Property investment combines steady rental income with long-term capital growth. For global investors, bricks and mortar can diversify a portfolio, hedge against inflation and provide reliable cash flows when markets wobble.

Why Property Investment Works

According to the Office for National Statistics (ONS) and Gov.uk, UK house prices rose by 2.6% year-on-year in 2025, while private rents climbed 5.0%. These figures illustrate how rental income and capital gains can work in tandem.

Key advantages include:

- A tangible asset that typically keeps pace with inflation

- Predictable rental yields of 4–6% in established markets

- Capital appreciation driven by economic growth and demographic change

A simple rule of thumb: a 5% rental yield plus 2–3% annual price growth can rival—or even surpass—average stock market returns (source: ONS).

Look overseas and emerging markets in Eastern Europe or Southeast Asia often deliver gross yields above 7%, while established hubs like London or Berlin trade at 3–4%.

- UK Outer London Boroughs: average gross yield 4.2% (2025, Gov.uk)

- Berlin: average net yield 3.3% (2025, German Federal Statistics)

- Warsaw: yields up to 8% (local housing authority)

Key Benefits Of Property Investment

- Diversification across regions and asset types

- Amplified returns through mortgage leverage

- Legal protections and tax reliefs for buy-to-let

Due diligence is essential to mitigate tenant defaults, regulatory changes and market cycles.

A Roadmap To Practical Insights

- How to calculate net rental yield and total ROI

- Which financing routes suit international buyers

- A data-driven framework for comparing markets

For a broader introduction, see our Beginners Guide to Real Estate Investing. This guide will end with a clear checklist to turn data into confident action.

Exploring Property Investment Models And Types

Choosing a property investment model depends on your time, capital and risk tolerance. Each approach balances returns, effort and liquidity differently.

Buy-to-Let

Resembles placing cash in a savings account—except you earn a 4–6% rental yield and benefit from capital growth. Typical parameters:

- Gross yield: 4–6%

- Holding period: 5–10 years

- Management: hands-on or via a letting agent

Flipping

Short-cycle strategy: purchase, refurbish and sell. Suitable for active investors with project management skills.

- Yields: 8–12%

- Holding period: 3–12 months

- High management intensity

Development

Involves land or property upgrades to capture significant capital gains. Requires planning, procurement and construction oversight.

- Yields: 15–25%

- Holding period: 1–3 years

- Very high management commitment

REITs

Real Estate Investment Trusts function like property mutual funds. You buy shares, receive dividends and trade on exchanges.

- Yields: 3–5%

- Holding period: 1–5 years

- Passive management, high liquidity

This comparison highlights the trade-off between hands-on involvement and ease of entry.

Case Study Examples

- A UK residential REIT investor collects quarterly dividends while minimising operational duties.

- A developer in Munich negotiates planning permission and achieves a 20% profit on completion.

For off-plan options, review the pros and cons of buying off-plan properties.

Calculating Yields And ROI For Property Investment

Gross Rental Yield

Annual Rent ÷ Purchase Price × 100

Example: £12,000 ÷ £250,000 × 100 = 4.8%

Net Rental Yield

(Annual Rent − Annual Expenses) ÷ Purchase Price × 100

Example: (£12,000 − £2,500) ÷ £250,000 × 100 = 4.2%

Capitalisation Rate (Cap Rate)

Annual Net Income ÷ Current Market Value × 100

Example: £9,500 ÷ £260,000 × 100 = 3.7%

Total Return Metrics

- Cash-on-Cash Return: Annual pre-tax cash flow ÷ equity invested (e.g. £5,000 ÷ £50,000 = 10%)

- Break-Even Ratio: Price decline threshold before income fails to cover costs

- Internal Rate of Return (IRR): Annualised return, including timing of cash flows

Compare these metrics side by side to evaluate deals objectively.

Key Metrics At A Glance

- Gross Yield: 4.8%

- Net Yield: 4.2%

- Cap Rate: 3.7%

Leveraged vs Unleveraged Returns

A 20% deposit on our £250,000 flat means £50,000 equity:

- Unleveraged: Net yield 4.2%

- Leveraged: Cash-on-cash return 10% (assuming a 3.5% mortgage)

Over five years, an IRR of around 12% is feasible with 3% annual price growth and reinvested surplus. Always stress-test for downturns.

For detailed ROI calculations, see our guide on calculating return on investment for real estate.

