You've found a promising rental flat in Manchester, a holiday unit in Spain, or an apartment in Dubai. The property makes sense on paper. The financing often doesn't.

That's where most investors lose time and money. They chase the asset first, then discover the loan product, lender rules, tax treatment, and cross-border paperwork don't match their plan. A strong deal with weak finance is still a weak deal.

The best investment property loans are the ones that fit your strategy, your tax position, and your ability to hold through rate pressure. Cheap debt isn't always best. Flexible debt often wins. For global investors, the right loan also depends on where you live, where you earn, and whether a lender can underwrite foreign income without turning your application into a bureaucratic mess.

Securing Finance Your Global Investment Blueprint

If you're buying outside your home country, treat finance as part of deal selection, not an admin task at the end. That one shift will save you months.

Start with three questions.

- What's the property for. Long-term let, holiday let, capital growth hold, or value-add project.

- Who will own it. You personally, jointly, or through a company.

- Which lender type matches that plan. Mainstream bank, specialist buy-to-let lender, or private/commercial route.

Most investors make the same mistake. They compare headline interest rates and ignore underwriting logic. That's backwards. A lender that understands rental income and portfolio growth is often more useful than one advertising a lower rate but rejecting perfectly good deals.

The UK is a good example because the rules are clearer and more formalised than in many overseas markets. Spain and Dubai can still offer attractive opportunities, but financing there can be more relationship-driven, more document-heavy, and more dependent on lender appetite at the time you apply. You need to know the lending culture as much as the market.

Practical rule: Choose the market first, then choose the ownership structure, then shortlist lenders. Don't reverse the order.

A simple finance blueprint looks like this:

- Define your target return: Decide whether you care more about monthly cash flow or long-term appreciation.

- Set your real budget: Include deposit, lender fees, legal costs, tax, and a cash buffer.

- Match loan type to strategy: A standard buy-to-let mortgage suits a straightforward rental. A specialist product may suit a portfolio landlord or foreign buyer better.

- Prepare documents early: ID, proof of income, bank statements, tax records, and evidence of deposit should be organised before you offer.

- Get market-specific guidance: If you're buying overseas, read a country-specific buying guide such as how to buy property abroad before speaking to lenders.

The investors who finance well aren't guessing. They build a repeatable process and use debt deliberately.

Understanding the Core Investment Loan Products

The phrase best investment property loans usually gets reduced to rate shopping. That's lazy analysis. Product type matters more than the headline rate because each loan is built for a different investor profile.

In practice, most investors will encounter three broad categories first. Buy-to-let mortgages, interest-only structures, and portfolio-style lending.

Buy-to-let mortgages

A buy-to-let mortgage is the core product for residential investment property in the UK. It's built around rental income rather than owner-occupier affordability.

As of Q1 2026, the average interest rate for a 2-year fixed UK buy-to-let mortgage is 5.42%, with typical deposits of 25 to 40% and rental coverage requirements of 125 to 145% of mortgage interest payments, based on stressed affordability tests, according to Bankrate's summary of UK investment property lending criteria. The same source notes that a £300,000 property at 75% LTV would need projected monthly rent of at least £1,250 to qualify under typical lender criteria.

That tells you two things immediately. First, this market is income-tested through the property itself. Second, financing is available, but it isn't freely granted.

For most first-time landlords, a straightforward buy-to-let mortgage is still the cleanest starting point. If the property has stable rental demand and you've got the deposit, don't overcomplicate it.

If you're still learning the lender side of second-home and rental borrowing, review these second home mortgage requirements before applying. The distinction between personal-use and investment-use borrowing matters more than many buyers realise.

Interest-only loans

An interest-only mortgage keeps monthly payments lower because you pay interest during the term and repay the capital later, usually by sale, refinance, or another exit strategy.

That can improve cash flow. It can also create false confidence.

Interest-only works best when you have a clear plan. Investors using it well usually fit one of these profiles:

- Yield-focused landlords: They want lower monthly outgoings and stronger surplus cash flow.

- Short-to-medium term holders: They expect to refinance or sell rather than hold debt unchanged for decades.

- Investors preserving liquidity: They prefer to keep capital available for deposits, refurbishments, or reserve funds.

