You're probably in one of two positions right now. You've found the market you want, the numbers on the property look workable, and then the finance side starts to get murky. Or you already know the property will be abroad, but you haven't yet decided whether the smarter route is to borrow at home, borrow locally, or use a specialist who can stitch the deal together.

That's where most first-time international buyers lose time. Not because the opportunity is bad, but because cross-border lending isn't a standard residential mortgage with a different postcode. A buy property abroad mortgage is a separate underwriting exercise. Lenders look at country risk, currency risk, foreign income, legal process, and sometimes the condition of the property more closely than buyers expect.

The practical mistake is assuming the property itself is the main hurdle. In reality, the mortgage structure often determines whether the deal is investable at all.

Understanding Your Overseas Mortgage Options

The first reality check is cash. For UK buyers, overseas mortgages usually need a bigger deposit than a domestic loan. HSBC notes that lenders usually require at least 20% down, and for a Spanish property bought by a non-resident the deposit can rise to 30% to 40%. On a EUR200,000 apartment, that can mean up to EUR80,000 upfront before fees and currency costs, according to HSBC's guide to financing an overseas property.

That single point changes how you should think about the whole purchase. A buy property abroad mortgage is rarely just about monthly affordability. It's about whether you have enough liquidity to satisfy the lender, cover local buying costs, and still leave yourself with reserves.

Three routes that usually matter

Most investors end up choosing between three broad financing routes:

- Borrow from a bank in your home country. This can feel simpler because your income, banking history, and identity documents are already familiar to the lender.

- Borrow from a lender in the country where you're buying. This can suit buyers who want a mortgage aligned with the local market and legal system.

- Use a specialist international broker. This route helps when the case is unusual, the income is complex, or the target market isn't well served by mainstream lenders.

HSBC also frames an overseas mortgage in broad terms. It may come from a local bank, an overseas lender, or from releasing equity in an existing home. That's useful because many investors think too narrowly about “getting a mortgage abroad”, when the better question is which debt source gives the cleanest execution.

Practical rule: Pick the finance route first, then negotiate the property. Buyers who do it the other way round often end up trying to force a lender into a deal that doesn't fit policy.

What each route is really trading off

A domestic lender can reduce friction, but product choice may be narrow. A local lender may understand the asset class and legal process better, but may ask for translated documents, local tax numbers, or proof that doesn't map neatly from the UK. A specialist can widen your options, but that guidance has a cost and only adds value if the broker knows the country and lender panel well.

One concept that becomes more important abroad is loan-to-value, because even small changes in lender appetite materially affect your cash commitment. If you want a quick refresher before comparing lenders, this guide to understanding LTV ratio is useful context.

The best route depends on what matters most in your case. If speed and familiarity matter, start domestic. If pricing and local fit matter, go local. If your income is layered across salary, company drawings, overseas assets, or multiple jurisdictions, specialist advice usually earns its keep.

