Securing a mortgage for a second home is a different discipline compared to financing a primary residence. Lenders view it as a higher-risk proposition, which means applicants face a more rigorous approval process. A substantial deposit, robust credit history, and clear evidence of your capacity to afford two mortgages simultaneously are fundamental.

This guide provides an authoritative, data-driven look at the requirements for global property investors, focusing on long-term fundamentals and actionable insights.

What Lenders Require for a Second Home Mortgage

When you approach a lender for a second home loan, their primary concern is risk management. The logic is straightforward: if an individual encounters financial difficulty, they are statistically more likely to default on a discretionary property mortgage than the one for their primary family home. This fundamental difference is why the requirements are deliberately strict.

Lenders demand irrefutable evidence of financial stability. This is not merely about whether you can obtain the loan today; it is about proving you can manage the costs over the long term, even if your personal or wider economic circumstances change.

The Four Pillars of a Strong Application

To mitigate their risk, lenders will scrutinise your application based on four core pillars. A weakness in any one of these areas can jeopardise approval or result in less favourable terms.

- A Substantial Deposit: For a second home, lenders will typically demand a minimum of 25% of the property’s value. In certain markets or for non-resident investors, this can increase to 30-40%.

- A Robust Credit History: Your credit file will be meticulously examined. Lenders seek a strong score and a flawless track record of managing debt.

- A Low Debt-to-Income (DTI) Ratio: This ratio measures your total monthly debt obligations against your gross monthly income. Lenders must be satisfied that an additional mortgage will not over-leverage your finances.

- Verifiable Income and Cash Reserves: You must prove you have a stable and sufficient income to cover both mortgages, plus several months of liquid cash reserves as a financial buffer.

Understanding Affordability Stress Tests

Beyond these pillars, lenders employ a crucial tool called an 'affordability stress test'. This is not about whether you can afford the monthly payments at today’s interest rate. The lender will calculate if you could still meet your obligations if rates were to rise significantly, often by several percentage points.

This stress test is a key component of second home mortgage requirements. It ensures you possess the financial resilience to handle increased costs without defaulting, protecting both you and the lender from future economic shocks.

When considering a second mortgage, particularly with other outstanding loans, it is also important to understand how lenders prioritise existing debts. You can learn more about how they handle different loans by reading up on Subordination Agreements. This provides essential groundwork for the detailed requirements we will now explore.

The Four Pillars of Mortgage Approval

When it comes to securing finance for a second property, every lender bases its decision on four core pillars. For any global investor, demonstrating strength across these four areas is non-negotiable. Lenders view a second home as a discretionary purchase, which automatically increases its perceived risk profile. Your objective is to present an application so robust that it leaves no doubt about your financial stability.

Pillar 1: The Deposit

The size of your deposit is the most immediate signal of your financial strength and commitment. For a second home, lenders require a significant upfront investment to lower their own exposure from day one.

As a general rule, you should be prepared to provide a minimum deposit of 25% of the property’s price. In more competitive or emerging markets, where a lender might feel more exposed, that figure can easily rise to 30% or even 40%, particularly for non-resident buyers. A larger deposit not only improves your probability of approval but can also unlock more competitive interest rates.

Pillar 2: Your Creditworthiness

Your credit history is your financial curriculum vitae, demonstrating how reliably you have managed debt in the past. Lenders will analyse this meticulously, looking for a clear and consistent pattern of on-time payments across all credit facilities.

This can become a significant hurdle for investors with credit files in different countries. Not all credit reports are directly transferable, and some lenders lack the framework to assess a foreign file. It is vital to obtain official copies of your credit report from every jurisdiction where you have held credit and be prepared to provide them, sometimes with certified translations. An 'excellent' score in your home country is a strong starting point, but you must be able to substantiate it.

Pillar 3: The Debt-to-Income Ratio

The debt-to-income (DTI) ratio is one of the most critical metrics in any mortgage application. It measures your total monthly debt payments—including your existing mortgage, car loans, and credit card minimums—against your total monthly income before tax.

Your DTI is calculated with a simple formula: (Total Monthly Debt Payments / Gross Monthly Income) x 100. While a DTI below 36% is often targeted for a primary mortgage, lenders apply stricter limits for second homes, typically requiring a ratio below 43% inclusive of payments for both properties.

