You’re probably looking at Thailand for one of two reasons. Either UK buy-to-let returns feel increasingly squeezed, or you want part of your portfolio in a market tied to tourism, lifestyle demand, and a different economic cycle from Britain.

That instinct isn’t wrong. Thailand can offer stronger gross rental yields in the right locations, and it remains one of the few markets where a foreign buyer can still find a relatively accessible entry point through condominiums. But buying property thailand isn’t a sun-and-sea shortcut to easy income. The rules are different from the UK, the paperwork matters more than many first-time overseas buyers expect, and a small mistake in ownership structure or fund transfer can create a large problem later.

UK investors usually underestimate three things. First, you can’t approach Thai property law as if it were just a warmer version of England and Wales. Second, the legal structure you choose affects resale, financing, tax handling, and inheritance planning from day one. Third, fund remittance is not a banking afterthought. It’s part of the ownership process.

If you want a broad market backdrop before you narrow down areas, review recent Thailand housing price trends. Then focus on the mechanics that protect your capital. That’s where good deals usually survive, or fail.

An Investor's Introduction to the Thai Property Market

Thailand attracts investors because it combines lifestyle demand with a broad range of property products. Bangkok offers urban apartments tied to business, education, and long-stay demand. Phuket offers resort-led rental potential. Other markets sit somewhere in between, often with lower entry costs and less institutional competition.

For a UK buyer, the appeal is usually practical rather than romantic. You’re looking for diversification, income, and a market that doesn’t move in lockstep with British housing. In selected Thai locations, gross yields can look stronger than what many UK landlords now expect from conventional buy-to-let. That matters, but only if the legal setup is sound and the cash can be repatriated cleanly later.

Thailand rewards investors who treat the purchase as a regulated cross-border transaction, not as a holiday impulse.

The key difference is ownership. In the UK, buyers assume freehold or leasehold are familiar concepts with established lending and transfer norms. In Thailand, foreign ownership is narrower, more document-driven, and highly dependent on asset type. Condos are one thing. Land is another entirely.

That’s why experienced buyers start with four filters:

- Asset type first: A condo, villa, or land-based project each creates a different legal path.

- Income model second: Long-stay tenant demand behaves differently from holiday lets.

- Exit route third: Resale to another foreign buyer isn’t always as straightforward as the brochure suggests.

- Currency discipline always: Your sterling return can look very different from your baht return.

If you get those filters right early, the market becomes much easier to read.

Navigating Foreign Ownership Laws in Thailand

The first question isn’t where to buy. It’s what you can legally control.

Thai property law gives foreign investors workable routes into the market, but they aren’t interchangeable. Each route changes your risk profile, your paperwork burden, and your resale flexibility. The most important thing to understand is that legal convenience and legal control are not always the same thing.

Hard rule: A foreign individual generally cannot directly own land in Thailand.

That single rule shapes almost every purchase strategy.

The three main routes

For most UK investors, the realistic options are condominium freehold, long leasehold, or a company structure. If you need a primer on the broader ownership concepts, this guide to freehold versus leasehold property investing is a useful companion before you compare Thailand-specific structures.

Here’s the practical comparison.

| Structure | Ownership Type | Best For | Key Consideration |

|---|---|---|---|

| Condominium | Direct ownership of a condo unit, subject to the foreign quota | Investors who want the simplest and clearest route | You must confirm the project still has room within the foreign ownership quota |

| Leasehold | Registered long-term right to use property | Villas, houses, or land-based lifestyle assets | Control can be strong, but it is not the same as freehold ownership |

| Thai company structure | Property held by a Thai entity | Genuine operating businesses with a real commercial purpose | High compliance burden and serious risk if used improperly |

Condominium ownership

For a foreign buyer, this is usually the cleanest route. Thai law allows foreigners to own condominium units, provided the building remains within the foreign ownership quota. This structure is popular because it gives direct title to the unit and is generally easier to understand, manage, and resell than more complex arrangements.

