from sources like the Global Property Guide.

To provide a clearer market overview, the following table summarises key metrics for the main urban centres.

Vietnam Property Market Snapshot 2026

This table summarises key metrics for international investors evaluating property opportunities in Vietnam's three largest urban centres.

| Metric | Ho Chi Minh City | Hanoi | Da Nang |

|---|---|---|---|

| Avg. Rental Yield | 5% – 7% | 4.5% – 6.5% | 5% – 8% |

| Price Growth (2025-26) | Strong (5-10%) | Steady (4-7%) | High (8-12%) |

| Main Tenant Pool | Expats, Professionals | Gov't, Professionals | Tourism, Expats |

| Affordability | Moderate-High | Moderate | High |

While Ho Chi Minh City and Hanoi remain the primary economic hubs, Da Nang is rapidly emerging as a high-growth alternative, combining a strong tourism sector with a coastal lifestyle.

Beyond Hype: Tangible Market Fundamentals

An exciting emerging market narrative must be backed by solid fundamentals. Vietnam delivers on several key fronts:

- Urbanisation and Infrastructure: The government is channelling significant capital into major infrastructure projects, such as the new metro lines in Ho Chi Minh City and Hanoi. This is opening up new districts and unlocking value in previously overlooked areas.

- Favourable Demographics: With a median age of approximately 33, Vietnam possesses a young, energetic population. This ensures a long-term pipeline of first-time buyers and renters for decades to come.

- Relative Affordability: Even in prime city-centre locations, high-quality, modern apartments can be acquired for a fraction of the cost in London, Sydney, or even nearby Bangkok.

Key Takeaway: For a UK investor accustomed to gross rental yields of 3-4% in major cities, the 6-8% yields achievable in parts of Ho Chi Minh City or Da Nang represent a significant opportunity. This is not just a capital growth story; it is about acquiring an asset that generates strong, consistent cash flow.

Vietnam’s property market is maturing, transitioning from a frontier play to a more structured investment destination. To see how it compares globally, you can read our guide on the best countries for property investment.

Understanding Vietnam's Foreign Ownership Laws

Grasping the legal framework is often the primary hurdle for international investors considering property in Vietnam. While the regulations are more restrictive than in the UK or US, they are clear, structured, and manageable with proper guidance. Understanding them is the first step toward a secure purchase.

The foundation for foreign ownership is Vietnam's Law on Residential Housing. This legislation permits foreigners with a valid visa to legally purchase certain property types, a pivotal step in welcoming direct real estate investment.

A fundamental distinction exists: all land in Vietnam is collectively owned by the people and managed by the state. Consequently, one cannot own land freehold. Instead, what is acquired is a long-term leasehold on the property built upon that land.

The 50-Year Leasehold Explained

For foreign individuals, the ownership term is a 50-year leasehold. This is a common point of confusion for investors accustomed to freehold titles, but it is a straightforward concept. It should not be viewed as a temporary rental, but as owning a long-term right to use, sell, lease, or bequeath the apartment for that 50-year period.

Upon expiry of the 50-year term, an extension can be requested. Given Vietnam's consistently pro-investment government stance, the market widely anticipates that a formal, transparent renewal process will be well-established by the time the first leases come up for renewal.

This leasehold structure is a core concept. For a detailed comparison, our guide on the differences between freehold vs leasehold property provides further context.

The 30% Foreign Ownership Cap

Another critical regulation is the foreign ownership quota. In any single condominium building, foreigners as a group can own a maximum of 30% of the total units. For landed property projects, such as villas and townhouses, this cap is typically set at 10% of the homes within a single project.

This quota has two major implications for your investment approach:

- Scarcity and Demand: In popular, high-end projects, this 30% foreign quota can sell out rapidly. This scarcity often creates a premium on the resale market for these "foreign-eligible" units, as they are the only ones other foreigners can legally acquire.

- Due Diligence is Key: It is absolutely essential to verify that the specific unit you intend to buy falls within this foreign quota. Any reputable developer or lawyer can confirm this by checking the project’s master list with the local Department of Construction.

