TL;DR: In 2025, the average monthly cost living in Dubai for a single person, excluding rent, is 4,150 AED (£880). Add a one-bedroom city centre rent of 8,333 AED, and typical total monthly living costs rise to around 12,500 AED (£2,650), based on Numbeo’s Dubai cost of living data.

Most advice on Dubai affordability gets the investor question wrong. It treats living costs as a relocation checklist for residents, when in practice they’re one of the cleanest ways to judge rental depth, tenant resilience, and the rent ceiling your asset can realistically support.

If you buy a flat in Dubai without understanding what your target tenant can spend after groceries, transport, utilities and housing, you’re not underwriting an investment. You’re guessing. The useful lens isn’t whether Dubai is “cheap” or “expensive”. It’s whether a given tenant profile can absorb your rent comfortably enough to stay, renew, and keep arrears risk low.

Rethinking Dubai's Affordability for Property Investors

Dubai is often marketed as a luxury market first and an investment market second. That framing is too blunt. For landlords, the more important point is that Dubai combines high-end global-city positioning with living costs that are lower than many buyers assume.

According to April International, Dubai ranks as the 15th most expensive city globally, yet its cost of living is 35% cheaper than New York City and 22% less expensive than average US cities. The same source also places the average monthly cost for one person at $2,229, with housing typically accounting for 30-40% of income. That gap between reputation and reality is what creates the affordability story many investors miss when they assess tenant demand through headlines alone, as outlined in April International’s Dubai cost guide.

Why affordability matters more than headline rent

A buy-to-let investor doesn’t earn a return from average rent alone. Return comes from sustainable rent, sustained occupancy, and a tenant base broad enough to support leasing even when market sentiment shifts.

That’s why cost living in dubai matters beyond relocation planning:

- Tenant affordability sets the rent ceiling. If your unit targets young professionals, your pricing has to fit around their full monthly burn, not just salary.

- Neighbourhood choice changes demand quality. Areas that reduce commuting and daily spend can hold stronger renewal demand even if they’re not the most prestigious.

- Lower living costs widen your demand pool. A city that feels attainable to internationally mobile renters usually supports more consistent leasing activity.

Investor lens: Living-cost analysis is demand analysis. It tells you not only what tenants can pay, but what compromises they’ll accept on location, size and finish.

The practical takeaway for global buyers

For a UK investor, the key comparison isn’t Dubai versus London on headline prestige. It’s whether Dubai offers a stronger combination of tenant affordability and landlord pricing power.

That’s where the market becomes interesting. If a city can attract residents who perceive it as offering premium amenities at a more manageable cost base than London or New York, landlords gain room to position stock well without relying purely on luxury branding. In plain terms, a tenant who feels they’re getting better value is more likely to tolerate rent at the upper end of that neighbourhood’s viable range.

The result is a useful paradox. Dubai can look expensive from the outside while still being affordable enough, relative to global peers, to support active rental demand. For investors, that’s not a lifestyle footnote. It’s part of the return model.

Analysing Accommodation Costs and Rental Yields by Neighbourhood

Housing is the largest line item in any Dubai budget and the largest single variable in your buy-to-let model. The city doesn’t operate as one rental market. It operates as a series of micromarkets with very different affordability bands, and that’s where capital allocation decisions become sharper.

The most important split is between central and outer-centre stock. According to DMCC, one-bedroom apartments in city centre locations average AED 8,700 per month, while comparable units outside the centre average AED 5,365.79, a 38.3% differential. Purchase pricing shows the same pattern. City centre property averages AED 2,471.83 per square foot, versus AED 1,381.26 outside the centre, a 44% variance, based on DMCC’s expat cost of living analysis.

The central versus outer-area investment trade

Prime areas usually win on branding, tenant prestige and liquidity. Outer areas often win on capital efficiency. DMCC’s data takes this further by noting that outer-area properties generate rental yields of approximately 4.7%, compared with 5.2% in central locations, despite requiring 44% lower capital deployment.

That matters because investors often overpay for centrality without checking whether the yield premium is proportionate. In Dubai, the numbers suggest a more nuanced picture. Prime stock gives you somewhat stronger yield and usually stronger address value, but the capital hurdle is materially higher. If your objective is portfolio diversification or faster scaling, outer areas can be the more rational entry point.

Prime addresses can support pricing power. Lower-cost districts can support faster portfolio building. They aren’t the same strategy, and they shouldn’t be judged by the same metric.