It also suits many UK investors because the asset is straightforward. You can model service charges, rental income, and management costs more easily than with a villa on leased land. If your priority is a defensible legal position rather than maximum lifestyle appeal, condos often win.

Leasehold for villas and houses

Leasehold is common where the attractive asset sits on land, especially villas and detached houses. In practice, buyers use it to secure long-term possession and use rights where freehold land ownership is unavailable.

The trade-off is simple. A well-drafted registered lease can provide practical control, but it is still a time-limited interest. Your solicitor’s drafting matters. Renewal language matters. Registration matters. The seller’s title and ability to grant the lease matter. Investors who treat leasehold casually often discover too late that “secure use” and “bankable asset” are not the same thing.

A lease can still work very well for lifestyle-backed investments, especially where rental performance and personal use matter more than pure resale simplicity.

Company structures

Some buyers are drawn to the idea of using a Thai company to hold land. This can be lawful in the right commercial context, but it is not a shortcut for private ownership. If the company exists only to mask foreign land ownership, you are in dangerous territory.

A legitimate structure requires proper corporate substance, governance, accounting, and tax compliance. That’s a business decision, not a casual property trick. For most private UK investors buying one apartment or one holiday home, a company route is usually more burden than benefit.

What works and what doesn’t

What works:

- Buying a condo with clear foreign quota availability

- Registering leasehold rights properly at the Land Office

- Using independent legal advice instead of relying on the developer’s documents

- Choosing structures that match the property’s real use

What doesn’t:

- Assuming verbal assurances are enough

- Treating nominee arrangements as normal market practice

- Buying first and asking legal questions later

- Confusing operational control with secure title

The legal structure is not admin. It is the investment.

Selecting the Right Thai Property Market

Location in Thailand is less about chasing the hottest map pin and more about matching the market to your intended tenant, hold period, and exit route.

At a national level, Thailand still shows measured price growth rather than runaway overheating. According to Bank of Thailand data from Q2 2025, the Nationwide Residential Property Price Index rose by 2.71% year-on-year, with the South up 5.48% and the North up 1.84% according to Bank of Thailand figures reported by Global Property Guide. For investors, that regional split matters. It tells you demand drivers are local, not uniform.

If you’re comparing destinations globally, a broader framework for where to buy investment property overseas helps put Thailand’s cities and resort markets in context.

Bangkok for liquidity and depth

Bangkok usually makes sense for buyers who want a deeper occupier market. Demand is driven by professionals, students, long-stay residents, and domestic movement, not just holiday traffic. That typically creates a more stable rental base than purely resort-led locations.

The downside is competition. Stock selection matters more. A mediocre unit in an oversupplied tower can underperform badly even if the district looks attractive on paper. In Bangkok, I’d focus more on micro-location, building management quality, and practical tenant appeal than on glossy amenities.

Phuket for income focus

Phuket is a different proposition. Investors usually buy there for lifestyle demand and stronger holiday or short-stay income potential. The market is more emotionally driven, but that doesn’t mean you should evaluate it emotionally.

The critical question is whether the property works outside peak visitor periods. Beach proximity helps, but so do access roads, management quality, and whether the building is specifically set up for lettings rather than owner-occupier marketing.

In resort markets, a weak management company can damage returns faster than a weak location.

Emerging markets and second-tier choices

Places such as Chiang Mai or Hua Hin can appeal to buyers who want lower pricing pressure and a different tenant mix. These markets may suit long-stay retirees, remote workers, or buyers planning future personal use.

That said, “emerging” shouldn’t be confused with “automatically better value”. Thinner resale pools can offset lower entry prices. If you buy in a smaller market, your exit may take longer and depend more on local demand than on international investor sentiment.

A practical way to choose

Use this filter before you shortlist property:

- For rental income: Prioritise areas with established tenant demand and competent local management.

- For capital preservation: Prefer markets with broader buyer pools and easier resale logic.

- For mixed personal use and income: Accept that convenience and enjoyment may reduce pure financial efficiency.

