You've identified a UK property, the exchange rate still looks workable, and at least one lender has said your case is “possible”. That's the easy part. The harder part is turning a possible case into a bankable file that survives underwriting, valuation, compliance, and legal checks without falling apart two weeks before exchange.

That gap catches out many overseas buyers. An overseas mortgage for UK property isn't blocked by lack of demand. It's blocked by execution. Lenders want clarity on income, tax position, residence, credit profile, deposit trail, and how the property fits their risk model. If one of those pieces is weak, the case doesn't usually fail dramatically. It just slows down, then stalls.

The UK market is still familiar ground for international investors, especially in London and other liquid cities. But familiarity shouldn't be confused with ease. If you're buying from abroad, treat financing as an operational project, not just a product search.

An Investor's Introduction to UK Property Finance

The starting point is simple. Overseas ownership in the UK is already established. Approximately 202,568 properties across England and Wales are registered to individuals with an overseas correspondence address, representing 0.7% of all registered titles, and London holds the highest concentration, with the largest groups of foreign homeowners coming from Hong Kong, Singapore, the USA, the UAE, and China according to latest Land Registry reporting discussed here.

That tells you two things. First, the route is proven. Second, it is concentrated. International buyers tend to focus on markets with depth, rental demand, legal transparency, and resale liquidity. In practice, that usually means London, major regional cities, and established commuter locations rather than thinly traded fringe stock.

A mortgage is only one part of the investment equation. If you'll be remote after completion, it's worth thinking early about managing UK investment properties from overseas, because poor operational management can erode returns faster than a slightly higher mortgage rate.

The three lender routes that matter

Most overseas buyers fit into one of three routes:

| Lender route | Typical profile | What works | What usually doesn't |

|---|---|---|---|

| High street or near-mainstream lenders | Borrowers with strong UK ties, simple income, clean documentation | Lower complexity, familiar process | Foreign income, unusual residence, layered company structures |

| Specialist lenders | Expats, foreign nationals, buy-to-let investors, mixed income cases | Flexibility on residency and income profile | Weak paperwork, unclear source of funds, unusual property types |

| Private banks | High-net-worth borrowers with substantial assets and larger loans | Bespoke underwriting, relationship-led approach | Small loan sizes, thin asset backing, purely transactional approach |

If you're still deciding whether the UK is the right destination, a broader guide to buying UK property from overseas helps frame the wider acquisition picture beyond the mortgage.

The strongest overseas cases are rarely the cheapest on day one. They're the ones that remain executable through to completion.

Established markets usually give lenders more confidence because valuers, solicitors, and asset managers understand them well. Emerging local pockets can offer stronger headline yield, but the financing side is often less forgiving if tenant demand, building condition, or resale evidence is hard to prove.

The Lender Landscape and Your Eligibility

A borrower based in Dubai, Singapore, or Geneva can have strong income, substantial assets, and a clean credit profile and still fail to get a UK mortgage agreed on workable terms. The gap is usually operational. Lenders may like the headline case, then reduce appetite once they test foreign income, trace deposit funds through several accounts, or review a company structure spanning more than one jurisdiction.

Why high street banks often fall away early

Mainstream lenders are built for speed and standardisation. They tend to work best where the borrower has UK income, simple employment, familiar tax documents, and an address history that fits automated checks.

Overseas cases break that pattern quickly.

A foreign national paid in dollars, holding assets through a family company, and buying via a UK SPV may be perfectly bankable. But many retail lenders will either decline at policy stage or issue terms that become harder to honour once underwriting asks for translated documents, accountant references, overseas credit evidence, and a clearer audit trail on wealth.

Where overseas borrowers get financed in practice

The workable route is usually either a specialist lender or a private bank.

Specialist lenders tend to suit expats, non-residents, and buy-to-let investors whose cases do not fit a retail credit model. They are more willing to assess foreign salary, dividend income, contractor income, or mixed income streams, but they will stress-test them harder. Currency matters. Tax treatment matters. The consistency of the paperwork matters even more.