This calculation is fundamental to affordability assessments. In the UK, for instance, securing a mortgage for a second home often means meeting stringent buy-to-let (BTL) criteria. Lenders typically demand that minimum 25% deposit, and run stress tests to ensure the investment remains viable at higher interest rates. Data from the Financial Conduct Authority provides further insight into these lending trends.

Pillar 4: Cash Reserves

Finally, lenders need to see evidence of a financial safety net. After you have paid the deposit and all associated transaction costs, you must have sufficient liquid cash remaining. This demonstrates you can manage the mortgage payments on both your properties for a period, even if you face an unexpected loss of income or the rental property sits vacant.

Lenders will generally require sufficient cash reserves to cover three to six months of payments for both your primary and second home. For higher-value properties or in markets they deem riskier, they may request even more. These reserves prove you are not financially overstretched and can withstand a financial downturn without defaulting.

Primary vs. Second Home Mortgages at a Glance

This table offers a clear comparison of typical mortgage requirements for a primary residence versus a second home or buy-to-let property in an established market like the UK.

| Requirement | Primary Residence (Owner-Occupied) | Second Home / Buy-to-Let |

|---|---|---|

| Minimum Deposit | 5-10% is common, but varies. | 25% or more is standard. |

| Affordability Test | Based on personal income and expenditure. | Stricter stress-testing; often requires rental income to cover 125-145% of the mortgage payment at a higher 'stress' interest rate. |

| Interest Rates | Generally lower, more competitive rates. | Typically higher to reflect the lender's increased risk. |

| Cash Reserves | Sometimes required, but less common. | 3-6 months of payments for both properties is a common requirement. |

| Credit Score | 'Good' is often sufficient. | 'Excellent' is strongly preferred; any issues are scrutinised more heavily. |

As evidenced, the standard is set considerably higher for second properties. Lenders are not just looking for a good borrower; they need to be convinced you are a low-risk, financially resilient investor.