Securing Financing And Understanding Tax Implications

Mortgage Options

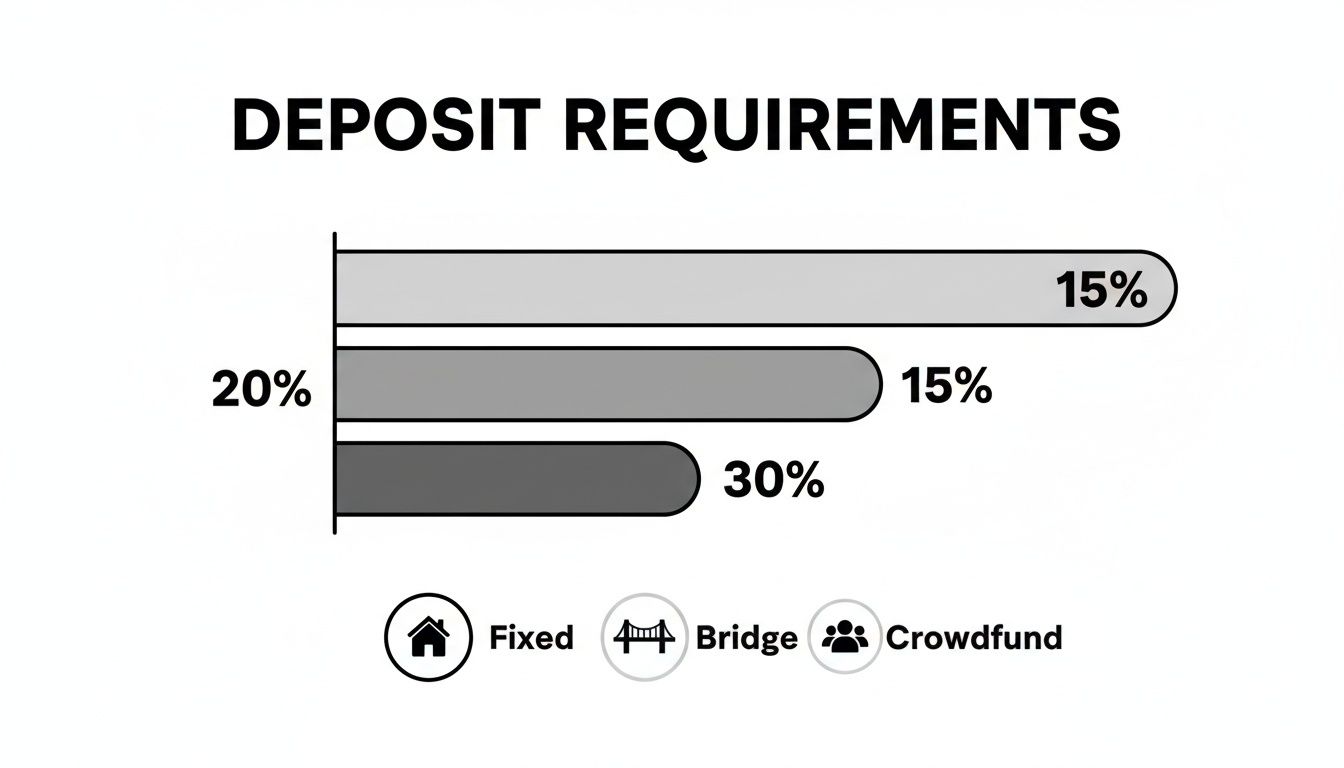

- Fixed Rate: deposit from 20%, stable payments (based on Bank of England base rate)

- Variable Rate: deposit from 15–25%, payments track base rate changes

- Interest-Only: higher deposit or personal guarantee

- Expat Mortgages: 25–30% deposit plus proof of foreign income

| Currency | Loan Amount | Interest Rate | Monthly Payment |

|---|---|---|---|

| GBP | £200,000 | 3.5% | £898 |

| EUR | €230,000 | 2.8% | €930 |

| USD | $250,000 | 4.0% | $1,193 |

Adjust for local base rates and currency fees.

Specialist Finance

Bridging Loans: 0.5–1.5% per month, suited to refurbishments or rapid land purchases.

Crowdfunding Platforms: 5–8% yields with 15% minimum deposit, watch platform fees.

Mezzanine Finance: second-charge debt for larger schemes.

Tax Implications

Cross-border investors face stamp duty, capital gains tax and rental declarations. Typical reliefs:

- Wear and Tear Allowance (furnished)

- Mortgage Interest Relief (basic rate cap)

- Capital Gains Reinvestment Relief

- Non-Resident Trustee Relief

Title searches, planning checks and professional surveys help avoid costly compliance errors. For deeper financing insights, see financing investment property in our guide.

Choosing Markets And Regional Insights

An effective market selection rests on four pillars:

- GDP Growth (ONS, Bundesbank)

- Rental Demand and vacancy rates

- Regulatory Stability (local housing authorities)

- Currency Risk

Regional House Price And Rent Growth

| Region | House Price Growth | Rent Growth |

|---|---|---|

| England | 2.8% (ONS) | 4.9% |

| Wales | 3.1% | 5.2% |

| Scotland | 2.4% | 5.5% |

Comparing Established And Emerging Markets

Mature economies like the UK and Germany offer legal clarity and stable rents. Emerging regions in Eastern Europe or Southeast Asia provide higher yields but carry extra currency and regulatory risks. Balance stability with upside potential.

For a detailed market comparison, see the best countries to invest in property.

Applying The Framework

- Gather GDP, inflation and employment data (ONS, Bundesbank).

