A lot of UK investors arrive at Denmark the same way. They start with a shortlist of stable European markets, they like the idea of a transparent legal system and resilient tenant demand, and then they assume the tax side will look roughly familiar. It doesn’t.

The point that usually causes trouble isn’t the purchase process. It’s the ongoing holding cost. In Denmark, land tax isn’t a side issue. It is one of the main variables that can alter your net return, your cash flow planning, and even which district makes sense to buy in.

That matters most when you’re comparing a Copenhagen flat with a UK buy-to-let, or deciding whether a lower-yield core market is still worth holding for the long term. If you treat denmark land tax as a small annual line item, you’ll underwrite badly. If you treat it as part of the asset’s operating structure, you can analyse Danish deals with much more confidence.

Investing in Denmark A Balancing Act of Yield and Tax

A typical investor scenario looks like this. You’ve found a well-lented apartment in Copenhagen, you like the location, and on paper the market looks orderly compared with more volatile destinations. Then the Danish tax language starts appearing. Grundskyld, public valuation, municipal permille rate, provisional assessments, retroactive adjustments.

That’s where many otherwise capable buyers hesitate.

The practical issue isn’t that the system is impossible. It’s that it’s different enough from the UK model that standard shortcuts don’t work. A British investor is used to thinking in terms of acquisition tax, council-style annual charges, and income tax on rent. Denmark asks you to focus much more carefully on the land element of the asset and how the municipality applies its rate to that assessed value.

For investors browsing homes for sale in Copenhagen, this is the variable that often separates a solid long-term hold from an overestimated return.

Why this matters more than many buyers expect

Two properties can sit in the same city, attract similar tenants, and still produce different after-tax outcomes because the land component and local rate don’t behave in the same way. That isn’t unusual in Denmark. It’s built into the system.

Practical rule: Before you compare Danish opportunities by headline rent, compare them by assessed land value, municipality, and likely tax treatment.

The better way to look at denmark land tax is not as a penalty but as a design feature of the market. Denmark’s historical reforms moved taxation away from older feudal structures and towards valuation-based systems on land and property. The long-term consequence is a framework that tries to tax the site value without penalising improvements in the same way a broader property tax can.

That distinction matters for portfolio strategy. If you’re buying for long-term rental income, redevelopment potential, or land scarcity in strong urban locations, you need to understand how Denmark taxes the site itself. Once you do, the market becomes much easier to read.

Understanding Denmark's Dual Property Tax System

Denmark uses a dual property tax framework. If you miss that point, almost every later calculation becomes muddled.

One tax applies to the land. The other applies to the wider property value. Investors often hear both terms and assume they will both hit a rental property in the same way. Usually, that’s the wrong starting point.

The two taxes in plain English

Think of a property as two separate things. First, the plot itself. Second, the building sitting on it.

Grundskyld is Denmark’s land tax. It targets the undeveloped land component only.

Ejendomsværdiskat is the property value tax. It applies to the total property value including buildings.

That split is more than an academic distinction. In Denmark’s dual property tax framework, land tax targets only the undeveloped land component, while property value tax applies to the total property value including buildings. Rental properties are exempt from the property value tax and instead taxed on net rental profits, while land tax remains payable and deductible. Municipal boards use central statistical valuations every two years to support this system.

For a buy-to-let investor, that usually means Grundskyld is the recurring property tax you need to model most carefully.

Why buy-to-let investors should focus on Grundskyld

This is the part that clears up most foreign investor confusion. If you’re buying a rental property, you’re generally not looking at the same tax profile as an owner-occupier.

The owner-occupier may face the broader housing tax framework tied to occupation and property value. The landlord’s focus is different. The landlord still carries land tax, but rental profits are taxed through the income side instead.

That creates a specific incentive structure:

- Land remains taxable: You can’t ignore the recurring land charge just because the building is income-producing.

- Improvements aren’t taxed through Grundskyld: The tax targets the site value rather than the full improved asset.

- Deductibility matters: For commercial rental income, land tax can support after-tax efficiency because it is deductible.

- Location selection becomes sharper: A high-demand district may still disappoint if the land-value component weighs too heavily on cash flow.

