Investing in property beyond your home country is a classic strategy to diversify a portfolio, protecting it from the economic fluctuations of a single, localised market. It provides access to potentially higher rental yields and capital growth opportunities that may not exist domestically, spreading your risk across different currencies and legal frameworks.

Why You Should Consider Investing in Global Property

Expanding your property portfolio beyond familiar borders is a strategic move that unlocks a superior tier of investment possibilities. While your domestic market offers comfort and familiarity, it also means concentrating your capital in one economic basket.

A downturn in the local economy, an adverse change in government policy, or a sharp rise in interest rates can negatively impact your entire asset base simultaneously. International real estate investing provides a powerful hedge against these single-market risks.

The Core Benefits of a Global Mindset

The primary driver for most investors is diversification. By holding assets in different countries, you are not entirely dependent on one economy’s performance. For instance, while the UK property market might experience a period of stagnation, a well-chosen property in a thriving Southeast Asian city could be delivering strong capital growth. This geographical spread helps to smooth returns over the long term.

Beyond risk mitigation, investing globally opens doors to markets with fundamentally different characteristics. Some offer significantly higher rental yields than can be achieved at home, providing a robust stream of passive income.

Consider these key advantages:

- Higher Rental Yields: Many emerging markets offer gross rental yields that far exceed those in established Western economies. A city-centre flat in a high-growth area might yield 6-8%, compared to just 3-4% in a major city like London.

- Capital Appreciation: Investing in areas with planned infrastructure projects, growing populations, and increasing foreign investment can lead to substantial long-term capital growth.

- Currency Diversification: Holding assets and earning rent in different currencies (such as Euros or US Dollars) can protect your wealth from fluctuations in your home currency.

- Lifestyle and Personal Use: A property abroad can double as a holiday home that generates income when not in personal use, effectively helping it to pay for itself over time.

For the strategic investor, international property is not merely about owning a holiday home. It is about building a resilient, geographically balanced portfolio that can weather economic storms and capitalise on global growth trends wherever they appear.

Ultimately, international real estate investing allows for greater selectivity. You can pinpoint markets that align precisely with your financial goals—whether that is stable, long-term income from a buy-to-let in Germany or opportunistic growth from a development project in Portugal.

How to Select the Right International Property Market

Choosing where to invest your capital is the single most critical decision you will make. This choice dictates your potential returns, the risks you will face, and the day-to-day reality of managing your asset. A correct decision simplifies subsequent steps; a poor one can undermine even a high-quality property.

Successful investors learn to look beyond glossy marketing materials and focus on objective data. This disciplined, analytical approach separates a sound, long-term investment from a speculative gamble. It requires an understanding of a market’s vital signs, from its economic pulse to its demographic trends, enabling you to identify genuine opportunities with confidence.

Analysing Economic Stability and Growth Drivers

A country’s economic health is the bedrock of its property market. A stable, growing economy creates jobs, attracts talent, and boosts disposable incomes—all of which fuels tenant demand and supports property prices.

Begin by assessing the macroeconomic picture. Look for consistent GDP growth, low unemployment, and manageable inflation. Government bodies such as the UK’s Office for National Statistics (ONS) or international organisations like the IMF provide reliable data. Political stability is equally critical; a predictable legal and political environment provides the confidence necessary for long-term investment.

A powerful indicator of future property demand is foreign direct investment (FDI). When international companies invest in a country, they create jobs, which in turn brings new tenants into the rental market. According to Gov.uk data, this influx of capital from businesses directly supports local economies and property markets.

Interpreting Key Property Metrics

After evaluating the macroeconomic overview, drill down into property-specific data. For any buy-to-let investor, two metrics are absolutely essential: rental yield and the price-to-rent ratio.

- Gross Rental Yield: This is the annual rent divided by the purchase price, expressed as a percentage. It is a quick method for comparing the income potential of different properties and markets.

- Price-to-Rent Ratio: This compares median property prices to median annual rents. A low ratio suggests it is more favourable to buy than rent, which is a strong indicator of healthy rental demand.