- For long-term diversification: Choose places whose demand drivers differ from your UK holdings.

The best Thai market is the one that fits your actual plan, not the one with the best drone footage.

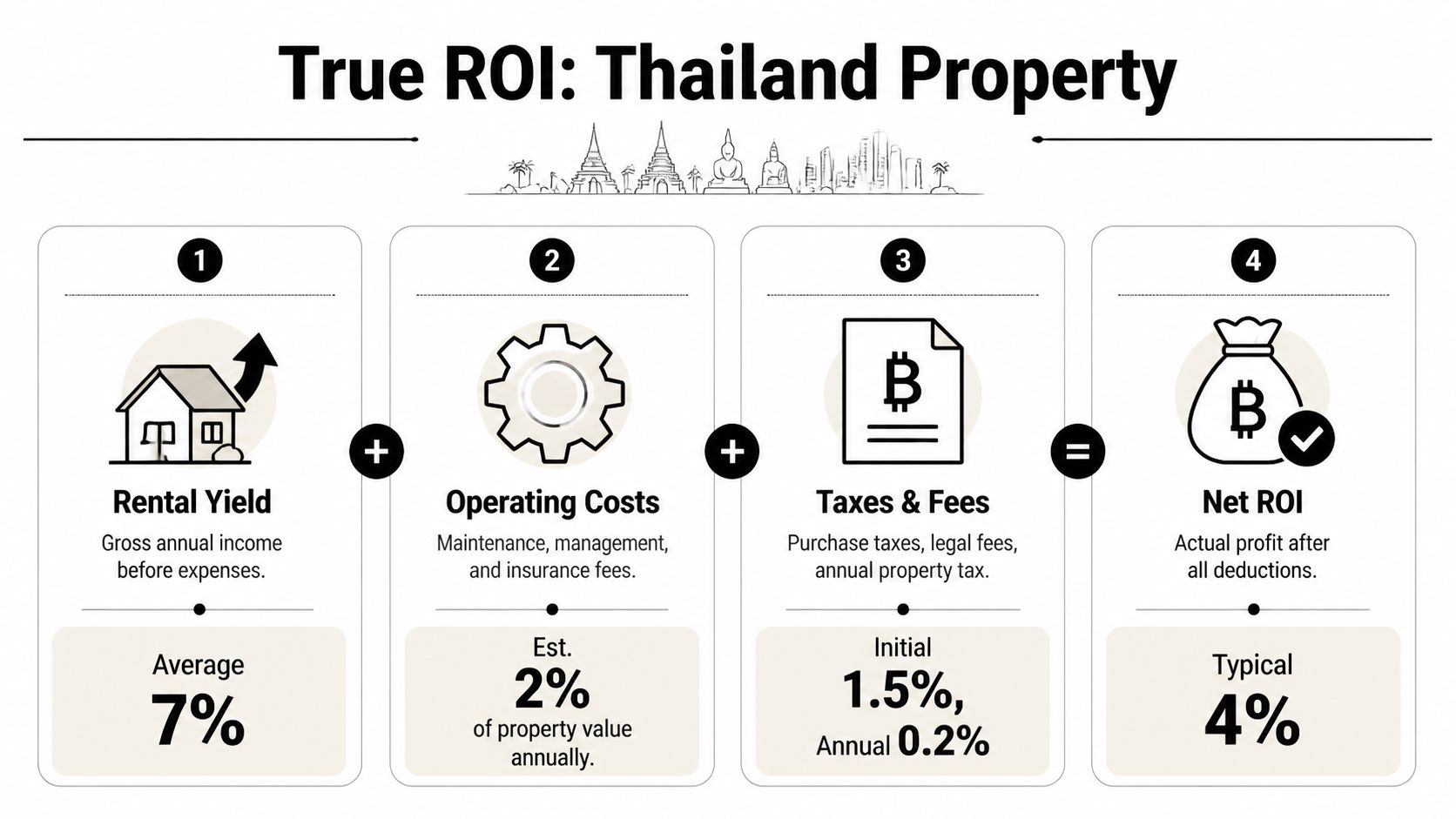

Calculating Your True Return on Investment

Headline yield is where many cross-border purchases go wrong. Gross income looks attractive. Then fees, tax treatment, vacancy, repairs, management friction, and currency movement pull the actual return back to earth.

