Greek residential values are projected to rise notably by August 2026, based on market figures cited later in this article. For UK buyers, that matters less as a headline and more as a signal. Greece is no longer a cheap second-home story. It is an EU property market where timing, tax treatment, and deal structure now affect returns.

Post-Brexit, a British buyer has to assess more than purchase price. The practical questions are residency rights beyond 90 days in 180, sterling to euro currency risk, how the UK-Greece tax treaty applies to rental income and capital gains, and whether an older property will absorb cash after completion through legalisation work, roof repairs, boundary disputes, or electrical upgrades.

That is where many buyers lose margin.

The better approach is to underwrite Greece as an international investment. Start with expected use, rental strategy, holding period, and exit route. Then test the asset for hidden costs, especially in older village houses and island stock, where listing photos often hide deferred maintenance and planning irregularities. Buyers considering income should also benchmark local letting demand against the practicalities of the Greek rental market for houses and holiday property.

Handled properly, Greece can still offer strong lifestyle value and solid long-term upside. Handled casually, it becomes an expensive lesson in cross-border buying.

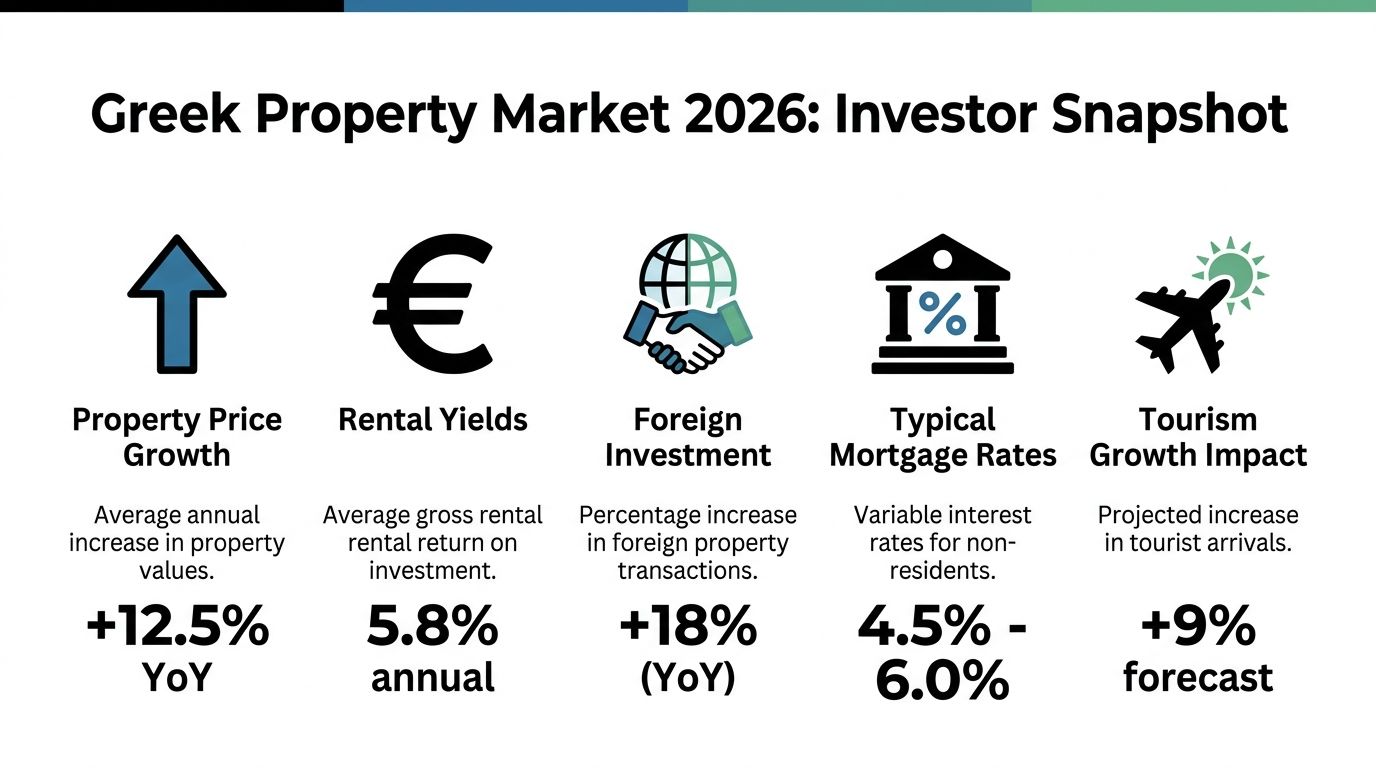

The Greek Property Market in 2026 An Investor's Overview

Greek residential values are expected to rise further by August 2026, from figures in 2023, based on projections cited earlier in this article. For a UK buyer, the headline matters less than what sits behind it. Greece has moved out of the bargain-bin category, but it still trades below many Western European markets while offering stronger tourism-linked income potential in the right locations.

The market case is straightforward. Entry pricing remains attractive relative to France and, in many areas, Spain. Demand is supported by tourism, foreign capital, and limited high-quality supply in proven micro-markets. The complication for British buyers is post-Brexit execution. A purchase now sits inside a cross-border framework that includes 90-day stay limits for non-residents, sterling to euro exposure, and tax planning under the UK-Greece double taxation treaty.

That changes how I assess a deal.

A Greek purchase should be underwritten in euros, stress-tested for slower resale, and reviewed for legal and building risk before any buyer starts comparing it with a UK buy-to-let. In practice, the spread between a good deal and a poor one is often hidden in the asset itself. Older houses can look cheap on a listing and still destroy yield through roof works, boundary issues, electrical replacement, or planning regularisation after completion.

Why UK buyers are still active

British demand has not disappeared because Brexit made the process harder. It has become more selective.

