Spain’s living costs are materially below the UK’s, and that gap has direct implications for residential property returns.

For a UK investor, the relevant question is not whether Spain feels cheaper on holiday. It is whether a lower local cost base can support rent collection, reduce void risk, and protect net yield after operating costs. Cost of living affects all three. In markets where tenants spend less on transport, food, and household bills, rent usually sits within a more sustainable share of income. That can improve payment reliability and length of stay, especially in mainstream long-let stock rather than purely seasonal product.

This is also why broad national averages need careful handling. A low-cost profile helps only when purchase prices have not already fully priced in that advantage. Malaga, Madrid, Valencia, and Alicante may all look attractive to British buyers, but the investment case differs once local wages, achievable rents, service charges, and acquisition costs are tested together. Cheap daily life does not automatically produce strong ROI. It often produces better results in cities where affordability still supports tenant demand and where entry prices remain disciplined.

Viewed properly, cost of living in Spain is a core underwriting variable. It influences tenant quality, the ceiling for rent growth, and the margin between gross income and recurring ownership costs. The same framework is useful when comparing Iberian markets, particularly this analysis of the cost of living in Portugal, where similar lifestyle appeal can lead to very different yield outcomes for a UK buyer.

Analysing Spain's Cost of Living for Property Investment

Spanish households typically devote a smaller share of monthly spending to housing than households in the UK. For a property investor, that is not a lifestyle detail. It indicates greater rent tolerance and lower tenant financial stress, particularly in long-let markets where steady occupancy matters more than chasing peak seasonal pricing.

That point changes how Spain should be underwritten.

A lower everyday cost base can improve rental performance in three ways. First, tenants have more capacity to absorb rent increases before arrears risk rises. Second, landlords face a lower local service-cost base for cleaning, maintenance coordination, and routine household spend in furnished stock. Third, lower living costs can widen the gap between what a tenant can sustainably pay and what an investor needs to hit a target yield. That margin is where resilient buy-to-let models are built.

The catch is that affordability on its own does not create returns. It only helps when local incomes, employment depth, and purchase prices line up with the rent level you need. A cheap city with weak tenant demand can still produce poor cash flow. A more expensive city can outperform if wage levels, occupancy, and exit liquidity are materially stronger.

What investors should read into the affordability gap

For UK buyers, Spain’s cost structure is most useful as a screening tool. If a market combines moderate living costs with diversified employment and disciplined entry pricing, the result is usually stronger tenant quality and lower void risk. That tends to support better net yield than a superficially cheaper location where tenants are more price-sensitive and rent growth hits a ceiling quickly.

This is why regional selection matters more than the national average. Valencia, Alicante, Malaga, and Madrid all sit within the same country-level affordability story, but the investment case differs sharply once you test achievable rent against purchase price and local salary realities. Investors comparing Iberian options should also look at how the cost of living in Portugal affects rental yields, because similar lifestyle appeal can mask very different affordability and return profiles.

Key takeaway: Spain becomes more attractive when lower living costs translate into sustainable rents, lower arrears risk, and operating margins that still hold up after tax, service charges, and voids.

A Breakdown of Living Costs in Spain

Spain’s affordability story matters because tenant budgets set the upper limit on sustainable rent. For a UK investor, the national cost base is less a lifestyle footnote than a pricing framework for underwriting demand, arrears risk, and net yield.

Household costs and rent tolerance

As noted earlier, current national estimates indicate that monthly living costs for a single person are typically in a certain range excluding rent, and higher when including rent. For a family of four, these costs are also within specific ranges both without and with rent.

Those figures matter because they help define affordability bands before you analyse any individual city. If a local rental market already absorbs a large share of household income, rent growth becomes harder to sustain, even when tenant demand looks healthy on the surface. In practice, that tends to produce slower re-letting, more negotiation on renewals, and greater sensitivity to utility and transport costs.

National average rent has been cited as a certain monthly amount. That is a useful benchmark, but investors should treat it as a baseline rather than a target. In stronger urban markets, asking rents sit well above that level. The investment question is whether local incomes can support the premium without pushing tenants into financial strain.

Purchase pricing and the entry-cost advantage

As noted earlier, Spain’s housing market recently recorded double-digit year-on-year price growth, with average national pricing at a particular figure per square metre. For a UK buyer, the strategic implication is straightforward. Entry cost is often low enough to preserve yield potential, but only if rent demand is broad and repeatable.