A practical rental yield snapshot

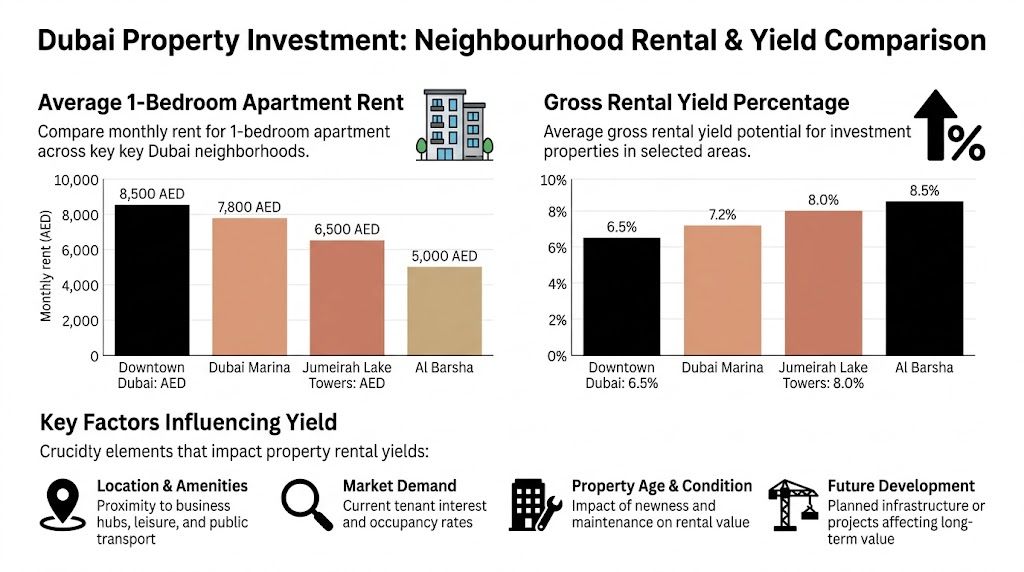

The infographic below uses neighbourhood examples to show how rent and yield can vary within Dubai. Treat these figures as area-level indicators rather than direct substitutes for city-wide averages.

| Neighbourhood | Average Monthly Rent (AED) | Average Purchase Price/sq ft (AED) | Estimated Gross Rental Yield |

|---|---|---|---|

| Downtown Dubai | 8,500 | Higher-priced prime stock | 6.5% |

| Dubai Marina | 7,800 | Prime waterfront pricing | 7.2% |

| Jumeirah Lake Towers | 6,500 | Mid-market urban pricing | 8.0% |

| Al Barsha | 5,000 | More budget-led stock | 8.5% |

These neighbourhood-level yield examples are useful as directional benchmarks, but your underwriting should still run through a proper model. A simple way to stress-test headline rent against acquisition cost is with a rental yield calculator for investment property.

How to read the table like an analyst

A common mistake is to chase the highest published gross yield. Gross yield is only one layer of the decision.

Use the table to ask better questions:

- Downtown Dubai: Can you justify the higher entry price through stronger tenant profile, lower vacancy risk, or resale demand?

- Dubai Marina: Does the balance of recognisable location and solid yield make it a better compromise than the absolute prime core?

- Jumeirah Lake Towers: Does the combination of accessible rent and strong yield broaden the tenant pool enough to reduce leasing friction?

- Al Barsha: Are you comfortable with a more budget-driven tenant base if the headline yield is stronger?

Family stock creates a different angle

DMCC also highlights a useful family-market dynamic. Three-bedroom apartments outside the centre average AED 11,320 per month, while monthly living costs for a family of four excluding rent range from AED 11,137 to AED 14,594. That creates an operational insight for landlords. A furnished three-bedroom unit in an outer area can be positioned as a convenience product for families trying to control total monthly outgoings.

The same source notes that investor-operators may be able to command a 15-20% premium positioning on all-inclusive furnished family rentals while still remaining competitive for tenant acquisition. That doesn’t mean every furnished unit deserves a premium. It means convenience becomes monetisable when the tenant is managing a full household budget rather than just a single-bedroom rent.

In practice, neighbourhood selection comes down to what you’re optimising for. Prime districts suit investors who value address strength and broader international appeal. Emerging and outer-centre districts suit investors who want lower capital exposure and stronger efficiency per dirham invested. The right answer depends less on city-wide averages and more on which tenant you intend to serve.

Building the Complete Expat Budget A Tenant's Perspective

Investor returns in Dubai are set by tenant maths before they are set by asking rents. A unit can look attractively priced against nearby listings and still underperform if the tenant’s all-in monthly budget is too tight to support renewals.

