You're probably in the same position as many first-time international buyers. You like the idea of owning something tangible, you want income as well as long-term upside, and you've realised that “buy where everyone else is buying” isn't a strategy.

A good guide to property investment starts with a simple shift in mindset. You are not buying a flat, villa, or block because it feels solid. You're buying an income stream, a future resale position, and a package of legal obligations in a specific market.

That's why experienced investors compare deals with a consistent framework. The country matters. The city matters more. The street, financing terms, tax treatment, and exit route matter most.

Why Invest in Property A Primer for Global Investors

Property attracts investors for two reasons that rarely arrive in equal balance. The first is income, usually through rent. The second is capital appreciation, which depends on what a future buyer will pay. Some markets offer steady rent and modest growth. Others offer stronger growth potential but weaker current cash flow.

For global investors, that split is useful. Property doesn't have to do one job only. A mature city-centre apartment might serve wealth preservation. A regional rental in a lower-cost market might serve income. A development site might be a higher-risk play on future value.

Why the asset class still appeals

Unlike many financial assets, property is easy to understand at an operational level. Tenants need homes. Businesses need premises. Infrastructure, jobs, schools, and transport shape demand in ways you can study directly.

That said, simplicity at a distance is deceptive. International property investment is really a chain of decisions about debt, law, tax, management, and timing. The asset is physical. The analysis must still be rigorous.

Practical rule: Treat every property purchase as a business acquisition with a local operating model.

A beginner often asks, “Where should I buy?” A better question is, “What am I trying to achieve, and which market structure gives me the best chance of achieving it?” That one change filters out most bad deals.

What property does well, and what it doesn't

Property can work well when you want:

- Income with asset backing: Rent can provide ongoing cash flow while the underlying property retains long-term value.

- Control over performance: You can improve lettings, presentation, layout, and management. That's different from passively owning a share.

- Portfolio diversification: Real estate behaves differently from many paper assets, especially across countries and sectors.

It works less well if you need instant liquidity, hate operational issues, or plan to rely on optimistic appreciation to rescue weak cash flow.

If you want a broader foundation on the wealth-building side, this guide on how to build wealth through property investment is a useful next read.

Understanding the Core Property Investment Strategies

Most investors don't fail because they choose the wrong country. They fail because they choose a strategy that doesn't match their time, risk tolerance, or skill set.

Buy-to-let and long-term rental income

This is the most familiar model. You buy a property and let it on a standard tenancy, aiming for predictable occupancy and manageable operating costs.

The strength of buy-to-let is clarity. You can usually assess tenant demand by looking at employment centres, transport links, university catchments, and local supply. The weakness is that many new investors stop at gross rent and ignore financing, repairs, regulation, and voids.

If you want a sharper definition of the model itself, buy-to-let definition is worth reviewing before you look at live deals.

Short-term and holiday lets

Short-term rentals can produce higher gross income in the right location, especially where tourism, seasonal events, or executive travel support premium nightly pricing. But they behave more like a hospitality business than a passive investment.

You need to think about:

- Operational intensity: Cleaning, guest communication, pricing updates, and platform management are constant tasks.

- Regulatory exposure: Cities often tighten rules quickly where short-term lets reduce housing supply.

- Income volatility: Occupancy can fluctuate with seasonality, local competition, and travel trends.

This model works best for investors who either operate professionally or hire competent local managers.

Flipping and value-add resale

A flip is not just “buy cheap, sell dear”. In practice, it's a race against time, budget creep, planning delays, contractor quality, and buyer sentiment at the moment you exit.

A value-add deal can still be attractive when the investor has a real edge. That might mean sourcing off-market stock, understanding renovation economics, or knowing how buyers in that submarket value layout, energy efficiency, and finish level.

A bad buy-to-let often limps along. A bad flip can destroy capital quickly.

Development and indirect property exposure

Development sits further up the risk curve. You're taking planning, construction, funding, and exit risk together. Returns can be strong, but the margin for error is thinner than many first-time investors realise.

At the other end of the spectrum are REITs and property funds. These suit investors who want exposure to real estate without handling tenants, maintenance, or local compliance. You lose some direct control, but you gain simplicity and usually better diversification.

A simple way to think about strategy is this:

| Strategy | Main goal | Management load | Typical risk profile |

|---|---|---|---|

| Buy-to-let | Stable income | Moderate | Moderate |

| Holiday let | Higher cash flow | High | Moderate to high |

| Flip | Capital gain | High | High |

| REITs/Funds | Passive exposure | Low | Market-dependent |

Calculating Returns Key Metrics for Smart Decisions

Investors often overcomplicate the maths, then make decisions on instinct anyway. Don't do that. A useful guide to property investment should leave you able to test a deal quickly and reject weak ones early.