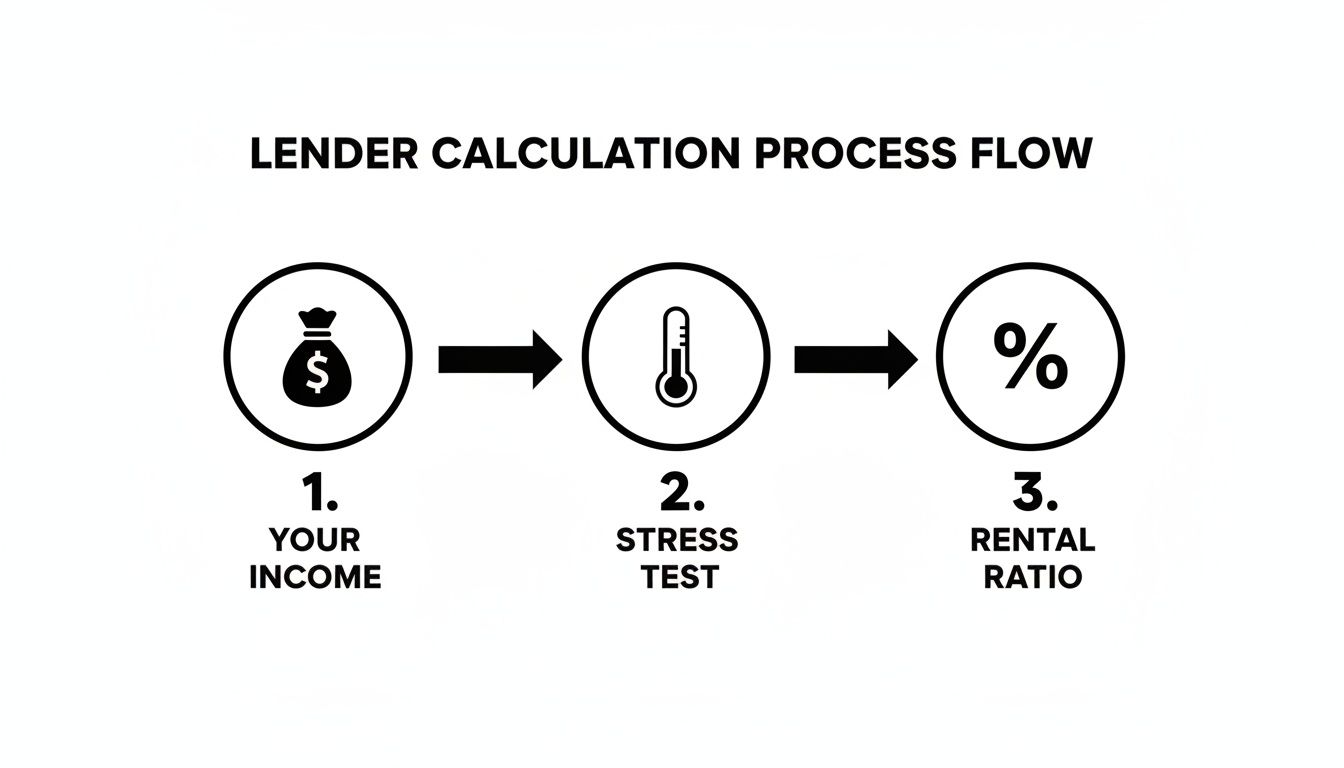

How Lenders Calculate Your Affordability

When you apply for a second-home mortgage, the lender’s primary concern is simple: can you genuinely afford this new commitment? They need to know you can service the loan even if interest rates climb or your circumstances change. This is determined through a methodical affordability stress test. Understanding this process allows an investor to evaluate a potential deal through a lender’s eyes.

Here is a breakdown of the steps a lender takes when assessing your application.

The process starts with your verifiable income, subjects it to a rigorous stress test, and then applies rental income rules (if applicable) to determine the final loan amount.

The Financial Stress Test Explained

A stress test is a financial simulation. Lenders are not just interested in whether you can afford the mortgage at today's rates. They need to ascertain if your finances can withstand a significant future increase in rates.

This is a mandatory part of the process for lenders regulated by bodies like the UK's Financial Conduct Authority. They will typically add a "buffer" of several percentage points on top of their standard variable rate or a benchmark rate. If your income cannot cover the mortgage payments at this higher, "stressed" rate, the application is unlikely to proceed.

These affordability checks are a cornerstone of UK second home mortgage requirements. For buy-to-let properties, lenders often need to see that you could afford repayments at rates of 5.5% or higher, regardless of the initial product rate. This is why having strong, provable income is so vital.

The Importance of Rental Coverage

For any property you intend to let, the calculation has another layer. Here, the focus shifts to the property’s ability to generate sufficient income to service its own debt. This is measured using a rental coverage ratio.

Lenders will usually insist that the gross annual rental income is between 125% and 145% of the yearly mortgage payments, calculated at their higher, stressed interest rate. This ensures the rent does not just cover the mortgage but also leaves a buffer for tax, insurance, maintenance, and potential void periods.

For instance, if the stressed monthly mortgage payment works out to be £1,000, the property would need to generate a rental income of at least £1,250 to £1,450 per month to satisfy the lender. This demonstrates a positive return on investment (ROI) from a cash flow perspective, which is critical for securing finance.

Factoring in All Your Commitments

Finally, lenders will assess the complete financial picture. The affordability check is not performed in isolation; it takes all your existing financial responsibilities into account.

This means they will analyse:

- Your primary residence mortgage: The outstanding balance and monthly payments are key figures.

- Other debts: This includes everything from car loans and personal loans to any outstanding credit card balances.

- Household expenditure: Lenders will use Office for National Statistics (ONS) data or your own declared spending to estimate your day-to-day living costs.

By adding the stress-tested mortgage payment to all your other outgoings, lenders build a comprehensive view of your financial capacity. They will only approve your application once they are satisfied you can comfortably manage everything with a healthy margin to spare. Our guide to financing an investment property explores this process in more detail.

Comparing International Mortgage Requirements

Securing a mortgage for a second home is not a universal process; regulations and lender appetite shift dramatically from one country to the next. Understanding these differences provides a significant strategic advantage, helping you identify markets where your financial profile is most likely to secure approval.

Established vs. Emerging Markets: A Comparative Look

Lender requirements often differ starkly between established markets like the UK or Germany and popular emerging or lifestyle markets such as Portugal, Turkey, or parts of Southeast Asia.

Established Markets (e.g., UK, Germany):

- Focus: Highly regulated, data-driven, and risk-averse. The emphasis is on verifiable income, credit history, and stress testing.

