You’re probably looking at the UK market and feeling two things at once. First, property still matters as a long-term wealth asset. Second, the domestic equation has become harder to like. Tax pressure, tighter regulation, and uneven returns have pushed many serious investors to ask a more useful question than “what’s hot?” The better question is where to buy property abroad for your specific objective.

That matters because overseas property isn’t one market. Spain, Greece, the UK, and other international destinations all reward different strategies. A holiday let in a tourism-led coastal market behaves differently from an urban apartment bought for long-term capital growth. A residency-led purchase has a different logic again. If you treat them as interchangeable, you’re much more likely to overpay, underperform, or get caught by tax rules you didn’t model properly.

Good international investing is usually less about spotting a fashionable country and more about filtering decisions in the right order. Start with your goal. Test the market’s fundamentals. Pressure-test the legal and tax position. Then decide whether the expected return still justifies the complexity. That’s the discipline that protects capital.

If you’re still narrowing your shortlist, this overseas property guide is a useful starting point for comparing markets at a high level before you commit to deeper due diligence.

Introduction: Navigating the Global Property Market in 2026

The global market in 2026 offers more choice than most investors can realistically process. That sounds positive, but too much choice often leads to weak decisions. Buyers jump from “Spain looks good” to “Greece has higher yields” to “maybe I should buy in Dubai instead” without a framework for judging what fits their portfolio.

For UK-based investors, the pressure to look abroad is understandable. Domestic tax changes, compliance burdens, and lower after-tax income in some common buy-to-let structures have made international property a mainstream diversification route rather than a niche move. Lifestyle demand also plays a bigger role than many investors admit. Buyers often want a property that can serve both financial and personal objectives, even if one goal clearly comes first.

The mistake is treating overseas property like a simple ranking exercise. There isn’t one correct answer to where to buy property abroad. There’s only a market that matches your time horizon, tax position, management tolerance, and target return.

The best market on paper can still be the wrong market if the legal structure, exit timeline, and operating model don’t suit you.

That’s why experienced investors work backwards. They define the job the property must do, then test which markets can realistically do it. A low-vacancy tourism zone may work for a furnished short-let strategy. It may be a poor fit for an investor who wants minimal management and no seasonal swings.

Clarity beats enthusiasm. So does process.

First Principles: Aligning Your Goals with Your Strategy

Before choosing a country, decide what success looks like. Investors who skip this step usually end up buying a compromise asset. It may be enjoyable to own, but it doesn’t perform clearly as an income property, a growth asset, or a residency tool.

A good way to begin is to think like an operator, not a browser. If you want a broader grounding in the basics, this real estate investing guide gives a useful overview of how investors assess property as an asset class. Once that foundation is in place, your overseas strategy becomes much easier to sharpen.

For readers who are still at the start of that process, this guide on how to invest in property is also useful for framing the decision before you shortlist countries.

Four investor profiles that drive most overseas purchases

The buy-to-let investor wants dependable rental income. This buyer usually prioritises occupancy, yield, local demand, and ease of management. They can live with moderate capital growth if the cash flow is consistent.

The holiday home buyer wants personal use plus selective rental income. This profile often overestimates rental performance and underestimates management friction. If this is your category, be honest about how often you’ll block out prime dates for yourself.

The residency-led buyer is using property to support mobility or lifestyle relocation. In this case, the legal pathway matters as much as the asset. The property is doing more than one job, so return analysis must include the non-financial value of residency access.

The growth-focused investor is looking for appreciation first. Rental income still matters, but mainly as a way to carry the asset while waiting for a stronger exit. This investor cares more about supply constraints, urban demand, infrastructure, and long-term market credibility.

Match your objective to your tolerance for complexity

These goals don’t carry the same operational burden.

- Income-first strategies usually need stronger property management and tighter cost control.

- Lifestyle-led purchases demand discipline, because personal attachment can lead to poor buying decisions.

- Residency strategies require more legal scrutiny and less optimism.

- Growth strategies need patience. They also need a clear view on exit liquidity.

A client looking for immediate rental performance often shouldn’t buy the same asset as a client planning eventual relocation. The country may be the same, but the property type, location, ownership structure, and financing approach often won’t be.

Practical rule: if you can’t describe your main objective in one sentence, you’re not ready to choose a market.

Questions worth answering before you research locations

Use a short filter before you do anything else:

- What matters most? Income, capital growth, lifestyle use, or residency.

- How active do you want to be? Hands-on management or fully delegated.