Gross yield is the first filter

Gross rental yield is commonly calculated by dividing annual rent by purchase price. It's a blunt tool, but it helps you compare markets and shortlist assets fast.

Example:

- Purchase price: £200,000

- Annual rent: £12,000

Gross yield = £12,000 ÷ £200,000 = 0.06, or 6%

That tells you very little about actual profit, but it tells you where to look next.

Net yield is closer to reality

Net yield asks a better question. What's left after real operating costs?

Use this basic structure:

- Start with annual rent.

- Subtract operating costs such as insurance, maintenance, management, licensing, and expected vacancy allowance.

- Divide the remaining figure by total acquisition cost or purchase price, depending on your comparison method.

Worked example:

| Item | Amount |

|---|---|

| Annual rent | £12,000 |

| Insurance | £600 |

| Maintenance reserve | £1,200 |

| Management | £1,200 |

| Expected void allowance | £600 |

| Net operating income | £8,400 |

If the purchase price is £200,000, net yield = £8,400 ÷ £200,000 = 4.2%

That's the difference between a listing brochure and a business decision.

ROI measures how efficiently your cash works

Return on investment asks whether the cash you personally put in is earning enough. For deals involving borrowed capital, that matters more than the headline yield.

A simple version is:

ROI = annual profit ÷ total cash invested

Suppose you invest:

- Deposit: £50,000

- Legal and buying costs: £8,000

- Initial works: £7,000

Total cash invested = £65,000

If annual profit after operating costs and finance is £5,200, ROI = £5,200 ÷ £65,000 = 8%

That's not a universal benchmark. It's a decision tool. You compare it with your risk, management burden, and alternatives.

For investors who want to go one step deeper, cash-on-cash return is another key real estate investment metric, particularly when debt is involved.

Investor check: If the deal only works when nothing goes wrong, the deal doesn't work.

If you want a dedicated walkthrough, this guide on how to calculate return on investment property is a good companion to your own underwriting spreadsheet.

Financing Your Purchase and Managing Hidden Costs

The use of debt can improve returns, but it also exposes every weakness in the deal. When debt is cheap, many properties look viable. When debt is expensive, weak underwriting shows up fast.

In the UK, that pressure has been obvious. The Bank of England held Bank Rate at 5.25% for much of 2024 before cutting to 5.0% in August 2024, while the ONS reported UK private rental prices rising 8.7% year on year in March 2025, which shows the tension between borrowing costs and rental growth in the same market (analysis of UK financing pressure and rental growth).

What leverage actually does

Debt magnifies outcomes. If rents are strong, costs are controlled, and the property appreciates, borrowing can lift your return on equity. If rates rise, rents stall, or repairs arrive early, borrowing can turn an acceptable asset into a monthly liability.

That's why lenders matter as much as rates. International buyers should expect deeper scrutiny around income proof, source of funds, tax residence, credit history, and the property's own income profile. Some lenders are comfortable with overseas borrowers. Others aren't.

Before you apply, it helps to understand your own ratios. This overview of how to calculate debt to income gives you the same lens many lenders use.

The costs beginners miss

Most bad first deals don't collapse because the investor forgot the rent. They collapse because the investor undercounted the friction.

Common hidden costs include:

- Acquisition taxes: Stamp duty or local transfer taxes can materially change your true entry price.

- Finance fees: Arrangement fees, valuation fees, broker fees, and legal charges often arrive before completion.

- Operational leakage: Insurance, maintenance, licensing, service charges, and management costs reduce net income.

- Dead periods: Void periods and arrears don't show up in optimistic projections, but they affect cash flow immediately.

- Exit costs: Selling fees, legal fees, and possible tax liabilities shape your real return, not just your paper gain.

Stress-testing before you buy

A disciplined investor runs the numbers three ways:

| Scenario | Rent assumption | Cost assumption | Purpose |

|---|---|---|---|

| Base case | Current market rent | Normal running costs | Initial viability |

| Conservative case | Slightly softer rent | Higher maintenance and voids | Downside resilience |

| Refinance case | Future debt terms uncertain | Include fee drag | Medium-term planning |

This video is a useful primer on the financing mindset investors need before they commit capital.

If the property only remains cash-flow positive in the best-case version of your spreadsheet, step back. International investing gives you enough uncertainty already. You don't need to manufacture more through aggressive assumptions.