That creates two workable investment theses:

| Investment stance | What the cost base supports |

|---|---|

| Income-first | Lower acquisition pricing can support stronger gross yield where rents are backed by stable local employment |

| Portfolio diversification | A lower cost per asset can reduce concentration risk and allow exposure to multiple Spanish micro-markets rather than one high-value UK unit |

Investors screening markets at this stage should compare affordability with pricing discipline, not just chase the cheapest square metre. A guide to the best countries for investment property is useful here because Spain competes well on entry cost, but regional execution still determines whether that headline advantage converts into cash flow.

If you are financing the purchase, debt costs can erase the margin quickly in lower-income tenant markets. A separate review of mortgage rates in Spain is useful before you commit to a debt-funded acquisition.

Salaries, inflation and tenant resilience

As noted earlier, Spain’s average net monthly salary falls within a specific range, while the minimum wage is a certain net monthly amount. That spread is one of the most useful national indicators for landlords.

A tenant base clustered near the lower end of the income range gives you less room for aggressive rent increases, even if your own purchase price looks attractive. By contrast, markets with a deeper mix of professional salaries usually support lower arrears risk and more predictable occupancy, despite higher headline living costs.

Inflation also matters, but its effect is uneven. Earlier figures indicated annual inflation at a low single-digit percentage in mid-2025, broadly in line with Spain’s longer-run pattern of similar annual increases. For investors, that suggests a relatively stable operating backdrop rather than an automatic case for sharp rent uplifts. Rent rises tend to hold where job creation, wage depth, and supply constraints reinforce them. They stall where tenants are already near their affordability ceiling.

Daily spending and operating margin

The same cost ranges noted earlier show that everyday spending in Spain remains moderate by UK standards. That has a second-order effect many private investors miss. It shapes the local service economy around the asset.

Lower day-to-day costs can improve margins on furnished lets and short-stay stock because cleaning, basic maintenance, consumables, and guest turnover costs often run below comparable UK levels. The benefit is most visible on smaller units, where operating expenses consume a larger share of gross rent.

Investor reading: Cost of living affects both sides of the model. It influences what tenants can pay and what it costs you to keep the property lettable.

What national averages can and cannot do

National figures help you test whether Spain fits your return requirements. They do not tell you which market within Spain offers the best combination of yield durability, tenant quality, and exit liquidity.

That distinction matters. A low-cost environment is only attractive if it supports reliable occupancy and a rent level that still leaves room after tax, service charges, maintenance, insurance, and financing.