- What’s your holding period? Short-term trading logic and long-term asset building are different games.

- How much complexity can you absorb? Tax structuring, local compliance, and cross-border reporting all take time and money.

Once those answers are clear, country selection gets easier. You stop asking “where is everyone buying?” and start asking “which market suits the job I need this asset to do?”

Building Your Investment Framework: Key Selection Criteria

A country can look attractive in a headline and still be a weak investment. Serious buyers need a repeatable framework, especially when comparing established markets with recovering or emerging ones.

The legal and tax side deserves attention early, not after you’ve found a property. Post-Brexit buying in the EU has created hidden issues for UK investors. UK residents can face 40% inheritance tax on worldwide assets, and over 20,000 UK expats are caught annually, while unresolved double taxation treaties can reduce net returns in Spain and Portugal by 15-25%, according to the analysis cited by MyAssets on buying property abroad. Those are not small leaks. They can change the economics of an otherwise good deal.

If you want a broader location comparison model, this piece on the best location for property investment is useful alongside the framework below.

Pillar one: economic stability

Start with the country, not the property. You need to know whether the wider economy supports jobs, spending, inward movement, and credit confidence.

Look at central bank commentary, national statistics offices, local housing authorities, and major economic bodies. A stable economy doesn’t guarantee a good investment, but instability makes every assumption weaker. Weak growth, policy volatility, or unreliable institutions can turn routine ownership into a constant risk exercise.

Pillar two: property market health

Then assess the market itself. Price growth matters, but it never tells the whole story. Transaction volumes, stock availability, and buyer depth all shape how resilient a market really is.

A market with rising prices but poor liquidity can trap investors. A market with moderate growth and steady transactions is often healthier. What works in practice is looking for alignment between pricing, demand, and resale prospects.

Pillar three: rental demand drivers

Rental demand should come from something tangible. Tourism, student demand, expat communities, transport links, and employment hubs all matter because they create repeat occupancy.

Ask simple questions:

- Who rents here? Tourists, local workers, students, retirees, or digital professionals.

- Why do they choose this location? Climate, jobs, education, transport, or lifestyle.

- How durable is that demand? Seasonal demand can work, but only if your costs and management model account for it.

Pillar four: legal and tax reality

Many overseas purchases go wrong when buyers spend weeks discussing the view, the furniture, and the neighbourhood, then treat tax as a final admin task.

That approach doesn’t work. You need clarity on ownership rights, local property taxes, capital gains treatment, inheritance exposure, rental taxation, and whether any treaty relief works in practice. You also need to know whether your UK position changes the answer.

Buy only after your lawyer and tax adviser have reviewed the structure you plan to hold, not just the property you plan to purchase.

Pillar five: financing and purchase costs

Some markets are friendly to cash buyers but awkward for financed buyers. Others offer lending but impose process friction that drags out completion and increases risk. Entry costs also vary sharply. If you don’t model them upfront, your expected return is fiction.

A quick comparison framework helps:

| Criterion | What to test | Why it matters |

|---|---|---|

| Economic backdrop | Growth, policy stability, institutional reliability | Supports confidence and buyer demand |

| Market condition | Price trend, transaction depth, resale liquidity | Affects entry timing and exit options |

| Rental base | Occupier type and demand durability | Drives occupancy and yield stability |

| Legal and tax position | Ownership, tax exposure, succession planning | Protects net returns |

| Funding and costs | Mortgage access, fees, transfer process | Shapes real cash-on-cash performance |

Use this framework every time. It won’t remove risk, but it will stop you confusing a compelling destination with a stable investment market.

From Data to Decisions: How to Research International Markets

Research becomes manageable once you stop trying to know everything. You only need enough reliable information to reject weak markets quickly and investigate strong ones properly.

Start with primary sources whenever possible. National statistics offices, government tax guidance, local land registries, central banks, and established property portals usually tell you more than social media, broker commentary, or relocation forums. Then cross-check what you find with transaction evidence, local legal advice, and current listing reality.

UK investors have a clear reason to be disciplined here. Tax changes have altered the domestic comparison. The phasing out of the non-dom remittance basis by 2025 and the effect of Section 24 mortgage interest relief restrictions have pushed many investors to seek more tax-efficient returns abroad. In the UK, gross rental yields in Liverpool can reach 7.5% gross, and incorporating through a limited company has become standard practice for many investors trying to manage those pressures, as reflected in the verified UK tax and yield data provided in the brief.