Why Denmark set it up this way

Denmark’s land-tax history helps explain the logic. The system developed away from the old hardkorn tax, which was abolished in 1903, and shifted toward modern valuation methods based on capital land value and real estate value, according to the history of land valuation in Denmark. The 1922 National Land Value Tax Act introduced a 1.5 per thousand (0.15%) rate on capital land value and periodic valuations, and later reforms pushed the system toward taxing land rather than improvements.

For investors, the practical lesson is simple. Denmark wants the tax system to bear on the land itself, not punish every improvement made to the building.

A UK investor who treats Danish land tax like a rough equivalent of Council Tax will misread the deal. The Danish question is narrower and more specific. What is the assessed value of the land, and how will the municipality tax it?

What this means for underwriting

When I review Danish assets for international clients, I strip the analysis back to three tax questions early.

- Is the property owner-occupied or income-producing?

- What portion of the value sits in the land assessment?

- Which municipality controls the recurring rate?

If you answer those three points correctly, the rest of the denmark land tax analysis becomes manageable. If you skip them, you end up comparing assets on the wrong basis.

How Danish Land Tax (Grundskyld) Is Calculated

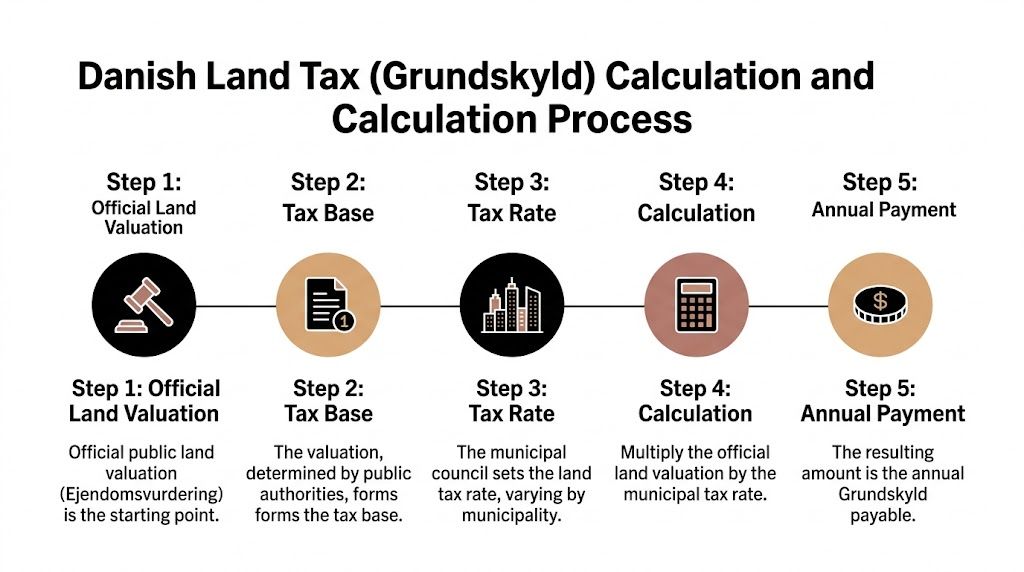

The calculation looks technical at first, but the moving parts are limited. In practice, most investors need to understand three inputs. The publicly assessed land value, the municipal permille rate, and the fact that the tax is paid semi-annually.

Denmark’s land tax is a semi-annual levy calculated as a permille rate of the publicly assessed land value, and municipalities set that rate within a parliamentary cap of 30 permille for 2024 to 2028, as outlined in the Danish tax overview at DLA Piper’s Denmark recurring taxation guide. The same guidance notes that annual taxable land value increases have been capped since 2003, but provisional levies for 2021 to 2023 based on delayed 2020 valuations are being recalculated, which can trigger retroactive adjustments. Investors should monitor Vurderingsportalen.dk for updates.

The three calculation inputs

Public land valuation

The first number is the official assessment of the land itself. This is not your purchase price and not your own estimate of market value. It is the public valuation used for tax purposes.

That public number matters because the tax is tied to the assessed land base, not to a landlord’s hoped-for rent.

Municipal permille rate

The second input is the local rate. Denmark expresses this as a permille rate, not a standard percentage. A permille is per thousand.

So if a municipality applies a rate of 10 permille, that means 10 per thousand of the taxable land value.

