Manchester outperformed the wider major-city pack on price growth. Over the five years to 2024, average property prices in the city rose 30.99%, against 15% across 20 major UK cities analysed by Colliers, according to this Manchester property growth analysis. For investors, that changes the usual framing. Manchester isn’t just a cheaper alternative to London. It’s a market where growth, rental demand, and relative affordability can align in the same asset.

That matters because many buyers looking at investment properties manchester still treat the city as a single market. It isn’t. A city-centre flat, a student house in Fallowfield, and a family rental in Levenshulme sit in different demand ecosystems, with different risks, operating costs, and exit routes.

A serious investment decision in Manchester starts with strategy, not postcode. Some areas suit yield-focused landlords who want stronger monthly cash flow. Others suit investors who can accept tighter income returns in exchange for stronger long-term capital positioning. The best opportunities usually sit where the asset type, tenant base, and regulation all line up.

Why Invest in Manchester Property in 2026

A city that has already recorded above-average house price growth can still attract fresh capital if rents, affordability, and tenant demand remain aligned. Manchester fits that profile in 2026, which is why it continues to draw both private landlords and larger investors.

The case for Manchester is less about a single headline growth number and more about market structure. Prices have risen enough to validate demand, but the city still sits within reach for buyers who have been priced out of London and parts of the South East. That leaves room for two distinct strategies.

For yield-focused investors, Manchester offers a large renter base spread across students, young professionals, and lower-cost family housing markets. For growth-focused investors, the stronger argument is the city’s ability to keep attracting jobs, graduates, and regeneration capital without the entry pricing seen in more mature southern markets. Manchester’s appeal lies in its ability to balance yield and growth, a combination many other UK markets force investors to separate.

Tenant affordability also matters. Investors assessing rent resilience should look beyond headline rents and consider how far local incomes still stretch on everyday costs. Our guide to Manchester living costs is useful here, especially for buyers comparing city-centre apartments with outer-neighbourhood family rentals.

The strategic implication is straightforward. Manchester should be treated as a set of sub-markets, each suited to a different objective, rather than as one broad “hotspot.”

That distinction will matter even more in 2026. Higher borrowing costs have made weak stock harder to justify, and regulation has become more relevant to returns. Houses in multiple occupation, short-let models, and emerging co-living formats can produce stronger income in the right location, but they also bring licensing, management, and compliance risk that many headline market summaries ignore. Investors who match asset type to tenant demand, local rules, and exit liquidity are far more likely to preserve returns over a full cycle.

The Macro Picture Manchester's Economic Engine

Manchester added roughly a tenth to its population between 2011 and 2021, while homeownership remains well below the national norm. For property investors, that matters more than a headline price-growth chart because it points to a city where renting is not a temporary stopgap but a durable part of how the housing market functions.

Growth has a real economic base

Manchester’s housing market is supported by a broad urban economy rather than a single demand story. As noted earlier, recent performance has outpaced many large UK cities, and the city continues to attract regeneration capital, office occupiers, and transport-led redevelopment. That mix matters because it supports both tenant demand and exit liquidity across market cycles.

For growth-focused investors, this is the central macro argument. Cities that keep adding jobs, commercial space, and infrastructure usually hold demand better when financing conditions tighten. Manchester has been one of the clearer examples outside the South East.

That does not mean every sub-market will appreciate at the same rate. Prime central apartments, family housing in commuter districts, and higher-yield stock in transitional areas respond to different drivers. Investors looking for a broader framework can compare this with our guide to property investment in 2025, which explains why capital is becoming more selective across developed markets.

Demographics support rental depth

Manchester also stands out for the scale of its renter base. According to this Manchester investment guide, the city’s population reached 551,938 in the 2021 Census, up 9.70% since 2011, above both the North West and England. The same source states that 62.0% of households rent privately or socially, while homeownership stands at 38.0%, far below the national figure.

Those numbers change the investment reading. In many UK cities, landlords depend heavily on marginal renters who may leave the sector when affordability improves. In Manchester, rental demand is tied more closely to the city’s tenure structure, age profile, and labour mobility.