The buyers still entering the market fit one of three profiles. They want urban exposure in Athens or Thessaloniki, a seasonal rental asset in Crete or the Ionian Islands, or a property that also supports a wider residency strategy. Those are valid approaches, but each needs a different return model and a different tolerance for vacancy, compliance work, and resale timing.

Rental income is one reason Greece stays on the shortlist. In the stronger tourism markets, gross yields can be attractive, but they are uneven and local. Anyone modelling income should compare assumptions against actual conditions for renting houses in Greece and regional holiday-let demand, especially where seasonality compresses annual occupancy.

What is supporting prices

Several forces are keeping the market firm, although they do not apply equally across the country.

- Foreign buyers continue to support demand in prime city districts and established island markets.

- Tourism remains a pricing driver where short-stay demand is deep enough to support investor interest.

- Lifestyle migration has widened the pool of tenants and buyers in selected coastal and urban areas.

- Supply remains tight for renovated, legally clean stock in desirable locations.

The main investment point is simple. Greece is not one market. Central Athens behaves differently from Chania. Lefkada trades on a different cycle from Thessaloniki. A village house with deferred maintenance should not be priced, or financed mentally, like a renovated apartment with clear title and proven rental history.

Market outlook for 2026

For 2026, I would treat Greece as a selective-buy market rather than a broad market chase. Prime areas with constrained supply can still perform well. Secondary locations and compromised stock need a larger discount because financing is less straightforward, buyer pools are thinner, and hidden capex can wipe out early gains.

For UK investors, the opportunity remains, but only if the numbers survive three tests. Net yield after all local costs. Legal clarity on title and building status. A holding structure that works under both Greek rules and the UK tax position. If those three line up, Greece can still deliver strong long-term value. If they do not, lower entry pricing is irrelevant.

Choosing Your Investment Location and Property Type

A UK buyer can make money in Athens and lose money on a cheaper house in Crete. Entry price alone does not decide the result. Liquidity, seasonality, legal status, and post-Brexit holding costs do.

Location choice should start with the end use. A property meant for year-round long lets, occasional personal use, or peak-season holiday income needs a different market, a different management model, and a different risk tolerance. For UK buyers, I also test whether the asset still works after Greek taxes, UK reporting, travel friction, and local operating costs.