A high rental yield is always appealing, but it must be weighed against capital growth potential and local risks. A 7% yield in an unstable market is often a far greater gamble than a 4% yield in a stable, established city with strong long-term growth prospects.

These figures help to quantify the immediate return and assess whether a market is becoming overheated. While the highest yields are often found in emerging markets, they usually come with higher risks. The key is to balance the promise of returns with the stability of the investment environment.

Established vs. Emerging Markets: A Strategic Comparison

Your choice between an established and an emerging market should be aligned with your personal risk tolerance and investment objectives. Neither is inherently superior—they simply offer different risk-reward profiles.

| Market Type | Key Characteristics | Best For Investors Seeking |

|---|---|---|

| Established Markets (e.g., UK, Germany) | Transparent legal systems, political stability, high liquidity. Often lower rental yields and higher entry prices. | Stable, long-term income, lower risk, and capital preservation. |

| Emerging Markets (e.g., Turkey, Thailand) | Potential for high capital growth, higher rental yields, and lower entry costs. Greater currency and political risks. | Higher returns, capital appreciation, and who are comfortable with more volatility. |

An investor focused on building a steady retirement income might favour a buy-to-let flat in a major UK city, valuing its reliable legal framework over a higher but less certain yield. In contrast, an investor seeking faster growth might find an off-plan property in a rapidly developing part of Southeast Asia a better fit. You can explore our detailed analysis to find the best buy-to-let locations that match your goals.

Ultimately, thorough research into demographic trends—such as population growth, urbanisation, and the presence of universities or major employers—will reveal where sustainable tenant demand truly lies. Combine this on-the-ground insight with solid economic data, and you will be in a strong position to make an informed and confident decision.

Choosing Your Global Property Investment Strategy

Once you have identified a promising market, the next step is deciding how to invest in it. There is no single “best” approach to buying property abroad; the right strategy depends on your personal goals, risk tolerance, and the amount of time you wish to dedicate to management.

The most effective investors match their strategy to the market’s strengths. A fast-growing city in an emerging economy may be ideal for a capital growth strategy, while a stable European capital with a large tenant pool is well-suited for generating reliable rental income.

Let's examine the three most common models for international investors.

The Classic Buy-To-Let Model

The buy-to-let is the cornerstone of most property portfolios. The objective is simple: purchase a property, secure a long-term tenant, and collect a steady, predictable income each month. This strategy is favoured for its stability and the potential for the property’s value to appreciate over time.

This approach works best in urban centres with strong, diverse economies—cities with major universities, corporate headquarters, or technology hubs. These locations offer a deep and consistent pool of professional tenants, which is the best defence against long and costly vacancy periods. A modern flat in a well-connected district of a major city like Berlin or Lisbon is a classic buy-to-let investment.

The success of any buy-to-let investment depends on tenant demand. Your focus should always be on locations with solid employment markets and population growth, as these are the engines that power a healthy rental sector.

While generally a lower-risk strategy, managing a property from another country requires professional support. You must factor in management fees, maintenance costs, and potential void periods when calculating your net yield.

Maximising Returns With Holiday Lets

For investors prepared to be more hands-on, the holiday let (or short-term rental) model can deliver significantly higher returns. This strategy involves buying property in a popular tourist destination and renting it out to travellers by the night or week.

Prime locations for this approach include coastal resorts, historic city centres, or areas near major cultural attractions. A villa in Portugal’s Algarve or a chic apartment in a historic part of Florence, Italy, are prime examples. The income generated during the peak season can often exceed what a long-term rental would produce in an entire year.

However, this approach comes with trade-offs:

- Higher Operational Demands: Holiday lets are a business. They require constant management, from marketing and guest communication to cleaning and changeovers between stays.

- Income Seasonality: Your earnings will likely peak during tourist seasons and decline significantly during quieter months. This must be factored into your annual cash flow projections.

- Regulatory Scrutiny: Many cities are implementing stricter regulations on short-term rentals. It is essential to research local laws and licensing requirements before purchasing.

Targeting Capital Growth

The capital growth strategy focuses less on immediate rental income and more on the long-term appreciation of the property itself. It involves identifying and investing in areas on the cusp of significant growth, often before this potential is widely recognised by the market.