This is why broad "hotspot" content often misses the point. Lists of the best places to buy an investment property can be useful as a starting point, but Manchester rewards a strategy-led approach more than a postcode-led one. A buyer targeting dependable income should care about tenant churn, licensing exposure, and stock type. A buyer targeting medium-term growth should care more about regeneration depth, transport links, and future owner-occupier demand.

Universities and workforce churn matter

The university pipeline adds continuity to that rental base. Large student cohorts support demand near campuses, but the more important factor for long-term investors is conversion. A meaningful share of graduates stay on, move into professional renting, and then shift outward through the city as incomes rise.

That progression helps explain why demand is not confined to the core. It moves from student districts into city-centre flats, then into outer areas with better value, more space, or stronger sharer economics.

It also creates an opening in formats many investors still underwrite poorly. Co-living and professionally managed shared housing can perform well in locations with strong transport, graduate employment, and constrained affordability, but only if the regulatory position is clear. Licensing rules, amenity standards, and management intensity can alter net returns far more than the gross yield suggests. For Manchester investors, the macro picture is attractive precisely because it is diverse. The opportunity is real, but strategy selection matters more here than in simpler single-driver markets.

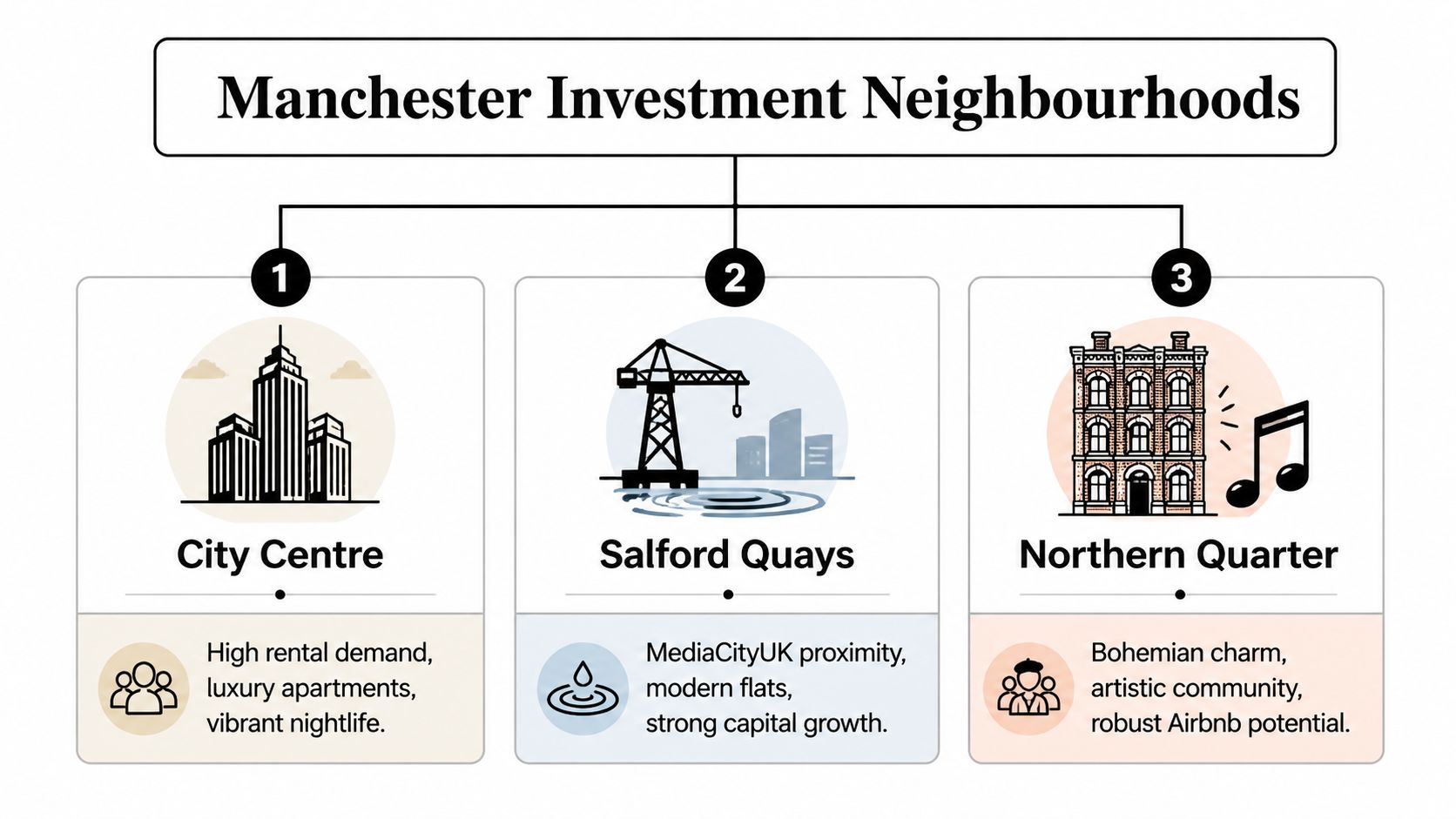

Where to Buy Investment Property A Neighbourhood Analysis

Manchester does not behave like a single market. A city-centre flat in M2 serves a different investment case from a sharer house in M14 or a city-fringe terrace in Ardwick. Buyers who group them together usually misprice either the income, the management burden, or the resale outlook.

Established prime areas

Central districts such as M2, M3, and M4 suit investors who value liquidity, modern stock, and a broad professional tenant base. The investment logic here is usually defensive rather than aggressive. You are buying easier reletting, stronger resale depth, and demand that is less dependent on one tenant group.

That does not make all central postcodes equal. As noted earlier in the article, yields vary meaningfully across the core, which matters because many buyers treat "city centre" as one pricing category. In practice, premium addresses can produce weaker income than fringe-central areas that still benefit from walkable access to jobs, retail, and transport.

This part of Manchester tends to work best for two investor types. The first is the landlord who wants lower operational friction than a student or HMO model. The second is the buyer who expects future resale demand from both investors and owner-occupiers, which can support pricing even when rental yields are not at the top of the city range.

High-yield districts

Income-led buyers should look harder at function than branding. M14, particularly Fallowfield and Rusholme, has long drawn attention because the stock, tenant profile, and local rental model can support stronger gross returns than prime central flats.