Private banks are relevant where the loan is larger, the assets are wider than earned income, or the borrower needs judgement rather than a rigid scorecard. They can be more flexible on structure, but the bar on liquidity, investable assets, and source-of-wealth evidence is higher. They also tend to want a broader relationship, not a one-off mortgage request.

A practical comparison

| Lender Type | Typical approach to non-residents | Minimum loan profile | Best fit |

|---|---|---|---|

| High street banks | Conservative policy, limited tolerance for foreign income complexity | Lower to mid-market loans | UK-linked borrowers with simple salaried income |

| Specialist lenders | Manual underwriting with more flexibility on residency and income type | Varies by lender and property | Buy-to-let, expat, foreign income, complex residency |

| Private banks | Bespoke credit view based on income, assets, and relationship depth | Usually higher entry point | HNW borrowers, larger loans, multi-jurisdiction wealth |

If you are weighing UK borrowing against wider international options, this guide to a mortgage for buying property abroad helps frame the broader financing choices.

What underwriters examine before a case gets traction

Nationality is only a small part of eligibility. Credit teams usually focus on how easy the case is to verify and how resilient it looks under stress.

- Country of residence. Some jurisdictions are straightforward for KYC and sanctions checks. Others trigger slower onboarding or reduced lender appetite.

- Income source and stability. Basic salary is easiest. Bonuses, dividends, partnership drawings, carried interest, and income split across countries need closer analysis.

- Currency and conversion risk. Sterling income is simplest. Major currencies can be acceptable, but lenders often apply haircuts or tougher affordability assumptions where exchange rate risk is material.

- Property purpose. A London pied-à-terre, a family home, and a buy-to-let investment sit in different credit boxes.

- Deposit and wealth trail. The issue is rarely just the amount. It is whether the funds can be traced cleanly from origin to completion account.

Strong applicants can find themselves caught out. They often assume wealth is enough. Underwriters need evidence that is clear, consistent, and easy to reconcile.

Foreign income is judged more harshly than many buyers expect

A lender does not merely convert your income into sterling and apply a standard affordability multiple. They look at how the income is earned, whether it is recurring, how it appears on local tax returns, and whether any part of it is discretionary or volatile. Bonus-heavy pay, commission, and dividend-led remuneration often get discounted. Retained profits may be ignored unless the lender is comfortable with your shareholding and access to those funds.

For self-employed borrowers, I usually see delays for one of three reasons. The accounts are prepared under unfamiliar local standards. The tax return does not line up neatly with the bank statements. The income sits across several entities and no one has summarised the structure properly for the underwriter.

Source-of-wealth checks start earlier for overseas clients

UK lenders and solicitors will ask where the deposit came from. For non-residents, the questions often go further. They may want to know how the wider wealth was built, especially where funds come from a business sale, inheritance, trust distribution, or years of savings moving through multiple jurisdictions.

That process is manageable, but only if it starts early.

A clean case usually follows a disciplined sequence:

- Screen the borrower first. Residence, nationality, visa status if relevant, income type, liabilities, and intended ownership structure.

- Screen the property next. Standard construction in a liquid market is easier to finance than short lease property, ex-local authority flats, or buildings with cladding issues.

- Test the evidence before application. Foreign income documents, tax returns, company accounts, and bank statements should reconcile before they reach underwriting.

- Prepare the AML story upfront. Source of funds and source of wealth should be explained in plain English, with documents that support each step.

The common mistake is chasing a quick decision in principle and treating documentation as an admin task for later. In overseas borrowing, that approach wastes time. A specialist broker earns their fee by knowing which lender can accept the case and by presenting it in a form credit teams can approve.