Choose the market that fits the income model

Established locations give you a clearer resale path and more predictable demand. You pay more for that visibility. Secondary or emerging areas can offer a better entry multiple, but only if you can hold longer and manage thinner buyer demand on exit.

| Location | Best suited to | Pricing position | Income profile |

|---|---|---|---|

| Athens South | Buyer seeking prime urban exposure and stronger resale liquidity | Premium relative to most mainland markets | Better suited to long-term lets and premium short stays in select districts |

| Thessaloniki | Buyer seeking city exposure at a lower ticket size than prime Athens | Mid-range for a major Greek city | More attractive for long-term residential demand than pure holiday income |

| Mykonos | Lifestyle-led buyer targeting prestige and high seasonal rates | Among the highest in Greece | Strong peak-season income, with sharper volatility and heavier management demands |

| Chalkidiki | Holiday-let investor focused on beach-led tourism | Wide spread based on frontage, access, and build quality | Seasonal income can be strong, but occupancy is concentrated |

I have removed locations where this section did not have fully verified table data. That is the right standard to apply. Chania and Kavala are still worth tracking, but they are better discussed qualitatively than forced into a table with uneven sourcing.

Athens works best for buyers who want broader exit demand, easier access to professional management, and an asset that is not entirely dependent on summer tourism. For a UK investor watching currency risk and tax leakage, that stability often matters more than chasing the highest headline nightly rate.

Thessaloniki can produce a more disciplined entry point. It suits buyers who prefer local tenant demand, universities, and lower capital exposure than prime Athens. The trade-off is a smaller international buyer pool if you sell.

Mykonos is a specialist market. It can produce exceptional gross revenue in the right micro-location, but the purchase price, staffing costs, compliance burden, and seasonality are all high. I only like it when the buyer accepts that this is an operating business as much as a property investment.

Chalkidiki suits buyers who understand drive-to tourism, family summer demand, and short occupancy windows. It is less forgiving if your financing model assumes smooth year-round income.

For a broader regional comparison, this guide to the best location for property investment is a useful starting point.

Property type changes the risk profile

The sharper decision is often not island versus city. It is renovated apartment versus older house.

A modern apartment with clear title, lawful floor plans, and clean service-charge records is easier to underwrite. An older stone house may look cheaper at first glance, but the discount often disappears once you price structural repairs, insulation, drainage, roof work, legal regularisation, and the months when the property cannot earn income.

According to Your Overseas Home on Greece property buying pitfalls, older Greek properties can be priced below comparable stock, but buyers often inherit damp, poor insulation, or unauthorised alterations. The same source notes that the state Renovate-and-Rent subsidy offers up to €8,100. That can help on minor works. It does not solve a failed roof, boundary dispute, or a house with multiple undocumented changes.

For UK buyers, older stock creates an extra layer of exposure. Since Brexit, repeat inspection trips are less convenient, contractor oversight is harder from the UK, and delays can leave you carrying an empty asset while dealing with both Greek administration and UK tax reporting.

My screening framework for older Greek properties

I use five filters before I treat any discount as value.

- Legal file: Check permits, plans, extensions, terraces, storage rooms, and boundary lines. If the built reality does not match the file, the price must reflect the cost and time needed to regularise it.

- Moisture and structure: Coastal salt exposure, hillside runoff, and old roofs create expensive problems. Cosmetic paintwork can hide active damp for one season, not for one winter.

- Energy performance: Poor insulation and dated heating systems hurt winter lettings, resale appeal, and operating margin.

- Access and services: Narrow roads, weak parking, septic issues, and unreliable utilities reduce both rental performance and exit liquidity.

- Exit buyer pool: Define who will buy from you later. A domestic cash buyer, another UK owner, or a lifestyle purchaser from northern Europe all value the same property differently.

One missing document can wipe out the apparent bargain.

Rule of thumb: If the seller cannot produce the technical and legal paperwork quickly, assume the discount is compensation for risk, not a gift.

UK buyers should also separate personal preference from investment logic. A charming village house can still be a poor investment if the local resale pool is thin, the renovation file is messy, and the income season is too short to cover capex. A plain apartment in the right part of Athens often produces a better risk-adjusted return.