The reason is straightforward. Tenants in this submarket are often paying for proximity to universities, bus routes, and shared affordability rather than for concierge services or skyline views. That changes the economics. A relatively modest terraced house can outperform a more expensive apartment on rent if the room configuration and licensing position are right.

It also changes the workload. Student-heavy and sharer-led areas reward landlords who can handle annual turnover, furnishing standards, maintenance intensity, and compliance in detail. Selective licensing, Article 4 restrictions, and HMO rules can alter net income far more than the headline yield suggests. A buyer who ignores those points may buy a property that looks attractive on paper and performs only moderately after costs.

There is a middle ground. Some investors want strong rental demand without relying almost entirely on students. In those cases, neighbourhoods near major employment nodes, hospitals, and transport corridors can produce more stable occupancy with fewer operational demands than a pure room-by-room strategy.

For readers comparing UK locations beyond Manchester, this overview of the best places to buy an investment property is useful because it sets city markets against one another instead of treating each in isolation.

Emerging growth corridors

Growth-focused investors should spend less time chasing the highest first-year yield and more time assessing where demand can broaden over the next cycle. In Manchester, that often points to city-fringe and well-connected outer districts where pricing still reflects an older local reputation more than current direction of travel.

Levenshulme fits that pattern. It has stronger appeal to renters who want more space and a neighbourhood feel while still keeping access to the centre. That tenant mix can support longer stays than a student-heavy area, which matters because lower churn protects net returns.

Ardwick is different. Its appeal lies in its position near the city core and major institutions. For investors, that creates optionality. A standard buy-to-let can work, but so can more specialist formats such as co-living or professionally managed shared housing, provided planning, licensing, and amenity standards are checked before purchase. That format is often overlooked in Manchester analysis, yet it can be well suited to areas where graduate renters are priced out of the centre but still want short commutes.

The wider point is that emerging districts are not merely "cheaper Manchester." They are separate propositions with different exit routes. Some are likely to mature into owner-occupier markets with stronger capital growth support. Others may remain mainly income plays with periodic bursts of pricing momentum tied to infrastructure or regeneration.

How to match area to strategy

A practical framework helps:

- For stronger monthly cash flow: Focus on rental districts such as M14, where shared housing economics can support higher gross income, but only after checking licensing and management requirements.