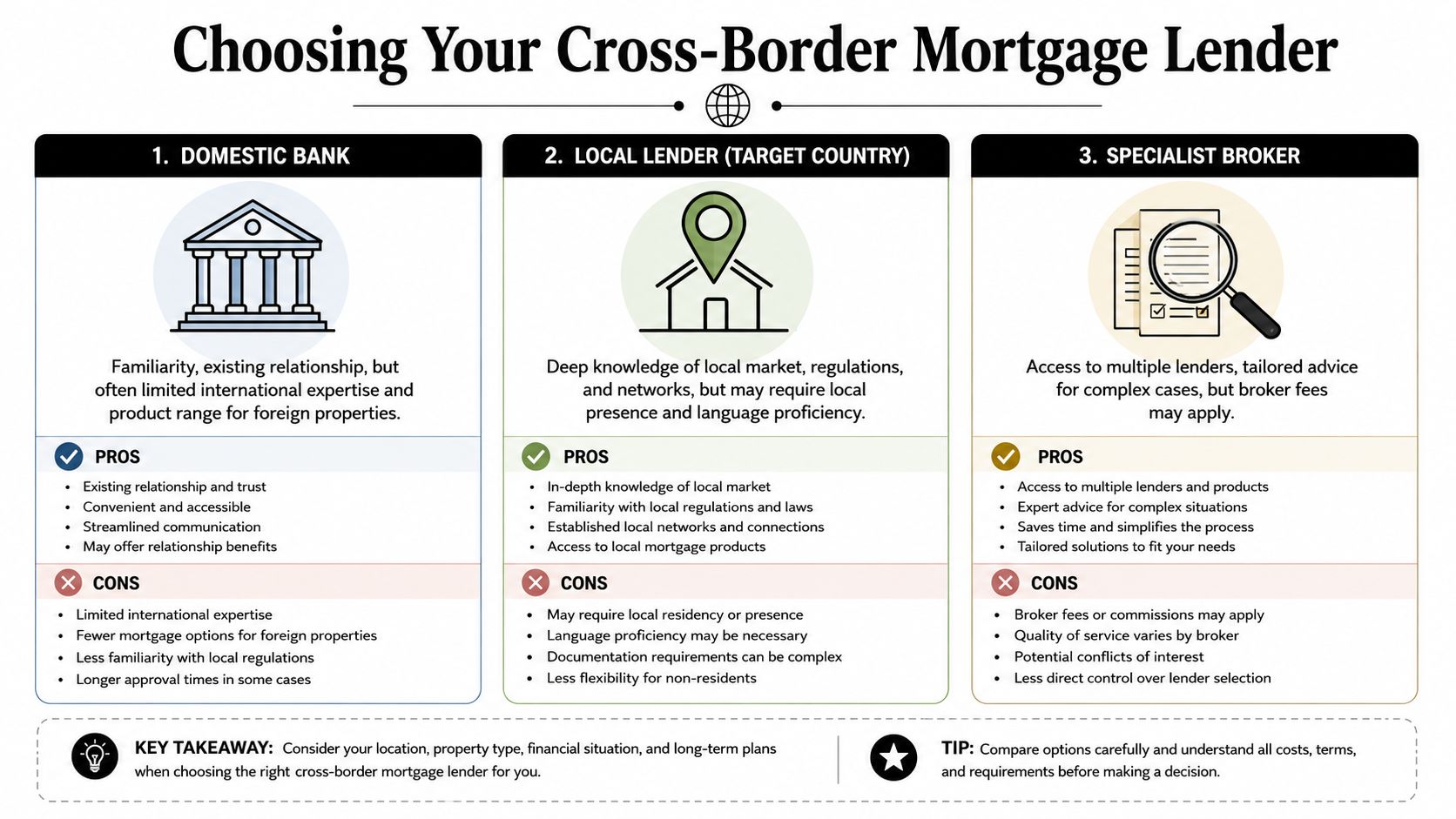

Choosing Your Lender Domestic Bank Local Lender or Specialist

The most effective way to choose a lender is to stop asking which route is “best” in general. Ask which route fits your profile, target country, and tolerance for paperwork.

Domestic bank

A domestic bank is usually the easiest conversation to start. The lender already understands UK-format income evidence, bank statements, and ID checks. If you've got an established banking relationship, that can help the process feel more predictable.

The downside is product scope. Many domestic banks don't cover a wide range of countries, property types, or borrower structures. If they do lend internationally, policy can be conservative.

What tends to work

- Straightforward salaried applicants: UK employment, clear tax records, and a standard residential or holiday-home purchase.

- Established banking clients: Existing customers can sometimes move more quickly through the initial review.

- Buyers who prioritise convenience: One language, one familiar compliance framework, fewer surprises.

What often doesn't

- Niche locations: If the country isn't on the lender's preferred list, the case stops early.

- Complex income: Self-employed structures, foreign dividends, and layered business income often create friction.

- Unusual assets: Renovation projects, mixed-use properties, or heavy rental dependence can fall outside policy.

Local lender in the target country

A local lender usually has better visibility on the market you're entering. That matters more than many investors realise. The bank understands local valuations, title practices, common property defects, and borrower demand in that market.

But local knowledge comes with operational friction. Documentation standards may be different. The legal process may be slower. Translation requirements can turn a simple underwriting query into a long delay.

Borrowing locally often works best when the buyer treats the mortgage as part of the country-entry process, not just as a source of leverage.