For broader context on market direction and how countries compare over time, this review of international property trends is a useful companion when you’re building a shortlist.

The three numbers that matter most

You don’t need a complex model on day one. You do need consistency.

Gross rental yield is annual rent divided by purchase price. It gives you a fast way to compare markets, but it ignores costs.

Net rental yield is more useful. It factors in management, maintenance, taxes, insurance, voids, and any local licensing or operating costs. Two markets with similar gross yields can produce very different net outcomes.

Return on investment should include the full picture. That means entry costs, financing costs, tax leakage, expected holding period, and likely resale conditions. Investors often call a property “high yielding” without measuring what reaches their account after friction.

A practical research workflow

Use a staged process rather than trying to analyse every market at full depth.

Screen the country

Focus on ownership rules, tax treatment, macro stability, and the type of demand driving the market.Screen the city or region

Compare urban demand, coastal demand, and whether the area depends on one narrow source of occupiers.Screen the asset type

Long-let apartment, short-let holiday unit, or villa for personal use all produce different economics.Stress-test the costs

Include furnishing, management, repairs, local compliance, and cross-border tax reporting.Test the exit

Ask who is likely to buy from you later. If the answer is vague, be cautious.

A property isn’t a good investment because it rents well in summer. It’s a good investment if the annual income, tax treatment, and exit path still work after costs.

What to ignore

Some signals look persuasive but usually mislead:

- Developer marketing language often presents best-case occupancy and growth assumptions.

- Expat forum enthusiasm can be useful for lifestyle context, but not for underwriting.

- One-off bargain stories distract from the more important question of whether the market works repeatedly.

Good research is comparative, not emotional. The goal isn’t to prove a favourite country is right. It’s to find out whether the asset survives scrutiny.

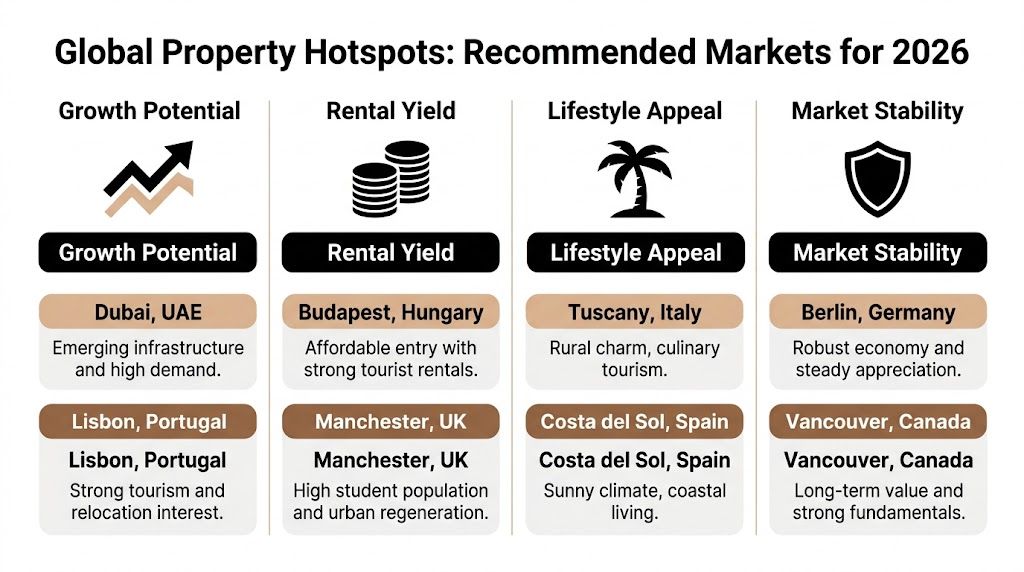

Global Property Hotspots: Recommended Markets for 2026

Some markets stand out because they fit a clear strategy well. Others are interesting but need more caution. The best shortlist is usually small.

If you’re comparing countries at a broader level, this guide to the best countries for property investment is a useful parallel resource. For most UK investors, though, a practical shortlist usually starts with established European markets that combine familiarity, rental demand, and transparent ownership structures.

Spain for stability, lifestyle, and proven demand

Spain remains one of the strongest answers to where to buy property abroad if you want a balance of lifestyle appeal and investment credibility. Property prices rose 9-13% year-on-year in 2024-2025, particularly in major urban and coastal areas, and coastal hubs offer average rental yields of 5-7%, according to the market summary published in this global property investment outlook. The same source notes that Madrid climbed to second place in European investment attractiveness in PwC’s 2025 report.