As noted earlier, Numbeo estimates monthly living costs in Dubai at 4,150 AED (£880) excluding rent for a single person and 14,594 AED (£3,100) for a family of four excluding rent. Once rent is included, typical monthly totals rise to around 12,500 AED (£2,650) for a single person and 30,887 AED (£6,550) for a family. For an investor, those figures are more useful as budget ceilings than as lifestyle trivia.

What a single professional can usually absorb

For one-bedroom stock, the single professional remains the key demand pool. The underwriting question is simple. How much of that tenant’s monthly income and spending capacity will your unit consume after rent, utilities, transport, and daily living costs are added together?

Mayak Real Estate’s 2025 budgeting breakdown offers a practical reference point. It puts a single resident’s total monthly outgoings at 11,500 AED, including 8,500 AED for rent, 600 AED for utilities, 1,200 AED for groceries, 400 AED for transport, and 800 AED for leisure. That matters because a one-bed priced close to that rent line has little margin for service inconsistency, long commutes, or recurring maintenance issues.

The implication for buy-to-let investors is straightforward. In buildings targeting professionals, tenant retention often depends less on squeezing an extra few hundred dirhams from headline rent and more on keeping the occupier’s full monthly cost predictable. A better-managed building can protect yield by reducing void risk.

A useful operational reference is this guide to apartment AMC costs and expectations for tenants and owners. It gives context on maintenance and common-area issues that regularly affect tenant satisfaction after move-in.

Couples and families change the budget equation

Couples usually do not behave like two single tenants sharing one unit. They tend to pay more for layout, finish, parking, and convenience if that choice lowers commuting pressure or improves day-to-day liveability. Mayak’s estimate of 18,800 AED total monthly for couples supports that pattern.

Family tenants are more disciplined. They assess rent as one line within a larger household budget that includes schooling, groceries, transport, utilities, and routine discretionary spending. That makes them less responsive to cosmetic upgrades and more responsive to practical value, including usable floor area, storage, access roads, and reliable building operations.

| Household type | Budget behaviour that matters to landlords |

|---|---|

| Single professional | Sensitive to one-bedroom rent, transport spend, and building reliability |

| Couple | More willing to pay for finish and location if the wider monthly budget still works |

| Family with children | Focused on stable total outgoings, space efficiency, and neighbourhood practicality |

That distinction affects ROI. A landlord targeting families can often accept a slightly lower headline yield if the asset sits in a location that supports longer tenancy duration and lower turnover costs.

How to convert tenant budgets into pricing decisions

A tenant budget should feed directly into your rent-setting model.

- Define the likely occupier. Price for a single professional, couple, or family, not for an abstract “Dubai tenant”.

- Map all-in monthly cost, not rent alone. Include utilities, transport, and normal living spend when judging affordability.

- Test renewal resilience. If your asking rent leaves the tenant with little room for other costs, expect more negotiation at renewal.

- Estimate ROI on net occupancy, not optimistic rent. A unit that lets faster and renews more often can outperform a higher-rent unit with more churn.

This is also where international benchmarking becomes useful. Investors comparing tenant affordability across gateway cities should review the cost to live in London for international residents and investors. London’s higher living-cost pressure often leaves less room between rent and disposable income, which helps explain why some Dubai neighbourhoods can sustain firmer occupancy and more resilient yields even when headline rents rise.

Uncovering Hidden Costs and Future Market Trends

Many overseas buyers still model Dubai deals on gross rent and purchase price alone. That isn’t enough. The biggest errors in underwriting usually come from costs that don’t appear in the marketing brochure.

The Housing Fee changes the real affordability picture

A critical ongoing expense in Dubai is the mandatory Housing Fee, which is equivalent to 5% of annual rent and is paid on top of utility bills. Engel & Völkers gives a simple example. A property renting at $2,000 per month adds an extra $100 per month through this fee, as outlined in Engel & Völkers’ Dubai cost guide.

For investors, the fee matters in two ways. First, it raises the tenant’s real occupancy cost beyond the advertised rent. Second, it can limit how far you can push asking rent before the all-in monthly cost becomes uncompetitive.

If you’re pricing against nearby stock, tenants won’t just compare rental listings. They’ll compare what leaves their bank account each month. A landlord who ignores that will often misread affordability.

Why gross yield can mislead

Gross yield is useful for screening deals. It’s weak for final decisions.

A sounder approach is to test whether your property still looks attractive after you account for the costs that shape tenant behaviour and net cash flow:

- Housing Fee exposure: Even if passed through operationally, it affects tenant affordability.