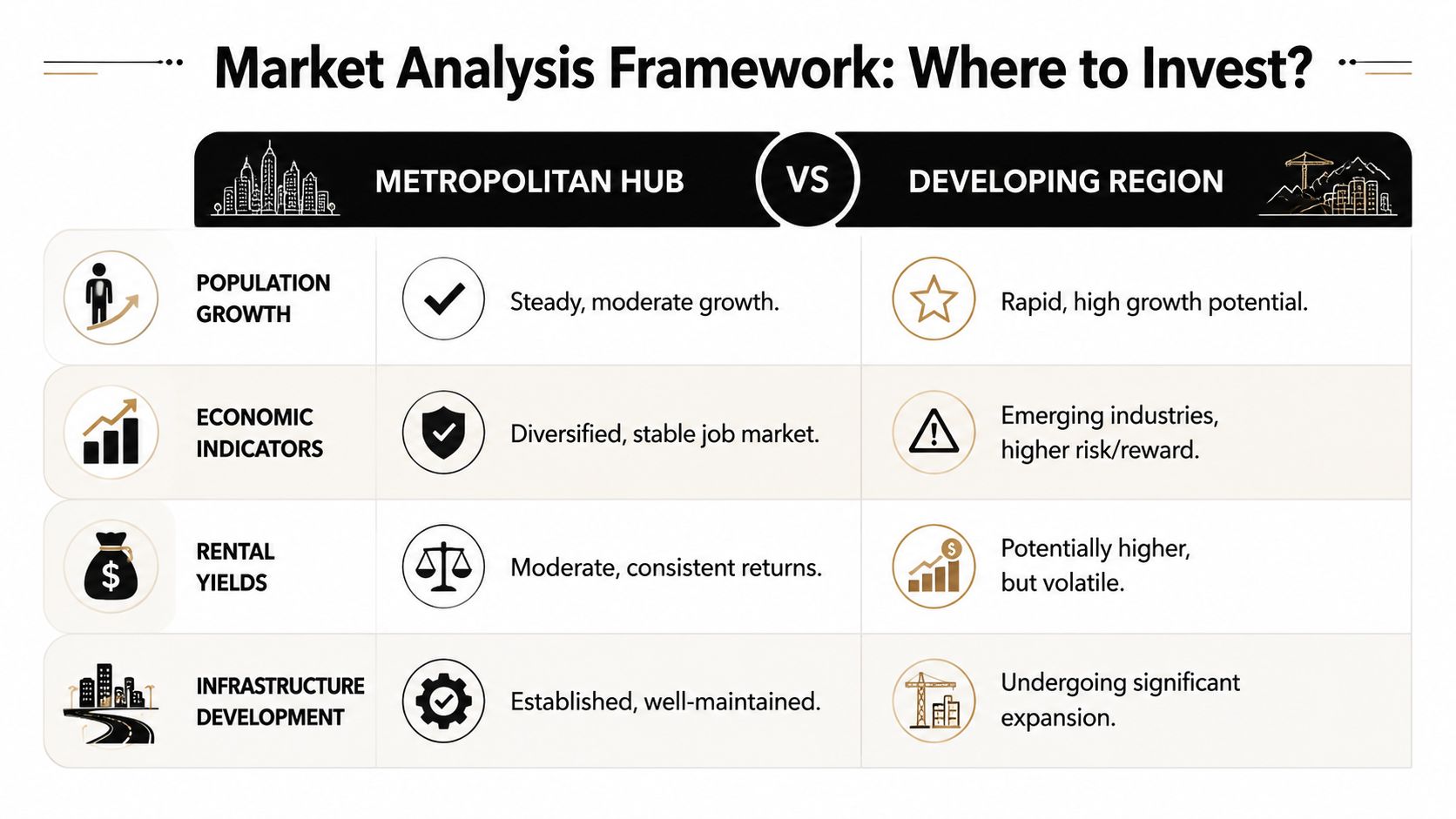

Choosing Where to Invest A Framework for Market Analysis

Location analysis is where disciplined investors separate from hopeful buyers. A mature market and an emerging market can both be attractive, but not for the same reasons and not under the same underwriting assumptions.

In the UK, the average house price was about £289,000 in 2024, and official data showed annual price growth moving from negative territory into positive growth during 2024. That matters, but it doesn't replace local underwriting. Professional analysis still starts with local price trends, local rent, and financing costs, not national headlines (UK property analysis and regional pricing context).

The four-pillar framework

When comparing markets, I focus on four pillars.

Economic drivers

Look for diverse employment, not a one-industry story. A city supported by finance, education, healthcare, logistics, and technology usually absorbs shocks better than one relying on a narrow base.

Questions to ask:

- Who employs tenants or buyers here?

