Global property investment is the strategic purchase of real estate outside your home country to generate rental income, capital growth, or both. It is a powerful method for portfolio diversification, accessing higher yields, and protecting wealth from domestic economic instability. This guide provides an authoritative overview for investors considering international markets.

Why Invest in Property Beyond Your Borders?

Expanding your property portfolio into international markets is a calculated decision to build a more resilient and profitable asset base. While investing domestically is familiar, a global approach unlocks opportunities unavailable at home, shielding your capital from localised market downturns and currency fluctuations.

The core principle is diversification. If the UK property market, for example, enters a period of stagnation, a well-chosen property in a growing economy like Portugal or Dubai could continue to deliver strong returns. This strategy is fundamental to long-term wealth protection.

Unlocking Higher Yields and Growth

A primary driver for investing overseas is the pursuit of superior returns. Rental yields—the annual rental income as a percentage of the property’s value—vary significantly across countries. While prime cities like London or Sydney might offer gross yields of 3-4%, certain high-demand urban centres in emerging economies can deliver 6-8% or more.

By looking overseas, investors gain access to markets at different stages of their economic cycle. Investing in a country with a burgeoning middle class, rapid urbanisation, and significant infrastructure development can lead to substantial capital appreciation that far outpaces more mature, stable markets.

Key Drivers for Global Investors

Four core factors consistently attract investors to international real estate:

- Geographic Diversification: Spreading investments across different countries reduces portfolio exposure to any single nation's political or economic risks.

- Currency Hedging: Earning rental income in a strong or stable foreign currency, such as the US Dollar or Euro, can protect purchasing power if your home currency weakens.

- Access to New Markets: Some economies grow faster than others. Global investment allows you to tap directly into this growth, whether in the tech hubs of Eastern Europe or the tourism hotspots of Southeast Asia. Our guide on the top emerging property investment markets provides a deeper dive.

- Lifestyle and Personal Use: Investment is not always purely financial. Owning property abroad can offer personal benefits, such as a holiday home, a future retirement location, or a base for international business.

How to Analyse International Property Markets

Successful global property investment is built on meticulous analysis, not speculation. To identify genuinely promising opportunities, a robust framework is required to assess the economic and demographic trends that support long-term property values.

Analysis should begin with macroeconomic indicators, which provide a snapshot of a country’s economic health. A rising Gross Domestic Product (GDP) signals a growing economy, which typically translates into higher wages and stronger housing demand. According to major economic bodies like the World Bank, consistent GDP growth that outpaces the regional average is a strong indicator of a market with potential for capital growth.

Beyond GDP, key metrics include employment rates and infrastructure spending. A falling unemployment rate means more individuals have disposable income for rent or property purchases. Major government investment in new transport links, hospitals, or digital networks can be a powerful catalyst, unlocking value in previously overlooked areas.

Decoding Property-Specific Metrics

Once the macroeconomic climate is understood, the focus must shift to data specific to the property market. These metrics reveal the current health and potential profitability of real estate in a given area.

- Price-to-Rent Ratio: This is calculated by dividing the median property price by the median annual rent. A low ratio suggests it is more favourable to buy than rent, often indicating strong rental demand and healthy yields.

- Rental Yield: This is the gross annual rental income expressed as a percentage of the property’s price. Comparing yields between cities or neighbourhoods helps pinpoint where capital will work most effectively.

- Historical Price Trends: Analysing long-term price cycles helps to understand a market's maturity and volatility. Stable, established markets often show slower, steadier growth, while emerging markets can exhibit sharper peaks and troughs.