A local lender can be particularly useful if you're buying in an established European market where non-resident lending is familiar. In an emerging market, though, the spread between “possible in theory” and “practical in reality” can be wide.

Specialist broker

A strong international broker doesn't lend the money. The value lies in lender matching, packaging the case properly, and steering around avoidable problems. That's most useful when your file won't fit a standard box.

Typical examples include self-employed borrowers, expats paid in more than one currency, buyers using existing property equity, and investors comparing several jurisdictions at once.

Here's a simple comparison:

| Route | Best for | Main strength | Main weakness |

|---|---|---|---|

| Domestic bank | Simpler profiles | Familiar process | Limited market coverage |

| Local lender | Country-specific purchases | Local underwriting insight | More admin and local compliance |

| Specialist broker | Complex or cross-border cases | Access and structuring | Broker fees may apply |

If you're comparing financing structures before you commit to one market, this overview of investment property loan options is a useful companion.

The route I'd usually avoid is choosing a lender based only on headline pricing. In cross-border property finance, a slightly cheaper offer that fails at document stage is more expensive than a lender that understands your profile from day one.

Meeting Lender Eligibility and Document Requirements

Most overseas mortgage applications fail indirectly. Not with a formal decline at the start, but with repeated document queries, unresolved underwriting concerns, and deadlines that drift until the seller loses patience.

The fix is simple in theory. Build the file before you apply.

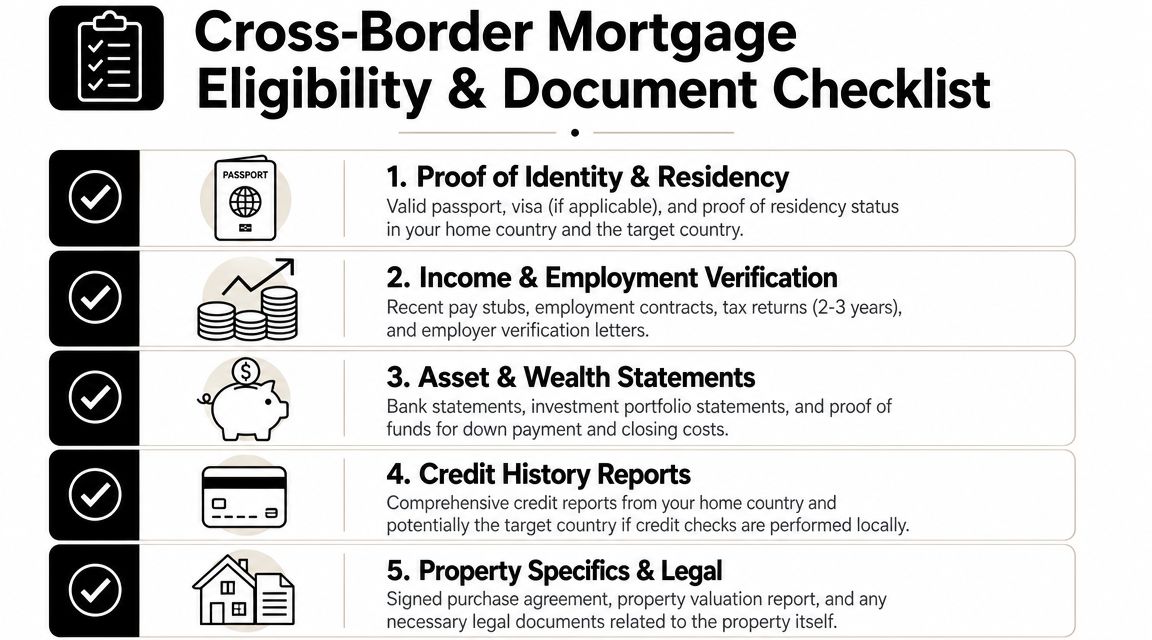

What lenders usually want first

A lender wants to answer three questions. Who are you. Can you repay. Is the property good security.

That means your first document pack should usually include:

- Identity and address evidence: Passport, proof of current address, and any residency or visa paperwork if relevant.

- Income proof: Payslips, tax documents, company accounts if self-employed, and bank statements showing income receipt.

- Asset evidence: Funds for deposit, reserves, and sometimes evidence of broader net worth.