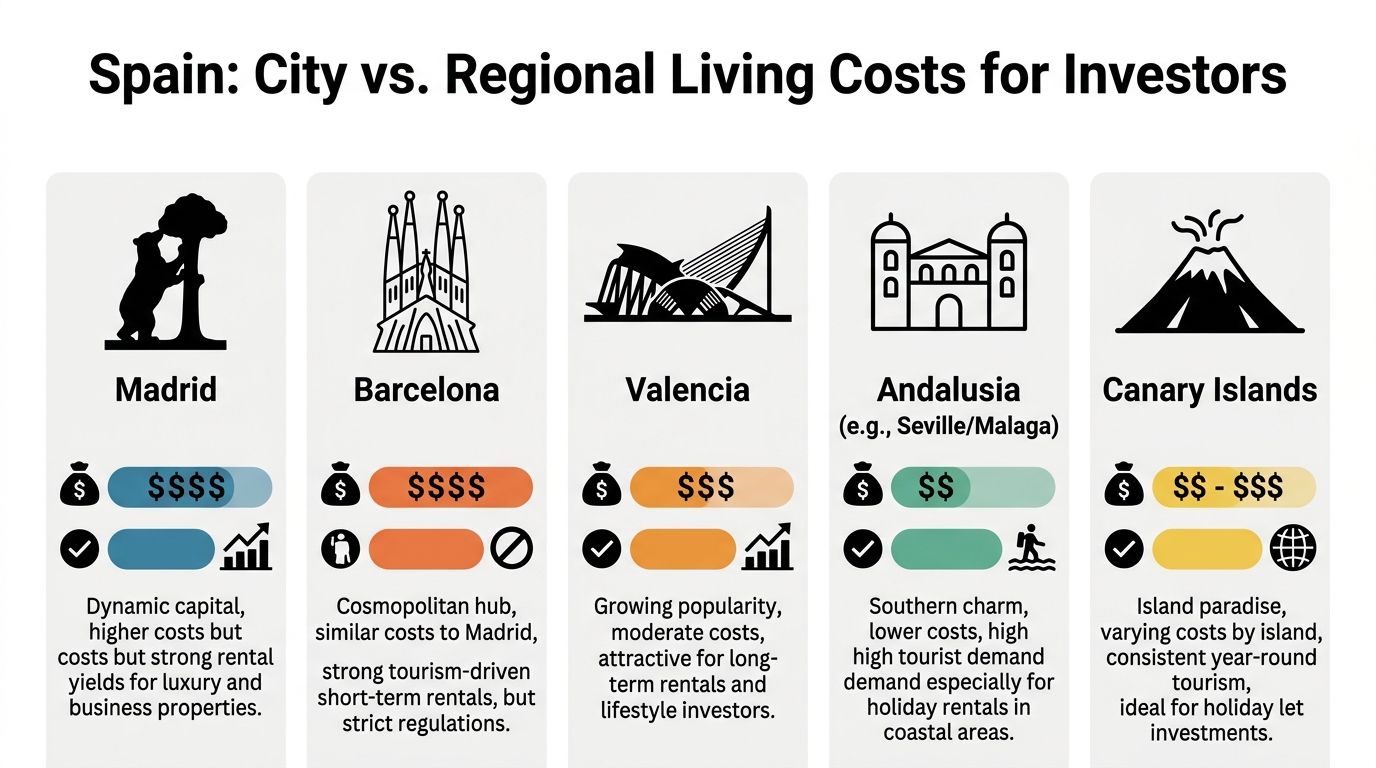

City and Regional Cost Analysis for Investors

A 1-point shift in gross yield often comes from geography rather than asset quality. In Spain, the spread between a high-entry gateway city and a lower-cost regional market can change the investment case more than a cosmetic refurbishment or a small rent review.

Spain works as a set of local affordability systems. Investors who use one national cost figure across Madrid, Valencia, Bilbao, Seville, and the islands usually misprice either rent risk or exit risk. The better approach is to read living costs as a market signal. They show how far rents can rise before tenant quality weakens, arrears risk increases, or demand shifts to cheaper districts.

Barcelona and Madrid as pricing leaders

Barcelona and Madrid set the benchmark for pricing pressure. Earlier data in this article showed property values in both cities reaching high figures per square metre, which puts them in a different underwriting category from most regional Spanish markets.

That matters because high acquisition cost changes the whole model. Investors need stronger tenant covenants, lower vacancy, and better resale liquidity to justify tighter initial yields. These cities can still work, especially for well-located units aimed at professionals, corporate tenants, or supply-constrained central districts. The margin for error is thinner.

The main advantage is market depth. Demand is diversified across domestic professionals, international residents, students, and in some submarkets tourism-linked occupiers. The constraint is affordability. Once rents absorb too much of local income, landlords rely more heavily on premium tenant segments and less on broad-based local demand.

Valencia as the balance play

Valencia often presents a cleaner income case for UK buyers. Rent levels remain meaningful, but entry pricing is generally less aggressive than in Madrid or Barcelona, which can leave more room in the model for service charges, maintenance, finance costs, and tax.

That combination tends to support steadier long-term rental strategies. A city does not need the highest headline rents to produce a better return. It needs a purchase price that has not already capitalised every positive story about lifestyle, climate, and inward migration.

For investors focused on standard residential lets rather than highly managed short-stay stock, Valencia often sits in the most investable part of the Spanish market. Demand is broad enough to support occupancy, but affordability is not under the same pressure as in the top two cities.

Bilbao, Galicia, and the wage-to-rent test

Regional analysis becomes more useful when you stop asking which city is cheapest and start asking which city gives tenants enough financial headroom to keep paying through slower economic periods.

For example, Galicia rents for a two-bedroom property average a certain monthly amount, while Bilbao salary levels were cited as significantly higher in the source used earlier in this article. Barcelona salary levels were cited as even higher, but that does not automatically make Barcelona the safer income market if housing costs absorb a larger share of earnings.