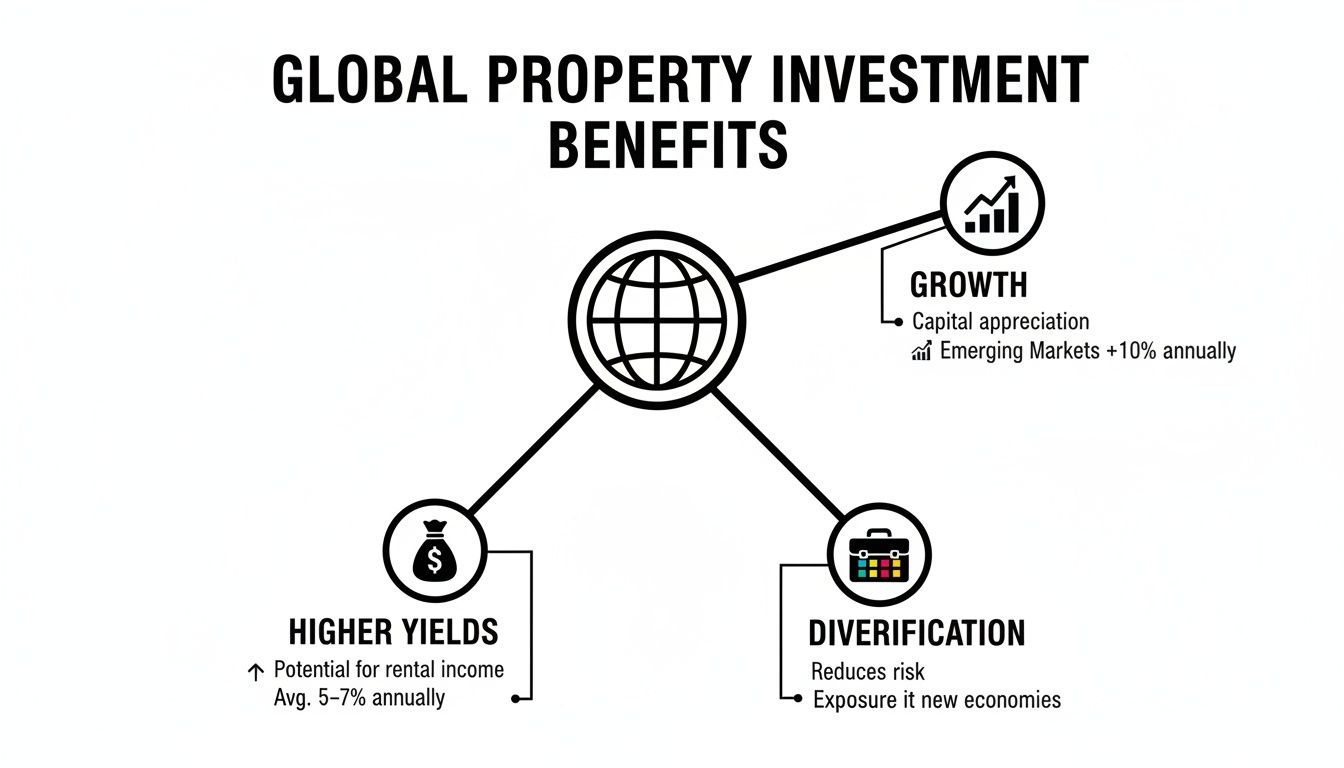

The diagram below summarises the core benefits that a well-analysed international property investment can deliver.

The primary advantages are the potential for higher yields, capital growth, and crucial portfolio diversification.

Established vs. Emerging Markets: A Comparison

Research will lead to a critical decision: investing in a stable, established market or a high-growth emerging one. Each presents a distinct risk-and-reward profile, and the correct choice depends on your financial goals and risk tolerance.

An established market is analogous to a blue-chip stock—predictable, transparent, and generally lower risk. An emerging market is more akin to a tech start-up—it offers the potential for explosive growth but comes with higher volatility and less certainty.

Established markets, such as the UK, Germany, or Canada, are characterised by:

- Strong legal frameworks that protect property rights.

- High levels of transparency with accessible data.

- Economic and political stability.

- Lower but more consistent rental yields and capital growth.

For instance, data from the Halifax House Price Index, a long-running UK series, shows a clear pattern of long-term appreciation. This reflects the steady, reliable growth typical of a mature market. Further data on UK housing trends can be found at sources like Trading Economics.

Conversely, emerging markets in regions such as Southeast Asia, Eastern Europe, or Latin America offer a different proposition. They are typically defined by:

- Rapid economic growth and urbanisation.

- A growing middle class fuelling housing demand.

- Higher potential for capital appreciation and rental yields.

- Greater political risk, currency volatility, and less market transparency.

Choosing between them is not about which is "better," but which aligns with your investment strategy. A balanced portfolio may include properties from both categories, blending stability with high-growth potential. Our guide to investing in overseas property offers further insights.