- Credit background: The lender may review your home-country profile and, in some cases, local history if you have one.

- Property file: Reservation form or purchase agreement, listing details, and later a valuation and legal papers.

The investor error is sending the minimum requested and waiting for the next question. Good applications arrive already organised, translated where needed, and internally consistent.

The hidden underwriting tests

The headline criteria are rarely the ones that cause trouble. The hidden tests are the actual problem.

One is income interpretation. Foreign income often needs more explanation than borrowers expect. A lender may understand salary quickly, but company profits, retained earnings, partnership income, and irregular bonuses usually require careful presentation. Self-employed applicants need especially clean accounts and a defensible story that ties tax returns to actual cash flow.

Another is source of funds. Lenders and lawyers want a clear trail showing where the deposit came from. Savings are easiest. Gifts, business distributions, and recently moved funds need tighter explanation.

Then there's the issue many buyers misunderstand: rental income. Guidance aimed at UK investors buying abroad often glosses over this point, but many lenders either don't count future rent in affordability or only count it in limited cases. Simon Conn's guidance notes that lenders typically underwrite on earned income, pension income, and sometimes investment income rather than projected rent. That makes second home mortgage requirements worth reviewing before you build your case.

Don't assume the property “pays for itself” in the lender's eyes. In many cross-border cases, they want to see that you can service the debt without relying on projected rent.

How to present a stronger file

A strong file usually has these characteristics:

- Clean chronology: Documents line up by date, address, and employer details.

- Readable translations: If documents need translation, use formal versions the lender can rely on.

- Explained anomalies: Large bank credits, recent job changes, and variable income should be clarified up front.

- Property realism: If the property needs work, expect more scrutiny around valuation and lendability.

The best applications feel boring. That's a good thing. Underwriters like files that answer questions before they need to ask them.

The Cross-Border Mortgage Application Process

The application process is manageable once you know the order of play. Problems usually come from trying to skip stages, or from assuming a lender will sort out country-specific issues later.

The broad workflow for UK buyers is clear. Wise's guidance says the practical sequence is to compare UK and foreign lenders, secure an agreement in principle, then assemble the full document pack before formal application. The same guidance also stresses budgeting for tax, legal, and translator fees because translation and local compliance checks can delay overseas applications, as explained in Wise's UK guide to overseas mortgages.

To keep the process straight, use this roadmap.