This is the key investor distinction. Absolute rent is less important than rent relative to local earning power. Markets with moderate rents and acceptable wage support can produce better occupancy durability than fashionable cities where tenants are close to their affordability limit.

| Market type | Income profile | Likely yield effect | Main risk |

|---|---|---|---|

| Primary city | Higher nominal salaries, broader tenant mix | Often lower initial yield because entry prices are high | Affordability pressure can cap rent growth |

| Secondary city | Balanced wages and living costs | Better chance of stable yield with fewer extremes | Demand pool is smaller than in Madrid or Barcelona |

| Regional market | Lower rents and lower cost base | Can improve gross yield on entry | Weaker resale liquidity and uneven tenant demand |

Andalusia and the margin question

Andalusia attracts investors for a different reason. The appeal is not only lower costs for residents. It is the way that lower local living costs can widen the tenant base for certain asset types, especially units aimed at retirees, remote workers, and value-driven domestic movers.

That can help occupancy, but only if the submarket has year-round demand. A low-cost city with thin winter demand or highly seasonal turnover can still underperform a more expensive urban market with stronger twelve-month occupancy. Investors should separate affordability from depth. They are related, but they are not the same variable.

Seville, Málaga, and selected coastal markets each sit in different parts of that equation. Seville may suit long-term income strategies better in some areas. Parts of Málaga may justify stronger rents, but acquisition cost and competition can reduce the spread between gross and net return.

Canary Islands and island economics

The Canary Islands require a different filter. Local wages matter, but visitor demand, second-home ownership, and operational intensity matter more than they do on the mainland.

That changes the role of cost of living in the model. On the islands, lower resident costs do not guarantee better buy-to-let performance. Investors need to test whether occupancy reliability, regulation, and management friction offset the extra complexity. In practice, island assets can produce attractive income only when owners control lettings, compliance, and seasonal volatility with discipline.

A practical market selection filter

UK investors should screen Spanish markets in this order:

- Check rent against local earning power. This is the best first test of tenant resilience.

- Assess entry price against realistic net yield, not headline rent. Expensive cities can still work, but the underwriting needs to be tighter.

- Separate broad demand from seasonal demand. A full August calendar does not prove a durable annual return.

- Test exit liquidity before purchase. Ask whether the likely buyer is another investor, a local owner-occupier, or an overseas lifestyle buyer.

While this regional analysis matters, comparing Spain with the best investment property markets globally gives useful strategic context.

Practical rule: The strongest Spanish market for a buy-to-let investor is usually the one where local households can still afford the rent, operating costs stay controlled, and the purchase price has not fully priced in future demand.

Sample Monthly Budgets and Lifestyle Implications

A rental market becomes investable when household budgets leave room after rent. In Spain, that is often the difference between a property that stays occupied and one that suffers churn, discounting, or payment stress.

For a UK investor, sample budgets are not lifestyle content. They are underwriting tools. They show which tenant groups can absorb rent increases, which markets depend on lower fixed costs to sustain occupancy, and which property formats match local spending power.

Sample Monthly Budgets in Spain 2026 Estimates

| Expense Category | Single Professional (Valencia) | Retired Couple (Malaga) | Family of Four (Madrid Suburb) |

|---|---|---|---|

| Rent | €750 to €1,150 | €900 to €1,400 | €1,300 to €2,000 |

| Food and groceries | €220 to €350 | €350 to €550 | €500 to €800 |

| Transport | €40 to €90 | €80 to €180 | €150 to €300 |

| Leisure and dining | €120 to €250 | €180 to €350 | €180 to €400 |

| Utilities and services | €90 to €160 | €130 to €220 | €180 to €300 |

| Estimated monthly total | €1,220 to €2,000 | €1,640 to €2,700 | €2,310 to €3,800 |

These ranges are estimates rather than quoted national averages. The point is not precision to the euro. The point is affordability headroom. A tenant with a €1,700 monthly budget behaves very differently from one already stretched at €1,650 before an electricity spike or annual insurance bill.

Persona one, the Valencia professional

This tenant usually optimises for total monthly cost, not floor area. A one or two-bed flat near transport can outperform a larger unit in a weaker micro-location because the occupier is buying convenience and budget control together.

That has a direct yield implication. Smaller, efficient stock often produces better rent per square metre, while also widening the tenant pool to younger professionals, remote workers, and couples without children. If the all-in monthly cost remains manageable, occupancy tends to be steadier and void risk lower.

Persona two, the Málaga retiree couple

This profile values climate, healthcare access, walkability, and predictable monthly outgoings. Retirees can be reliable long-stay tenants, but they are usually disciplined on price and less willing to absorb sharp rent increases when a coastal location attracts foreign demand.

For investors, that argues for practical units in established neighbourhoods rather than paying a premium for prestige addresses that compress net yield. In this segment, tenant quality often improves when the property reduces friction. Lift access, nearby services, and manageable utility costs matter as much as sea views.