Assembling a Winning Mortgage Application

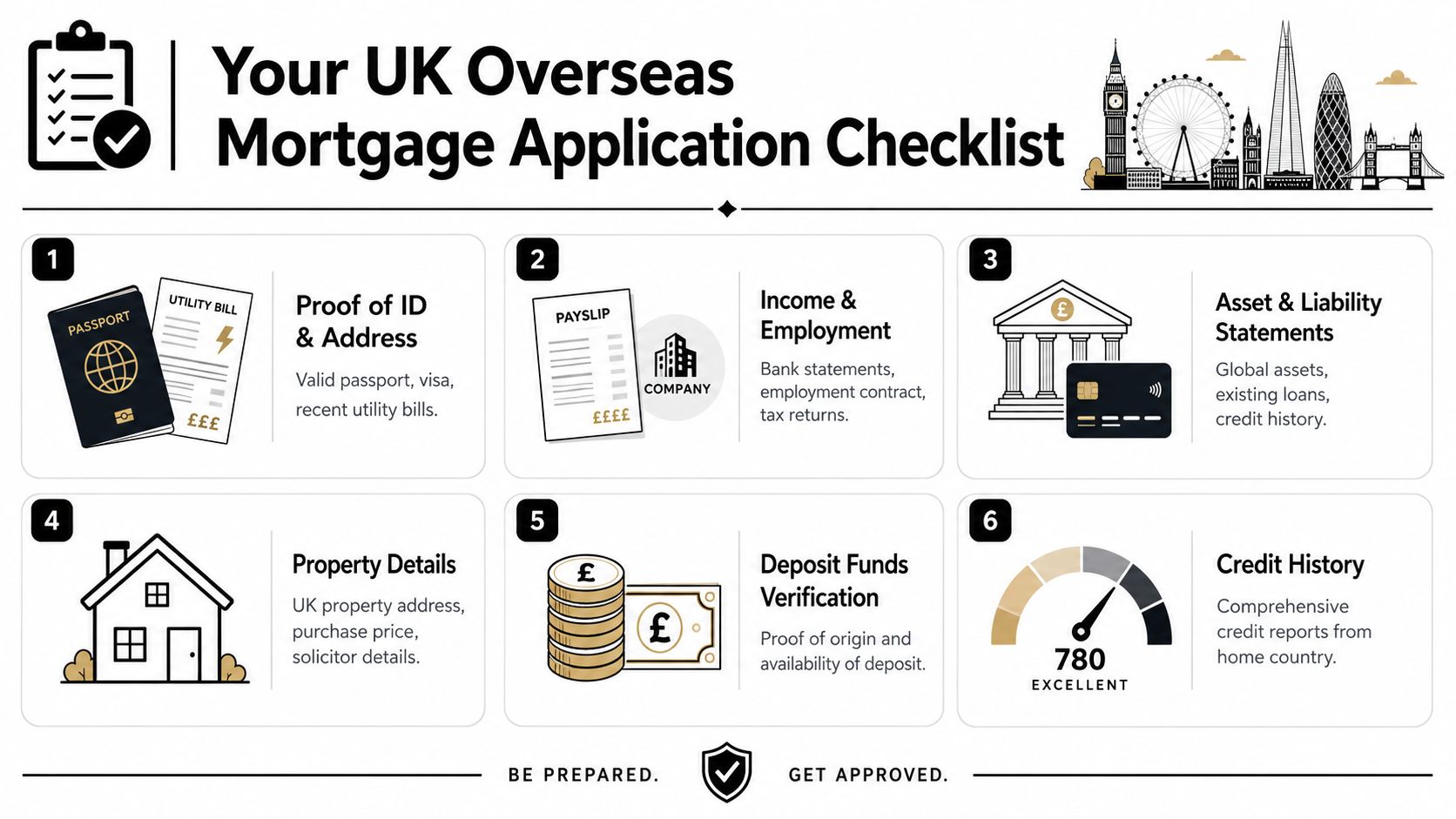

A strong overseas mortgage application is built, not submitted. The lender must be able to trace who you are, where you live, how you earn, what you own, what you owe, and where the deposit came from without making assumptions.

The file that gets traction

Success depends on presenting a complete financial profile, including 3 to 6 months of bank statements and evidence of stable income, because lenders run strict affordability checks and may decline cases where tax implications or currency risks are not adequately addressed, according to this guide for UK buyers arranging overseas-style mortgage applications.