- Is demand owner-led, renter-led, or tourism-led?

- Does the local economy depend on one large employer or sector?

Demographics

Population growth is useful, but the composition matters more. Students, young professionals, retirees, and transient workers all create different housing demand and tenancy patterns.

A city can grow and still disappoint investors if the new supply targets the same tenant base you're chasing.

Infrastructure and connectivity

Transport links, regeneration zones, digital infrastructure, and employer relocation plans often shape future demand well before price charts make it obvious.

Buy where daily life is getting easier for residents. Commutes, access, and liveability usually show up in rents before they show up in resale prices.

Entry price versus exit depth

High-growth narratives often distract from the most practical question. If you need to sell in an awkward year, who is the buyer? A local owner-occupier, another investor, an overseas buyer, or almost nobody?

That exit depth matters. It's one reason mature markets still attract cautious capital even when headline yields look less exciting.

Mature market versus emerging market

Here's the practical contrast.

| Factor | Mature market such as the UK | Emerging region |

|---|---|---|

| Entry environment | More transparent, often more expensive | Lower entry cost in some areas, but more variability |

| Income profile | Can be steadier in proven rental corridors | Can be stronger on paper, but less predictable |

| Legal certainty | Usually clearer and better documented | Often requires deeper local advice |

| Financing access | Broader lender ecosystem | May be more limited for foreign buyers |

| Exit options | Larger resale audience in established areas | Can depend heavily on local sentiment and liquidity |

A mature market suits investors who value predictability, financing access, and deeper resale pools. An emerging market can suit investors willing to accept political, currency, operational, and liquidity risk in exchange for stronger upside potential.

The key is consistency. Use the same checklist in every country. Don't become more relaxed just because the brochure looks more exciting.