Persona three, the Madrid suburban family

Families are often the clearest test of rental sustainability because their budgets are less flexible. Rent competes with food, commuting, school-related costs, and childcare.

That changes the investment case. A landlord targeting this segment should prioritise durable layouts, storage, transport links, and cost-efficient buildings over cosmetic upgrades. Families can support lower turnover and longer tenancy length, but only where monthly housing costs do not crowd out the rest of household spending.

Investor lesson: The best tenant profile is usually the one with the strongest residual income after rent, utilities, transport, and food, not the one with the highest headline income.

This budgeting lens also helps when comparing Spain with other lifestyle-led markets. A review of the cost of living in Malta shows how two destinations can attract similar overseas buyers while producing very different affordability profiles for year-round tenants.

Translating Living Costs into Your Investment Strategy

A Spanish rental can look cheap to a UK buyer and still be overpriced for its local tenant base. That gap sits at the centre of buy-to-let performance.

Local affordability sets the rent ceiling

The strategic question is not whether Spain is cheaper than the UK. It is whether the tenant segment in your chosen district can support the rent you need after food, transport, utilities, and other fixed spending.

HousingAnywhere’s Spain comparison makes the point clearly. The platform notes that Spain’s living costs are materially below the UK, while also warning that local salary levels constrain what many tenants can pay. For an investor, that distinction separates a market with sustainable rents from one where rents have outpaced local capacity.

This matters most in underwriting. A rent level supported mainly by foreign demand, seasonal workers, or short-stay visitors is less dependable than one supported by local incomes across a broad tenant pool.

Yield only matters if the rent is durable

A high gross yield can hide weak rental resilience. The more useful test is whether the rent remains affordable through slower wage growth, utility increases, and longer void periods.

Assess four points before you buy:

- Does the intended tenant still have healthy residual income after rent and basic living costs?

- Are service charges, utilities, and routine maintenance low enough to protect net yield?

- Does the pricing depend on international tenants rather than local wage support?

- Could the property still let on a standard residential basis if tourism weakens or regulation tightens?

A property that fails the final test belongs in a higher-risk bucket, even if the headline income looks strong.

Lower living costs can improve net operating performance

Spain’s lower day-to-day cost base can support better margins, but only in the right format. In practical terms, lower cleaning, transport, and routine household spending can reduce turnover pressure in furnished rentals and make long-term tenancies easier to sustain.

That does not automatically create pricing power. It improves retention and occupancy when the unit is positioned for a tenant who values predictable monthly costs. Buildings with efficient utilities, walkable services, and manageable community fees often outperform prettier stock with heavier running costs.

For UK buyers, this is also where tax discipline matters. A deal with modest rent growth can still produce strong total return if acquisition costs, operating friction, and capital gains tax on foreign property are modelled properly from the start.

Market type changes the investment case

Primary cities usually offer deeper demand, better liquidity, and a broader exit market. That tends to lower vacancy risk, but purchase prices can compress yield.

Secondary markets often work differently. Lower entry prices can produce a stronger income return, but only if local affordability is sound and employment demand is stable enough to support occupancy beyond a narrow seasonal window.

Cheap stock is not the same as productive stock.

The best opportunities often sit between those two extremes. A middle-income district in a liquid city can offer a better combination of tenant depth, reletting speed, and resale optionality than either a prime address or a very low-cost peripheral market.

Inflation and budget pressure

Moderate inflation does not remove tenant stress. It changes where the stress appears.

If utilities, food, or transport rise faster than wages, rent collection becomes more sensitive even in markets that still look affordable on paper. For landlords, that shows up in slower rent reviews, more negotiation at renewal, and weaker absorption of newly listed units at ambitious prices.

Three workable investment theses

Cost-of-living data is most useful when it feeds a specific strategy.

Income thesis

Target districts where local households can support rent without budget strain. In Spain, that usually favours practical flats in employment-led areas over premium stock priced for occasional lifestyle demand.

Lifestyle thesis

Target markets with demand from retirees, remote workers, and part-time residents who choose Spain because their budget stretches further. This can work well, but only if the asset still functions as a conventional let when discretionary demand softens.

Price arbitrage thesis

Use lower acquisition costs and a cheaper operating base to build cash flow that would be harder to achieve in many UK cities. This approach works best where low entry pricing is matched by reliable year-round demand, not just a low headline purchase figure.