That principle applies directly to an overseas mortgage for UK property as well. The lender wants consistency more than drama. Clean, stable, explainable documents beat impressive but messy wealth every time.

What a lender expects to see

- Identity and residence. Certified passport, proof of current address, and residency evidence where required.

- Income evidence. Payslips, employment letter, tax returns, company accounts, dividend vouchers, or pension statements depending on profile.

- Banking evidence. Personal and sometimes business statements, especially where income lands in one jurisdiction and spending happens in another.

- Assets and liabilities. Global property schedule, mortgages, loans, securities portfolios, and contingent liabilities.

- Deposit evidence. The paper trail must show where the funds originated and how they moved.

Practical rule: if a compliance officer can't follow the money in one read-through, the case will slow down.

How foreign income is actually stress-tested

Many otherwise good applications often weaken, as lenders do not merely convert your foreign income into sterling at the live rate and proceed. They usually take a more cautious view. They'll look at the currency, the stability of the jurisdiction, the type of income, and whether that income is recurring.

A salaried employee paid in US dollars by a global company is easier to assess than someone drawing variable consulting income from several companies in multiple countries. A landlord with several rental streams may still be acceptable, but only if the evidence is organised and the tax position is clear.

Here's the practical logic lenders tend to follow:

| Area reviewed | What the lender looks for | Common issue |

|---|---|---|

| Currency | Stability and convertibility into sterling | FX exposure reduces comfort |

| Income type | Sustainability and traceability | Bonuses or dividends treated cautiously |

| Tax position | Whether net income is reliable after tax | Missing returns or unclear liabilities |

| Existing debts | Full global monthly obligations | Offshore liabilities omitted from initial fact find |

For borrowers trying to sense-check their debt capacity before applying, a debt burden framework like this debt-to-income guide is a useful starting point.

A worked example without false precision

Take a buyer earning in US dollars who wants a buy-to-let property in Manchester. A specialist lender won't just ask what the salary converts to in sterling today. It will ask whether the income is fixed, whether there's a track record, whether the borrower also has dollar liabilities, and whether the rental income on the UK property supports the case on a standalone or semi-standalone basis.

If the borrower is employed, paid monthly, and has clean statements, the case can be straightforward. If the borrower also receives annual bonus income and holds other mortgaged property abroad, the lender may use only part of that wider income picture or ask for stronger liquidity.

The lesson is simple. Don't assume all your global income will count equally. Package it in order of credibility, not optimism.

Calculating Deposits Affordability and FX Rules

A common failure point is simple. The client can afford the property in real life, but the lender will not sign off the case on paper.

For overseas applicants, the gap usually appears in three places. Deposit size, affordability treatment, and foreign exchange exposure. Those three points decide whether a deal proceeds, stalls at underwriting, or needs to be restructured.

A non-resident borrower should expect to contribute more equity than a UK-based applicant. In practice, many lenders want a larger buffer on overseas cases because foreign income is harder to stress-test, documents take longer to verify, and any resale risk sits with a narrower buyer pool. UK Finance's borrower guidance sets out the broader principle that deposit level directly affects the mortgage terms and lender appetite, which is why overseas cases tend to be assessed more conservatively on loan-to-value. See UK Finance's guide to mortgage deposits and loan to value.

To make the moving parts easier to visualise:

What the deposit really does

A larger deposit is not just a pricing tool. It changes the underwriter's view of the whole file.

It gives the lender room if the valuation comes in below the agreed price. It helps if the lender applies a harsher currency haircut than the client expected. It also reduces the chance that a technically good case fails because one part of the profile, often bonus income or overseas debt, is treated more cautiously than the client assumed.

I often advise clients to work backwards from a realistic maximum loan rather than forwards from the purchase price they want. That avoids wasting weeks on a property that only works if every part of the underwriting case is accepted in full.