- Utilities and service expectations: They influence whether furnished or all-inclusive packaging makes sense.

- Maintenance burden: A cheaper acquisition with frequent issues can underperform a better-run asset.

- Renewal risk: High turnover erodes real returns through voids and reletting costs.

Practical rule: If a cost changes what the tenant can comfortably pay, it belongs in your underwriting model even if it doesn’t sit neatly in a gross-yield formula.

A related example in the verified data is that a £500,000 portfolio generating £50,000 in annual rental income would see £2,500 represented by a 5% fee if that cost is relevant to the occupancy structure. The broader lesson isn’t about the exact portfolio size. It’s that small percentage-based charges can materially change the ultimate outcome of return calculations.

Model affordability before you model growth

The video below is worth watching if you’re trying to think more critically about market positioning and operating assumptions in Dubai.

Future market trends matter, but no forecast rescues an asset bought on weak assumptions. A disciplined investor starts with the tenant’s all-in cost, then tests whether the property remains competitive if rents soften, incentives rise, or maintenance expectations increase.

That’s the difference between buying a marketed yield and buying a durable income stream.

Dubai Versus The World A Global Investment Benchmark

International investors don’t buy Dubai in isolation. They buy it instead of London, instead of New York, or instead of adding to an existing home-market portfolio. That means the right question isn’t whether Dubai is affordable on its own. It’s whether Dubai offers better value relative to other global cities competing for the same capital.

One of the clearest comparisons comes from the verified data on London. Mayak reports that one-bedroom city centre rent in London is 2,700 USD (£2,100) versus 1,800 USD (£1,400) in Dubai, and that Dubai offers 28% lower total costs, at 2,800 USD versus 3,960 USD. For an investor, that changes the yield conversation immediately. Lower tenant living costs can support stronger demand elasticity at a rent level that still looks attractive against acquisition pricing.

What this means for a UK investor

A UK landlord is used to mature-market constraints. High purchase prices, tighter rental margins, and tenants already carrying heavy living costs leave less room for error. Dubai’s appeal is that the city can still look globally aspirational while giving tenants a more manageable monthly equation than London.

That doesn’t automatically make every Dubai asset a better investment. It does mean the city deserves to be benchmarked on value, not on reputation.

Consider the contrast:

- London: Higher city-centre rent burden for the tenant.

- Dubai: Lower city-centre rent and lower total living costs in the verified comparison.

- Investor implication: A tenant who feels less financially stretched is often more resilient through lease renewals.

Established markets versus diversification markets

Established markets offer familiarity, legal depth, and easier emotional comfort for domestic investors. Diversification markets offer a different payoff. They may improve portfolio efficiency if they combine lower entry friction, broader tenant appeal, and stronger rental economics.

That’s why comparisons with other overseas destinations matter too. If you’re weighing Dubai against Europe for diversification, it helps to compare lifestyle-cost positioning alongside property economics. A useful starting point is this guide to the cost of living in Spain for property investors and expats.

Dubai’s strongest comparative argument isn’t that it’s the cheapest city. It’s that it can deliver global-city appeal without forcing tenants into the same level of cost pressure seen in some older markets.

The result is a market that often sits between the safety of established hubs and the upside of more flexible investment jurisdictions. For the right investor, that middle ground is exactly the point.

Strategies to Maximise Buy-to-Let Returns in Dubai

The best Dubai strategy starts with a simple discipline. Match the property to the tenant’s full cost structure, not just to market-wide rent averages. Investors who do that usually make better decisions on furnishing, neighbourhood selection and rent packaging.

Position the unit around the tenant, not your preferences

A one-bedroom in a well-connected district usually works best when it’s easy to occupy and easy to maintain. Professional tenants often value convenience more than excess fit-out. If the property is in a more family-oriented outer area, the value proposition shifts. Space, practical layout and operating simplicity matter more.

That means your decision on furnished versus unfurnished should be tactical:

- Furnished stock often suits mobile professionals and relocation-driven demand.

- Unfurnished stock may appeal more to longer-stay households who want control over their own setup.

- All-bills-included packages can make sense when convenience is part of the product and the pricing remains competitive on all-in monthly cost.

Price from affordability ceilings, not from optimism

The numbers discussed earlier give you a framework for setting rent with discipline. If a tenant segment already carries significant non-rent living costs, aggressive rent setting can shorten tenancy length even when the first lease is achieved.

A stronger method is to work backwards:

- Choose the target tenant profile.

- Assess what that profile is already spending on non-rent life costs.