It's a useful tool, not a shortcut. If your whole strategy depends on prices rising quickly, your financing is fragile.

Interest-only is a cash-flow tool. It isn't a substitute for an exit plan.

Portfolio loans

A portfolio loan is less about one asset and more about your broader book of properties. Some lenders assess your portfolio strength, aggregate rental income, and management track record rather than viewing each property in isolation.

This route suits investors who already own multiple rentals and want simpler scaling. It can also help when one or two properties in the portfolio are awkward by mainstream standards, but the overall portfolio is strong.

These facilities are usually more flexible than standard retail mortgages. They also require cleaner reporting. If your accounts, tenancy records, and ownership structure are messy, lenders will notice immediately.

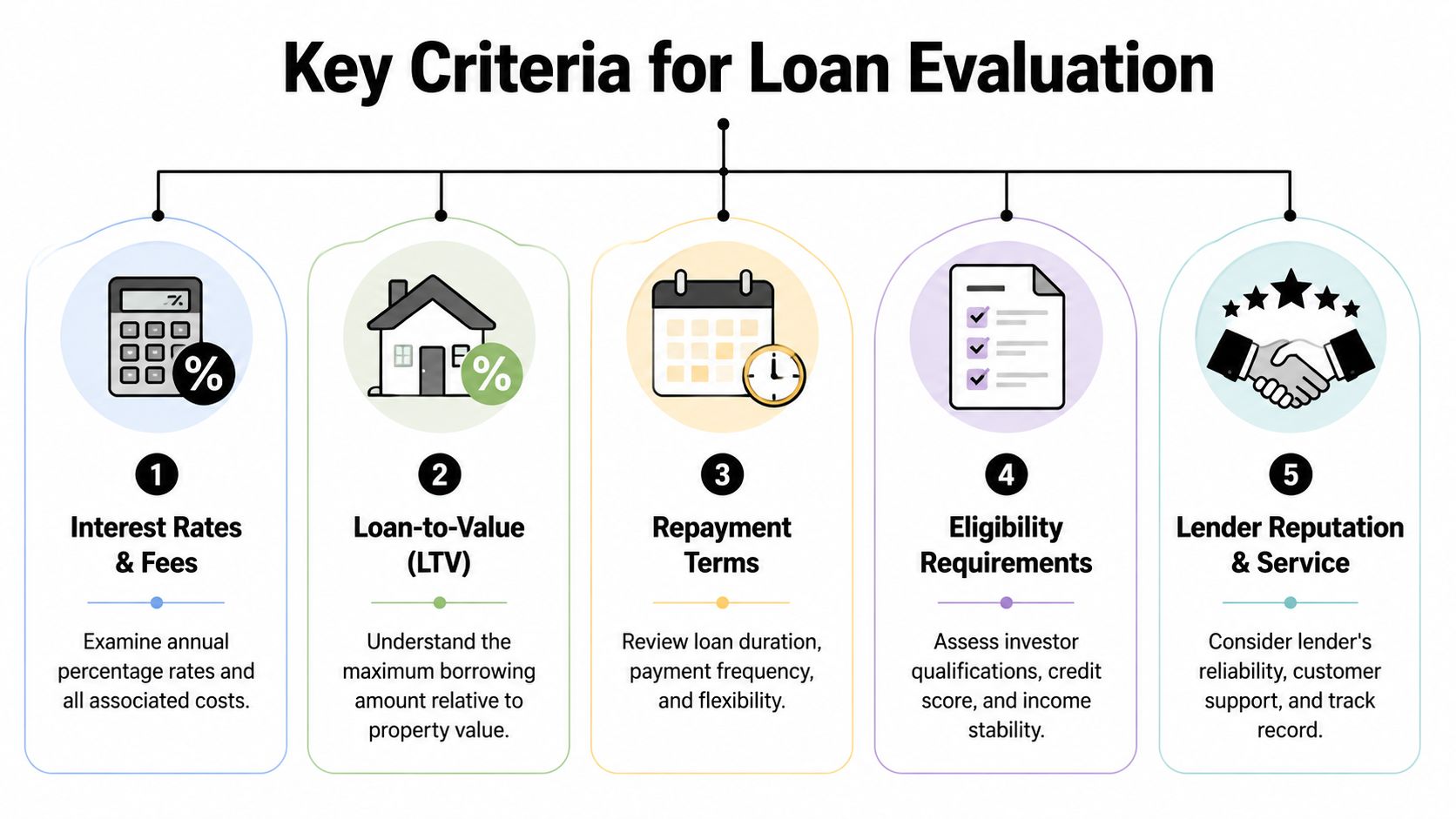

The Key Criteria for Evaluating Loan Offers

Most loan comparisons are superficial. Investors look at the rate, glance at the monthly payment, and stop there. That's not enough. You need to assess how the entire loan behaves under pressure.

LTV and the deposit question

Loan-to-value, or LTV, determines how much of the purchase price the lender will fund and how much cash you must contribute.

Higher LTV gives you more financial power. It also gives the lender more reason to scrutinise the deal. For investors, this isn't just about how much cash you can put down. It's about whether using more debt improves your return without making the deal too tight.

If the rental margin is thin, aggressive use of borrowed funds can hurt rather than help. If the property has resilient demand and room in the numbers, the use of borrowed funds can support faster portfolio growth.

Rate type and payment risk

A low starting rate isn't automatically attractive. What matters is whether the payment structure matches your hold period.

Use this practical lens:

- Fixed rate: Better for investors who want payment certainty and hold for income.

- Variable rate: More flexible, but exposed to market movements.

- Tracker-style structure: Useful only if you understand what drives the reference rate and can tolerate movement.

A lot of borrowers fix because it feels safe. That's reasonable. But if your plan is to renovate, refinance, or sell in the near term, flexibility may matter more than certainty.

Fees and friction costs

Arrangement fees, valuation fees, legal fees, broker fees, and early repayment charges can change the actual cost of a loan materially.

