For many global investors, property has traditionally been a domestic affair. However, with shifting economic landscapes, rising taxes, and complex regulations in markets like the UK, a growing number are looking further afield. Dubai has rapidly emerged as a primary destination for those seeking to diversify their portfolios and secure stronger net returns.

The appeal lies in a simple, powerful difference: in Dubai, your investment is structured to perform with minimal fiscal drag.

Why Investors Are Turning to Dubai in 2026

Let's be practical. Being a landlord in many Western markets, such as the UK, has become progressively more challenging. Investors navigate a complex environment of income tax on rental profits, significant capital gains tax upon sale, and intricate transfer taxes like the UK's Stamp Duty Land Tax (SDLT).

Dubai offers a fundamentally different framework. The financial incentives are not minor perks; they are the cornerstone of the market's structure. This is the core reason why a significant volume of international capital is now flowing into the UAE property sector.

The Financial Case for Dubai: A Data-Driven View

The mathematics is refreshingly straightforward. Dubai's property market is built on tax efficiency and pro-investor policies, creating a clear financial advantage over jurisdictions where returns are consistently eroded by taxation.

For an international investor, the key distinctions are material:

- Zero Income Tax on Rent: Rental income earned in the UAE is not subject to local income tax. The gross rent is the net rent.

- Zero Capital Gains Tax: Profit realised from the sale of a property is entirely free from capital gains tax within the UAE.

- No Annual Property Taxes: Unlike the UK's Council Tax or similar annual levies in other countries, there are no annual property taxes in Dubai.

Key Takeaway: A tax-free environment has a direct and substantial impact on net returns. A significantly higher percentage of the gross rental income remains with the investor, accelerating capital recovery and enabling stronger, more predictable cash flow from the outset.

Comparing Yields and Transaction Costs

This tax efficiency becomes even more compelling when analysing rental performance. While average UK buy-to-let yields hover between 5-7% in many regions according to recent market analysis, Dubai's typical 6-9% gross rental yields are already superior. When factoring in the absence of tax, the real-world difference in retained income is profound.

To provide a clear picture, here is a side-by-side comparison of the key metrics.

Dubai vs. UK Property Investment: A Snapshot

| Metric | Dubai | United Kingdom (Average) |

|---|---|---|

| Gross Rental Yield | 6-9% | 5-7% |

| Income Tax on Rent | 0% | 20-45% |

| Capital Gains Tax | 0% | 18-24% |

| Property Transfer Tax | 4% DLD Fee (one-off) | Stamp Duty (tiered, up to 15%) |

| Annual Property Tax | None | Council Tax (varies) |

As the data shows, the financial hurdles to both entry and operation are substantially lower in Dubai. Whereas UK investors face a tiered and often punitive Stamp Duty, Dubai levies a single, one-off 4% Dubai Land Department (DLD) fee on transfer of ownership. This makes market entry far more cost-effective.

Combined with the strong capital appreciation observed since 2021 and the city's commitment to growth through infrastructure investment and policies like the Golden Visa, it is evident why Dubai is a leading global property hub. You can learn more about how the investor visa programme works for property owners in our detailed guide. This powerful combination of high yields, minimal tax, and a clear path to long-term residency presents a compelling case for international investors.