That combination matters. Spain isn’t just a holiday-home story. It offers depth. Buyers can target large cities such as Madrid, Barcelona, Malaga, and Valencia, or focus on coastal zones where tourism and established international communities support rental demand.

The appeal for UK investors is straightforward:

- Established market structure makes due diligence more predictable than in less mature markets.

- Lifestyle resilience supports both resale demand and lettings demand.

- Tourism-driven occupancy helps buy-to-let investors in the right coastal locations.

- Clear foreign buyer familiarity reduces some of the friction that first-time overseas investors often fear.

Spain isn’t perfect. Regional variation is real, and buying a mediocre asset in an overhyped micro-location can still disappoint. But for investors who want a market with broad appeal, transparent dynamics, and multiple exit routes, Spain earns its place near the top of the list.

Greece for yield, recovery momentum, and residency-led buyers

Greece suits a different profile. It tends to appeal more strongly to investors who want higher income potential, stronger lifestyle upside, or a residency-linked strategy.

Average property price growth reached 4-6% in 2025, while premium coastal and island markets achieved 8-10%, according to the same verified market data. Rental yields are reported at 6-8%, with holiday lets in tourism-led areas reaching 7-9%, supported by a rebound to 35 million visitors and a longer tourism season. The country’s Golden Visa structure also remains a major draw, with €250,000 investment in select areas granting residency, based on the verified Greece market data in the brief.

That creates a compelling mix for certain investors. Greece offers lower entry points in many areas than more crowded Western European favourites, while still benefiting from strong tourism and a clearer reform story than the country had during its crisis years.

What works well in Greece:

| Investor goal | Why Greece fits |

|---|---|

| Income-focused buy-to-let | Strong tourism demand and attractive holiday-let economics in the right locations |

| Lifestyle plus rental | Islands and coastal markets offer personal use value alongside lettings potential |

| Residency-led purchase | Golden Visa access can be central to the investment case |

| Growth with moderate risk | Recovery-backed growth can appeal if bought selectively |

The trade-off is operational. Greece can still require more patience on process, and buyers need strong local advisers. That doesn’t make it a weak market. It means the margin for casual decision-making is smaller.

Greece often works best for investors who accept a little more complexity in exchange for stronger yield potential and residency optionality.

The UK for selective domestic diversification

This is a guide to buying abroad, but the UK still belongs in the comparison because many investors are deciding whether to deploy capital internationally or stay domestic and move into different regional markets.

Foreign investors in the UK now face stricter transparency requirements under the Economic Crime and Corporate Transparency Act 2023, which contributed to a 22% drop in overseas purchases from £17.2 billion in 2022 to £13.4 billion in 2023, according to the verified UK market data in the brief. That tells you something important. The UK remains investable, but the compliance burden is rising.

Within the UK, regional city economics often look stronger than prime London for income-focused investors. Manchester is highlighted in the verified data with gross rental yields of 6.2%, compared with 3.8% in London, while Liverpool can reach 7.5% gross in the separate verified tax and yield data. For investors who still want legal familiarity and sterling exposure, that can be a better move than forcing an overseas purchase too early.

How to choose between them

If you strip away the noise, the decision often comes down to fit.

- Choose Spain if you want a mainstream European market with strong lifestyle demand, broad resale appeal, and solid rental performance.

- Choose Greece if you want stronger yield potential, tourism-led upside, and possible residency benefits.

- Choose a domestic regional UK strategy instead if your priority is keeping legal and financing complexity lower while still pursuing income.

There isn’t a universal winner. There is only the market that best matches your objective, tax position, and appetite for operational work.

Executing Your Purchase: A Step-by-Step Buying Checklist

Buying abroad gets easier once you break it into stages. The right process won’t remove risk, but it will stop most of the avoidable mistakes that come from rushing, trusting the wrong people, or sending funds before the paperwork is secure.

One useful comparison point is the UK itself. The Economic Crime and Corporate Transparency Act 2023 introduced a public register for overseas entities owning UK property, contributing to a 22% drop in overseas purchases in 2023, according to this overview of real estate investment countries and UK foreign-buyer regulation. Many overseas markets still feel more straightforward in practice, provided you follow a disciplined transaction process.

The transaction sequence that works

Build your team first. You need an independent lawyer, a reputable local agent, and if relevant, a mortgage broker and tax adviser. Don’t rely on a developer’s recommended lawyer without independent checks.