A lower rate with punitive fees may be worse than a slightly higher rate with simpler terms. Read the offer letter carefully. If you can't explain the total cost in plain English, you don't understand the loan well enough yet.

Decision test: Compare total borrowing cost over your expected hold period, not just the initial rate.

Serviceability and affordability

Lenders don't just ask whether you can afford the loan today. They ask whether the property can withstand a tougher environment.

That's where rental stress testing, interest cover, and your wider obligations come in. Your debt burden outside the property still matters, especially with mainstream lenders. If you want a clear primer on how DTI impacts home loans, that framework helps explain why some borrowers look strong on income but still fail credit underwriting.

For investors, serviceability should be tested in your own spreadsheet too. Don't rely on the lender's minimum pass. Model the property with voids, maintenance, and higher financing costs. If the deal only works in ideal conditions, reject it.

Tax and ownership consequences

The loan isn't separate from tax. It never was.

When you compare offers, consider:

- Ownership route: Personal ownership and company ownership can produce very different after-tax outcomes.

- Deductibility: The treatment of mortgage interest can alter net returns sharply.

- Exit implications: Refinance, sale, and inheritance planning all sit downstream of the original borrowing decision.

A sensible investor chooses the loan after looking at the entire holding structure, not before.

| Criterion | What to check | Why it matters |

|---|---|---|

| LTV | Maximum borrowing and required deposit | Controls leverage and cash tied up |

| Rate type | Fixed, variable, or flexible structure | Affects payment certainty |

| Fees | Arrangement, legal, valuation, exit charges | Changes true cost of borrowing |

| Serviceability | Rent cover, income review, stress tests | Determines approval and resilience |

| Tax fit | Personal or company borrowing | Shapes net return, not just gross yield |

Comparing Lenders and Markets A Global Perspective

The right lender in the wrong market still creates a bad outcome. So does the wrong lender in the right market. Investors need to compare both at the same time.

High Street banks versus specialist lenders

In the UK, mainstream banks tend to suit borrowers with clean income, simple structures, and straightforward properties. They often want more conventional documentation and a predictable borrower profile.

Specialist lenders are often the better option for portfolio landlords, company borrowers, and non-residents. They can be more expensive. They can also be far more useful.