Market Selection Checklist: Established vs. Emerging Markets

This checklist outlines the key differences to help you weigh which approach fits your objectives.

| Factor | Established Markets (e.g., UK, Germany) | Emerging Markets (e.g., Thailand, Turkey) |

|---|---|---|

| Capital Growth | Slow and steady appreciation | High potential, but more volatile |

| Rental Yields | Lower but consistent (3-5%) | Higher potential (6-10%+) |

| Market Stability | High; less prone to shocks | Lower; can be affected by politics/economy |

| Legal Framework | Strong, clear property rights | Can be complex and subject to change |

| Data Transparency | Excellent; abundant public data | Limited; requires more on-the-ground research |

| Entry Costs | High purchase prices | Lower entry points |

| Risk Profile | Low to moderate | Moderate to high |

| Best For | Risk-averse, wealth-preservation investors | Growth-focused, higher-risk tolerance investors |

This framework clarifies the trade-offs. Established markets offer security, while emerging markets present the potential for greater returns. The key is to understand the associated risks before committing capital.

Navigating Foreign Ownership and Tax Rules

Beyond market analysis, the most significant hurdles for global investors are often administrative. Understanding local laws on foreign ownership and the tax implications of a purchase is fundamental.

A misstep can lead to unforeseen costs that erode returns or, in the worst cases, significant legal complications. Each country has its own regulations; some welcome foreign buyers, while others impose strict limits on what non-residents can purchase and where.

Understanding Ownership Structures: Freehold vs. Leasehold

One of the first legal concepts to understand is the type of ownership. The distinction between freehold and leasehold is critical, as it dictates your rights and long-term control over the property.

- Freehold: This is the most complete form of ownership. When you buy a freehold property, you own the building and the land it stands on in perpetuity. This is common for foreign buyers in markets like the UK, Spain, and Portugal.

- Leasehold: With a leasehold, you own the property for a fixed term—often a long one, such as 99 or 999 years—but you do not own the land. At the end of the lease, ownership typically reverts to the freeholder. This structure is common in markets like Dubai (in designated zones) and Thailand, where foreigners are restricted from owning land.

Understanding the ownership structure is vital for your exit strategy and the asset's long-term value.

The Inescapable Reality of Property Taxes

Taxes are a constant in property investment, and they vary substantially between countries. Failure to budget for them can turn a profitable investment into a financial drain. Tax liabilities generally fall into three categories.

A successful global property investor is not just an expert in markets, but also a diligent student of tax codes and legal frameworks. The purchase price is only the beginning of your financial commitment; ongoing taxes and compliance costs determine your true net return.

Common taxes include:

- Acquisition Taxes: These are one-off costs paid upon purchase completion. In Spain, this is the Impuesto de Transmisiones Patrimoniales (ITP) on resale properties, while in the UK, it is the Stamp Duty Land Tax (SDLT). These taxes are usually tiered based on the property's value.

- Annual Property Taxes: These are ongoing council or municipal taxes. In France, this is the taxe foncière, and in Portugal, it's the Imposto Municipal sobre Imóveis (IMI). These funds typically support local services.

- Capital Gains Tax (CGT): This is the tax paid on the profit made when the property is sold. Rates and exemptions differ widely. For example, the UAE currently has 0% CGT on property sales, making it highly attractive for investors focused on capital growth.

Thorough research into these costs is essential. To go deeper, you can understand property taxes in greater detail with our comprehensive guide.

Finding Reputable Local Counsel

The single most important step to manage legal complexity is to hire an independent, reputable lawyer in your target country. Do not rely on recommendations from the estate agent or the seller’s solicitor. An independent lawyer works solely for you.

They will verify the property's title deed, check for hidden debts or legal claims, explain the sales contract, and provide a clear breakdown of all taxes and fees. Securing the right professional is the cornerstone of a safe global property investment.

Financing Your Investment and Managing Currency Risk

Structuring your finance correctly and managing currency volatility are critical when buying property abroad. Mismanagement of either can erode profits or create significant complications. A considered approach from the outset ensures your capital works for you, not against you.

The first hurdle is funding the purchase. Most investors pursue one of two main routes, with the best choice depending on personal finances and the target market.

Exploring Your Financing Options

Sourcing funds for an overseas purchase requires careful planning. While some investors are cash buyers, most will need to arrange a mortgage or another form of loan.

Common methods include:

- Securing a Local Mortgage: Many international banks in your target country will lend to non-resident investors, provided they meet strict criteria. Expect a larger deposit requirement, often 30-40%, and a thorough income assessment.

- Equity Release from Your Home Portfolio: A popular method is to remortgage a property owned in your home country to release capital. This allows you to act as a cash buyer abroad, which often provides a stronger negotiating position.

- Specialist International Lenders: Some financial firms specialise in cross-border property finance. They are experienced with different legal systems and can sometimes offer more flexible terms than traditional high-street banks.

The right path will depend on interest rates, risk appetite, and the required speed of transaction. Our guide on financing an investment property breaks these options down further.