The broad attraction is real. The UK’s buy-to-let market offers average yields around 4.5%, while prime Thai locations like Phuket can deliver gross rental yields between 6% and 8% according to this Thailand versus UK yield comparison. But that’s a gross comparison. It is useful for screening markets, not for making the buy decision.

A proper model needs to answer one question. After everything, what are you actually keeping?

Start with gross income, then strip it back

I’d break Thai property returns into four layers:

Advertised rental yield

This is the number developers and agents lead with. Treat it as the top line, not the result.Operating drag

Common area charges, repairs, furnishing refreshes, letting fees, and management costs all sit here.Transaction and tax friction

Purchase-related fees, resale taxes on exit, and tax treatment of rental income affect the actual economics.Currency effect

If your base wealth and future spending are in pounds, sterling matters. A decent baht return can still disappoint once translated back.

If you want to stress-test a holding period rather than just annual yield, an essential business payback tool can help estimate how long the asset takes to recover its upfront cost under different income assumptions.

Costs buyers often underweight

The purchase price is not the full entry cost. Investors regularly miss the practical drag created by smaller recurring items and by legal work they shouldn’t skip.

Watch for:

- Legal fees: Independent legal review isn’t optional if you’re foreign and buying remotely.

- Building charges: Condos with heavy facilities can look attractive but cost more to hold.

- Furnishing and replacement cycles: Holiday and short-stay stock wears faster.

- Vacancy assumptions: A unit can be rentable without being occupied consistently.

- Tax handling in both jurisdictions: Thai income treatment and UK reporting obligations need to be considered together.

Investor test: If the deal only works on the brochure yield, it probably doesn’t work.

Comparing Thailand with a UK buy-to-let

A key reason many British investors look at Thailand is not just yield uplift. It’s portfolio diversification. Thai demand drivers can be tied to tourism, regional migration, or long-stay international residents in ways that differ from a standard UK rental market.

That opportunity comes with different risks:

| Factor | Thailand | UK buy-to-let |

|---|---|---|

| Yield profile | Often stronger in selected resort and prime demand areas | Often lower but more familiar to local investors |

| Legal familiarity | Lower for UK investors | High |

| Currency exposure | Yes, if your capital base is sterling | Usually no for domestic investors |

| Management complexity | Higher if you’re overseas | Lower if local |

For a more detailed framework on modelling returns, this guide on how to calculate property investment ROI is worth keeping beside your spreadsheet.

What a good model looks like

A sound underwriting model doesn’t need heroic assumptions. It uses conservative rent, realistic downtime, proper management costs, legal expenses, and a holding-period view. It also assumes that selling takes effort and that repatriating funds requires documentation.

When those assumptions still produce a satisfactory return, you may have a durable investment. When the return disappears under realistic friction, you’ve probably just avoided an expensive lesson.

Executing Your Property Purchase Step by Step

At this stage, buyers either create a clean title path or leave themselves exposed. The purchase process in Thailand is manageable, but only if you treat each stage as evidence-building, not box-ticking.

UK demand is not marginal. Data from Thailand's Real Estate Information Center shows that in 2024, UK buyers accounted for approximately 12% of foreign condominium transfers in key tourist zones like Phuket, as summarised in this overview of foreign condo buying in Thailand. That makes process discipline even more important, because busy foreign-buyer markets also attract rushed decisions.

Build your team before you reserve anything

You need two local professionals at minimum: an agent who knows the area and an independent lawyer who acts only for you. Not the seller’s lawyer. Not the developer’s in-house contact. Yours.

A solid workflow checklist also helps. If you want a practical reference, BoloSign's transaction steps for real estate deals are useful for tracking the sequence of documents, approvals, and completion tasks.