UK Finance data from Q1 2026 shows that DSCR buy-to-let loans achieve average LTVs of 75 to 80%, compared with 65 to 70% for conventional buy-to-let loans from mainstream banks, as noted in UK Finance data and research. For investors trying to scale, that difference matters. A lender focused on property cash flow can open doors that a salary-based underwriter will close.

My view is simple. If you're buying your first standard rental and your income is easy to prove, start with mainstream options. If you're building a portfolio, buying via a company, or applying as a foreign investor, go to specialists early and save yourself the false starts.

Established versus international lending environments

The UK remains one of the easier markets to analyse because the mortgage framework is familiar, the legal system is established, and the buy-to-let product set is mature. That doesn't make borrowing easy. It makes it understandable.

Spain and Dubai are different propositions.

Spain often appeals to lifestyle-led investors and holiday-let buyers. Dubai attracts yield-seekers and investors who want exposure to a fast-moving international hub. In both cases, foreign buyers should assume extra document checks, more scrutiny around source of funds, and less standardisation than in the UK.

If you're assessing Iberian opportunities, review current mortgage rates in Spain before you compare expected returns against UK deals. Too many investors compare asset prices and ignore financing friction.

The easiest market to buy in isn't always the most profitable. The hardest market to finance often looks better in estate agent brochures than it does in a lender's credit committee.

International Investment Loan Feature Comparison

| Feature | United Kingdom | Spain | Dubai (UAE) |

|---|---|---|---|

| Lender landscape | Mature buy-to-let market with mainstream and specialist lenders | More bank-led and documentation-heavy for foreign buyers | International buyer market with lender appetite varying by profile |

| Foreign investor process | Structured, but strict on income proof and affordability | Can be slower and more document-intensive | Often efficient in practice, but lender selection is critical |

| Best fit for | Long-term landlords, portfolio builders, company structures | Lifestyle investors and selective holiday-let buyers | Investors prioritising international exposure and flexible market entry |

| Key challenge | Stress testing and tax-efficient structuring | Documentation, local bank requirements, and slower underwriting | Matching the right lender to residency and income profile |

| Adviser view | Best for disciplined, numbers-first investing | Best for buyers who understand local demand deeply | Best for experienced investors comfortable with market cycles |

The comparison isn't about declaring one winner. It's about fit.

If you want regulation, transparency, and scalable finance, the UK is still hard to beat. If you want a personal-use angle alongside investment, Spain can work. If you want international diversification and a different demand profile, Dubai deserves attention. But in Spain and Dubai, poor local advice can cost you more quickly.