Affordability is tested, not assumed

Lenders do not underwrite overseas borrowers on the spot FX rate and a headline salary figure. They want to know what survives stress.

For an employed applicant, the usable income may be lower than the gross figure shown on the payslip once tax, pension deductions, housing costs, school fees, and overseas liabilities are factored in. For self-employed borrowers, the lender may average income over more than one year, discount volatile revenue, and place more weight on retained profits only if the structure and tax position are clear.

Foreign currency adds another layer. Some lenders use only a selected list of currencies. Some reduce accepted income to allow for exchange-rate movement. Others want to see cash reserves in sterling or in a major currency that can be converted quickly. That is the practical chasm between “a lender exists” and “the mortgage is approved”.

A sensible pre-application model should test:

- the deposit after purchase costs, not before

- monthly affordability if sterling strengthens against your income currency

- a higher stressed pay rate, not just the initial product rate

- rental shortfalls, voids, service charges, and maintenance

- whether liquidity remains after completion

A Manchester case, as an underwriter sees it

Take an investor earning in US dollars buying a Manchester flat to let. On the client side, the numbers may look straightforward. Deposit available, strong salary, and projected rent that appears to cover the mortgage.

The lender looks at different risks. Will the rent still cover the loan at the stressed interest rate? If the rent falls short, does the borrower's dollar income still support the loan once converted on the lender's terms, not the client's? If sterling rises, does the repayment become uncomfortable in home-currency terms? If the client's deposit was built from bonuses, business distributions, or asset sales, is there a clear source-of-wealth trail?

That last point matters more than many applicants expect. A borrower can have ample funds and still lose time if the money trail is fragmented across jurisdictions, family accounts, or recent transfers. By the time the underwriter and solicitor both start asking questions, the transaction timetable is already under pressure.

If you hold capital in one currency and the property is priced in another, review strategies for hedging currency risk before exchange rather than after funds are needed.

Clients buying short-let or hybrid-use property should also check the tax treatment early, especially if the investment case depends on furnished holiday let assumptions. This overview of property tax advice from Action Accountants is a useful starting point.

Later in the process, many buyers also find this short explainer useful:

Rate environment still matters

Even high-net-worth borrowers should model debt costs carefully. Product choice affects liquidity, covenant comfort, and exit flexibility.

The FCA's mortgage lending statistics show that average UK fixed rates increased materially over the period reported, while the stock of residential mortgage lending remained large. In practice, that means overseas borrowers need more margin for error. A deal that still works after rate stress, FX movement, and a stricter view on income is the deal worth pursuing.

The UK Conveyancing and Tax Implications

The mortgage offer is not the finish line. It is the point at which legal and tax execution starts to matter more.

Overseas buyers often underestimate how much scrutiny their solicitor will apply to funds coming from abroad. A good conveyancer won't just receive money and send contracts. They'll ask where the funds originated, how they moved, whether any gifting is involved, and whether the structure matches what the lender was told.

The legal side that causes delays

From a practitioner's point of view, many avoidable problems start with poor coordination. The broker knows the lender's conditions. The solicitor knows the title and the money trail. The tax adviser understands ownership structure and reporting. If those parties work in silos, delays appear late and expensively.

One recurring issue is buyers choosing a solicitor who is perfectly competent domestically but inexperienced with non-resident files. International source-of-funds reviews take longer. Certification standards matter. Timelines for moving money matter. If the solicitor isn't used to that, the purchase can drift.

Use a solicitor who regularly handles non-resident funds, certified overseas documents, and lender conditions on international clients. That is not a luxury add-on. It is part of risk control.

Tax needs to be considered before exchange

This is not tax advice, but overseas buyers need a working understanding of the tax framework before they commit. Stamp Duty Land Tax, income tax on rental profits, the Non-Resident Landlord Scheme, and Capital Gains Tax on disposal can all affect net return. Your structure also matters. Buying personally, jointly, or through a company can lead to very different outcomes.

For buyers who also plan to let on a short-stay basis or are comparing holiday-let structures, specialist property tax advice from Action Accountants is a useful reference point before deciding ownership and operating model.