This could mean buying in a neighbourhood undergoing major regeneration, a city set to benefit from a new infrastructure project, or an emerging market with a rapidly expanding middle class. An off-plan apartment in a developing district of Dubai, for instance, would be a typical capital growth play.

This strategy requires a keen eye for future trends and a higher tolerance for risk, as the anticipated growth is not guaranteed. Investors usually need a longer time horizon—often five years or more—to realise their returns. Understanding your options is a key part of the process, and you can learn more by exploring our detailed guide on financing your international investment property.

Getting to Grips with Foreign Legal and Financial Systems

Successfully investing in international real estate requires a mastery of detail. While selecting the right market and strategy is the exciting part, it is the practical work of navigating a country’s legal and financial rules that protects your capital and ensures smooth operations. This is where a clear head and a meticulous approach are invaluable.

Every country has its own unique regulations for property ownership, taxes, and finance. Understanding these rules is not merely a formality; it is a fundamental part of your due diligence. An error in this area could lead to costly delays, unexpected tax bills, or even challenges to your legal ownership.

Understanding Foreign Ownership Rules

First, you must confirm that you are legally permitted to buy. Foreign ownership laws vary significantly from one country to another. Some nations welcome overseas capital, while others impose significant restrictions on what non-residents can purchase.

One of the first concepts you will encounter is the type of ownership, or ‘title’, you will hold. The two most common forms are:

- Freehold: This is the most complete form of ownership. You own the property and the land it sits on outright and in perpetuity. It is the most secure form of ownership, common in countries like the UK.

- Leasehold: This grants you the right to use the property for a fixed, long-term period—often 99 or even 999 years. You own the building, but the land belongs to a freeholder, to whom you may have to pay ground rent. This is very common for flats and apartments.

Many popular investment destinations have specific rules for foreign buyers. Some may restrict the purchase of agricultural land or property near military installations. In other locations, such as Thailand, foreigners cannot directly own land on a freehold basis and must use alternative structures like a long-term lease.

Demystifying the Tax Landscape

Tax is an unavoidable and complex aspect of international investing. Failure to understand your obligations from the outset can significantly erode your returns. Your tax liabilities will typically arise in three main areas.

First is the tax paid upon purchase. This is usually a stamp duty or property transfer tax—a percentage of the purchase price paid to the government upon completion. The rates vary widely; for example, the stamp duty on an additional property in England can be substantial compared to the much lower rates in some other European countries.

Next, you will be taxed on any income the property generates. Rental income is almost always taxed in the country where the property is located. Finally, when you sell, you will likely face a Capital Gains Tax (CGT) on any profit you have made.

A crucial element for any international investor is the Double-Taxation Treaty (DTT). These are agreements between countries designed to prevent you from being taxed twice on the same income—once in the property's location and again in your country of residence. Always check if a DTT exists between your home country and your target investment location.

Securing the Right Financing

Financing an overseas purchase raises a key question: should you use a local bank in that country or an international lender? Both options have advantages and disadvantages.

Obtaining a mortgage from a local bank can be a good choice, as they possess in-depth knowledge of their own market and legal requirements. The drawback is that as a non-resident, you will likely face stricter lending criteria, higher interest rates, and be required to provide a larger deposit—often 30-40% of the property's value.

Alternatively, using an international lender or a specialist broker in your home country might feel more familiar. They are often better equipped to assess your finances based on your local credit history. The key is to compare rates, fees, and terms from multiple sources to find the most suitable deal. For a deeper look at this, our guide to investing in overseas property offers further valuable insights.

Ultimately, the most important takeaway is this: you must build a trusted local team. A good solicitor, a sharp tax adviser, and a reliable property manager are not expenses—they are essential investments. These professionals will be your eyes and ears on the ground, guiding you through an unfamiliar system and protecting your asset for years to come.

Comparing Established and Emerging Property Hubs

This is where theory meets practice. A sound investment strategy is only effective when you can confidently compare different market types and select the one that aligns with your objectives. At its core, international property investing involves a classic trade-off: prioritising the security of an established hub versus pursuing the higher growth potential of an emerging one.