The buying sequence that protects you

A disciplined purchase usually follows this order:

Choose the legal structure first

Don’t reserve a unit before you know whether the asset suits foreign condo ownership, leasehold, or another lawful setup.Run due diligence on the property

Your lawyer should verify title, seller authority, registered encumbrances, and, for a condo, whether foreign quota remains available.Review the sale terms in detail

Deposit conditions, completion deadlines, included fixtures, tax allocation, and default remedies all belong in writing.Plan the remittance route before sending funds

This matters more than many first-time buyers realise.Complete transfer at the Land Office

That’s where ownership or registered rights become formal.

The remittance rule that catches people out

For foreign condo ownership, proof that funds came from abroad in foreign currency is central. The Thai bank documentation supporting that remittance is part of the legal pathway to registration. If the money trail is wrong, the ownership registration can become difficult or impossible.

That means you should coordinate the bank transfer wording, the recipient details, and the purchase purpose before any money moves. Don’t improvise this after signing. And don’t assume a UK bank transfer reference that makes sense to you will satisfy what the Thai side needs to see.

Keep every bank record, remittance document, contract version, and receipt in one deal file from day one. You’ll want the same trail again when you sell and move funds back out.

What to check in the contract

Many problems are visible before completion if someone reads the paperwork properly.

Focus on:

- Seller identity: The contracting party must match the person or entity with legal authority to sell.

- Property description: Unit number, title details, and boundaries must align with official records.

- Fee allocation: Don’t leave transfer costs and taxes vague.

- Completion mechanics: Specify what happens if either party is late or documents are missing.

- Handover condition: Spell out what is included and what condition the property must be in.

A short explainer can also help if you want to visualise the process before completion:

Final completion

At the Land Office, the practical goal is simple. Documents match. Funds are ready. Registration happens cleanly. If you’ve prepared properly, completion is administrative. If you haven’t, small discrepancies can delay everything.

That’s why the purchase process should feel boring by the end. Boring is good. Boring means the legal work was done before transfer day.

Planning Your Long-Term Rental and Exit Strategy

A Thai purchase only becomes a successful investment when the management model and exit plan work as well as the acquisition.

Most UK owners need a local management arrangement. The main question is not whether to use one, but how much control to delegate. For a straightforward long-let condo, you may only need rent collection and maintenance oversight. For a holiday-led unit, you’ll need guest handling, cleaning coordination, key management, repairs, and tighter income reporting.

Rental strategy choices

Long-term rentals usually produce steadier occupancy and lower operational noise. Short-term rentals can produce higher gross income in the right building and area, but they also create more friction, more wear, and more compliance risk. Before buying, check what the building rules allow. Some projects are investor-friendly. Others are not.

If you want a practical landlord-focused view, Towne and Country's condo rental advice is a useful reminder that rental success depends as much on management and rules as on the unit itself.

Exit planning matters on day one

Your future buyer will care about the same things you should care about now. Clear title, clean remittance records, manageable running costs, and a property that appeals to a real pool of buyers.

For foreign owners, resale is only part of the exit. Repatriating funds matters too. Keep your original purchase documents, transfer evidence, and banking records organised from the start. If those records are incomplete, the later sale process becomes harder than it needs to be.

Tax also belongs in the exit discussion, not just the purchase discussion. If you want a broader framework for planning disposal costs, this guide to capital gains tax on foreign property is a good starting point before you take market-specific advice.

Buy the asset you’ll be able to sell, not just the asset you’d enjoy owning.

For most UK investors, the strongest long-term Thai deals are the boring ones. Good building management. Clear ownership structure. Reliable tenant appeal. Defensible paperwork. Those aren’t glamorous advantages, but they’re the ones that usually survive contact with reality.

If you’re comparing Thailand with other overseas markets, World Property Investor offers practical country guides, market analysis, and step-by-step buying advice to help you assess yields, risks, ownership rules, and long-term investment potential before you commit capital.