Legitimate Structures for Seasoned Investors

While direct ownership is the most common route, some experienced investors utilise alternative structures. These add complexity and cost, and expert legal advice is vital.

Two common methods include:

- Forming a Vietnamese Company: By establishing a 100% foreign-owned company in Vietnam, that legal entity can then acquire property. The ownership term is tied to the company's operational licence. This path is generally reserved for larger-scale or commercial investments.

- Using a Long-Term Lease Agreement: This involves signing a long-term lease (often for 50 years) directly with a Vietnamese owner or a developer. You pay the full value upfront and receive the right to use, sublet, and control the property. While you do not hold the official title (the "Pink Book"), a well-drafted legal contract can provide robust security.

For most first-time investors targeting a residential apartment, direct ownership via the 50-year leasehold is the most secure and straightforward path.

Where to Invest: Comparing Vietnam's Top Property Markets

Deciding where to buy property in Vietnam is not about finding a single “best” city, but about matching a location to specific investment objectives. The country’s three primary markets—Ho Chi Minh City, Hanoi, and Da Nang—each offer a distinct risk-reward profile.

A property promising high capital growth may deliver lower rental yields, while a steady income-producing asset may see more modest appreciation. Let's break down the on-the-ground dynamics of each city, comparing established districts with emerging hubs.

Ho Chi Minh City: The Economic Powerhouse

Ho Chi Minh City (HCMC) is Vietnam’s undisputed commercial engine, attracting multinational companies and a deep tenant pool. This makes it a prime target for investors seeking both rental income and capital gains.

Established vs. Emerging Districts

District 1 & Binh Thanh District (Established): These are blue-chip neighbourhoods. District 1 is the central business district with the highest prices and rents. Binh Thanh, home to landmarks like Vinhomes Central Park, offers premium apartments with solid rental demand from high-earning expatriates. An investment here is in stability and proven performance, with gross yields typically around 5-6%.

Thu Duc City (Emerging): This sprawling eastern area, a "city-within-a-city," is the focus of massive infrastructure investment, notably the new Metro Line 1. This connectivity is unlocking enormous potential, making it an epicentre for capital growth. While initial yields may be slightly lower, the potential for price appreciation is significantly greater than in the saturated city centre.

Hanoi: The Capital of Stability

As the nation's political heart, Hanoi’s property market is generally considered more stable and less speculative than HCMC’s. Demand is anchored by government officials, embassy staff, and a growing tech sector.

Hoan Kiem & Ba Dinh (Established): These central districts represent the soul of old Hanoi. Property is scarce and holds its value well. The trade-off is more modest rental yields, typically around 4-5%.

Tay Ho (West Lake) (Prime Income): This is the preferred enclave for expatriates and affluent locals. It delivers the best rental yields in the capital, often reaching 6.5% or more. For income-focused investors in Hanoi, West Lake is the premier choice.