The Overlooked Challenge of Currency Risk

Once financing is arranged, an ongoing challenge is currency risk. Exchange rates are constantly fluctuating, and even small shifts can significantly impact investment returns.

For example, you buy a flat in Spain for €250,000. At an exchange rate of £1 = €1.15, the property costs £217,391. You secure a local mortgage and begin collecting rent in Euros.

Currency risk affects your investment at every stage: the initial purchase, monthly mortgage payments, receipt of rental income, and the final profit upon sale. An adverse movement can turn a profitable deal into a loss.

If the Pound strengthens against the Euro six months later to £1 = €1.25, two things occur. First, the rental income in Euros is now worth less when converted back to Pounds. Second, the value of your asset, in Pound terms, has just fallen to £200,000. This volatility makes financial planning difficult and directly erodes net profit.

Practical Strategies to Mitigate Currency Risk

While you cannot control foreign exchange markets, you can implement strategies to shield your investment from volatility. These are the tools used by professional investors to create certainty and protect cash flow.

Practical methods include:

- Forward Contracts: This allows you to lock in an exchange rate with a currency specialist for a future date. It is ideal for property purchases as it guarantees the exact cost in your home currency on completion day, regardless of market movements.

- Foreign Currency Bank Accounts: Open a bank account in the country where your property is located. This allows you to collect rent and pay local expenses (such as the mortgage and management fees) in the local currency, minimising conversions and exposure to rate changes.

- Limit Orders: This is an instruction to a currency broker to automatically execute a transfer if a specific target exchange rate is reached. It is an effective way to capitalise on favourable market movements without constant monitoring.

By addressing these financial details from the start, you build a much stronger foundation for your global property investment, ensuring market volatility does not derail your long-term goals.

Comparing Markets: The UK vs. An Emerging Hub

A side-by-side comparison brings the theory of global property investment to life. By contrasting a stable, mature market with a high-growth emerging hub, we can see how different risk-reward profiles translate into practice.

This comparison is crucial. It helps investors move beyond abstract concepts and align their strategy with a market that genuinely fits their financial objectives.

For this analysis, we will use the United Kingdom as our established market and Dubai as its emerging counterpart. Each offers a different set of opportunities and challenges, making them ideal case studies.

Case Study: The United Kingdom

The UK property market is a textbook example of a mature, stable environment. It has long been a destination for international investors seeking security and predictable returns, supported by a robust legal system that protects property rights.

Its transparency is a significant advantage. A vast amount of publicly available data from official sources like HM Land Registry and the Office for National Statistics (ONS) allows for thorough due diligence.

The market is characterised by long, steady cycles of growth rather than the explosive, short-term spikes seen elsewhere. This resilience allows it to absorb shocks and recover over time. More historical data on UK property prices at GlobalPropertyGuide.com can provide further context.

Rental yields in the UK are typically modest but consistent. In London, gross yields often average 3-4%. However, major regional hubs like Manchester and Birmingham are increasingly attractive, with returns often in the 5-6% range, driven by strong student populations and growing professional sectors.

For the risk-averse investor, the UK offers a compelling proposition: lower but reliable rental income, the potential for steady long-term capital appreciation, and the security of a world-class legal framework.

Case Study: Dubai, an Emerging Hub

In sharp contrast, Dubai represents the high-growth dynamics of an emerging property hub. Its market is known for rapid growth cycles, often driven by government initiatives, major global events like Expo 2020, and its status as a tax-efficient business centre. The primary attraction for many investors is the potential for swift and substantial capital growth.

Foreign ownership rules in Dubai differ from the UK. Non-residents can purchase freehold property, but only in specific designated areas. This requires careful legal verification. While the legal system is modern, it is newer and can evolve more quickly than in established Western markets.

The returns profile is also different. Dubai can offer significantly higher gross rental yields, often ranging from 6-8% or more in high-demand communities. This reflects the higher perceived risk and the market's focus on strong cash flow generation.

However, this potential for high returns comes with greater volatility. The market can experience sharp corrections influenced by global oil prices, regional geopolitics, or shifts in economic sentiment. Success here depends not just on property selection, but also on market timing and a higher risk tolerance.

Key Takeaways: UK vs. Dubai

This comparison provides a clear framework for decision-making. Neither market is inherently "better"—they simply cater to different investor profiles.

- Primary Goal: UK investors often prioritise wealth preservation and steady income. Dubai investors are typically focused on high capital growth and strong rental yields.