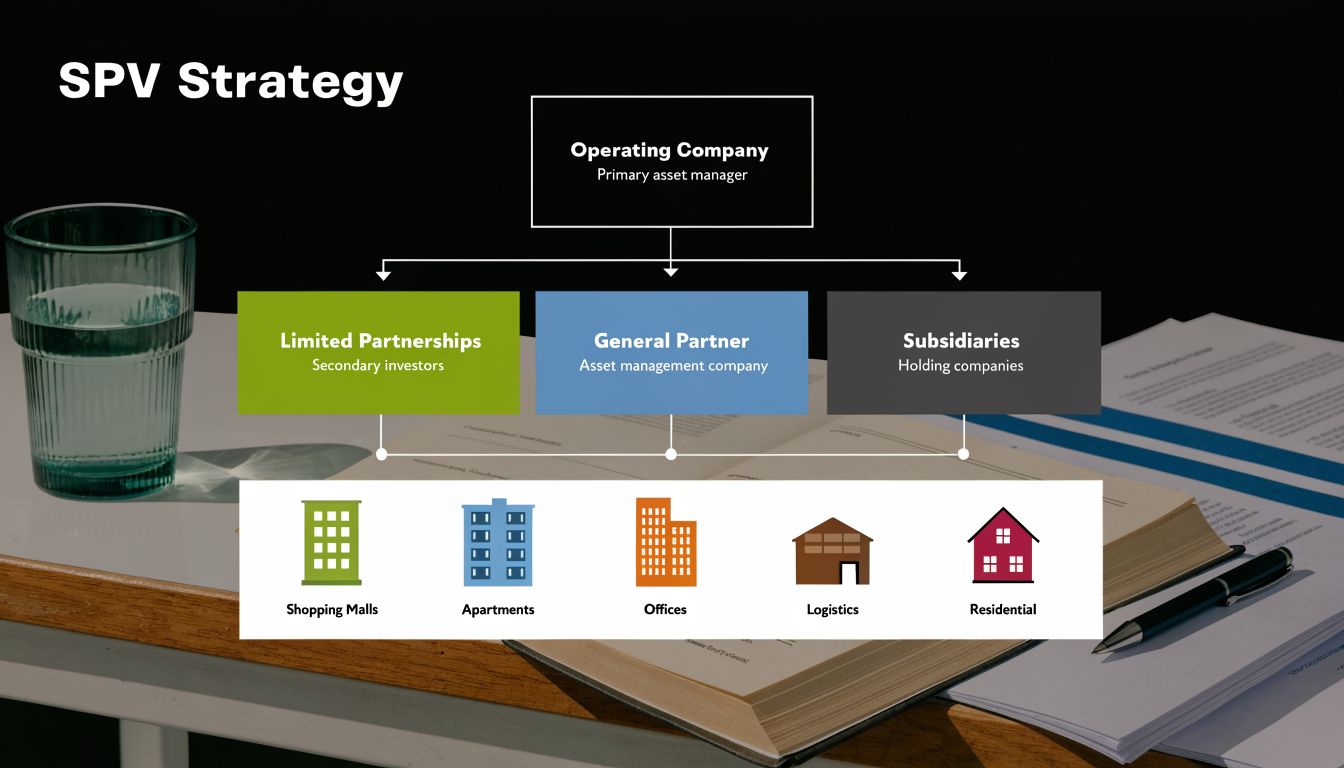

Advanced Strategy Using a Limited Company for Property

For many serious investors, personal ownership stopped being the obvious answer years ago. In the UK especially, limited company buy-to-let has become the default route for anyone thinking beyond a single rental.

According to Mashvisor's summary of UK buy-to-let lending trends, 68% of all UK buy-to-let purchases in 2025 were made via limited companies, up from 42% in 2017. The same source attributes that shift to investors responding to Section 24 tax relief restrictions and the ability to deduct mortgage interest as a business expense, with profits taxed at corporation tax rates of 19 to 25% rather than personal income tax rates of up to 45%.

That trend didn't happen by accident. Investors ran the numbers and changed behaviour.

Why the company route appeals

The biggest advantage is tax efficiency for the right borrower profile. If you're a higher-rate taxpayer, personal ownership can become unattractive quickly once finance costs and rental profits are fully analysed.

A limited company structure can also make portfolio management cleaner. You separate the investment activity from your personal finances, and lenders dealing with professional landlords are used to this setup.

That doesn't mean everyone should rush into an SPV.

Use the company route when these factors apply:

- You plan to scale: One or two rentals can be held personally in some cases, but portfolio expansion often favours a company structure.

- You're a higher-rate taxpayer: The tax difference can be meaningful.

- You want clearer ring-fencing: Company ownership can simplify administration and planning.

If you're at the point of setting up a vehicle, use proper legal and tax advice first. Administrative services such as OnBiz llc formation service can help with entity setup workflows generally, but UK property investors still need structure-specific advice on company formation, lender acceptance, and tax treatment before proceeding.

The trade-offs investors ignore

Running a company adds compliance, accounts, filings, and lender-specific rules. Some lenders price company borrowing differently. Some solicitors move slower when structures get more complex. Some borrowers save tax and then lose part of that gain through poor administration.

Advisor's view: A limited company is powerful when it supports a long-term plan. It's wasteful when it's set up just because other landlords are doing it.

Before choosing this route, calculate the full picture:

- Mortgage availability

- Accounting costs

- Directors' guarantees or personal support

- Future refinancing flexibility

- Stamp duty implications

For UK buyers running the ownership comparison, a stamp duty calculator for limited companies is a practical starting point because transaction costs can change the deal from day one.

This short explainer is useful if you want a visual overview before speaking to your accountant or broker:

The company route isn't fashionable. It's functional. For the right investor, that's enough.