- Compare asking rents with completed transactions on local platforms.

- Monitor regulatory updates via housing authorities.

- Run currency-scenario models using forward rates.

Example: Berlin yields 3.3% with transparent landlord laws; Warsaw yields 7%+ but demands careful zloty hedging.

Sectoral Trends

- UK logistics: yields near 5%, driven by e-commerce

- German warehouses: yields around 4% as institutional capital flows in

- Southeast Asian retail parks: yields rebounding to 6%

Key Takeaways For Market Selection

- Prioritise economic growth and regulatory clarity over headline yields

- Layer in ONS data for balanced rental and capital-growth views

- Blend established and emerging markets to spread risk

- Validate assumptions with real-world examples

- Continuously monitor market data

Building Your Buying Checklist And Managing Risks

A robust checklist keeps tasks ordered and reduces oversights. From deal screening to handover, follow these steps.

Valuation And Legal Due Diligence

- Commission a survey via RICS to flag defects.

- Verify title, planning permission and tenant licences.

- Obtain two professional valuations.

Closing And Post-Purchase Steps

- Confirm mortgage offer and solicitor’s terms.

- Secure deposit in a client account.

- Obtain building insurance for completion day.

- Register title with the land registry.

Managing Common Risks

- Diversify by region and asset class.

- Lock in a fixed-rate mortgage to cap costs.

- Maintain a 3–6 month cash buffer for voids and repairs.

- Include break clauses in leases.

Interest Rate Impact

| Scenario | Rate | Monthly Payment | Cash Flow Impact |

|---|---|---|---|

| Base (3.5%) | 3.5% | £950 | — |

| +1% Hike | 4.5% | £1,075 | –£125 |

| +2% Hike | 5.5% | £1,205 | –£255 |

Tenant Default Contingency

- Secure deposits in protection schemes.

- Use direct-debit for rent collection.

- Screen tenants and enforce clear notice periods.

Market Correction Safeguards

- Track local indices via the Office for National Statistics.

- Ensure lender support for void periods.

- Model a 10–15% price fall.

- Predefine exit options (sale, refinance, equity release).

Exit Strategies And Liquidity Planning

- Include staged upgrade clauses for phased sales.

- Negotiate forward-sale agreements.

- Factor in 6–12 month marketing windows.

- Maintain relationships with multiple brokers.

Additional Investor Examples

| Investor | Location | Deposit | Mortgage Rate | Net Yield | Risks Mitigated |

|---|---|---|---|---|---|

| German Buyer | Lisbon | 20% | 4.2% | 6.8% | Interest-rate risk |

| Australian Investor | Manchester | 15% | 3.8% | 5.5% | Vacancy risk |

Real returns hinge on risk controls as much as on headline numbers.

Checklist Summary

| Step | Action |

|---|---|

| Deal Screening | Location, yield and financing filters |

| Valuation | Comparables, surveys and cap rate checks |

| Legal Due Diligence | Title search, planning and lease review |

| Financing Approval | Mortgage offer, deposit and terms confirmed |

| Contract Exchange | Deposit paid, insurance in place |

| Completion Day | Funds transferred, keys and handover |

| Asset Management | Tenant onboarding, maintenance schedule |

Key Takeaways

- Use a step-by-step checklist to avoid oversights

- Balance yield targets with financing and legal requirements

- Stress-test for rate rises and void periods

- Engage local experts for surveys and legal advice

- Update exit plans as markets evolve

Professional Support

- RICS-chartered surveyor for valuations

- Licensed conveyancer for contracts and registration

- Tax adviser for cross-border reliefs

Ongoing Asset Management

- Automate tasks with property-management software

- Conduct tenant satisfaction surveys

- Review insurance cover annually

- Update financial models twice a year

- Build a multi-year sinking fund for refurbishments

Frequently Asked Questions

Buy-to-Let Capital Requirements

Expect to invest around 20–30% of property value plus 3–5% closing costs. In some emerging markets, deposits can reach 30% and fees 6%.

Example: A £300,000 flat in Manchester typically requires a £60,000 deposit and circa £9,000 in stamp duty and legal fees.

Standardising Yield Comparisons

To compare apples with apples:

- Calculate gross yield in local currency.

- Deduct local withholding and income taxes.

- Subtract management and maintenance costs.

Berlin’s 3.3% cap rate may compress to 2.8% net after taxes, whereas Warsaw’s 8% can sit nearer to 5.5%.

Legal Checks For Overseas Investors

- Verify title history for liens or easements.

- Use a local solicitor for contract review and compliance.

- Register purchases with the land authority.

Non-resident UK landlords must register to claim tax reliefs and stay compliant.

When To Leverage Your Purchase

Debt magnifies both gains and losses.

- £50,000 equity on a 3.5% mortgage can yield 10% cash-on-cash.

- Unleveraged net yield on the same asset is 4.2%.

Stress-test for rate rises: a 1% hike can reduce cash flow by around 15% in many European markets.

Visit World Property Investor to compare global opportunities today.