- Requirements: Lower deposits (typically 25%) are possible, but affordability tests are stringent. For a UK buy-to-let, the rental stress test (125-145% coverage) is the primary hurdle. According to Gov.uk data on property transactions, this strict lending environment helps maintain market stability.

- Investor Takeaway: Success depends on a clean financial record and demonstrating positive cash flow under stressed conditions. Yield is king.

Emerging & Lifestyle Markets (e.g., Spain, Portugal, UAE):

- Focus: More emphasis on the asset itself and the size of the investor's deposit. Affordability checks can be less formulaic.

- Requirements: Higher deposits are standard, often 30-40% for non-residents. Lenders are more interested in your overall net worth and the source of your funds, as a way to mitigate their risk. Local housing authorities often have different rules for foreign nationals.

- Investor Takeaway: A larger capital outlay is your entry ticket. Demonstrating significant net worth can be more persuasive than income alone. For example, before its recent changes, Spain's Golden Visa program linked residency directly to property investment, shaping lending attitudes.

The USA: A Data-Centric Approach

The American lending market is defined by its focus on credit scores and DTI ratios. For international buyers, the requirements are transparent but can be difficult to meet without a US financial footprint.

A non-resident buyer in the US will likely need a deposit of 30% or more. Lenders will meticulously calculate your global DTI ratio, which must typically remain below 43%, including the new mortgage. Building a US credit file or working with a specialist lender familiar with international credit is vital for success.

For a clearer perspective, our guide on investing in overseas property provides further context on navigating these diverse markets.

International Mortgage Requirements: A Snapshot

| Country/Market Type | Typical Non-Resident Deposit | Key Affordability Test | Investor Takeaway |

|---|---|---|---|

| United Kingdom | 25-30% | Rental income stress test (125-145% coverage at a higher rate). | Focus on property yield and verifiable income. |

| Spain & Portugal | 30-40% | Overall income and net worth assessment. | A higher deposit is the key to unlocking finance. |

| United States | 30%+ | Strict Debt-to-Income (DTI) ratio and credit score analysis. | Data is paramount; a US financial profile is a major advantage. |

| Emerging Markets | 40-50% | Asset quality and large deposit. | Higher risk for lenders means higher capital entry for investors. |

Your Essential Documentation Checklist

A successful mortgage application is built on a flawless paper trail. For international investors, presenting a clear, organised set of documents is the single best way to overcome a lender’s inherent caution and secure an approval. Delays are most often caused by missing information or a poorly organised file.

Your application is a business case for yourself as an investable proposition. This checklist breaks down exactly what you will need, helping you meet the stringent second home mortgage requirements with confidence.

Proof of Identity and Address

This section is foundational. Any ambiguity causes delays.

- Proof of Identity: Certified copies of your valid passport are required. Some lenders will also ask for your residency permit or visa for your country of residence.

- Proof of Address: Lenders typically require two recent utility bills (e.g., council tax, electricity) or bank statements, dated within the last three months, showing your name and current address precisely as it appears on the application form.

Verifying Your Income

This is where lenders scrutinise your finances, especially if your income originates from outside their home country. Your goal is to make your earnings exceptionally easy to understand and verify.

For employed applicants:

- Your last three to six months of payslips.

- Your most recent annual tax summary (e.g., P60 in the UK, W-2 in the US).

- A formal letter from your employer on headed paper, confirming your role, salary, and employment duration.

For self-employed investors or company directors:

- Two to three years of finalised accounts, prepared by a chartered or certified accountant.

- Corresponding personal and/or business tax returns for the same period. For UK applicants, these are your SA302 tax calculations and tax year overviews from HMRC.

- For international entrepreneurs, a summary letter from a recognised chartered accountant explaining your earnings can add significant credibility.

Demonstrating Your Deposit and Funds

Lenders must verify not only that you have the deposit, but also its origin. This is a non-negotiable part of their anti-money laundering (AML) checks.

Be prepared to provide six to twelve months of bank statements for the account holding your deposit. These statements must show the funds accumulating over time or arriving from a legitimate source, such as savings, the sale of another asset, or an inheritance. A large, unexplained cash deposit is a major red flag.

For global investors, it is critical that any documents not in the lender’s native language are professionally translated and certified. Presenting your foreign income in a clear, lender-friendly format—often converted to the local currency—demonstrates you are a serious, organised borrower. It is also wise to understand the local tax implications of your purchase. You can learn more about how to understand property taxes for your investment in our detailed guide.