Payment structure and timing

Grundskyld is paid semi-annually. That matters for cash flow planning, especially if you’re holding through a period where provisional valuations are later corrected and the authority recalculates prior years.

A simple worked example

Use a hypothetical example rather than trying to memorise every local wrinkle.

Assume a Danish investment property has:

- An official land valuation

- A municipal Grundskyld rate

- A semi-annual payment cycle

The basic formula is:

Land tax = official taxable land value × municipal permille rate

If the municipality’s rate is expressed in permille, convert it into a per-thousand multiplier before calculating. Then divide the annual result into the normal payment schedule.

The key point is not the arithmetic. It’s which number you multiply. Foreign buyers often model land tax against total property price. That’s the wrong base. The Danish system works off the assessed land value, and the gap between land value and total value can materially alter the annual cost.

If you’re checking a deal quickly, don’t ask “What tax would this purchase price attract?” Ask “What land value has the authority assessed, and what rate applies in this municipality?”

Why municipal variation matters

Rates vary by municipality, and that creates real differences between otherwise similar investments. You should never assume one Danish city or borough works like another.

The same DLA Piper guidance notes that historical municipal ranges have been wide, and practical differences between municipalities can move effective costs enough to affect net yield assumptions. That’s why local due diligence matters more than country-level generalisations.

Here is a simple investor working table.

| Municipality | Indicative Land Tax Rate (Permille) | Commentary |

|---|---|---|

| Copenhagen | Municipality-specific | Check current local rate and valuation treatment before underwriting. |

| Aarhus | Municipality-specific | Don’t assume it mirrors Copenhagen or other major cities. |

| Odense | Municipality-specific | Useful for comparison when screening regional income opportunities. |

The table is intentionally conservative. Unless you have current municipal data for the exact asset, treat the rate as something to verify, not guess.

What often goes wrong in analysis

When investors build a quick spreadsheet, I usually see one of four errors.

- Using total purchase price instead of land value: This usually overstates or distorts the annual charge.

- Ignoring provisional valuations: That can leave a buyer exposed to later recalculation.

- Assuming one city’s rate applies nationally: It doesn’t.

- Treating Grundskyld as a minor operating expense: For some assets, it’s material enough to shift the hold decision.

This is also why deal analysis should sit alongside return modelling. If you’re testing a Danish acquisition, a proper investment property ROI framework should include the land tax as a recurring line item, not as a vague reserve.

The practical investor habit

The investors who handle denmark land tax well do something simple. They verify the official assessment early, confirm the municipality’s current rate, and stress-test what happens if the valuation changes or an adjustment arrives later.

That is more useful than chasing a generic “average Danish tax” figure, because there isn’t one number that tells you what your property will cost to hold.

The 2024 Reforms and Future Changes for Investors

The current Danish system can’t be understood properly if you’re still relying on pre-2024 assumptions. The rules now in force changed the holding-cost discussion, especially for buyers entering after valuations have started catching up with reality.

One reform matters more than most for investors. The 2024 housing taxation agreement eliminated the regulation ratio that had capped land tax hikes, and a Nationalbank analysis projected this would increase effective taxes by an average of 0.14 percentage points on single-family homes. The same analysis has been cited alongside 8% Copenhagen appreciation in 2025, which underlines the risk that rising land values can feed into higher holding costs for new entrants, as discussed in Nationalbank’s housing taxation agreement analysis.

What changed in practical terms

For years, many investors got used to the idea that Denmark was stable and predictable enough that tax changes would move slowly. There is still a lot of truth in that. But stable doesn’t mean static.

Removing the old cap mechanism changes how you should think about entry timing. A new buyer in 2026 isn’t stepping into the same tax environment that shaped legacy returns for long-term owners.

That matters because established owners may already have benefited from earlier valuation conditions, while newer buyers are underwriting in a system where assessed land values and effective taxes can align more quickly.

Who benefits and who feels the pressure

This is one of those reforms that looks administrative until you apply it to a real portfolio decision.

For an established owner, the market may still offer relatively strong positioning. For a new buyer, especially in areas where land values have run ahead, the reform can narrow the margin for error. If your deal already relies on a thin yield spread, a higher effective land tax burden can be the difference between acceptable and mediocre performance.