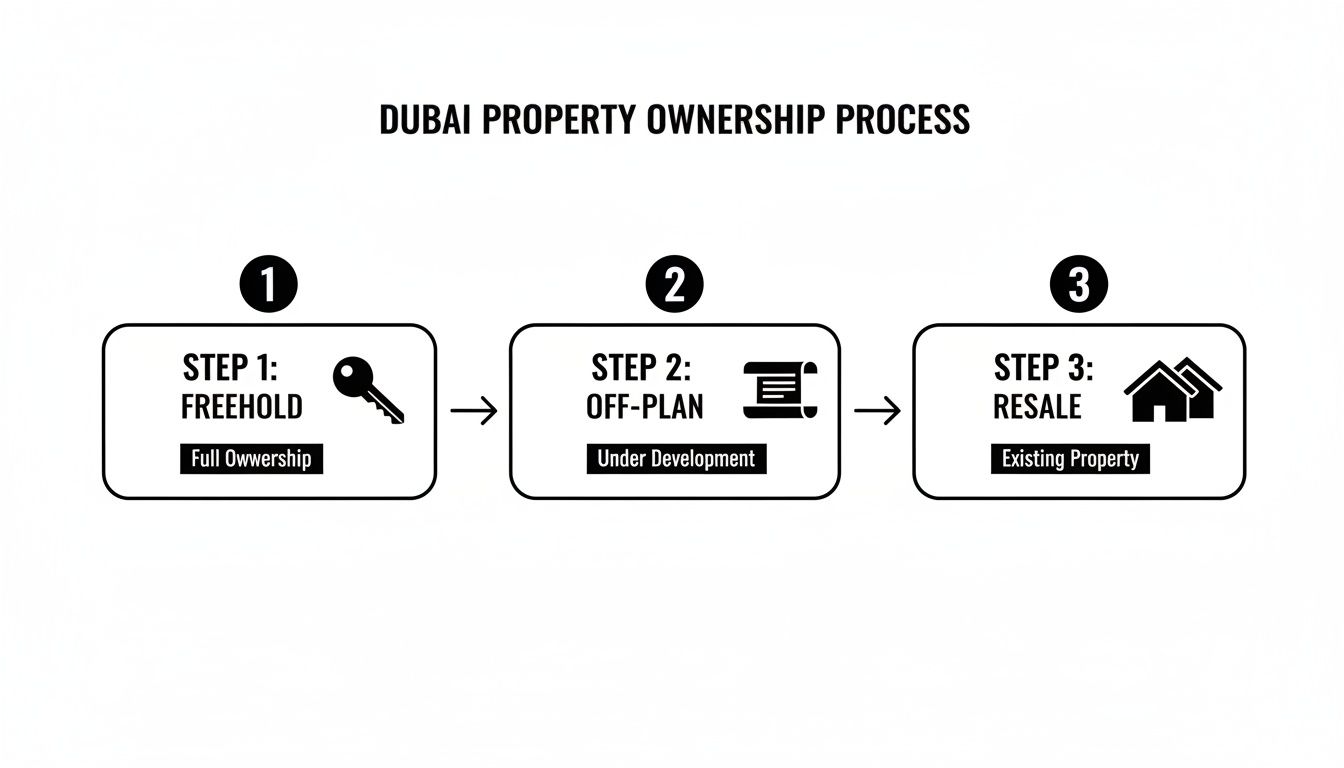

Understanding Your Dubai Property Ownership Options

Before exploring listings, it is vital to understand the fundamental ownership structures in Dubai. The path an investor takes will shape everything from budget and risk profile to potential returns. For some useful context on the market, you can find helpful general real estate information that can frame your choices.

The first decision point is whether to purchase a property off-plan from a developer or a resale property on the secondary market. Even more critical, however, is the legal ownership model.

Freehold vs. Leasehold Ownership

For any international investor, Freehold is the most important concept to grasp. Legislation enacted in 2006 permits non-GCC nationals to buy, own, sell, and inherit both land and property outright, but only within specific designated geographical zones. This grants full and indefinite control over the asset, similar to the freehold model familiar to UK buyers.

These freehold zones encompass most of the city’s well-known and desirable communities, including:

- Dubai Marina

- Palm Jumeirah

- Downtown Dubai

- Jumeirah Village Circle (JVC)

- Arabian Ranches

Leasehold ownership, conversely, grants the right to use a property for a fixed term—typically up to 99 years—without ownership of the underlying land. At the lease's expiration, ownership reverts to the freeholder. While a less common route for foreign residential buyers, it is a crucial distinction to understand. Our article on the differences between freehold and leasehold ownership provides a more detailed breakdown.

Off-Plan vs. Resale Properties

Once clear on the legal structure, an investor must decide between a new property from a developer or an existing one from its current owner.

Buying Off-Plan

This involves committing to purchase a property before its construction is complete, often based on architectural plans and 3D renderings. The primary attraction is the payment plan. Developers frequently offer attractive, post-handover payment structures that can significantly reduce the initial capital outlay. For example, a common structure may involve paying 40% during construction and the remaining 60% over several years after receiving the keys.

This strategy is favoured by investors targeting capital growth. An investor could secure a two-bedroom apartment in a high-growth area like Arjan or JVC with a relatively small down payment, anticipating capital appreciation as the project and surrounding community matures. The principal risk is project delays, but Dubai’s Real Estate Regulatory Agency (RERA) provides robust protection, including mandatory escrow accounts for all developer funds.

Key Takeaway: Off-plan is ideal for investors prioritising capital appreciation and flexible payment terms, who are comfortable with a longer timeline before realising rental income.