Navigating the Legal Path to Ownership

A Greek purchase can move from accepted offer to completion in a matter of weeks, but speed is not the metric that matters. For UK buyers after Brexit, the true test is whether the deal is legally clean, tax-efficient, and executable without creating residency or banking friction you did not price in at the start.

The key principle

The legal process in Greece rewards sequencing, not enthusiasm.

UK buyers often focus first on price and location. The better approach is to secure your legal representative early, confirm how funds will move from the UK into Greece, and only then commit to a deposit structure. Post-Brexit, that order matters more because a non-EU buyer faces extra practical checks around tax registration, document certification, powers of attorney, and time spent in Greece.

Your lawyer is the risk filter. The notary formalises the transfer, but the lawyer should identify title defects, inherited ownership issues, undisclosed charges, planning irregularities, and whether the seller has the legal capacity to complete the sale.

Set up the file before you negotiate hard

A non-EU buyer needs a Greek tax number, known as an AFM, to transact. Many buyers also open a Greek bank account early, although the exact banking route depends on the seller, the notary, and anti-money-laundering checks on the source of funds.

For UK clients who do not want repeated travel, a Power of Attorney usually saves time and prevents delays at signing stages. It needs to be prepared properly for Greek use, with the right certification path in the UK. Getting this wrong is expensive because it tends to fail late, when the transaction is already under deadline pressure.

This wider guide on how to buy property abroad is useful if you want to compare the Greek process with other cross-border purchases.

Build an independent team

At minimum, appoint:

- A bilingual Greek lawyer who acts only for you.

- A notary to prepare and execute the deed.

- A civil engineer or surveyor to confirm the physical and planning reality of the asset.

Independence matters. An estate agent may recommend all three, and some recommendations are perfectly serviceable, but I prefer clear separation between the sales side and the due diligence side. If a deal is legally awkward, you want advisers who are paid to slow it down, not push it through.

Treat the reservation and deposit stage seriously

In Greece, the first money paid can carry significant legal and financial consequences. Before any deposit is released, your lawyer should confirm who owns the property, whether there are mortgages or claims registered against it, and whether the property’s built form matches the approved documentation closely enough to proceed.

For UK buyers, this is also the point to test the practical side of the transaction. Can the seller provide a clean document pack quickly? Are there old additions, enclosed terraces, storage rooms, or boundary discrepancies that need engineer sign-off? If the answer is vague, assume the timetable will slip and the actual cost will rise.

What legal due diligence should cover

A proper review goes beyond asking whether the seller has a title deed.

Your lawyer and engineer should verify:

- the seller’s legal ownership and right to sell

- any mortgages, liens, court claims, easements, or other encumbrances

- whether the cadastral position and boundaries match the marketed asset

- whether the building permit, plans, and actual construction align

- whether municipal taxes, common charges, and utility issues are outstanding

- whether the documents required for notarial transfer and registration are complete

Older Greek properties deserve extra scrutiny. The hidden-cost problem is rarely one dramatic defect. It is a stack of smaller issues, such as an unregularised extension, missing plans, a disputed boundary wall, outdated electrical work, or incomplete inheritance paperwork. Each item may be fixable. Together, they can change the return profile of the deal.

UK-specific tax and residency points buyers miss

Owning Greek property does not by itself make a UK buyer Greek tax resident, but use patterns matter. If you plan long stays, rental activity, or a later move under a residency route, structure the purchase with that end use in mind from day one.

The UK-Greece double taxation framework helps prevent the same income being taxed twice, but it does not remove filing obligations in both jurisdictions where they apply. Greek-source rental income, local property taxes, and the way expenses are treated should be reviewed before completion, not after the first tax deadline arrives. A lawyer is not always a tax adviser, so cross-border buyers often need both.

This is one of the biggest gaps I see in generic buying guides. Buyers spend heavily on the asset and too little on pre-purchase tax planning.

Completion and registration

Completion takes place before the notary, with the final deed executed once the pre-signing legal and tax steps are in order. After signing, the transfer must be registered correctly with the relevant land or cadastral records.

Registration is part of the acquisition, not admin to tidy up later.

Ask for written confirmation of each completed stage, including legal checks, tax number setup, deed execution, and registration filing. In cross-border purchases, paper trails protect you as much as the contract does.