Denmark is still investable. But the old shorthand of “low-tax Nordic stability” no longer does enough work. You need to model the post-reform holding cost, not rely on market reputation.

Why this changes market selection

The reform pushes investors to become more selective about submarkets and entry prices.

A premium district with strong long-term appeal may still be a good hold if you are buying for capital preservation, tenant quality, or scarcity. But if your strategy is income-led, the post-2024 framework makes it even more important to ask whether a lower-entry city or district offers a cleaner relationship between rent and recurring tax cost.

That’s why broader international property trend analysis is useful only as a starting point. In Denmark, the local tax architecture can alter what looks attractive on a headline market chart.

The investor takeaway for 2026

The practical takeaway is straightforward. Don’t underwrite Danish property using historical assumptions borrowed from older articles or legacy owners. Use the current rules, current valuations, and current municipality-specific data.

Investors who do that can still build a sensible case for Danish exposure. Investors who don’t usually discover the tax reality after exchange, when it’s too late to renegotiate the economics.

A Guide for UK and Foreign Property Investors

Standard European property advice is rarely enough for UK buyers in Denmark. The legal title may be manageable, the market may look orderly, but the tax and reporting side becomes more complicated the moment income crosses borders.

The first issue is treaty complacency. Many UK investors assume that a tax treaty eliminates most practical overlap. It doesn’t. The verified position here is that UK investors face double-taxation risks because the UK-Denmark tax treaty does not fully mitigate all property-related taxes. That alone means your Danish purchase should be modelled as a cross-border tax project, not just a foreign letting purchase.

The UK-specific problem

A domestic Danish investor and a UK-resident investor aren’t solving the same puzzle.

The UK investor has to think about:

- Where rental income is taxed

- How foreign property taxes interact with UK reporting

- How gains and deductions are recognised

- What exchange-rate movements do to sterling return

That final point gets neglected far too often. Even if a Danish asset performs operationally, a UK investor still lives in pounds. The actual portfolio result is what remains after Danish tax, UK reporting, and currency conversion.

Valuation risk and backdated assessments

The second issue is administrative risk. Denmark’s valuation system has gone through delays and recalculations, and that isn’t just a background story for lawyers.

The verified data points are stark. A prudence rule taxes land at 20% below assessed value, yet backdated bills in high-value areas such as Copenhagen’s Nordhavn have averaged DKK 220,000, about £25,000, due to agency errors, according to the material supplied for this article. For a foreign owner with no Danish-language administrative routine, that sort of surprise can hit harder than the underlying annual tax itself.

A foreign investor usually copes with tax rates. What causes real stress is a retrospective bill tied to a valuation process they didn’t fully monitor.

That is why I treat Danish assessment monitoring as part of asset management, not as paperwork to sort out after completion.

Compliance is not a box-ticking exercise

The market has become more visible to British buyers. The verified material notes a 15% year-on-year rise in UK searches for “Denmark property investment”, but practical guidance on compliance and foreign-exchange hedging remains thin.

For UK buyers, that gap matters. You need a process for tracking Danish assessments, preserving tax documents, and matching Danish filings to UK reporting obligations. If you’re also managing a broader overseas portfolio, you should think about Danish land tax in the same discipline as you would capital gains tax on foreign property, because the compliance logic is cross-border even when the taxes differ.

A useful explainer sits below.

What foreign investors should actually do

There isn’t a glamorous answer. The right approach is procedural.

- Track assessments actively: Follow the public valuation process and keep copies of notices and revisions.

- Match Danish and UK records: Don’t wait until year-end to reconcile rental income, expenses, and tax payments.

- Model in sterling as well as kroner: Your operational yield in Denmark can look fine while your sterling result weakens.

- Use local specialists where the facts justify it: That is especially true for higher-value assets or any case involving revised assessments.

The primary mistake is to buy in Denmark using generic EU property assumptions. Denmark is investable, but it rewards investors who treat tax administration as part of the investment case, not as an afterthought.

Strategic Planning to Minimise Your Tax Burden

Tax planning in Denmark is less about tricks and more about disciplined execution. Investors who do well here usually aren’t doing anything exotic. They’re checking valuations early, selecting assets with the right land-to-improvement profile, and making sure every deductible expense is captured.