An established market, like the UK, offers a robust legal framework, political stability, and high liquidity. An emerging hotspot, like Turkey, may offer the prospect of much higher rental yields and faster price growth, but this often comes with currency volatility and a less predictable regulatory environment. Neither is automatically better—they simply fulfil different roles in a balanced portfolio.

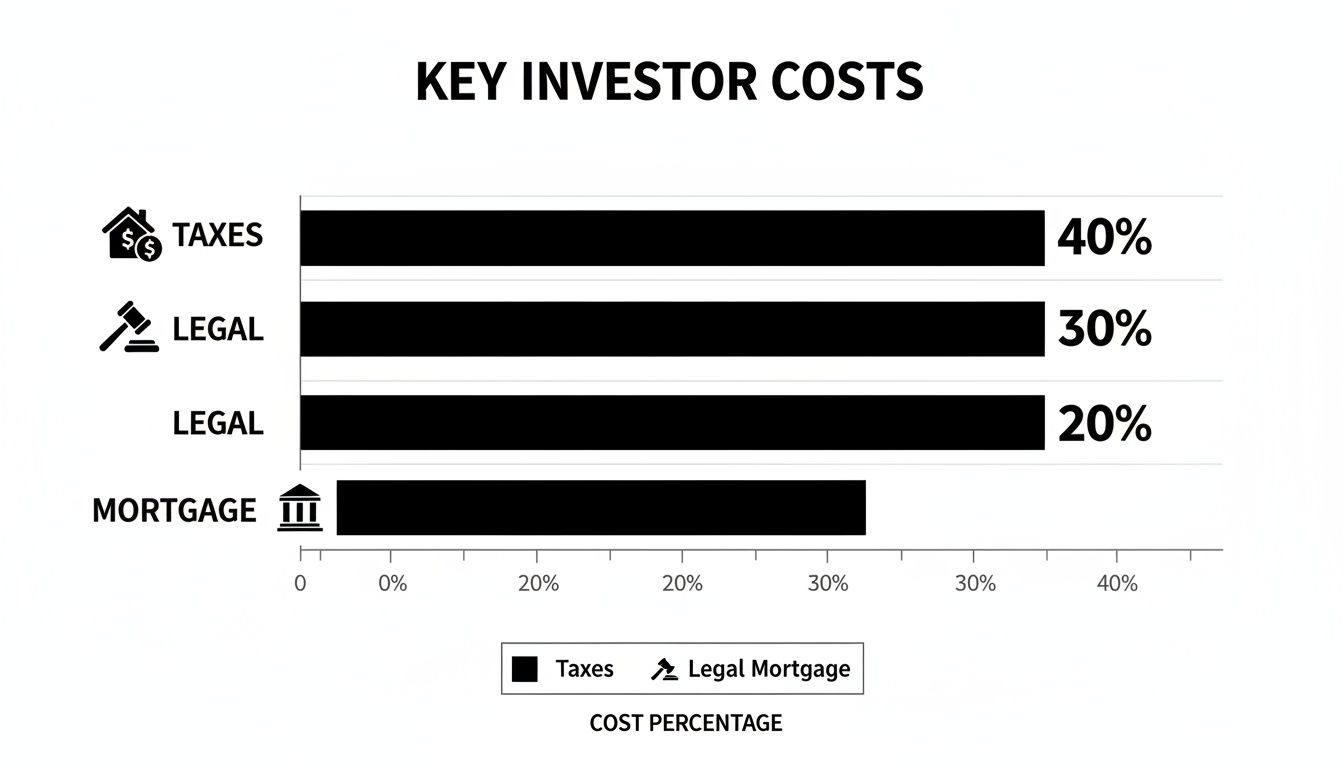

Before examining specific countries, it is crucial to understand the upfront costs. This extends beyond the purchase price; taxes and fees can significantly impact your budget if you are unprepared.

As the chart illustrates, taxes are often the single largest associated cost. This is why obtaining professional advice on local tax obligations is essential before making an offer. This step distinguishes professional investors from amateurs.

