Property has built more private wealth than most investors realise, not because it’s glamorous, but because it combines income, appreciation and borrowed capital in a way few assets can. In the UK alone, the average house price rose from £63,866 in January 1995 to £268,548 by December 2023, according to the Office for National Statistics, a nominal CAGR of about 5.1% as cited in this real estate investment analysis. That single data point reframes the discussion. Wealth through property usually comes from patient ownership, disciplined underwriting and sensible debt, not from chasing the latest hot market.

That matters even more for global investors in 2026. Capital moves faster, financing options are broader, and international buyers can compare London, Berlin, Dubai or Istanbul from the same desk. But access has created noise. Many investors still buy where they holiday, follow social media hype, or confuse gross rent with real return. Those mistakes are expensive.

A workable approach is simpler. Start with fundamentals. Choose markets strategically. Match the right financing structure to the right asset. Analyse every deal conservatively. Protect returns through tax planning, legal structure and risk controls. That’s how to build wealth through property investment without relying on luck.

The global angle matters because the same framework travels. An established market may offer stronger legal certainty and shallower yields. An emerging market may offer stronger rental demand or lower entry prices, but more currency, policy or execution risk. The job is not to prefer one category blindly. It is to know what you are being paid for in each one.

For investors comparing regions and strategies, this broader perspective sits well alongside World Property Investor’s guide for property investors, especially if you’re thinking beyond your home market.

Introduction

From 1980 to 2023, UK residential property delivered 8.4% annual total returns, against 7.2% for equities, as summarised earlier in this article. The point is not that property always wins. It is that wealth in this asset class is usually built through a combination of income, appreciation and time.

Strategic investors start with the target, not the asset. A portfolio built to fund retirement income should be structured differently from one designed for long-term capital growth or family succession. That decision shapes everything that follows, from debt terms and cash reserves to tax treatment and jurisdiction.

Property creates wealth through two return streams working together. Rental income supports holding power and can compound through debt amortisation and reinvestment. Capital growth expands equity and improves refinancing options over time. Looking at only one side leads to poor decisions, especially when comparing markets internationally.

Why total return matters

Serious investors judge property on total return, not headline rent. A well-located flat in Manchester or Berlin with lower initial yield may produce better long-run results than a higher-yield unit in a volatile submarket where vacancy, tenant default, currency moves or weak resale demand erode returns.

That comparison becomes sharper across borders. Established markets such as the UK or Germany tend to offer stronger legal certainty, deeper lending markets and more predictable exits. Markets such as Dubai or Turkey can offer stronger income or lower entry prices, but investors are taking on different risks, including policy shifts, execution quality and foreign exchange exposure. The question is never which category is better in the abstract. The question is whether the expected return compensates for the risks you are taking.

Property rewards investors who buy on disciplined assumptions, survive weak periods, and hold through full cycles.

Set a mandate before you buy

I advise clients to write a clear investment mandate before reviewing deals. It improves discipline when markets get noisy and helps compare opportunities across very different countries on the same basis.

- Income first: Prioritise durable rent, conservative borrowing and assets that remain lettable in weaker trading conditions.

- Growth first: Accept a lower starting yield where supply constraints, infrastructure and occupier demand support long-term appreciation.

- Balanced mandate: Combine income and growth. For many private investors, this produces the best trade-off between resilience and upside.

- Legacy planning: Decide early how the portfolio will be owned, managed and passed on, especially if assets sit in more than one jurisdiction.

Investors at the start of the process often need a practical operating view alongside strategy. VerticalRent's property guide is useful for the mechanics of moving from first purchase to stable operation. For a broader cross-border perspective, this guide for property investors complements the framework set out here.

One purchase rarely creates lasting wealth. A repeatable method does. The investors who compound successfully tend to do the same few things well in every market they enter. They define the objective, compare jurisdictions on consistent criteria, buy with margin for error, and keep enough liquidity to hold through setbacks.

The Foundations of Property Wealth Creation

Cross-border property returns can diverge sharply even when the asset class looks similar on the surface. The difference usually comes from market structure, not marketing. Investors who build durable wealth compare jurisdictions with the same discipline they use to assess an individual deal.