- For balanced yield and resale flexibility: Look at M3 or M4, where central access, modern stock, and broad tenant appeal can produce a steadier mix of income and liquidity.

- For medium-term growth potential: Study Levenshulme and Ardwick, where entry pricing can still leave room for rerating if transport links, public realm, and buyer demand continue to improve.

- For lower operating complexity: Choose conventional flats or houses over management-heavy shared assets, even if the initial gross yield is lower.

Area choice should follow the business plan. Investors who want a broader framework for comparing strategy by location can also review this guide on where to buy investment property.

Analysing the Financials Prices, Rents and Yields

A spread of roughly three to four percentage points between Manchester and London gross rental yields changes the investment equation. It shifts the discussion away from simple “best area” lists and toward strategy selection: income first, growth first, or a blend of both.

Manchester works best when pricing, rent, operating costs, and financing are tested together. A flat in a premium central postcode can look weaker on headline yield but still suit an investor targeting liquidity and resale depth. A terraced house in a rental-led district can produce stronger income, yet the margin can narrow quickly once licensing, maintenance, and management intensity are priced in.

What the city-level numbers mean

As noted earlier, Manchester’s average rents and purchase prices still support stronger gross yields than much of southern England. That matters less as a marketing line than as a buffer. Higher starting yield gives investors more room to absorb financing costs, service charges, voids, and regulatory change without the deal falling apart.

Property type also matters. Flats usually offer a lower entry price and easier access to central demand, but service charges and future building-safety costs can reduce net returns. Terraced housing often starts with better gross income and broader tenant demand, especially in shared or family formats, though maintenance exposure is usually higher. Detached and semi-detached stock can appeal to owner-occupiers on exit, but they are rarely the first choice for investors focused on immediate yield.

That is why city averages are only the starting point.

Gross yield versus real return

Gross yield is a screening tool, not an investment decision. Annual rent divided by purchase price is useful for comparing one listing with another, but it ignores the costs that determine whether a property produces durable cash flow.

Take a typical rental-led example in M14. A three-bed terraced house around the low-to-mid £200,000 range with rent around £1,450 per month can produce a headline gross yield close to 8%. On paper, that looks materially stronger than a central flat. In practice, the net result depends on whether the property is a standard single let, a sharer household, or an HMO, because each route changes management input, compliance costs, wear and tear, and void risk.

A simple rule helps. Use gross yield to build the shortlist. Use net yield, financing costs, and stress testing to decide whether the asset fits your plan.

If you are comparing debt structures before underwriting a purchase, this overview of property finance options is a useful starting point.

Manchester Postcode Investment Snapshot (2026)

| Postcode | Key Area(s) | Average Property Price | Average Monthly Rent | Average Gross Yield |

|---|---|---|---|---|

| M2 | City Centre core | Higher than many outer districts | Not provided in verified data | Lower than rental-led outer areas |

| M3 | Central Manchester | Mid-to-upper central pricing | Not provided in verified data | Mid-6% range in prior market comparisons |

| M4 | Northern Quarter and nearby central areas | Mid central pricing | Not provided in verified data | Mid-to-high 6% range in prior market comparisons |

| M5 | Salford fringe / nearby rental market | Competitive versus core centre pricing | Not provided in verified data | Mid-6% range in prior market comparisons |

| M14 | Fallowfield, Rusholme | Lower entry point than prime central postcodes | Example rent around £1,450 on a typical three-bed terrace | Around the high-7% range on gross assumptions |

The pattern is consistent. Premium central postcodes usually suit investors prioritising liquidity, newer stock, and tenant depth over maximum yield. Rental-led districts farther from the core often suit income investors prepared to handle more operational complexity.

There is a third category worth watching. Areas where conventional flats struggle to deliver enough net income after service charges may become better suited to alternative formats such as co-living or professionally managed shared housing, provided the local planning and licensing position is checked first. That trend is still uneven, but it is one of the more overlooked ways to improve returns in a city where affordability pressure is rising.

Investors can speed up first-pass underwriting with a rental yield calculator for comparing gross and net returns. The serious work sits in the assumptions. Service charges, refurbishment cycles, voids, licensing, and management fees determine whether a 7% gross deal is better than a 5.5% one with fewer moving parts.