Financing Your Purchase and Understanding Costs

Greek acquisition costs often add roughly 8% to 15% above the agreed price before renovation, furnishing, or financing friction. For a UK buyer working in sterling and purchasing in euros, the key underwriting question is not "Can I afford the property?" It is "What is my total capital in, and what could still go wrong after completion?"

The all-in budget matters more than the asking price

The purchase price is only one line in the model. Buyers also need to account for transfer tax where applicable, notary fees, legal fees, land registration costs, agent fees if agreed on their side, bank charges, valuation costs, and foreign exchange spreads.

The tax treatment depends on the asset. Resale property is typically subject to transfer tax. New build taxation needs checking at the time of purchase because the temporary VAT suspension that many older guides refer to was time-limited and should not be treated as a standing rule in 2026. I advise clients to confirm the tax position on the specific unit in writing, through their lawyer and accountant, before they commit funds.

A conservative buyer should also hold a contingency reserve. Older Greek properties, especially on islands or in historic areas, often come with cost items that do not show up in the brochure: electrical upgrades, damp treatment, septic or drainage work, roof repairs, boundary clarification, and delayed utility transfers.

A practical cost framework for older properties

UK buyers can improve returns by underwriting better. I use a four-part screen before calling an older property "good value":

1. Acquisition costs. Taxes, notary, legal, registration, survey, FX, and mortgage setup if debt is involved.

2. Immediate capex. Works required in the first 12 months to make the property lettable, insurable, or structurally sound.

3. Operating drag. ENFIA, insurance, management, service charges, maintenance, licensing compliance for short lets if relevant, and vacancy allowance.

4. Exit friction. Future saleability, tax on disposal, buyer pool depth, and whether irregularities in title or construction could reduce resale value.

This framework matters more in Greece than many buyers expect. A low entry price can hide a weak return if the property needs legal regularisation, heavy remedial works, or ongoing maintenance that is hard to manage remotely from the UK.

Financing options for UK buyers

Many British buyers still purchase in cash because Greek lending to non-residents can be selective, documentation-heavy, and slower than buyers expect. Where financing is available, terms vary by borrower profile, property type, and source of income. Lenders will want clean proof of funds, declared income, tax records, and a property they are comfortable taking security over.

Debt can improve returns, but only when the borrowing cost, FX exposure, and holding period all make sense together. A euro mortgage against euro rental income can create a cleaner match than funding everything from sterling, but that depends on whether the asset is an income property or mainly for personal use.

For financing preparation, this guide on second home mortgage requirements gives a good framework for lender expectations and affordability discipline.

Ongoing ownership costs and cross-border tax exposure

Annual property taxes and routine running costs rarely destroy a deal on their own. Poor forecasting does. The bigger issue for UK buyers is that Greek costs sit alongside UK reporting obligations, and the combined effect is often missed at purchase stage.

Immigrant Invest’s overview of Greek real estate investment highlights the points that need proper cross-border advice: treatment of Greek rental income, use of relief under the UK-Greece double taxation framework, inheritance planning, and the question of personal versus company ownership.

That last point deserves attention. A company structure can look tidy on paper and still be inefficient in practice once you factor in compliance, banking, reporting, and eventual disposal. For most private buyers, simplicity has value, but the right answer depends on use case, expected rental income, succession planning, and whether residency is part of the wider plan.

Questions to settle before exchange

- What is your total acquisition budget after taxes, fees, FX costs, and contingency?

- Is the property a resale unit or a new build, and what tax applies to that exact purchase in 2026?

- What capital expenditure is required in the first year, not just eventually?

- Will the property generate income, and if so, how will that income be reported in Greece and the UK?

- Are you buying in personal name for simplicity, or considering a structure that may add cost without improving the outcome?

- If you are borrowing, have you stress-tested rate risk, currency risk, and vacancy assumptions together?

A short explainer is useful here as well:

Practical advice: Ask your advisers for a written all-in cost sheet before exchange, including tax treatment, closing costs, first-year capex, annual holding costs, and the UK reporting implications. That document prevents more expensive mistakes than any negotiation on the headline price.