The useful questions are consistent across borders. What supports demand. What restricts supply. How reliable is the legal system. How available is finance. How punitive is the tax position. How liquid is the exit. Headline yield and recent price growth matter, but they sit downstream of those fundamentals.

Established markets such as the UK and Germany usually offer clearer title, deeper lending markets and more predictable enforcement. Faster-moving markets such as Turkey and Dubai can offer stronger income, lower entry prices in some segments, or a better growth case tied to migration and business inflows. They also bring higher exposure to policy shifts, currency moves, execution risk and wider swings in sentiment. The right choice depends on whether the extra return more than pays for those risks.

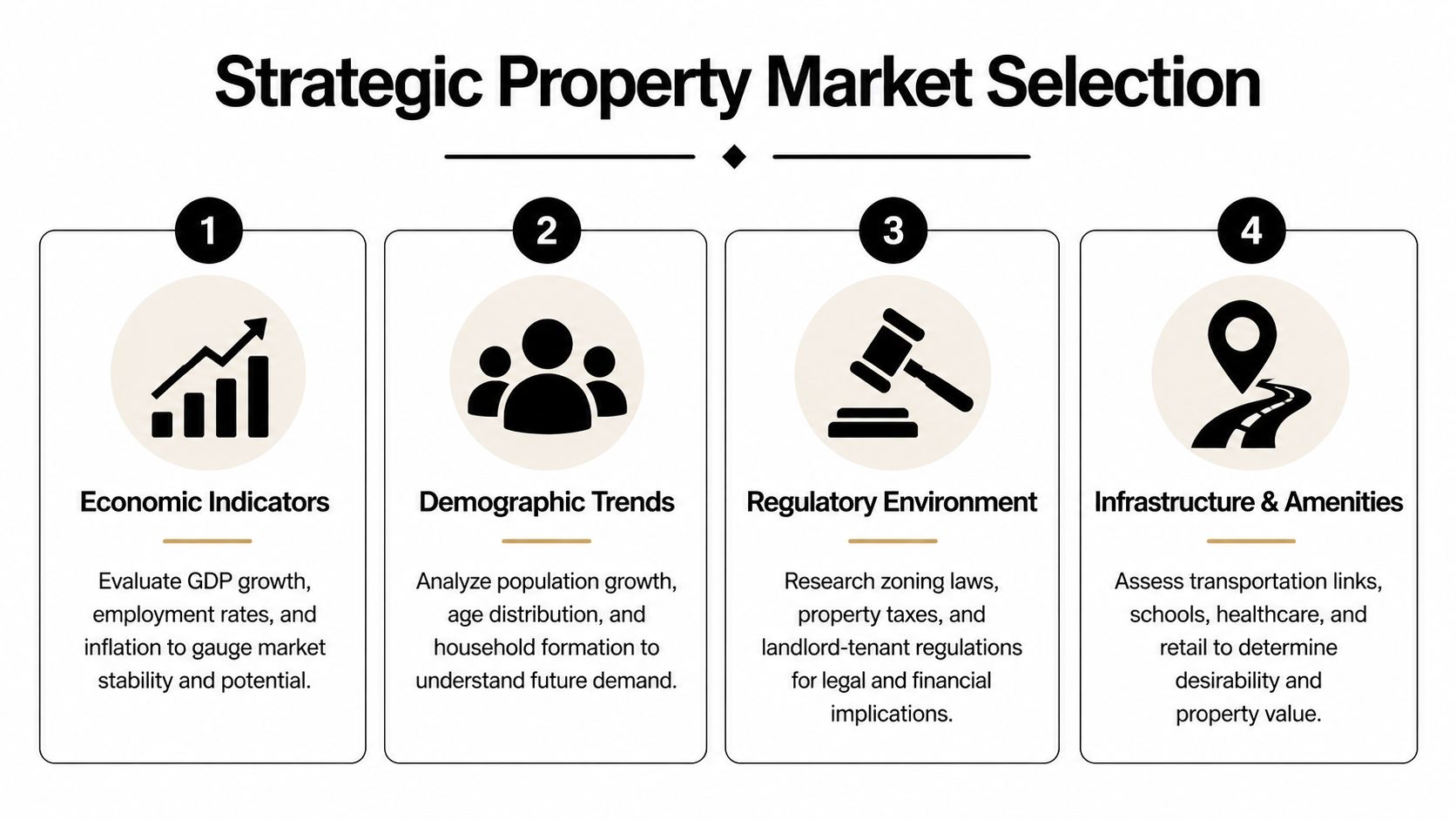

A practical framework for market selection

A market should pass the same test whether you are buying in Manchester, Berlin, Istanbul or Dubai.