International Market Snapshot Comparison

To make this tangible, let's examine some real-world data across two established and two emerging markets. This table provides a high-level view of what you can expect in terms of costs, returns, and the general investment climate.

| Metric | UK (London) | Portugal (Lisbon) | Turkey (Istanbul) | Thailand (Phuket) |

|---|---|---|---|---|

| Avg. Gross Yield | 3-4% | 4-5% | 5-7%+ | 6-8%+ |

| Capital Growth | Stable, Mature | Moderate to Strong | High Potential | Moderate to High |

| Market Stability | Very High | High | Moderate (Currency Risk) | High (Tourism Dependent) |

| Foreign Ownership | Straightforward | Straightforward (EU) | Straightforward | Restricted (Condos Only) |

| Typical Investor | Risk-Averse, Capital Preservation | Balanced, Lifestyle & Growth | Growth-Focused, Higher Risk | Lifestyle, Holiday Let Income |

This snapshot clearly highlights the core trade-offs. London offers predictability but modest yields, whereas markets like Istanbul and Phuket promise higher income but come with their own set of rules and risks that require careful management.

Established Hubs: The Appeal of Stability

Established markets are the bedrock of many global property portfolios. They are the blue-chip assets of the real estate world: transparent, with mature legal systems and deep pools of tenants, making them ideal for investors seeking capital preservation and a steady, reliable income.

The United Kingdom (London)

London has long been a global safe haven for property. Investors are drawn to its political stability and landlord-friendly legal system. While entry prices are high and gross rental yields are modest, typically hovering around 3-4%, the market offers exceptional liquidity. The high volume of transactions means a buyer can almost always be found when it is time to exit.

The UK market has proven remarkably resilient even in the face of economic headwinds. The enduring appeal of the UK market for global investors from the CoStar report underscores this confidence, making it a primary choice for conservative investors.

Portugal (Lisbon)

Portugal has transitioned from an emerging hotspot to a solid, established European destination. It offers an excellent quality of life, a stable political climate as part of the EU, and attractive residency programmes. In the best parts of Lisbon, rental yields can reach 4-5%, providing a slight advantage over London with a much lower cost of entry. The market is fuelled by strong demand from tourists, expatriates, and a thriving technology scene, which together create a very solid tenant base.

Emerging Hubs: The Pursuit of Growth

Emerging markets are where investors seek higher returns. These are often countries with fast-growing economies, an expanding middle class, and major infrastructure projects—all fertile ground for significant capital growth. But with greater potential comes greater risk.

Turkey (Istanbul)

Istanbul is a powerhouse market, situated at the crossroads of Europe and Asia. It offers comparatively low property prices and the potential for gross rental yields of 5-7%, and even higher in certain districts. The country's citizenship-by-investment programme has also served as a major attraction for foreign buyers.

The primary risk in markets like Turkey is currency volatility. A sudden depreciation in the Turkish Lira can erode rental income and capital gains when converted back to your home currency. This is a risk that must be actively managed.

Thailand (Phuket)

Known for its world-class tourism, Thailand—particularly locations like Phuket—is a top choice for holiday let investments. Yields on short-term rentals can be excellent, often exceeding 6-8% net in a strong year. However, foreign ownership laws are strict. Non-residents cannot own land freehold, making condominiums the simplest and most common investment vehicle. Expert local legal guidance is essential to navigate this landscape.

If you are keen to explore locations with high-growth potential, you might want to review our guide on the top emerging property investment markets to watch. It provides a deeper analysis of some of the most exciting opportunities available today.

Managing the Key Risks of Investing Abroad

Successful international property investing is not about avoiding all risk—that is impossible. It is about identifying challenges clearly, understanding them, and implementing a plan to mitigate them before they become significant problems.

A prepared investor is a protected one. Beyond market fundamentals, you must account for the unique hurdles of cross-border asset ownership—from currency fluctuations that can erode profits to the practical challenges of managing a property from thousands of miles away.