Buying Resale

The alternative is purchasing a resale property on the secondary market. The primary advantages are certainty and speed. An investor can physically inspect the exact unit, assess its condition, and it is often ready to generate rental income almost immediately.

A classic example is the purchase of a three-bedroom villa in a mature, sought-after community like Arabian Ranches. The full payment (or mortgage financing) is required upfront, but a tenant could be secured within weeks, providing instant cash flow. This path is often preferred by investors who seek stable, immediate income and have a low appetite for development risk.

Navigating the Legal and Financial Process

Once a property type is selected, the next stage is mastering the transaction itself. A successful investment in Dubai real estate requires understanding the legal and financial steps, which are overseen by regulatory bodies designed to protect all parties.

The two most important bodies are the Dubai Land Department (DLD) and the Real Estate Regulatory Agency (RERA). The DLD acts as the official registry, responsible for recording all property sales and issuing title deeds. RERA, its regulatory arm, establishes the rules that all developers, agents, and transactions must adhere to.

This flowchart illustrates the main pathways to ownership for both new-build and ready properties.

Whether pursuing an off-plan or resale property, the ultimate objective for an international investor is securing a freehold title, which grants complete and outright ownership.

Key Documents and Transaction Costs

The property sale is formalised via a Memorandum of Understanding (MOU), or more officially, 'Form F'. This is a legally binding contract stipulating all key terms of the sale, from price to handover date.

Before the final transfer, the seller must obtain a No Objection Certificate (NOC) from the developer. This document is critical, confirming that all service charges and other fees are settled, thus clearing the property of any outstanding liabilities before it changes hands.

Accurate budgeting is vital. The main transaction costs to plan for include:

- DLD Transfer Fee: A mandatory 4% of the property’s purchase price, paid to the Dubai Land Department to register the sale.

- Agency Fees: Typically 2% of the purchase price, plus VAT.

- Trustee Fees: A fixed administrative fee of circa AED 4,000, paid to a DLD-approved trustee office for handling the title deed transfer.

Example: For a property valued at AED 1,500,000, an investor should budget for at least AED 94,000 in additional closing costs (4% DLD fee + 2% agency fee + trustee fees). Precise calculation is essential for understanding your total initial investment.

To successfully navigate the complexities of property investment in Dubai, consider consulting a comprehensive practical guide on how to invest in Dubai real estate, which covers financing, legal steps, and partnering with agents.

Financing Your Dubai Property

For investors not making a cash purchase, securing a mortgage from a UAE bank is a well-established route. Banks in the UAE are experienced in lending to non-resident investors.

As a non-resident, the maximum Loan-to-Value (LTV) ratio is typically 50%. This means a 50% cash deposit is required, plus sufficient funds to cover all transaction fees. While some banks may offer slightly higher LTVs, this is a prudent baseline for financial planning.

To apply for a mortgage, you will generally need to provide:

- Six months of personal bank statements.

- Proof of income (e.g., payslips, tax returns).

- A copy of your passport.

Obtaining pre-approval from a bank before making offers is strongly advised. This establishes a clear budget and demonstrates credibility to sellers.

The Golden Visa Investment Pathway

A powerful incentive for investors is the UAE Golden Visa programme, a long-term residency visa directly linked to real estate investment.

To qualify, an investor must make a property investment of at least AED 2 million (approximately £450,000). The property can be off-plan or ready, and a portion may be financed via a mortgage from an approved local bank, provided the cash equity meets the minimum threshold.

The benefits are substantial, including a 10-year renewable residency visa for the investor and their family without the need for a local sponsor. For many, this residency benefit is as valuable as the financial return, providing a long-term lifestyle or business base.

It is also important to note that holding a Dubai property may have implications for your domestic tax position; our guide on capital gains tax on foreign property offers further insights.

Finding High-Yield Neighbourhoods to Maximise Returns

Once you understand the mechanics of acquisition, the focus shifts to strategy. This involves identifying which neighbourhoods align with your investment objectives: immediate rental income, long-term stability, or high capital growth.

Dubai's property market can be broadly segmented into established, prime districts and high-yield emerging communities, each offering a distinct risk-and-reward profile.

Emerging Communities for High Rental Yields

For investors focused on maximising cash flow, Dubai's emerging neighbourhoods offer some of the most attractive gross yields in the city. These areas attract a growing demographic of young professionals and families seeking modern amenities at a competitive price point.