If you need a primer on transaction tax itself, this guide to stamp duty on property helps frame the questions to put to your solicitor and accountant.

What I'd want clarified before committing

- Who is the legal buyer. Individual, joint names, or company.

- How rental income will be reported. Especially if you remain non-resident.

- How sale proceeds may be taxed later. Exit planning matters at entry.

- Whether the lender's conditions conflict with the ownership structure. This happens more often than buyers think.

The investors who move smoothly are rarely the ones with the most aggressive targets. They're the ones who resolve ownership, lending, and tax treatment before they negotiate the last detail of price.

Avoiding Common Pitfalls and Using a Broker

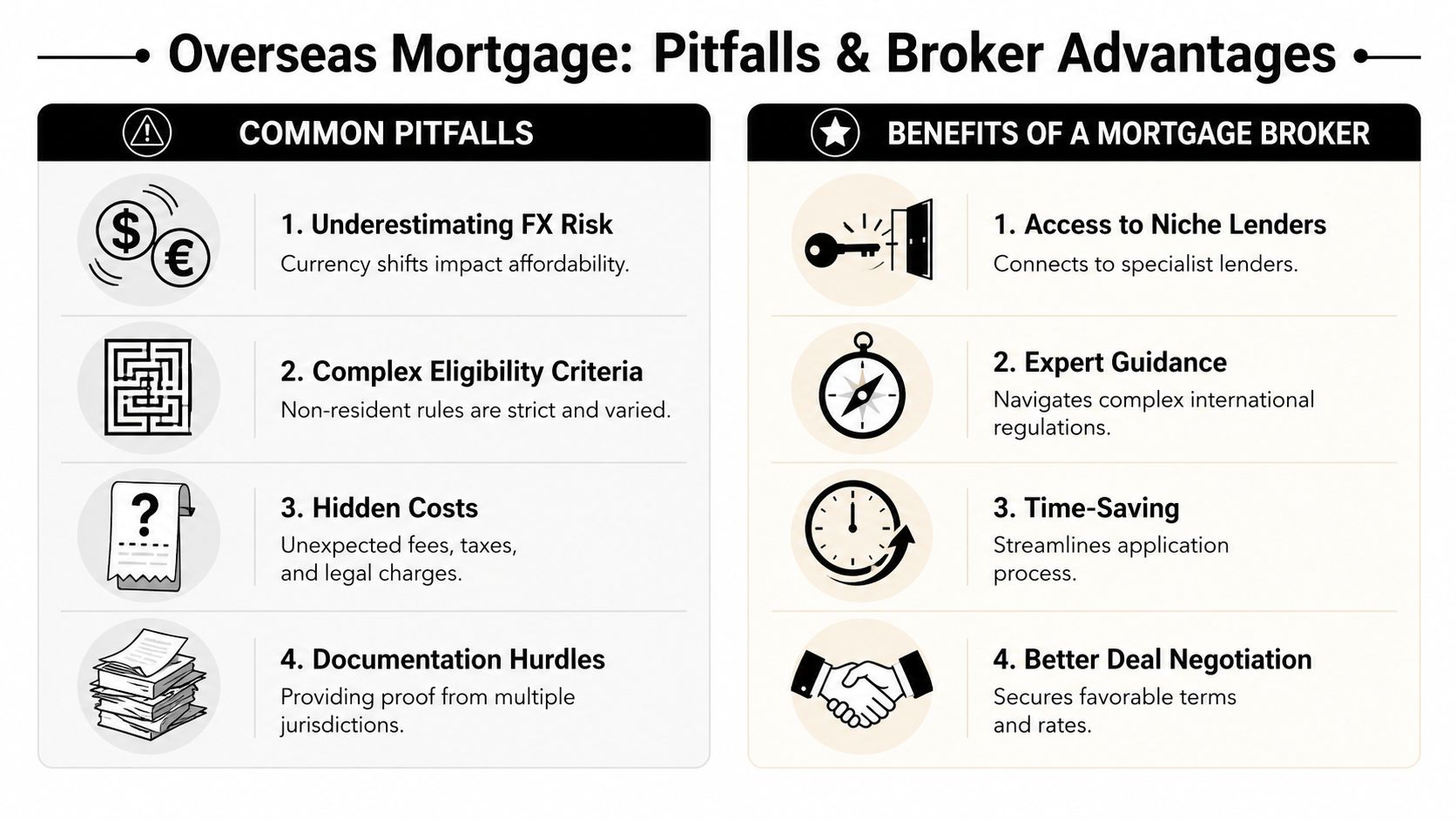

Most failed overseas mortgage cases don't fail because the borrower lacks wealth. They fail because the process was handled like a domestic application with extra documents bolted on.

The mistakes that keep repeating

A major one is assuming the lender's verbal interest equals a reliable route to offer. It doesn't. Until the case has passed document review, credit assessment, valuation, and compliance, it is only a live possibility.

Another is underestimating friction in cross-border paperwork. When using a foreign lender, applicants often need financial and legal documents translated into the local language, and they must account for local property taxes, translator fees, and arrangement fees that are not typical in UK domestic mortgage transactions, as explained in this guide to mortgages for overseas property. Even where the property is in the UK, the same lesson applies. Cross-border documents create drag.

The contract trap buyers forget

For UK residents buying abroad, one of the clearest warnings from specialist international brokers is the risk of paying a deposit without mortgage protection in the contract. Enness notes the importance of wording a purchase contract so it is subject to an acceptable mortgage offer, because otherwise a deposit can be at risk if finance fails. The exact legal mechanism differs by jurisdiction, but the principle is universal. Don't commit funds before finance and legal protection align.

A second structural issue is regulation. Many high-street lenders don't offer overseas property mortgages, and these loans are not regulated by the FCA in the same way as domestic lending, which is one reason specialist advice matters, as discussed in this overview of mortgages for overseas property.