- Risk Profile: The UK is a low-to-moderate risk market with high stability. Dubai is a moderate-to-high risk market with greater potential for volatility.

- Legal Framework: The UK offers centuries of established property law. Dubai's framework is modern but subject to more rapid change.

- Due Diligence: In the UK, data is abundant. In Dubai, success relies more on on-the-ground research and trusted local partners.

Your choice should depend on your investment timeline, risk tolerance, and financial objectives. A younger investor may be drawn to Dubai's growth potential, while someone nearing retirement might prefer the stability of the UK. A balanced portfolio could include assets from both to blend security with opportunity.

Your Final Due Diligence Checklist

Before committing capital to an overseas property, a methodical due diligence process is your best defence against a poor investment. This checklist provides a framework for protecting your funds, incorporating the key principles covered in this guide. This is the most critical stage of the entire process.

The first step is always legal and regulatory. You must confirm that local laws permit foreign ownership of the specific property type. This requires hiring your own independent lawyer—never one recommended by the seller or developer—to conduct a full title search. Their role is to ensure the property is clear of any hidden debts, liens, or ownership disputes.

Financial Scrutiny and Projections

Once the legal aspects are verified, focus on the numbers. A proper Return on Investment (ROI) projection is more than a simple yield calculation; it must be a detailed financial model accounting for every potential cost.

Your ROI breakdown should include:

- Acquisition Costs: The full purchase price, plus stamp duty, legal fees, and agent commissions.

- Ongoing Expenses: Annual property taxes, building insurance, service charges, and a realistic budget for maintenance—a good rule of thumb is 1-2% of the property’s value annually.

- Management Fees: If letting the property, factor in management costs, typically 8-12% of monthly rental income.

Only by subtracting all these costs from your projected rent will you arrive at the true net yield. This rigorous approach is essential when you determine a property's investment potential and prevents being misled by optimistic forecasts.

Physical Verification and Long-Term Logistics

Never purchase a property sight unseen. A physical inspection is non-negotiable. If you cannot attend in person, hire a trusted local surveyor or building inspector. They are trained to identify issues you might miss, such as structural problems, damp, or ageing utilities that could lead to significant future costs.

A successful global property investment is built on meticulous verification. From checking the title deed with an independent lawyer to planning your tax-efficient exit strategy before you even buy, every step in this checklist is a layer of protection for your capital.

Finally, consider long-term management and your exit strategy from day one. A reliable property management company is crucial for handling tenant screening and rent collection. Simultaneously, have a clear plan for an eventual sale. Understanding local Capital Gains Tax (CGT) rules and market cycles will help you decide the optimal time to realise your profits.

Understanding long-term cycles is key. For example, analysis of the UK housing market has shown long periods where affordability improves due to supply increases, not just price falls. You can learn more about these long-term affordability cycles at Schroders.com.

Frequently Asked Questions About Global Property Investment

Here are clear, practical answers to some of the most common questions from investors considering overseas property.

What Are the Biggest Hidden Costs When Buying Property Overseas?

Beyond the purchase price, investors must budget for legal fees, property registration taxes (equivalent to UK Stamp Duty), and currency conversion charges.

Ongoing costs often catch investors out. These include annual property taxes, which vary by municipality, and property management fees, typically between 8% to 12% of rental income. To avoid surprises, obtain a detailed cost breakdown from a local solicitor before committing.

Is It Better to Invest in a City Centre Apartment or a Holiday Villa?

This depends on your investment goals and risk appetite. A city centre apartment generally offers consistent, year-round rental demand from professionals and long-term residents, providing a stable income stream.

Conversely, a holiday villa can generate high income during peak season but may sit empty for long periods, leading to inconsistent cash flow. Your decision should be guided by local market data on year-round occupancy rates and demand drivers.

How Do I Find a Reliable Estate Agent and Lawyer in Another Country?

Finding trustworthy local professionals is critical. Start by seeking recommendations on expatriate forums, through professional networks, or from other foreign investors. When selecting estate agents, check for membership in accredited national associations, which typically enforce a professional code of conduct.

The most important rule is to always instruct an independent lawyer with no connection to the seller, agent, or developer. Their sole duty is to protect your interests. Conduct due diligence: search online, check client reviews, and verify their credentials before instructing them.

This independent verification is your best defence against potential conflicts of interest and ensures a secure purchase.

At World Property Investor, we provide the in-depth guides and market analysis you need to make informed decisions. Explore our resources to compare markets, understand tax implications, and invest with confidence. Find your next opportunity at https://www.worldpropertyinvestor.com.