- Decide whether your unit saves time, commute cost, or hassle.

- Price for renewal strength, not only for first-year headline income.

Buy where the strategy fits your capital

There isn’t one “best” Dubai district for all investors. Prime areas may suit buyers who want recognisable locations and broader resale appeal. More affordable districts may suit landlords who want stronger capital efficiency and room to scale.

If you’re still narrowing your market-entry plan, this guide on how to invest in Dubai real estate as an international buyer is a useful next step.

In practical terms, returns improve when the product, the tenant and the neighbourhood all match. Most underperformance in buy-to-let doesn’t come from choosing the wrong city. It comes from choosing the wrong unit for the wrong tenant at the wrong price.

Frequently Asked Questions for Dubai Property Investors

Is Dubai actually affordable enough to support long-term rental demand

Usually, yes, but affordability in Dubai is not uniform. That distinction matters more to investors than the headline question itself.

Rental demand stays durable when a unit fits the spending limits of a defined tenant group after transport, utilities, schooling, and day-to-day living costs are accounted for. In practice, Dubai supports several demand pools at once: price-sensitive renters looking for efficient commutes, professionals paying for convenience, and households willing to spend more for space or school access. For a landlord, that means affordability should be tested at neighbourhood level, not city level.

Should I focus on city-centre property or outer-area property

Choose based on income strategy, not prestige.

Central districts often attract tenants who will pay a premium for shorter travel times, recognisable addresses, and a denser amenity base. Outer districts can produce better capital efficiency because entry prices are lower while demand remains broad among tenants managing tighter monthly budgets. The better question is whether your expected rent is supported by the full cost of living in that area. A lower-rent district can outperform on yield if purchase price discipline is stronger and tenant turnover is lower.

Does tenant budgeting really affect ROI that much

Yes. It affects yield through renewal rates, vacancy periods, and pricing power.

A tenant does not judge rent in isolation. They judge the all-in monthly cost of occupying the property. If commuting costs are high, utility bills are difficult to predict, or neighbourhood spending is consistently above their comfort level, renewal risk rises. That has a direct effect on net income, even if the initial lease is signed at a strong headline rent.

Are furnished rentals worth it in Dubai

Only if the target tenant values immediate usability enough to cover the extra cost.

Furnished units often work best for newly arrived expatriates, corporate tenants, and renters who expect flexibility. In those segments, furniture can support faster leasing and a higher asking rent. In longer-stay family markets, the premium may be limited, and replacement costs can erode the gain. The test is simple. Compare the extra rent you can realistically achieve against furnishing, maintenance, and refresh costs over the expected holding period.

What’s the most overlooked cost in Dubai rental analysis

Tenant-side occupancy costs are often underestimated, especially the Housing Fee and recurring setup or service-related charges.

Tenant affordability sets a ceiling on sustainable rent. A unit may appear attractive on gross yield, yet still face resistance if the tenant’s monthly outgoings are already stretched by charges beyond base rent. Investors who model only purchase price and headline rent often misread where pricing pressure will emerge first.

How should I benchmark a Dubai deal against my home market

Use one framework across both markets and compare net outcomes, not familiar narratives.

Assess the relationship between acquisition cost and rent, the likely tenant profile, the stability of that tenant base, and the all-in occupancy cost from the renter’s perspective. Then stress-test vacancy and renewal assumptions the same way in each market. This guide on how to calculate return on investment for property is a practical method for standardising that comparison.

Is Dubai better suited to first-time international investors or experienced landlords

It can suit both. The advantage differs.

First-time buyers are often drawn to Dubai because the product is easy to understand and tenant demand is visible across multiple neighbourhoods. More experienced landlords usually find the stronger opportunity in pricing inefficiencies between submarkets, building types, and tenant segments. In both cases, returns depend less on broad confidence in Dubai and more on whether the unit is matched to a tenant budget that can hold through renewals.

What’s the main mistake overseas buyers make when assessing cost living in dubai

They treat cost living in dubai as background reading rather than as a core input in underwriting.

Living-cost data should shape rent assumptions, neighbourhood selection, and unit type. A studio aimed at a mobile professional has a different affordability ceiling from a two-bed aimed at a school-age family, even within the same district. The key insight is simple. Cost-of-living analysis helps investors identify where demand is deepest, where rent growth is more defendable, and where income is more likely to prove resilient if tenant budgets tighten.

If you’re comparing Dubai with other international markets, World Property Investor publishes detailed country and city guides, rental yield breakdowns, and practical buying analysis to help you research deals with more confidence.