How to Buy Your Manchester Investment Property

Buying investment properties manchester is straightforward in principle and detail-heavy in practice. The process rewards preparation more than speed.

Start with the structure, not the listing

Before viewing properties, decide what you’re buying for. A city flat, a standard family let, and a student HMO all need different financing, legal checks, and management assumptions. Investors often waste time on listings that don’t fit their chosen structure.

The biggest early decision is whether the asset works better as a personal purchase or through a company structure. That choice has tax, lending, and admin implications, especially if you expect to scale into multiple units. If you need a simple primer before speaking to brokers or solicitors, this guide on how to do property investment is a sensible starting point.

A related issue is title. Flats are commonly leasehold. Many houses are freehold. The legal and cost implications are significant, particularly where service charges, ground rent, permissions, and lease terms affect income and resale. This explainer on leasehold versus freehold helps clarify what to check before you commit.

Build your buying team early

In England, a smooth acquisition usually depends on four professionals:

- Mortgage broker: Useful for matching your profile to lenders, especially if you’re self-employed, overseas, or buying a specialist rental asset.

- Conveyancing solicitor: Handles title review, searches, contract negotiation, and completion.

- Surveyor: Critical for older houses, converted stock, and anything with visible maintenance risk.

- Letting agent or management firm: Valuable if you need realistic rent advice before purchase, not only after completion.

Many first-time landlords appoint the solicitor too late. That creates delays once an offer is accepted. A better approach is to line up your legal team, your proof of funds, and your financing route before you start bidding.

Follow the sequence

A practical buying flow looks like this:

- Define your target asset. Decide whether you want a flat, terrace, or shared housing model.

- Secure decision-in-principle finance. That sharpens your budget and strengthens your offer.

- Offer subject to survey and legal review. Keep your wording precise.

- Run due diligence. Check title, lease length where relevant, planning constraints, local licensing rules, and expected repair costs.

- Exchange contracts. At this point, the deal becomes legally binding.

- Complete and insure. Then move immediately into lettings, compliance, and management set-up.

Here’s a useful visual walk-through of the process and the mindset needed when evaluating deals:

Costs buyers often underestimate

Purchase price is only one layer of cost. Investors should also budget for financing fees, legal work, surveys, furnishing, insurance, compliance upgrades, and any refurbishment needed to reach the target tenant profile.

The most expensive mistakes usually come from underestimating condition and ongoing obligations. A leasehold flat may look low-maintenance until service charges erode cash flow. An older terrace may appear cheaper to run until repairs and compliance works start stacking up. Investors who stay disciplined at purchase tend to outperform those who negotiate hard on price but ignore total ownership cost.

Buy with your exit in mind. The easiest property to finance isn’t always the easiest to let, and the easiest to let isn’t always the easiest to resell.

Understanding Investment Risks and How to Mitigate Them

Manchester is attractive, but “good market” doesn’t mean “easy market”. The biggest mistake investors make is assuming strong city-level demand cancels out asset-level risk. It doesn’t.

Regulation can change the return

Recent UK regulatory changes can materially affect profitability, especially for higher-rate taxpayers. Section 24 tax restrictions and the proposed Renters (Reform) Bill are two of the most important issues flagged in this Manchester 2025 investment guide. The same source gives a concrete example: a £200K property with an 8% gross yield, producing £16K in rent, could see its net return fall below 5% after a 45% tax on profits.

That’s an important warning because high-yield student stock often looks best on gross numbers. Tax treatment can narrow the advantage sharply.

Operational risk varies by strategy

Risk isn’t distributed evenly across Manchester strategies.

- Student-led houses: Strong demand, but more turnover, furnishing wear, and compliance pressure.

- City-centre flats: Broad tenant appeal, but leasehold costs can weaken income if service charges rise.

- Emerging-area houses: Better entry prices, but more dependence on local execution, maintenance quality, and neighbourhood trajectory.

A high-yield property with frequent voids, higher repairs, and tighter regulation can underperform a lower-yield asset with stable tenants and cleaner operating costs. That’s why investors should underwrite for the actual model, not the advertised headline.

Practical mitigation moves

Several defensive steps matter more than trying to predict the market perfectly:

- Stress-test the deal: Model the property with conservative rent assumptions and realistic running costs.