The strategic logic sits deep in the system’s history. Denmark’s land tax evolved from the abolition of the hardkorn tax in 1903, then moved to capital land value taxation under the 1922 National Land Value Tax Act, which introduced a 1.5 per mille rate and periodic valuations. Modern land value tax rates of 0.6% to 2.4% are presented as part of a framework that encourages development by taxing fixed land supply without penalising improvements, according to the historical and policy discussion in the Land Research Trust chapter on Danish land value taxation.

What works in practice

Investors often ask how to “beat” denmark land tax. The more realistic objective is to minimise avoidable cost and avoid overpaying because of poor diligence.

Here is what tends to work.

- Verify the valuation before completion: If the public land assessment looks out of line with the asset’s reality, flag it immediately and investigate the challenge process.

- Model land tax as a deductible rental expense: For income-producing property, that deduction matters to the actual after-tax return.

- Prefer clarity over headline glamour: A well-located asset with a sensible land component can outperform a prestige address with weak tax-adjusted yield.

- Keep assessment records organised: When recalculations or retroactive adjustments occur, documentation matters.

Choosing the right type of asset

Denmark’s system rewards careful asset selection. Because the tax focuses on land rather than improvements, the relationship between site value and income-producing building value becomes more important.

Here's a practical perspective:

| Asset profile | Likely tax planning implication |

|---|---|

| Prime urban plot with high land value | Strong location, but tax drag may be heavier and needs tighter underwriting |

| Asset with stronger building-income contribution | Can offer better tax-adjusted income if the land share is less dominant |

| Redevelopment or repositioning angle | More attractive where the tax system does not punish improvements in the same way |

UK investors often fixate on acquisition costs and broad annual charges, a habit that can mislead when considering Denmark. In Denmark, the strategic question is often whether the site valuation makes sense against the income plan.

Best lens: Don’t ask only whether the property is expensive. Ask whether the land value embedded in the tax assessment is justified by the rent, location, and long-term use.

A working checklist for investors

I’d use a simple checklist before exchange and again after completion.

- Check Vurderingsportalen.dk records for the latest valuation and any pending changes.

- Confirm the municipality’s current rate rather than relying on broker shorthand.

- Run two cash-flow cases. One on the current assessment, one on a less favourable revised assessment.

- Capture deductibility properly in your rental-income calculations.

- Review whether the asset’s appeal comes from land scarcity or income efficiency. They are not the same thing.

- Understand your wider ownership consequences, especially if the purchase links to lifestyle use or a second-home plan. That broader lens matters in the same way it does for second-home tax planning.

What does not work

What fails is casual underwriting.

It doesn’t work to rely on a seller’s informal tax estimate. It doesn’t work to ignore the public valuation because the initial bill “looks manageable”. And it doesn’t work to assume that a high-quality building automatically means an efficient tax profile. Grundskyld isn’t based on architectural charm. It is based on the taxable land position.

The investors who usually end up satisfied with Danish property are the ones who treat tax review as part of acquisition discipline. In Denmark, that isn’t defensive admin. It is part of buying well.

Conclusion Key Takeaways for Investing in Danish Property

For a time-poor investor, three points matter most.

First, separate the two taxes properly. In a buy-to-let context, Grundskyld is usually the recurring charge that deserves your attention, not the broader owner-occupier property value tax.

Second, verify the land assessment and the municipal rate before you commit. Denmark land tax is driven by the assessed land component and local application, so country-level assumptions aren’t enough for deal analysis.

Third, underwrite using the post-2024 reality. The newer rules make holding costs more sensitive to current valuations, which means lazy historical assumptions can damage projected returns.

Denmark remains a credible market for long-term property investors. The tax system is detailed, but it isn’t opaque. Buyers who respect the valuation process, watch for assessment changes, and build the land tax into their cash-flow model can manage it well. In that sense, denmark land tax isn’t a reason to avoid the market. It’s a reason to do proper diligence.

If you're comparing Denmark with other international markets, World Property Investor offers practical country and city guides, rental yield analysis, tax explainers, and cross-border buying insights to help you assess opportunities with more confidence.