Established vs. Emerging Markets Comparison

- Established (e.g., Dubai Marina): Offers stability, premium rents, and strong capital preservation. Lower risk profile with gross yields typically between 6-7%. Suited for wealth preservation and balanced returns.

- Emerging (e.g., Jumeirah Village Circle): Delivers higher rental yields (7-9%+) and greater potential for capital appreciation as the area matures. Higher reward profile but may involve development risk and less infrastructure.

Two areas, in particular, have become epicentres for this high-yield strategy:

- Jumeirah Village Circle (JVC): Arguably the focal point for high-yield investing in Dubai. Dominated by new apartment buildings and townhouses, JVC consistently delivers gross rental yields in the 7-9% range. Strong and reliable tenant demand is driven by a constant influx of new residents.

- Arjan: Located adjacent to the prestigious Dubai Hills Estate, Arjan is another high-performing area. It offers a similar yield profile to JVC—often between 7-8.5%—with the advantage of newer building stock and significant ongoing development.

Key Takeaway: These areas are ideal for a buy-to-let strategy focused on cash flow. Lower entry prices allow capital to go further, and strong demand for one and two-bedroom apartments keeps vacancy rates low.

Established Neighbourhoods for Stability and Growth

In contrast, Dubai’s established prime neighbourhoods offer a different value proposition. While gross rental yields are more moderate, investors gain unmatched stability, robust capital preservation, and prestige. These are the "blue-chip" postcodes of Dubai real estate.

Locations like Dubai Marina, Downtown Dubai, and Palm Jumeirah are global brands. They attract a wealthier demographic of high-net-worth individuals, tourists, and senior executives, which underpins a premium rental market.

- Dubai Marina: A perennial favourite known for its vibrant waterfront lifestyle. It commands consistent rental demand, with apartments typically yielding 6-7%. The potential for short-term lets can push these returns higher.

- Downtown Dubai: As home to the Burj Khalifa and The Dubai Mall, this is the city’s tourism and commercial heart. Yields are around 5.5-6.5%, but properties benefit from excellent liquidity and are considered a safe store of wealth.

- Palm Jumeirah: An iconic address synonymous with luxury. While apartment yields are around 5-6%, villas are primarily sought for significant capital appreciation and lifestyle appeal rather than rental income.

A key statistic attracting UK investors is the significant disparity in rental yields and tax efficiency. Dubai's 6-9% gross yields, free from income tax, deliver far superior net returns compared to London's modest yields, which are diminished by tax and high costs. You can find out more about Dubai's superior rental yields compared to London and why it’s a top choice.

Before making a final decision, it is vital to run the numbers properly. Use our interactive rental yield calculator to model different scenarios based on purchase price, expected rent, and service charges. This simple tool helps you look beyond headline figures to understand how a potential investment will truly perform.

Performing Due Diligence and Building Your Team

Identifying a target location is only half the battle. The most critical part of investing in Dubai real estate is protecting your capital through rigorous due diligence and assembling a trusted team of professionals. Overlooking this fundamental step is a costly mistake.

This process is not about delay; it is about ensuring your investment is secure, transparent, and legally sound from the start.

Your Due Diligence Checklist

Before signing any contract or transferring funds, you must independently verify the key details of the property and all parties involved.

Here are the non-negotiable items for your checklist:

- Verify the Developer and Project: For off-plan purchases, use the Dubai Land Department’s official Trakheesi system. This allows you to check the developer’s registration and, most importantly, confirm the project has a valid escrow account. This legal requirement protects your funds by ensuring they are used only for construction.

- Check the Title Deed: For a resale property, you must scrutinise the title deed. This document identifies the legal owner and reveals any existing mortgages or other liabilities registered against the property.

- Analyse Service Charges: High service charges can significantly erode your net yield. Request a full breakdown of charges for the past two years to get a realistic picture of running costs. In Dubai, these fees cover building maintenance, security, and amenities and are a major factor in your true profitability.

Key Takeaway: A property may be advertised with a 7% gross yield, but if annual service charges equate to 2% of the property’s value, your net yield is far lower. Always calculate your net yield after all costs are accounted for.

Assembling Your Professional Team

Navigating a Dubai property transaction without local experts is a high-risk endeavour. Building a reliable team is non-negotiable for a smooth, secure purchase. For more general advice on international property acquisition, you can explore our guide on how to buy property abroad.

Selecting Your Real Estate Agent

Your first appointment should be a reputable, RERA-certified agent. Their role extends beyond sourcing property to providing market intelligence, advising on fair value, and handling initial negotiations.