The core principle is straightforward. Occupancy, arrears risk, and rent growth all improve when local living costs leave tenants with room in their monthly budget.

A UK Investor's Checklist for Maximising Returns in Spain

A good Spanish deal is usually won before completion. It is won in the way you screen costs, price the rent, and control operating friction.

Pre-purchase checklist

- Check local wage support: Compare your intended rent with the likely tenant base in that district. If the deal only works for a narrow premium tenant, know that upfront.

- Test the fallback use: If you are buying for holiday lets, ask whether the property still works as a standard residential rental.

- Review building efficiency: Lower utility burdens help both tenant retention and marketing appeal.

- Scrutinise service charges and recurring costs: A cheap purchase can become an average investment once recurring expenses appear.

Operations checklist for landlords

- Use local managers selectively: In tourism-heavy markets, responsive local management often protects reviews and occupancy.

- Keep furnishing practical: Durable furniture and easy-to-replace items usually outperform overdesigned interiors.

- Price for retention, not ego: A slightly lower rent with a stable tenant can outperform a higher asking rent with churn.

- Control utility exposure: If bills are included, track usage tightly. If they are excluded, make expected costs clear from the start.

Personal cost checklist for investors spending time in Spain

Some UK investors partly self-manage or spend extended periods on the ground. In that case, your own cost discipline matters too.

- Choose your base carefully: A lower-cost base city can reduce inspection and setup expenses.

- Bundle visits with supplier meetings: Lawyers, agents, builders, and administrators should be scheduled in the same trip.

- Use local banking and payment systems efficiently: Friction on transfers and admin can erode margin.

- Keep tax planning in view: Disposal and income structuring matter as much as entry price. This is especially relevant if you later review capital gains tax on foreign property.

Checklist principle: In Spain, cost control is not about being cheap. It is about keeping your property affordable to occupy and efficient to run.

What to avoid

Do not buy on national averages alone. Do not assume a famous city guarantees better returns. Do not model rent growth without checking whether the local tenant can pay it.

That discipline matters more in Spain because the market can look inexpensive from London while still being expensive for the household that has to rent your flat.

Final Verdict Is Spain a Cost-Effective Investment Market

Yes, but only for investors who read affordability correctly.

Spain’s lower cost base gives UK buyers a genuine advantage. It can reduce operating pressure, support stronger tenant retention, and open markets that look expensive in the UK but still make sense on a Spanish budget. That is the opportunity.

The risk sits in the same data. Lower local wages can cap rent growth, especially in markets where international demand has pushed pricing away from domestic earning power. That is why cost of living spain is not a lifestyle side note. It is a filter for yield quality.

The strongest Spanish investments usually sit where three factors meet. Purchase prices remain sensible, tenants can realistically afford the rent, and the property still works if market conditions change. Investors who underwrite Spain at that level tend to find better long-term value than those who buy on sunshine and headline cheapness alone.

Frequently Asked Questions for UK Investors

Does cost of living affect residency planning in Spain

Yes. Even where residency is not directly tied to a property purchase, living-cost assumptions affect whether your income, pension, or savings will support time in Spain comfortably. For investors who split time between the UK and Spain, realistic budgeting matters as much as visa paperwork.

Does Spain’s lower cost base automatically mean higher rental yields

No. Lower costs can improve net income, but yields still depend on purchase price, tenant affordability, occupancy, and the type of rental model used. A cheaper city can produce weaker returns if demand is thin or rent ceilings are low.

Are local salaries important if I plan to target foreign tenants

Yes. Foreign demand can help, but it should not be your only support. A property that works only for one narrow tenant group is usually more exposed when conditions shift.

Is Spain better for long-term lets or holiday lets

It depends on the market. Cities and suburbs with stable resident demand often suit long-term income. Coastal and island locations may suit short-term rentals, but they usually require tighter management and stronger regulatory awareness.

What should UK buyers pay most attention to after Brexit

Banking, mortgage access, legal process, tax treatment, and ongoing administration all deserve careful review. The practical burden is manageable, but it is higher than many first-time overseas buyers expect.

What is the single biggest underwriting mistake

Ignoring affordability at city level. A national average can tell you Spain is cheaper than the UK. It cannot tell you whether your target tenant in one district can sustain your target rent.

World Property Investor helps buyers compare global markets with practical guides on yields, taxes, buying rules, and long-term strategy. If you are weighing Spain against other international options, visit World Property Investor for research built around real investment decisions rather than lifestyle marketing.