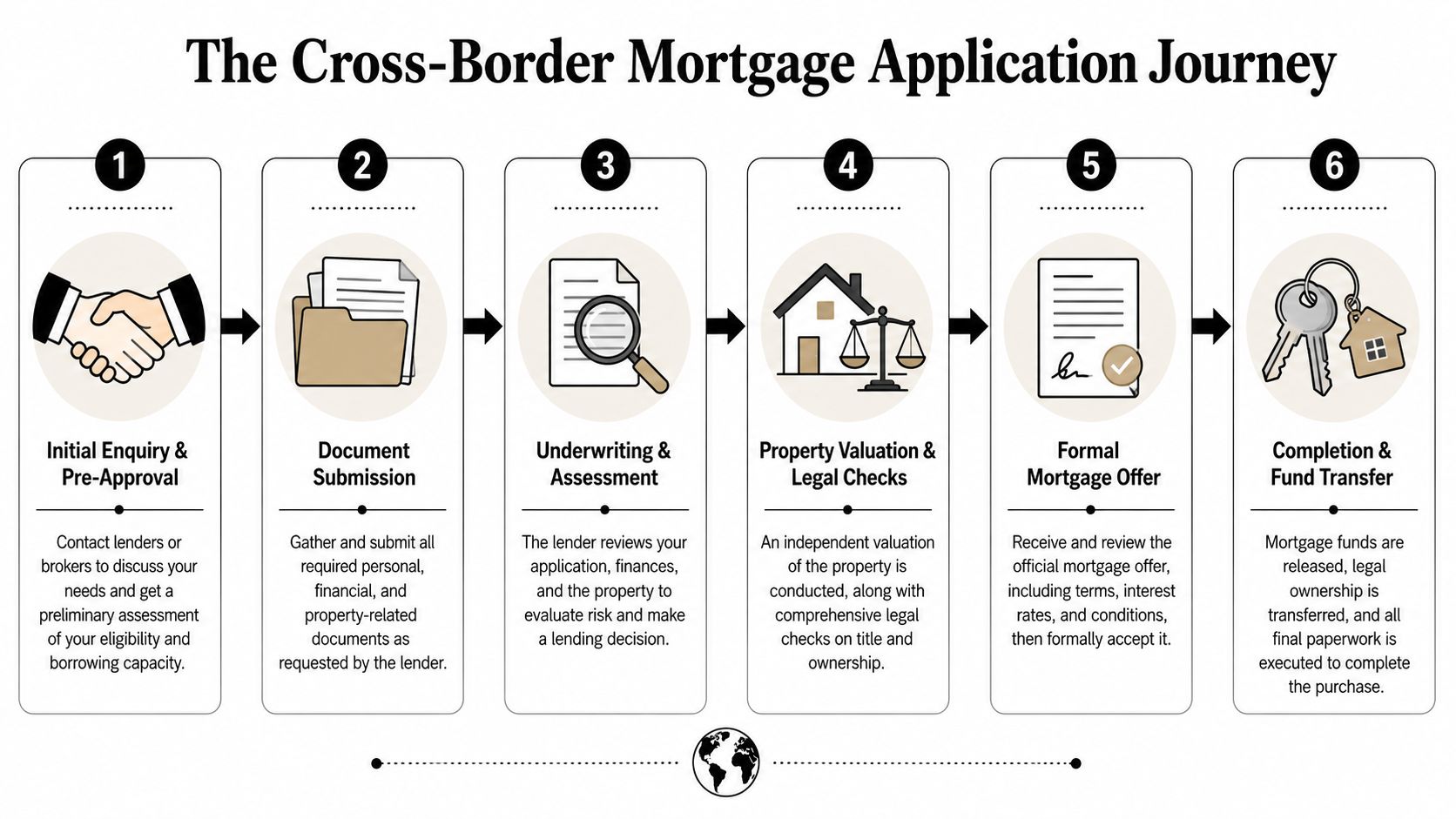

The sequence that actually works

Initial lender comparison

Test both home-market and target-country options early. Don't assume one route will be better without seeing how each lender interprets your profile.Agreement in principle

This step matters because it flushes out obvious eligibility problems before you spend heavily on legal work or commit too far with a seller.Full document submission

Here, many buyers slow themselves down. Incomplete packs create repeat queries, and repeat queries kill momentum.Valuation and legal review

The lender checks the asset, while the lawyer checks title, debt against the property, and local legal compliance.Formal offer

Read the conditions, not just the rate. Cross-border offers often contain practical conditions that affect timing and cash flow.Completion and fund transfer

Final release depends on the legal sign-off, your contribution arriving on time, and all lender conditions being satisfied.

A broader market overview can help if you're still deciding where to buy. This guide on investing in property abroad is a sensible starting point.

A short video can also help visualise the mechanics before you start speaking to banks or brokers.

Where delays usually happen

The slowest part of an overseas mortgage is rarely the decision itself. It's the gap between what the lender asks for and what the borrower can prove in the format the lender accepts.

Common sticking points include translations, proof of address mismatches, missing visa or residency evidence, and legal questions around title. The practical answer is to treat admin as part of the investment return calculation. Time lost in process has a cost.

Managing Costs Risks and Financial Alternatives

The deposit is only one line in the budget. Many buyers focus on loan approval and then get caught by the wider cash requirement around the deal.

Wise's broader overseas property guidance is useful here. It notes that international mortgage lenders commonly ask for 20% to 50% deposits, and recommends reserving 10% to 20% of the purchase price for taxes, legal fees, and closing costs in cross-border purchases, according to Wise's overview of overseas property mortgages.

The real acquisition budget

A buy property abroad mortgage should be underwritten against the full transaction, not just the property price.

That means budgeting for:

- Deposit and lender reserves: The cash you need to satisfy underwriting.

- Taxes and closing costs: These vary by market, but they can materially change the equity required.

- Legal and translation fees: These become more relevant when the lender, notary, or registry needs certified paperwork.