I use four questions.

Who will rent or buy this asset in five years?

Focus on employment depth, household formation, migration and the quality of local incomes. A city with broad demand usually forgives mistakes better than one driven by a single employer or a narrow buyer pool.What constrains new supply?

Planning delays, land scarcity, infrastructure gaps and construction costs shape long-term pricing power. Tight supply in a healthy local economy often matters more than short-term market sentiment.How easy is it to finance and refinance?

Debt availability affects both returns and exit options. A market with active local lenders and predictable underwriting is very different from one where foreign buyers rely on specialist finance or cash.What can change the rules after purchase?

Rent controls, licensing, foreign ownership restrictions, transfer taxes and enforcement standards can alter net returns quickly. Cross-border investors need to underwrite regulation as carefully as they underwrite rent.

Comparing established and emerging property markets

| Characteristic | Established Markets (e.g., UK, Germany) | Emerging Markets (e.g., Turkey, Dubai) |

|---|---|---|

| Legal framework | Usually clearer, slower-changing and easier to diligence | Can change faster, with higher policy or interpretation risk |

| Rental yield profile | Often lower headline yields in prime cities | Can be stronger, especially outside prestige districts |

| Capital preservation | Typically holds up better in downturns | More sensitive to macro shocks and capital flows |

| Financing access | Deeper mortgage markets, broader lender competition | Often narrower, especially for non-resident buyers |

| Currency exposure | Lower for domestic investors borrowing and earning locally | Can become a major source of gain or loss |

| Exit liquidity | Usually a broader buyer base and easier resale | More variable outside prime locations |

| Operational complexity | More standardised management and compliance systems | Often requires stronger local partners and closer oversight |

A good market is one where income, financing, regulation and exit align.

Where contrarian investors can find resilience

Some of the better risk-adjusted returns sit in neglected segments rather than fashionable postcodes. In the UK, social and affordable housing structures can produce steady income when they are set up correctly and backed by competent operators. The attraction is straightforward. Demand tends to be durable, tenant turnover can be lower in the right structure, and the return profile is often driven more by income security than speculation.

That segment still requires care. Lease terms, covenant strength, maintenance obligations, regulatory oversight and operator quality matter far more than brochure yields. I treat it as an income strategy first, not a shortcut to rapid capital growth.

How this applies across borders

The same framework works in every jurisdiction, but the required margin for error changes. In Germany, an investor may accept a lower starting yield in exchange for legal predictability, tenant depth and cheaper long-term finance. In Turkey or Dubai, the underwriting should demand more upside because currency, policy or execution can move against you faster.

That side-by-side method is what turns global investing from guesswork into process. A disciplined starting point is this guide on where to buy property abroad, then narrowing markets by strategy, financing fit and tax treatment rather than by noise or fashion.

Financing Your Portfolio and Using Leverage Wisely

Across markets, borrowed capital is usually the factor that determines whether an investor compounds steadily or gets forced out early. The same asset can be durable with conservative gearing in Germany, and fragile with aggressive debt in Dubai or Turkey if rates, currency or refinancing terms shift against you.

Debt works well only when the property already stands up on its own merits. Strong locations, resilient tenant demand, and enough cash flow to absorb a dull year matter far more than the cheapest headline rate. I would rather own a plain asset with financing headroom than a fashionable one that only survives under optimistic assumptions.

What borrowed capital actually changes

Borrowing increases returns on equity when rent collection is stable, costs are controlled, and debt remains serviceable. It also widens the consequences of weak underwriting. In practice, the right structure is rarely the one with the highest projected return. It is the one that still holds together if rents soften, a letting takes longer than expected, or refinancing arrives on worse terms.