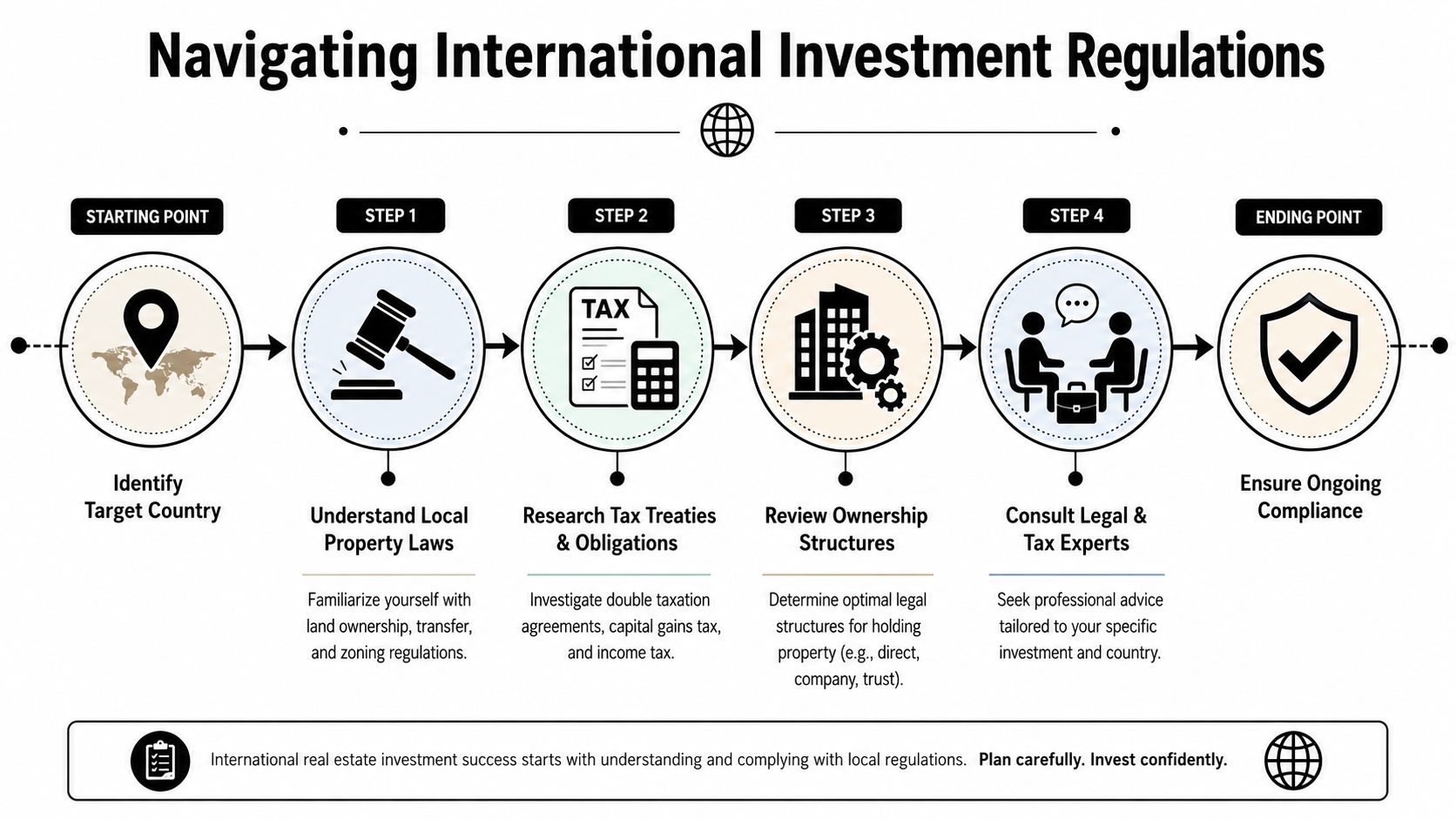

Navigating International Tax and Legal Regulations

Cross-border property investing is never just about the asset. It is also about who can own it, how income is taxed, what reporting is required, and what future rules might do to your hold period and exit value.

The legal questions to ask in any market

You don't need to memorise every country's statute book. You do need a repeatable legal checklist.

Start with these:

- Ownership rules: Can foreign buyers own directly, lease long-term, or only invest through approved structures?

- Income taxation: How is rental income taxed locally, and how does that interact with your home-country obligations?

- Capital gains treatment: What happens when you sell, and are there withholding or reporting requirements?

- Inheritance and succession: Can your heirs inherit the asset cleanly, and under which legal system?

- Landlord compliance: What licensing, safety, tenancy, or registration obligations apply after purchase?

For complex transactions, a local specialist matters. A strong international real estate lawyer can often save more money than they cost by identifying structural problems before exchange.

The UK as a case study in regulatory risk

The UK is a useful example because it's established, transparent, and still full of moving parts. Investors sometimes assume mature markets are simpler to hold. They're often more rule-dense instead.

Current UK developments make that clear. The government has confirmed the Renters' Rights Bill is moving through Parliament in 2025, and in London the EPC C minimum standard is set for new tenancies by 2028 and all tenancies by 2030. That means landlords need to budget for compliance work, especially on older and less efficient stock (UK regulatory and EPC compliance context).

Why this changes investment decisions

These rules affect more than administration. They affect:

- Cash flow: Retrofit work, professional advice, and compliance upgrades cost money.

- Tenant operations: Stronger tenant protections can change arrears handling, possession strategy, and management timelines.

- Exit pricing: A buyer may discount properties that need energy upgrades or carry legal complexity.

- Asset selection: Older flats, leasehold-heavy stock, and inefficient buildings may become harder to hold and harder to sell.

The wrong legal structure or a missed compliance issue can turn a decent yield into a poor investment.

That is why due diligence shouldn't stop at title and survey. You also need to underwrite regulation itself. In many international markets, the property that looks cheapest today is sometimes the one carrying tomorrow's most expensive obligations.

Building Your Portfolio Your Next Steps

A strong property portfolio isn't built by collecting addresses. It's built by repeating a sound decision process across markets and over time.

The most useful guide to property investment is the one that teaches you to think clearly when a deal looks tempting. Start with strategy. Decide whether you want income, growth, a value-add opportunity, or passive exposure. Then test the numbers thoroughly. Then assess the local market. Then review the legal and tax position. In that order.

A practical investor checklist

Before committing to any purchase, make sure you can answer these questions clearly:

- Strategy fit: Does this asset match your objective, or are you forcing the deal to do a job it can't do?

- Return quality: Are you relying on net income and realistic ROI, or on gross figures and hope?

- Finance resilience: Can the property survive less favourable borrowing terms, voids, or repair costs?

- Market depth: Who will rent it, who will buy it from you later, and why?

- Regulatory durability: Will future compliance costs make the asset less attractive to hold or sell?

What works over the long term

Investors usually do well when they stay boring in the right places. They buy in locations with understandable demand, finance conservatively, keep cash reserves, and avoid underwriting that depends on perfection.

What usually doesn't work is chasing a fashionable city, a tax gimmick, or an apparent yield premium without understanding the operating reality beneath it.

If you keep one principle in mind, make it this: buy the business model, not just the building.

If you're ready to compare countries, cities, yields, taxes, and buying rules in one place, World Property Investor is a practical next step. Use it to shortlist markets, pressure-test your assumptions, and move from broad interest to informed action.