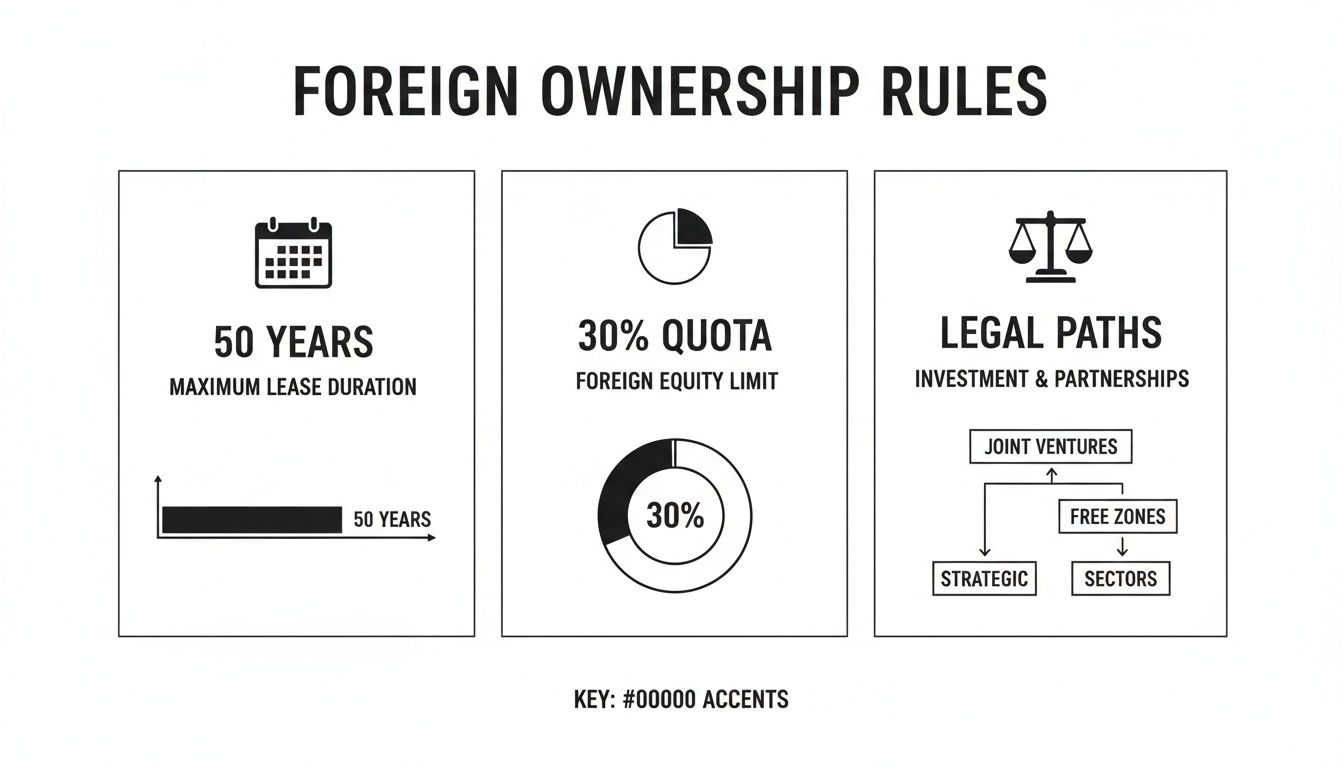

This infographic simplifies the foreign ownership rules discussed earlier.

It outlines the 50-year leasehold, the 30% foreign ownership cap, and available legal structures—all key rules defining what a foreign investor can buy.

Da Nang: The High-Growth Coastal Market

Located on Vietnam's central coast, Da Nang has transformed from a quiet beach town into a major tourism and tech hub. Its modern infrastructure and business-friendly environment have made it a magnet for investment. This market is ideal for those seeking high growth potential and strong, tourism-driven rental yields.

Key Takeaway: For investors seeking a hybrid asset—part holiday home, part income-producer—Da Nang is unmatched. The potential for high occupancy from tourists and digital nomads can generate gross rental yields of 7-8% or higher in peak season.

According to a recent report from Data Insights Market, Vietnam's residential sector is projected to grow at a CAGR of 12.55% between 2025 and 2033. In Q1 2025, Hanoi's apartment prices surged 29.6% year-on-year, demonstrating the powerful momentum in key urban centres.

Investment Profile of Key Vietnamese Cities

This table provides a comparative overview of the investment characteristics of Vietnam's prime real estate markets.

| City | Investor Profile | Average Price (per sqm) | Typical Gross Rental Yield |

|---|---|---|---|

| Ho Chi Minh City | Growth & Income Balanced | USD 3,000 – 6,000+ | 5-6% |

| Hanoi | Stability & Income Focused | USD 2,500 – 5,000 | 4-6.5% |

| Da Nang | High Growth & Tourism Yield | USD 2,000 – 4,000 | 6-8%+ |

HCMC offers a balanced portfolio, Hanoi provides stability, and Da Nang presents a higher-risk, higher-reward scenario. To broaden your perspective, consider our analysis of other emerging property markets.