Three rules travel well across borders:

- Match debt to strategy: Long-term holds suit stable, predictable finance. Refurbishment or repositioning projects need shorter facilities, wider margins, and real contingency.

- Keep liquidity after completion: Mortgage payments are only part of the carrying cost. Repairs, voids, taxes, insurance and delays usually hurt before rate movements do.

- Treat refinancing as upside, not a requirement: If the business plan fails without a perfect refinance window, the structure is too fragile.

Income assets versus active projects

For long-term rental property, conventional buy-to-let debt is often the cleanest option. The cross-border detail matters. If rent is earned in lira, dirhams or euros but the loan sits in sterling or dollars, exchange-rate moves can alter debt service and net cash flow far faster than many first-time international investors expect. That currency mismatch is one reason I compare established markets such as the UK and Germany with higher-volatility markets such as Turkey and Dubai using the same framework, but with a wider margin for error in the latter.

For active strategies, discipline needs to tighten further. Refurbishment finance, bridge lending and short-term facilities can work, but only if the purchase discount, build budget, timing and exit route are all realistic. The commonly used 70% rule in flipping reflects that reality: purchase price plus renovation costs should leave enough room below the expected end value to absorb overruns, finance costs and a slower sale. Performance in this segment is uneven, and this summary of house flipping strategy notes that a meaningful share of operators lose money when markets cool and costs run over.

Financing decisions that separate professionals from speculators

Professionals usually get the structure right before they expand.

| Financing choice | What usually works | What often fails |

|---|---|---|

| Deposit size | Leaves reserves after completion | Commits all available liquidity to the purchase |

| Rate selection | Fits the holding period and downside case | Chases a lower initial rate without proper stress testing |

| Borrowing currency | Matches the rent roll or hedging plan | Creates an unmanaged currency mismatch |

| Entity choice | Fits tax, succession and lender requirements from the start | Gets decided late, under transaction pressure |

| Refurbishment budget | Prices in contingency, delays and cost inflation | Assumes contractors, materials and timing all hold perfectly |

If you are comparing holiday-home and investment borrowing structures, second-home mortgage requirements for international buyers offer a useful reference point for how lenders assess affordability, reserves and risk.

Analysing Deals and Calculating Your Returns

Across property cycles, investors rarely lose money because they misread the brochure. They lose it because they underwrote an asset on optimistic rent, incomplete costs, or an exit that only works in a strong market.

A good deal survives pressure. It still works with a longer void, a higher interest rate, a slower refinance, or a weaker resale market.

Start with yield, then test what the yield is hiding

Gross yield helps you sort opportunities quickly. It does not tell you whether an asset builds wealth.

A recent Zoopla report has continued to show a familiar UK pattern. Lower-priced regions can produce stronger headline yields than prime London, but the investor still has to test arrears risk, tenant depth, maintenance intensity and resale liquidity. The same principle applies globally. A flat in Manchester, a residential block in Berlin, an apartment in Istanbul and a unit in Dubai may all show attractive income at first glance, yet they behave very differently once financing terms, service charges, vacancy periods, currency exposure and tax treatment are included.

That is why I compare established and emerging markets side by side at the same stage of analysis. The question is never just, “Which property yields more?” It is, “Which market gives the better risk-adjusted return after finance, friction and downside scenarios?”

The numbers that matter on every deal

Run the same core tests every time so you can compare markets on a like-for-like basis.

- Gross rental yield: Annual rent divided by total acquisition cost, not just the headline purchase price.

- Net Operating Income: Rent less operating costs such as management, repairs, insurance, service charges, licensing and realistic vacancy.

- Cash flow after finance: NOI less mortgage payments and any other debt costs.

- Cash-on-cash return: Annual pre-tax cash flow divided by the cash you invested, including fees and works.

- Debt service coverage: NOI divided by annual debt service. This shows how much room the property has before the loan becomes uncomfortable.

- Exit margin: The discount or premium you may face on resale, depending on who the next buyer is and how liquid that submarket is.

Use conservative assumptions in year one. Rents often take longer to stabilise than brokers suggest, and operating costs nearly always arrive earlier than expected.