Confirm ownership and title early. Your lawyer should verify legal ownership, planning status, debts attached to the property, and whether the asset can legally be rented in the way you intend.

Open the practical channels. In many countries, you’ll need a local fiscal number, a bank account, and an accepted route for transferring funds. These admin tasks often cause delays if left too late.

Negotiate the offer with your exit in mind. Price matters, but so do terms, deposit protections, inclusions, and timing. A cheap deal with weak legal protections can be expensive later.

For a useful supplementary overview, this guide on the steps to buying property abroad is worth reviewing before you instruct your team.

Due diligence before commitment

Many buyers become emotionally committed after a viewing trip. That’s the moment to slow down.

Use a formal checklist before signing anything:

- Legal review of title, planning, licences, and seller authority

- Tax review of purchase structure, rental treatment, and eventual disposal

- Operational review of management, maintenance, and local compliance

- Financial review of all costs, not just the headline purchase price

This is also the point where a notary or equivalent closing authority may become central, depending on the country. Their role is often procedural, not advisory. They are not a substitute for your own lawyer.

A short explainer can help if you want to visualise the process before moving ahead:

Completion and post-purchase controls

Completion isn’t the end of the job. After transfer, make sure title registration, utilities, insurance, tax registration, and management setup are all confirmed properly. If the property is meant to produce income quickly, the furnishing, licensing, and marketing plan should already be in motion before completion day.

Treat the first year of ownership as part of the acquisition, not a separate phase. That’s when weak assumptions show up.

A well-bought overseas property usually feels methodical, not dramatic. If the process feels rushed or unclear, stop and re-check the fundamentals.

Avoiding Costly Mistakes: Common International Buying Pitfalls

Most overseas property mistakes don’t come from bad countries. They come from bad habits. Buyers skip independent checks, underestimate costs, or assume a familiar holiday destination must also be a good investment market.

The first pitfall is relying on headline returns. Gross yield can make a property look attractive, but management fees, tax leakage, maintenance, licensing, and voids often reshape the picture. If you don’t underwrite the net position, you’re buying optimism.

The second is weak legal independence. Buyers still use the seller’s recommended lawyer, especially in resort markets where everyone seems connected. That may feel efficient. It isn’t protective. You need someone acting only for you.

The traps that catch sensible buyers

A few issues come up repeatedly:

- Underestimating total entry cost means the asset starts behind plan on day one.

- Ignoring currency exposure can alter the actual cost of purchase and income repatriation.

- Misreading inheritance and tax treatment can damage long-term returns more than a poor purchase price.

- Overestimating personal use plus rental compatibility often leads to weaker income than expected.

- Assuming management is easy from abroad creates operational drift and tenant issues.

Tax is the area where many investors need specialist support, especially if they have reporting obligations across jurisdictions. If you need a practical example of the kind of cross-border issues investors and advisers review, Nanak Accountants for international tax help offers a useful article on overseas investment tax considerations.

How to reduce the risk

Use simple controls.

- Get independent legal advice before reservation agreements or deposits become non-refundable.

- Model the property in a weak year rather than a perfect year.

- Decide who manages the asset before you buy it.

- Write down the exit plan at the same time as the purchase plan.

The easiest way to avoid a costly mistake is to refuse to solve important problems after exchange. By then, your leverage is gone.

Overseas property rewards preparation. It punishes assumptions.

Your Next Steps in Global Property Investment

The strongest overseas investors don’t start with a country. They start with a mandate. They know whether they want income, growth, lifestyle access, or residency support, and they test each market against that priority.

That’s the practical answer to where to buy property abroad. Spain may be the right choice for one investor because it blends transparency, rental demand, and broad buyer appeal. Greece may be better for someone seeking yield and residency options. A regional UK strategy may still win if simplicity and legal familiarity matter more than international diversification right now.

The discipline is always the same:

- Define the job the property must do

- Apply a repeatable market framework

- Research the numbers and legal position properly

- Buy through a professional process

- Plan the first year of ownership before completion

If you’re serious, pick one market from your shortlist and go deeper this week. Review ownership rules. Speak to a tax adviser. Compare one city, not ten. A focused decision process beats a broad but shallow search every time.

If you want a reliable place to compare countries, cities, yields, market trends, and buying processes before you commit capital, World Property Investor is a strong next step. It’s built for investors who want practical research, not hype, and it helps you narrow the field before you spend money on travel, legal work, or deal sourcing.