The Golden Visa and Residency for UK Buyers

More UK buyers now treat Greek residency as a planning issue, not a lifestyle extra. Since Brexit, British passport holders no longer have automatic freedom of movement in the EU, so any purchase tied to longer stays in Greece needs to be assessed against visa rules, tax residence exposure, and the practical cost of compliance.

The Greek Golden Visa can still work well for a UK buyer, but only if the property stands up on its own merits. Residency should sit on top of a sound acquisition. It should not be the reason a weak deal gets approved in your head.

Why the residency angle matters after Brexit

For a British national, the practical attraction is clear. A qualifying investment can support a Greek residence permit and give your family more flexibility for time in Greece and wider Schengen travel, subject to the permit rules in force at the time of application and renewal.

That said, a residence permit is not the same as tax residency. I see buyers blur those two concepts too often. Spending more time in Greece, earning rental income there, or shifting the centre of your life can change your filing obligations. UK buyers need their Greek lawyer and UK tax adviser aligned before completion, especially where double tax treaty treatment, foreign tax credits, and future inheritance planning are part of the wider strategy.

The threshold is only the start

The headline threshold gets attention, but the investment case is decided elsewhere. Location-specific minimums, asset category rules, and programme amendments can all affect eligibility, and those details need to be checked against the current law before you commit funds.

The more expensive mistake is overpaying for a qualifying asset in a visa-driven pocket of the market. That is common in parts of Athens and on islands with thin resale depth. If the premium is being justified mainly by residency demand, ask what happens to exit value if rules tighten, demand shifts, or a later buyer does not care about the permit.

I use a simple order of operations with clients:

- Underwrite the property as a property.

- Confirm it satisfies the current Golden Visa criteria.

- Test the holding structure, tax reporting, and family residency plan together.

- Check the exit. Resale demand matters more than entry status.

Older properties need a hidden-cost screen

This matters even more if you are buying an older Greek property to meet a residency route at a lower entry price. The nominal purchase figure can look efficient, then unravel once legalisation work, building compliance, electrical upgrades, plumbing, roof repairs, communal arrears, and energy improvements are priced properly.

For UK buyers, post-Brexit planning becomes more technical. If the property is meant to support part-time residence, family use, and some rental income, the wrong asset can create friction on three fronts at once. Higher capex, slower permit execution, and awkward tax reporting in both jurisdictions.

A practical filter helps. Before reserving the property, ask for a written schedule covering permit eligibility, engineer findings, declared square metres versus actual layout, any unauthorised works, and the first 24 months of expected capital expenditure. On older stock, that discipline protects returns far more effectively than focusing on the visa headline.

For broader context, this guide to EU Golden Visa options is a useful comparison point.

Mitigating Risks and Common Investor Pitfalls

Post-completion mistakes cost more than negotiation mistakes. In Greece, I see UK buyers lose time and yield through filing errors, restricted-area surprises, and underpriced renovation risk more often than through the headline purchase price itself.

The sales pitch often focuses on lifestyle and entry price. The operating reality is different. UK buyers now have a post-Brexit compliance burden that generic Greece guides understate, especially where the property may be used part of the year, rented seasonally, or held for a future residency option.

Ellas Estate’s step-by-step purchase process guide highlights two practical points that matter after closing. New owners must complete Cadastre and tax registrations, and owners remain exposed if rental income or annual property tax reporting is handled badly. That should shape your process from day one.

Common problems that erode returns

Seller paperwork is weaker than the agent suggests

Assume the file is incomplete until your lawyer and engineer confirm otherwise. Missing legality documents, unregistered alterations, boundary inconsistencies, communal fee arrears, and outdated plans are common failure points. A property can still reach signing stage and remain a poor investment if those issues delay rental licensing, refinancing, resale, or inheritance planning.

Restricted-area rules are spotted too late

Some border regions and islands require extra permissions for non-EU nationals, including UK buyers. That can slow the timetable materially. If your plan depends on a summer handover, immediate refurbishment, or first-season rental income, a delay here affects cash flow, not just convenience.