Compare markets by structure, not by headline promise

Established markets usually offer tighter yields, better debt availability and more predictable legal enforcement. Emerging markets may offer stronger income or growth, but often with wider spreads between the best and worst assets.

| Metric | Established market, such as UK or Germany | Emerging market, such as Turkey or Dubai |

|---|---|---|

| Entry pricing | Usually higher | Can be lower or more varied |

| Financing depth | Broader lender pool | More selective, often policy-sensitive |

| Income stability | Often easier to forecast | More dependent on local demand shifts |

| Operating friction | Usually lower and more standardised | Can include currency, licensing or service-charge complexity |

| Exit liquidity | Generally deeper buyer pool | Can narrow quickly if sentiment changes |

That framework stops investors from treating all 8 per cent yields as equal. They are not.

A 5 per cent yield in a market with strong mortgage availability, dependable tenancy law and active resale demand can outperform a nominally higher-yielding asset in a market where financing tightens, currency moves against you, or buyer demand is thin when you need to sell.

A worked comparison investors can actually use

Take two acquisitions with the same equity budget.

The first is a buy-to-let in a mature UK city. The yield is modest, but debt is available on reasonable terms, valuation evidence is easier to support, and resale demand comes from both investors and owner-occupiers. The second is a higher-yield apartment in an emerging market city. The entry price looks attractive, but service charges are heavier, borrowing terms are less forgiving, and your exit may depend on overseas buyers or a narrower local investor base.

On a spreadsheet, the second asset may win on gross yield. On a risk-adjusted basis, the first may produce a better long-term result because financing is cheaper, vacancy risk is lower, and the exit is broader. Sometimes the reverse is true. The point is to test the full capital stack and operating model, not just the rent-to-price ratio.

For investors who want a lender-side view before submitting offers, secure fast real estate investment capital gives a useful overview of how funding structure affects speed, flexibility and execution risk.

Use tools, but keep control of the assumptions

A short explainer can help if you want to refresh the mechanics of return analysis before opening your own spreadsheet.

The biggest underwriting errors are usually omissions, not bad arithmetic. Investors leave out furnishing, travel, local compliance, agency reletting fees, reserve funds, capital expenditure, FX costs, delayed rent-up periods, or the impact of an interest-rate reset. The model still produces a clean return number. The asset itself does not.

If you want a formula-by-formula reference while building your model, this guide to calculating return on investment for property is a practical companion.

Good analysis is repetitive by design. Run the same metrics, apply the same stress tests, and compare every market through the same lens. That discipline is what turns a collection of properties into a durable portfolio.

Mastering Tax, Legal Structures and Risk Management

Cross-border property investors rarely lose money on the spreadsheet first. Returns usually erode through tax leakage, weak legal structuring, regulatory delays and risks that were visible before exchange.

That matters more once you compare markets side by side. A UK buy-to-let, a German apartment block, a Dubai freehold unit and a Turkish rental can all produce acceptable headline returns, but the ownership vehicle, financing terms, tax treatment and enforcement risk are different in each case. Serious investors use one decision framework across all of them, then adapt for local law rather than relying on market-specific habits.

Structure before acquisition

Ownership should be set up before the offer is agreed, not after solicitors are already drafting. Buying in a personal name, through a company, or via a special purpose vehicle changes lender appetite, liability, reporting, succession planning and the tax position on both income and exit.

The right structure depends on scale, residency, holding period and the country where profits will ultimately be taxed. In the UK, company ownership may improve interest deductibility for some investors but can introduce extra administrative cost. In Germany, the legal form can affect transfer tax exposure and disposal planning. In Dubai, foreign ownership rules and free zone structures need to be checked against the intended use of the asset. In Turkey, title, currency exposure and repatriation procedures need the same level of scrutiny as the purchase price.

Home-country reporting also continues after completion. Double tax treaties can reduce duplication, but they do not remove filing obligations, local withholding, beneficial ownership checks or anti-money-laundering requirements. That is where experienced local counsel and a tax adviser usually save far more than they cost.

Keep a live compliance file for every asset. Include title documents, financing covenants, insurance terms, licensing requirements, beneficial ownership records, local tax registrations and filing deadlines. Investors who run this discipline portfolio-wide make better decisions because the operational reality is visible before a problem becomes expensive.