Calculating the True Cost of Buying Property

The advertised price is never the final cost. To accurately assess an investment in Vietnam, one must account for all costs over the lifetime of the asset. Budgeting for these expenses from the outset is what distinguishes experienced investors. By breaking down costs into initial purchase, ongoing ownership, and eventual sale, you can build a realistic financial forecast.

Upfront Costs: Purchase Taxes and Fees

When purchasing a property, several mandatory taxes and fees are incurred. These must be factored into your initial capital outlay.

For new-build properties, the primary cost is Value Added Tax (VAT), set at 10% of the apartment price (exclusive of the sinking fund). This applies only to the first sale from a developer. Resale properties are not subject to VAT.

Other costs to budget for include:

- Registration Tax: A fee of 0.5% of the property's value, paid to the government to officially register your ownership and initiate the process for obtaining the Ownership Certificate (the "Pink Book").

- Administrative Fees: Minor costs for document processing and notarisation.

Ongoing Ownership Costs

Once you take possession, your financial focus shifts to recurring expenses that impact your net rental yield.

Example: A modern condominium in Ho Chi Minh City may have a monthly management fee of around £0.60 to £1.20 per square metre. For a 75 sqm two-bedroom apartment, this translates to approximately £45 to £90 per month.

Your main ongoing costs will include:

- Management Fee: A monthly charge covering building operations such as security, cleaning of common areas, and lift maintenance. The rate depends on the project's quality and facilities.

- Sinking Fund: A one-off payment, typically collected at handover. It contributes to a long-term fund for major capital repairs. It is calculated as 2% of the pre-VAT apartment price.

- Land Tax: For foreign apartment owners, the non-agricultural land use tax is nominal, often amounting to just a few pounds per year.

Taxes on Exit When You Sell

A sound investment plan includes an exit strategy. When selling your property in Vietnam, you must account for Personal Income Tax.

The tax is calculated as a flat 2% of the total transaction price, regardless of profit or loss. While this simplifies calculations, you must factor this cost into your target sale price to protect your net return. On a sale of £200,000, for instance, the tax due would be £4,000.

Understanding these figures is fundamental. For a detailed look at the methodologies, learn more about how to calculate return on investment for a property in our dedicated guide.

A Step-by-Step Guide to a Successful Purchase

Buying property in Vietnam follows a well-defined process. Understanding the key stages enables a confident purchase. The timing is opportune; FDI in Vietnam’s real estate surged by 46% year-on-year in Q1 2025, signalling strong international confidence.

Stage 1: Crucial Due Diligence

Thorough due diligence before any financial commitment is non-negotiable. For foreign buyers, this means focusing on key legal verifications.

Your lawyer must confirm:

- Project Eligibility: Has the development been officially approved for sale to foreigners?

- Foreign Quota: Is there space within the 30% foreign ownership quota for the building? A reputable developer will provide a letter confirming this.

Additionally, investigate the developer’s track record. Review their past projects and ensure they have a solid reputation for delivering on their commitments.

Stage 2: The Reservation Agreement and Deposit

Once due diligence is complete, the first financial step is signing a Reservation Agreement. This secures the unit while the main contract is prepared.

You will pay a deposit, typically between £4,000 and £8,000. The terms (refundable or non-refundable) must be clearly understood before signing.

Stage 3: Signing the Sale and Purchase Agreement (SPA)

The Sale and Purchase Agreement (SPA) is the core legal contract. It details all terms of the sale, including the payment schedule, handover date, and property specifications.

Critical Note: Ensure all legal documents are professionally translated. Never sign a contract you do not fully understand. Your lawyer should review both the English and Vietnamese versions of the SPA. Reliable English to Vietnamese document translation services are essential for this.