Older stock looks cheap and performs badly

This is the trap I flag most often. A low acquisition price in Greece can conceal electrical work, plumbing replacement, roof repair, moisture treatment, façade obligations, energy upgrades, and legalisation costs for past alterations. On paper, the property looks like value. In practice, the yield disappears once capex and downtime are priced properly.

UK tax and Greek tax are treated as separate workstreams

They are not. A UK resident owner with Greek rental income, local taxes, and bank reporting obligations needs a joined-up plan. The UK-Greece Double Taxation Convention can help prevent the same income being taxed twice, but it does not remove the need to report correctly in both jurisdictions. The risk is usually administrative failure, not the treaty itself.

What reduces risk in practice

- Instruct an independent lawyer before paying a reservation deposit: Do not rely on the selling side to define what checks matter.

- Use an engineer who inspects legality and condition together: Structural defects and planning defects often sit in the same file.

- Price the first 24 months, not just the acquisition: Include tax filings, insurance, utilities setup, management, repairs, and a reserve for unexpected works.

- Stress-test the rental case: Check whether the property can support the licensing, season length, occupancy, and operating model assumed in your forecast.

- Confirm nationality-sensitive approvals early: UK buyers should not leave restricted-area checks until after funds are committed.

- Set up post-completion reporting before completion: ENFIA, rental declarations, local accounts, and UK reporting need named responsibility from the start.

One final filter helps. If the investment only works when everything goes right, the margin is too thin for an overseas buyer. The Greek assets that hold up best are the ones with clean documents, realistic capex, manageable tax reporting, and resale demand that does not depend on a perfect market.

Your Investment Checklist Before Buying in Greece

A good Greek purchase is the result of discipline rather than speed. Most problems show up early if you force the process into a checklist.

Before you search seriously

- Define the objective: Personal use, income, residency, or long-term capital growth. Pick one primary goal.

- Set the all-in budget: Include purchase taxes, professional fees, furnishing, management, insurance, and a repair reserve.

- Decide on ownership structure: This needs UK and Greek tax input before you commit.

- Shortlist locations by strategy: Prime urban areas, tourism-led islands, and emerging mainland markets behave differently.

Before you make an offer

Confirm the team

Use a bilingual lawyer, an independent engineer, and a notary who regularly handles foreign-buyer transactions. If you are relying on Power of Attorney, set it up early.

Test the property, not the brochure

On older homes, verify damp risk, insulation, legality of extensions, roof condition, and boundaries. A nice terrace view does not fix a bad file.

Check the rental thesis

If the property is an investment, ask who the tenant or guest is. Summer tourist, long-term local tenant, digital nomad, or mixed-use owner-occupier. That answer affects furnishing, licensing, management style, and cash flow.

Before signing a deposit contract

Use this as a decision gate, not a formality.

- AFM obtained: Without it, administration becomes slower.

- Lawyer has started title checks: Do not rely on seller statements.

- Document pack reviewed: Missing papers should trigger caution, not optimism.

- Deposit terms understood: Especially the consequences if either side withdraws.

- Currency plan in place: A large sterling-to-euro transfer should not be improvised.

Before completion

A prudent buyer wants a clean written record.

- Written due diligence summary from the lawyer

- Technical report from the engineer

- Final cost schedule from the notary and all advisers

- Proof of how taxes and fees will be settled

- Post-completion plan for registration and tax declarations

After completion

Ownership becomes real.

- Register at the Cadastre

- Declare the property correctly on Taxisnet

- Set up ENFIA handling

- Transfer utilities and arrange insurance

- If renting, align Greek and UK income reporting from the start

The buyers who do best in Greece are not the ones who move fastest. They are the ones who understand that buying a home in Greece is both a property transaction and a compliance project.

If you get the market selection right, the legal file clean, the tax structure sensible, and the building condition verified, Greece can be an excellent long-term addition to a UK investor’s portfolio. If you cut corners on any of those four, the “bargain” often disappears.

World Property Investor helps buyers compare markets, assess rental yield potential, understand foreign ownership rules, and manage cross-border property decisions with more confidence. Explore World Property Investor for in-depth country guides, market analysis, and practical international buying advice.