Regulatory risk changes the return

Planning and licensing rules can alter a strategy faster than rent growth can repair it. Short-term lets are the clearest example. In England, the government consultation on a registration scheme for short-term lets, published on GOV.UK, sits alongside reforms under the Levelling Up and Regeneration Act, with further implementation scheduled from 2025. For investors, the lesson is straightforward. A high-yield use case is only valuable if it remains lawful, financeable and insurable.

I apply the same test in every market. Before assuming premium nightly income in Edinburgh, Istanbul or Dubai, confirm the permissions, building rules, management restrictions and tax treatment attached to that use. If any one of those points is uncertain, underwrite the asset on a conventional long-let basis and treat the short-term upside as optional, not required.

The risks that deserve constant attention

- Interest-rate risk: Match debt terms to the business plan. Assets that need time to stabilise should not depend on a near-term refinance in a hostile rate environment.

- Currency risk: If rental income, debt service and investor reporting sit in different currencies, set a policy in advance. Some portfolios need hedging. Others need a cash buffer and conservative loan sizing.

- Legal risk: Confirm title, permitted use, tenant law, licensing and enforcement routes before exchange. Cross-border investors should be especially careful where contract enforcement is slow or documentation standards vary.

- Operational risk: Local managers determine arrears control, maintenance quality, tenant retention and compliance. Weak execution can turn a sound acquisition into a persistent underperformer.

- Tax leakage: Withholding tax, transfer taxes, VAT exposure, capital gains treatment and poor expense capture can reduce net returns more than a modest vacancy increase.

The boring controls preserve capital.

For investors tightening record-keeping and allowable cost capture, top tax deductions for investors is a useful reference to review with an adviser before year-end filings.

Conclusion Your Path to Generational Wealth

Property builds wealth slowly, then visibly. The formula isn’t mysterious. Buy in markets with real demand. Finance acquisitions responsibly. Analyse every deal with conservative assumptions. Protect what you build through sound legal and tax structuring.

That’s how to build wealth through property investment in a way that survives market cycles and supports long-term goals. The investors who create generational wealth don’t rely on hype. They stack good decisions, hold quality assets, and give time a chance to work.

Frequently Asked Questions

How much capital do I need to start?

There isn’t one universal number because the answer depends on market, financing access and strategy. A conservative investor should think beyond the deposit and include closing costs, setup costs and a meaningful cash buffer. If buying abroad, add legal, translation, banking and travel friction to your planning. Starting with enough liquidity is usually more important than starting quickly.

Should I prioritise rental yield or capital growth?

Neither in isolation. Strong wealth creation usually comes from balancing both. If you chase yield alone, you may buy in weak locations with management headaches and poor resale demand. If you chase growth alone, you may hold an asset that drains cash and limits your ability to expand. The better question is whether the asset’s total return fits your objective and risk tolerance.

Is buy-to-let better than flipping?

For most investors, buy-to-let is the more forgiving route because it gives you time. Time to refinance, time to improve management, and time for the market to recover from short-term weakness. Flipping can work, but it compresses every risk into a shorter holding period. That means budgeting, contractor control and exit timing all matter more.

Can I invest successfully in another country?

Yes, but distance magnifies weak process. Foreign investors need sharper local due diligence, stronger legal support and reliable in-country management. A market can look excellent on paper and still disappoint if title, tax, lettings rules or exit liquidity are misunderstood. The further you are from the asset, the more you need systems rather than instinct.

What type of property is best for a first investment?

The best first asset is usually the one that is easiest to understand, finance and manage. In practice, that often means standard residential stock in a location with durable rental demand. Complex mixed-use buildings, heavy refurbishment projects or tightly regulated short-term let models can produce good returns, but they leave less room for beginner mistakes.

Should I manage the property myself?

If the asset is close, straightforward and you want operational experience, self-management can make sense. If the property is overseas, management quality becomes part of the investment thesis. In that case, I’d rather pay for a competent manager than pretend remote ownership is passive.

If you’re comparing countries, yields, taxes and buying rules before making your next move, World Property Investor is a strong place to continue your research. It brings together market guides, country comparisons and practical buying analysis for investors building portfolios across established and emerging markets.