Strategies to Strengthen Your Mortgage Application

Securing a mortgage for a second home is not just about meeting criteria; it is about presenting a compelling case that positions you as a low-risk, well-prepared applicant. A strong application not only increases the likelihood of approval but can also lead to better interest rates and more flexible terms.

These strategies are designed to proactively address the specific concerns a lender will have when assessing an application against second home mortgage requirements.

Prepare Your Financial Foundations

Lenders demand a clear, stable financial picture. Your records must tell a simple story of fiscal responsibility and planning. A disorganised or complex financial history creates doubt, which often leads to rejection.

Begin by organising your bank statements well in advance. Lenders will scrutinise three to six months of statements to analyse your cash flow and verify the source of your deposit. In the period leading up to your application, avoid large, unexplained transactions or utilising overdrafts, as these are immediate red flags.

The objective is to present a clean, consistent financial narrative. A lender wants to see a predictable pattern of income and expenditure, demonstrating that you manage your money responsibly and live well within your means.

Exceed the Minimum Requirements

Meeting a lender's minimums is merely the price of entry. To distinguish your application, you should aim to exceed them, particularly regarding your deposit and existing debt levels.

- Boost Your Deposit: While 25% may be the minimum deposit, increasing this to 30% or more dramatically lowers the lender's risk (LTV). This demonstrates significant financial commitment and often results in a lower interest rate, yielding substantial savings over the life of the loan.

- Reduce Your Debts: Before applying, make a concerted effort to pay down high-interest, non-mortgage debts like credit card balances or personal loans. A lower DTI ratio provides more headroom in the lender’s affordability calculations, making it much easier to pass their stress tests.

Partner with a Specialist Broker

Navigating the second home finance market is complex, especially for international transactions. High-street lenders often lack the expertise or risk appetite for foreign income streams or overseas credit histories. A specialist mortgage broker is your most valuable asset in this scenario.

A broker who focuses on second homes or expatriate mortgages has established relationships with lenders who are comfortable with these more intricate deals. They understand which institutions are most likely to approve your application and can package your financial profile to meet their specific criteria. Their expertise is invaluable for overcoming the hurdles that often derail international investors. For a wider perspective on the investment landscape, our beginner's guide to real estate investing offers a solid foundation.

Your Questions Answered

When investigating finance for a second home, several specific questions frequently arise. Here are straightforward answers to some of the most common queries from global investors.

Can I Use Equity from My Primary Residence for the Deposit?

Yes, releasing equity from your main home via a remortgage is a common strategy for funding a deposit. However, lenders will scrutinise this thoroughly. They will recalculate the loan-to-value (LTV) on your primary residence and re-run your affordability assessment. Your income must now comfortably cover the larger mortgage on your main home in addition to the new loan for the second property.

How Does the Property's Intended Use Affect the Mortgage?

The intended use is a critical factor, as lenders assess risk differently for each scenario.

- Buy-to-Let: For a long-term rental investment, the lender's primary focus is the property's rental yield. They will require the projected rent to cover 125% to 145% of the mortgage payment, calculated at a "stressed" interest rate. The investment must demonstrate its own financial viability.

- Holiday Let: For short-term lettings, lenders assess a combination of your personal income and the property’s projected seasonal earnings. This is a specialist lending area, and criteria vary significantly.

- Personal Second Home: If the property is solely for your own use, there is no rental income to consider. Affordability is based entirely on your personal salary and existing financial commitments.

A £400,000 holiday home for personal use requires you to prove you can afford the entire mortgage from your income alone. If the same property were a buy-to-let investment, the lender would focus more on the rent it could generate to service the debt.

Do I Need a Specialist Solicitor for an International Purchase?

Yes, this is non-negotiable. You require a solicitor who specialises in the property laws of that specific country and is completely independent of the seller or estate agent. An experienced international property lawyer will be fluent in both English and the local language, can identify red flags in legal documents, and understands the rules around foreign ownership, local taxes, and the mortgage process. They are your most critical safeguard in an overseas transaction.

At World Property Investor, we provide the in-depth analysis and data-driven guides you need to make confident investment decisions across the globe. Explore our insights and find your next opportunity at https://www.worldpropertyinvestor.com.