The most common financial pitfall is currency risk. Even if all other factors are positive, an adverse movement in the exchange rate can severely impact your returns. For example, if your mortgage is in Euros but your rental income is in British Pounds, a weakening Pound would make your mortgage payments more expensive in real terms, squeezing your monthly cash flow.

Mitigating Financial and Political Uncertainty

To manage currency volatility, savvy investors often use financial instruments like forward contracts. These allow you to lock in an exchange rate for a future transaction, providing certainty when transferring purchase funds or repatriating rental profits.

Political and regulatory risks are equally critical. A government could abruptly change rules on foreign ownership, or a new tax could be introduced that alters the financial viability of your investment. This is precisely why stable, transparent markets are so popular with long-term global investors.

Confidence in a country's legal and political framework is a key driver for foreign investment. This stability is a primary reason why certain established markets consistently attract a high volume of international capital.

The best defence against regulatory surprises is thorough due diligence and a reliable local legal team. They can provide insight into proposed legislative changes and help structure your investment to be as resilient as possible.

Addressing On-the-Ground Operational Challenges

Sometimes, it is the simple, day-to-day operational issues that cause the greatest difficulties. An unreliable property manager can lead to long vacancies, missed repairs, and unhappy tenants, which directly reduces your returns. When managing from a different time zone, these small problems can quickly escalate.

To mitigate these operational risks, you need a robust plan:

- Vet Your Partners: Conduct exhaustive background checks on all local partners, from solicitors to property managers. Seek recommendations and find reviews from other foreign investors who have worked with them.

- Establish Clear Communication: Set a schedule for regular updates and agree on clear key performance indicators (KPIs) for your management team. Do not leave things to chance.

- Understand Local Laws: Ensure you are fully compliant with local tenancy laws and tax obligations. Non-compliance is a certain path to legal difficulties.

A firm grasp of your financial duties is non-negotiable. For a detailed breakdown, our guide on how to understand property taxes when investing abroad can be very helpful. This prudent and proactive approach ensures your international real estate journey is built on a solid foundation of preparation.

Got Questions About Investing Abroad?

Even with a well-defined strategy, taking the first step into international property will naturally raise questions. To provide further clarity and confidence, here are straightforward answers to the queries we hear most often from investors new to the global market.

How Much Capital Do I Really Need to Start?

The answer depends entirely on the market. While a significant sum is required for a prime flat in London or Paris, you can find modern, high-quality apartments in parts of Eastern Europe or Southeast Asia for well under £100,000. The global property market offers a vast range of price points.

However, the purchase price is only the starting point. A prudent investor always budgets an additional 10-15% on top of the property's value to cover the associated costs of acquisition.

- Legal Fees: For conveyancing and contract reviews. This is not an area to cut corners.

- Taxes: Such as stamp duty or property transfer tax. These are applicable in nearly every country.

- Due Diligence: Costs for building surveys and professional valuations.

- Furnishing: If you plan to let the property furnished, this cost must be factored into your budget.

Can I Obtain a Mortgage as a Foreigner?

Yes, this is often possible, but be prepared for additional paperwork and scrutiny. Local banks in your target country will almost certainly require a larger deposit than they would from a resident—typically 30-40% of the property’s value. They may also charge a slightly higher interest rate.

Lenders will want to see detailed proof of your income and will conduct a thorough review of your credit history in your home country. An excellent alternative is to engage an international mortgage broker. These specialists have existing relationships with lenders who are experienced in assessing overseas buyers.

What is the Best Way to Find a Good Property Manager?

Finding a reliable person on the ground to manage your investment is as crucial as selecting the right property. They are your local representatives.

The most effective method is to obtain personal recommendations from other foreign investors in the area. If that is not possible, look for established local firms with a solid track record and check for any professional accreditations they hold.

Always interview several candidates. Ask for references from their current clients and contact them directly. A great manager is transparent, communicates clearly, and provides detailed financial reports to demonstrate that your investment is being managed professionally.

Ready to explore the world's most promising property markets? World Property Investor provides the in-depth guides and data-driven analysis you need to invest with confidence. Visit us at https://www.worldpropertyinvestor.com to start your research today.