- Use specialist tax advice: Higher-rate taxpayers and portfolio landlords should test different ownership structures before exchange.

- Check local compliance early: Student and shared housing strategies need extra scrutiny on licensing, EPC standards, and planning restrictions.

- Choose management to fit the asset: A student let and a professional city flat need different operational oversight.

- Keep reserves: Maintenance and reletting costs rarely arrive at convenient times.

The best risk control in property isn’t optimism. It’s buying a property that still works when conditions are less favourable than today.

Real-World Scenarios and Your Investor Checklist

A Manchester buy-to-let that works well for one investor can be a poor fit for another. The difference usually comes down to strategy, not postcode alone. Yield-led buyers, growth-led buyers, and hands-on operators are solving for different outcomes, so the right asset is the one that fits the operating model as well as the spreadsheet.

Scenario one: the yield investor using a student or sharer model

An income-focused buyer may still find M14 attractive, as noted earlier, because rents are supported by a deep student market and a housing stock that lends itself to shared occupation. On paper, that can produce stronger gross yields than many central flats.

The trade-off is operational. A student or sharer house has more moving parts: licensing checks, furnishing replacement, more frequent reletting, and greater exposure to tighter standards on energy performance and management. In practice, this suits an investor who treats the property as an active income asset and is willing to accept higher oversight in exchange for stronger cash flow potential.

There is also a less obvious point. In areas dominated by one tenant type, income can look resilient right up to the moment regulation or local supply shifts. A high headline yield is only attractive if the landlord has priced in compliance costs and periods of heavier maintenance.

Scenario two: the growth-and-liquidity investor buying a city-fringe flat

A different buyer may prefer M4 or another near-centre district already discussed earlier. The appeal is usually not the highest starting yield. It is a combination of broad tenant demand, easier resale, and exposure to parts of Manchester that benefit from office, transport, and lifestyle demand at the same time.

This route often works better for investors who want lower management intensity and a clearer exit pool. Young professionals, relocators, and couples typically create a more diversified demand base than a single-use student market. That can matter more than an extra point of gross yield, especially once service charges, letting fees, and void assumptions are included properly.

Leasehold economics need close attention. A flat with acceptable rent and purchase price can still disappoint if service charges rise faster than rent or if major works are planned. For a growth-led investor, liquidity depends as much on sensible building costs and lease terms as on location.

Scenario three: the overlooked hybrid play in co-living and professional HMOs

A third strategy sits between the first two. Some investors are targeting houses for young professionals in locations just outside the core centre, where demand is linked to affordability pressure in prime districts and changing tenant preferences for flexible shared living.

This can be attractive because it spreads rent across multiple occupiers without relying entirely on the student cycle. It also carries sharper regulatory risk. Licensing rules, amenity standards, planning controls, and management quality matter more here than they do in a standard single-let. Investors considering this route need to be clear on whether they are buying a conventional buy-to-let with upside, or a regulated operational asset that needs specialist management from day one.

Investor due diligence checklist

Before exchange, test the deal against the strategy you are pursuing:

- Match the asset to the tenant base: A student house, a professional HMO, and a city flat each have different demand drivers and cost structures.

- Underwrite net income, not gross yield: Include management, service charges, furnishing replacement, licensing, insurance, maintenance, and realistic void periods.

- Check the regulatory position early: Confirm whether the property needs licensing, whether planning use is appropriate, and whether upcoming EPC rules could force capital spending.

- Review the building as well as the unit: For flats, inspect service charge history, reserve funds, cladding position where relevant, and any planned major works.

- Stress-test the exit route: Ask who the next buyer is likely to be. Another landlord, an owner-occupier, or a cash investor will each value the asset differently.

- Walk the micro-location: Street quality, competing stock, transport access, and nearby regeneration often have more impact on tenant demand than the wider postcode average.

- Choose management that fits the strategy: Low-touch single lets and high-turnover shared housing need very different operating systems.

The strongest Manchester investments usually look disciplined rather than exciting. They fit a clear strategy, produce acceptable returns after real costs, and remain sellable even if the market is less forgiving than it is today.

If you’re comparing Manchester with other UK and international markets, World Property Investor publishes data-led guides on yields, neighbourhoods, buying structures, and market fundamentals to help you research property opportunities with more confidence.