Navigating Cross-Border Finance as a Foreign Investor

Foreign investors often assume the hardest part is choosing the country. It usually isn't. The hardest part is proving yourself to a lender that doesn't know your employer, doesn't understand your tax documents, and has no reason to make exceptions.

The UK is a useful case study because overseas demand is real, but lenders still apply a tougher filter. According to HMRC guidance on UK rental income for people living abroad, non-UK resident buy-to-let lending grew 18% year-on-year in 2025, yet approval rates were only 62% for overseas applicants compared with 78% for UK residents. The same verified data states that proof of income is a major hurdle and that, under HMRC's Non-Resident Landlord Scheme, 20% tax is withheld on rental income unless an exemption is secured.

Such is the case. Cross-border finance is available. It just punishes poor preparation.

What overseas applicants need to fix first

Most non-resident applications fail for boring reasons. Documents aren't in the right format. Income evidence doesn't translate cleanly. Currency exposure isn't explained. The lender asks for one extra item and the deal drifts.

Focus on these basics:

- Income clarity: Foreign salary, business income, or dividends must be easy to verify.

- Source of deposit: Lenders and solicitors will want a clean audit trail.

- Tax registration: In the UK, deal with non-resident landlord requirements early.

- Credit narrative: If you have limited local credit history, explain the wider financial picture clearly.

If you're buying a rental from overseas, read a specialised guide to international buy-to-let before speaking to lenders. Generic mortgage advice usually falls apart once foreign income and tax residency enter the picture.

Why specialist brokers matter more here

A local branch adviser rarely solves a cross-border case well. You need a broker or lender team that handles foreign nationals, expats, and overseas income routinely.

Good cross-border advisers do three useful things. They know which lenders accept which jurisdictions. They know how to package income evidence properly. They know when a case is weak and how to restructure it before submission.

That saves time. More importantly, it protects your credibility. Every failed application can create more friction on the next one.

Get your documents lender-ready before reserving the property, not after. Cross-border underwriting slows down when the paperwork is merely adequate.

The practical advantage for prepared buyers

Foreign investors who prepare properly can still use financing as an edge. A financed buyer with organised documents and a broker who understands the case will often move more effectively than a cash buyer who hasn't dealt with tax, banking, and transfer logistics.

That's why I don't advise overseas buyers to avoid using debt by default. I advise them to avoid amateur applications.

Your Investment Loan Checklist and Next Steps

A good property loan supports the deal. A bad one controls it. Keep your process disciplined and investor-specific.

First-time investor

- Keep the structure simple: Start with a standard rental and a lender that understands straightforward buy-to-let.

- Protect your cash buffer: Don't use every pound for deposit and fees.

- Stress test the rent: Make sure the property still works with voids and repairs.

- Get advice early: A broker can tell you quickly whether your profile fits mainstream or specialist lenders.

Portfolio builder

- Choose lenders by scalability: Flexibility often matters more than the cheapest initial rate.

- Review ownership structure: Personal ownership may stop making sense as the portfolio grows.

- Standardise your records: Rent schedules, accounts, tenancy files, and deposit evidence should be clean.

- Think in groups, not singles: Finance decisions should work across the portfolio, not just on one asset.

International or expat investor

- Prepare income documents properly: Don't assume foreign statements will be accepted as-is.

- Handle tax status immediately: Non-resident withholding issues can reduce returns if ignored.

- Use market-specific brokers: Cross-border lending is not a generic mortgage exercise.

- Match currency exposure to your strategy: If your income and debt sit in different currencies, build in margin.

Universal next steps

Before you make a serious offer:

- Clarify your target market and holding strategy

- Decide whether to buy personally or through a company

- Assemble your documents before approaching lenders

- Compare loan offers on structure, fees, and flexibility, not rate alone

- Get an agreement in principle or equivalent early

The best investment property loans aren't the flashiest products. They're the ones that let you buy well, hold confidently, and scale without constant refinancing drama.

If you're comparing markets, yields, taxes, and financing routes across countries, World Property Investor gives you a practical base for doing that work properly. Use it to narrow markets, understand local buying rules, and approach lenders with a strategy instead of a guess.