Why a specialist broker earns their place

For an overseas mortgage for UK property, a specialist broker does far more than compare rates.

They should:

- Filter lenders early. That avoids unnecessary footprints and wasted applications.

- Package foreign income properly. This is often the difference between “declined” and “approved subject to valuation”.

- Pre-empt compliance questions. Especially around source of wealth and large deposits.

- Coordinate moving parts. Broker, bank, valuer, solicitor, and sometimes FX provider.

A good broker reduces uncertainty, not just price.

That matters even more for high-net-worth borrowers. Private banks and niche lenders can be flexible, but only when the case is framed coherently. A weak presentation can make a strong client look difficult.

Questions to ask before appointing a broker

Don't choose a broker merely because they say they handle international clients. Ask for specifics.

- Which lenders do you regularly place non-resident cases with? You want current market access, not old brand recognition.

- How do you assess foreign income and multi-jurisdiction liabilities before application? If they can't explain this clearly, expect trouble later.

- Who handles source-of-funds packaging? This should be proactive, not reactive.

- What property types do your lenders dislike? The answer will tell you how honest they are.

- How do you work with solicitors and valuers during the process? Execution matters.

You should also think about the wider protection layer around the debt. If you're reviewing how to compare mortgage life insurance alongside the purchase, do it as part of the financing decision, not after completion when cover is often treated as an afterthought.

What works in practice

The best overseas cases usually share the same features:

- The borrower selects the lender category before selecting the lender.

- The property is financeable, not just attractive.

- Income, tax, and deposit evidence are organised before the application starts.

- The solicitor is chosen for non-resident competence, not lowest fee.

- Currency planning happens before exchange.

That's the practical chasm. Lenders exist. Real approvals exist. But securing a mortgage is a different discipline from finding one.

If you're comparing locations, rental strategies, tax exposure, and financing routes across borders, World Property Investor is a useful place to research markets in depth before you commit capital. It helps investors weigh fundamentals, compare destinations, and make better property decisions with clearer context.