For off-plan properties, payment is typically staged. It is common to pay 25-30% of the value upon signing the SPA. The remainder is paid in instalments tied to construction milestones, with the final 5% often withheld until you receive the ownership certificate.

Stage 4: Handover and Securing the Pink Book

At handover, you will conduct a final inspection to identify any defects. Upon satisfaction and payment of the penultimate instalment (usually bringing the total to 95%), you take possession.

The final step is obtaining your Ownership Certificate, known locally as the "Pink Book". The developer manages this application process. It can take 6 to 12 months post-handover, but its receipt officially registers your ownership with the Vietnamese government.

This structured approach is common in many international markets. For comparison, see our general guide on how to buy property abroad.

Your Vietnam Property Investment Questions Answered

Practical questions often remain when exploring a new market. This section addresses the most common queries from investors regarding ownership, finance, and security in Vietnam.

Can I Get a Mortgage in Vietnam as a Foreigner?

The short answer is: it is exceptionally difficult. Non-resident foreigners will find securing a mortgage from a Vietnamese bank nearly impossible, as local lenders require official residency status and a verifiable local income.

Some international banks like HSBC may offer solutions to existing premier clients, but this is typically a loan secured against assets in your home country, not the Vietnamese property itself.

Key Takeaway: For most foreign buyers, the most practical approach is to use cash or arrange financing in your home country. It is essential to have funding secured before signing any binding agreements in Vietnam.

What Happens After the 50-Year Leasehold Expires?

This is a critical long-term consideration. Under Vietnam's current Law on Residential Housing, you have the right to apply for an extension upon the expiry of your 50-year leasehold. The outcome will depend on the laws in place at that time.

However, given Vietnam's consistent pro-investment stance, the market widely anticipates that a formal and fair renewal process will be established long before the first leases expire.

Furthermore, you have several options during the lease term:

- Sell at Any Time: You can sell your property at any point during the 50-year term.

- Sell to a Local Buyer: If you sell to a Vietnamese citizen, the ownership converts to freehold for them, potentially increasing the property's attractiveness on the resale market.

- Sell to a Foreign Buyer: If you sell to another foreigner, they acquire the remaining years on your original 50-year lease.

What Are the Biggest Risks I Should Know?

Every investment carries risk. In an emerging market like Vietnam, it is vital to be aware of the challenges.

The main risks to consider are:

- Legal and Administrative Complexity: Vietnam’s property laws are still maturing. Navigating the bureaucracy without experienced local professionals can be challenging.

- Off-Plan Construction Risk: Buying a new-build property carries the risk of construction delays or, in rare cases, project incompletion. Thorough due diligence on the developer is non-negotiable.

- Market Liquidity and Policy Changes: As an emerging economy, Vietnam may be more susceptible to sudden economic shifts or government policy changes that could impact property values or liquidity.

- Verification and Scams: It is crucial to work with independent lawyers and trusted agents to verify all claims and ensure the property is legally eligible for foreign purchase to avoid title issues or fraud.

Is It Better to Buy a New-Build or a Resale Property?

Both new-build (off-plan) and resale properties have distinct advantages and disadvantages. The right choice depends on your risk appetite and tolerance for complexity.

New-Build Properties

- Pros: Often the most straightforward route. Major developers ensure projects are pre-approved for foreign ownership and manage the 30% foreign quota transparently. You also benefit from modern facilities and flexible payment schedules.

- Cons: The main risk is construction-related. You are buying a promise, and delays can occur.

Resale Properties

- Pros: The property is tangible and can be inspected. There are no construction delays.

- Cons: The primary challenge is verifying if the 30% foreign ownership quota for the building has been filled. This administrative check requires diligent work from your legal team.

For most first-time investors in Vietnam, buying a new-build apartment from a top-tier, reputable developer is generally the simpler and more secure option.

At World Property Investor, we are dedicated to providing the clarity and data you need to make informed investment decisions across the globe. Our in-depth guides and market analyses are designed to help you navigate international real estate with confidence.

Explore more global property opportunities at https://www.worldpropertyinvestor.com.