- Valuation and lender charges: Often overlooked in the initial spreadsheet.

- Post-completion works: Important if the property needs upgrading before it can produce income.

If you're comparing transaction costs across markets, a tool like this property stamp duty calculator helps frame one part of the picture, though you'll still need local tax advice.

Currency risk is not a side issue

Currency risk affects three separate points. Your purchase cost, your debt servicing, and your exit value.

If your income is in sterling, your property is priced in euros, and your mortgage is also in euros, you've got one sort of risk. If your mortgage is in a different currency from your rental income, you've got another. Investors sometimes chase a market without asking whether the financing and income streams are naturally aligned.

That matters for return analysis. Yield can look attractive in local currency and less attractive once exchange movements, transfer spreads, and debt payments are considered. I'd always stress test the deal for adverse currency moves rather than assuming today's rate holds.

A property can perform operationally and still disappoint financially if the debt currency, income currency, and home currency pull in different directions.

Alternatives to a standard overseas mortgage

A traditional mortgage isn't always the best answer.

Releasing equity from a home-country property can be cleaner if local lending is awkward or slow. It gives you flexibility and may let you negotiate abroad as a cash buyer. The trade-off is concentration of risk against your existing property.

Developer finance can suit new-build purchases, especially where staged payments are normal. It can be useful, but the legal protections and delivery risk need careful review.

Bridging or short-term finance can help if you're buying quickly, restructuring a property, or waiting for a later refinance. This is usually a specialist tool, not something to use casually.

Cash purchase using liquid assets removes lender friction, but it also ties up capital that might be better deployed elsewhere.

The right choice depends on whether your priority is maximizing financing, speed, simplicity, or control over currency exposure.

Country-Specific Tips and Your Investor Checklist

Different markets reward different financing tactics. The mistake is assuming the mortgage process is basically the same everywhere.

Established markets versus emerging ones

In Spain, Portugal, and France, non-resident mortgage routes are generally easier to map because these markets have a long history of international demand. Documentation still matters, but the process is more familiar to banks, valuers, and lawyers. If Spain is on your shortlist, it helps to review current mortgage conditions in Spain before you approach lenders.

In emerging markets, local opportunity can be stronger, but mortgage execution is often less predictable. Lender appetite may be narrower. Local legal process may be more relationship-driven. The right response isn't to avoid these markets. It's to treat finance certainty as part of market selection.

The UK is its own interesting example from the foreign buyer side. International Citizens Insurance states that the UK has minimal restrictions for foreign buyers, making it one of the more accessible markets for international purchasers, while also noting that many properties may need renovation, which can increase scrutiny during mortgage approval, as outlined in International Citizens Insurance's guide to buying property abroad.

Mortgage-specific observations by market type

Here's the pattern I see most often:

- Established Western European markets: Better lender familiarity, but still document-heavy for non-residents.

- Markets with older housing stock: More valuation and condition scrutiny. Finance can tighten if works are needed.

- Developer-led markets: Easier entry points for some buyers, but you need to inspect the contract, handover schedule, and exit strategy carefully.

- Short-let driven destinations: Attractive in presentation, but lenders may still focus more on your personal income than on expected holiday rental performance.

If part of your strategy includes holiday letting, it helps to study operating models in mature rental markets. Even a niche guide like these strategies for SC waterfront rentals can sharpen your thinking on occupancy assumptions, seasonality, and guest-use economics.

Investor checklist

Before you submit any application, make sure you can answer these questions clearly:

- Can I fund the deposit and all buying costs without stretching liquidity too far?

- Which lending route fits my income profile and target country best?

- Will the lender accept my income type in the format I can prove it?

- Am I relying on rental income that the lender may ignore?

- Do I understand the property's legal status, title position, and any renovation issues?

- What happens to returns if exchange rates move against me?

- If the mortgage falls through, do I have a credible Plan B?

A good overseas purchase starts with boring preparation. That's usually what separates a smooth completion from a deal that looked good online and never got funded.

If you're comparing countries, financing routes, and investment fundamentals, World Property Investor is a strong place to continue your research. The site brings together country guides, mortgage insights, rental market analysis, and practical buying advice so you can evaluate deals with more context and fewer assumptions.