Red flags to watch for:

- Agents not listed on the DLD’s official Broker’s Register.

- Pressure to make a quick decision without proper checks.

- A lack of transparency regarding fees and commissions.

A true professional will welcome scrutiny and provide clear, verifiable information.

Appointing a Qualified Conveyancer

A qualified conveyancer or property lawyer protects your legal interests. Their role is separate from the agent's and is equally vital. They are responsible for reviewing all contracts, including the sales agreement (Form F), and ensuring all legal paperwork is correct.

The conveyancer conducts official legal checks, manages the transfer of funds, and ensures the No Objection Certificate (NOC) is processed correctly. They are your legal safeguard, ensuring the title you receive is clean and unencumbered. Never rely on the seller's or developer's legal team; always appoint your own independent representation.

Post-Acquisition: Management and Exit Strategy

Securing the keys to your new Dubai property is a significant milestone. For an investor, however, this is where the operational phase begins. For those managing an asset from overseas, the next step is transforming the property into a hands-off income stream.

This is where professional property management is indispensable. These firms handle everything from marketing the property and sourcing credible tenants to managing maintenance and ensuring timely rent collection. Their purpose is to ensure your asset performs without requiring your day-to-day involvement.

Creating a Hands-Off Investment

A good management company will handle all the administrative tasks unique to Dubai. This includes registering the tenancy agreement with Ejari, the mandatory government system that legally formalises the landlord-tenant relationship.

A comprehensive service should include:

- Tenant Sourcing and Vetting: Finding and screening quality tenants to minimise vacancy and default risk.

- Contract and Legal Management: Handling the tenancy contract, Ejari registration, and managing renewals or disputes.

- Rent Collection and Financials: Collecting rent payments and providing clear, regular financial statements.

- Maintenance and Repairs: Coordinating all necessary upkeep to protect the value of your asset.

Key Takeaway: The standard fee for comprehensive property management in Dubai is typically between 5% and 8% of the annual rent. While an additional cost, the professional oversight it provides is invaluable for an international investor.

Planning Your Exit Strategy

A prudent investment begins with the end in mind. A clear exit strategy is not just about when to sell, but also how to do so to maximise profit. Your exit should be a calculated move based on data, not a reaction to market sentiment.

Timing is critical. This involves monitoring Dubai’s property cycles, broader economic indicators, and major new infrastructure projects in your area that could influence prices. Selling at the peak of a market cycle can significantly impact your final capital gain.

When you decide to sell, be realistic about the costs involved. These are similar to your acquisition costs and will include a 2% agent’s fee (plus VAT) and potentially a share of the 4% DLD transfer fee, which is often split between buyer and seller. Factoring these costs in from the start is crucial for accurately calculating your net profit.

Finally, consider the repatriation of funds. UAE banks are highly experienced in handling international transfers from property sales, making the process straightforward. It is advisable to consult your bank early to understand their process and requirements.

Common Questions from Global Investors

To conclude, let's address some of the most common questions from international investors considering Dubai.

Do I Need a UAE Bank Account?

While not strictly mandatory for a cash purchase, managing your investment without one is administratively burdensome. It is highly recommended.

Most international investors open a non-resident account. It is the simplest method for receiving rental income, paying service charges, and handling other local expenses. Banks such as HSBC and Emirates NBD have well-established processes for non-residents.

How Do I Repatriate Funds?

This process is simpler than many assume. Moving funds from a property sale or repatriating rental income is straightforward and well-regulated.

The UAE has no currency controls, meaning you are free to transfer money to your home bank account at any time. Your UAE bank will execute the international transfer, which typically arrives within a few business days. Be sure to check their specific transfer fees and exchange rates.

What Are the UK Tax Implications for British Investors?

This is a critical consideration where many new investors err. While rental income and capital gains are tax-free within the UAE, UK residents are legally required to declare this foreign income to HM Revenue and Customs (HMRC).

Key Takeaway: Under UK tax law, residents are taxed on their worldwide income. Although double-taxation treaties exist, Dubai's 0% tax rate means there is no foreign tax to credit. Your liability will therefore be calculated based on your UK income tax bracket. It is imperative to seek advice from a tax professional specialising in international property.

Compliance with your home country's tax authority is as important as adhering to the regulations of the Dubai Land Department.

At World Property Investor, we provide the data and analysis you need to make informed decisions in global markets. Explore our guides to uncover your next investment opportunity at https://www.worldpropertyinvestor.com.