Yes. Foreigners can buy property in Spain, and the market is open to overseas buyers, including British nationals, with no significant ownership restrictions. In 2024, foreign buyers purchased nearly 93,000 homes in Spain, accounting for 14.6% of all property transactions, which tells you this is not an unusual route but a well-established part of the market.

If you're reading this from London, Manchester or Dubai with a shortlist open on your laptop and a Spanish estate agent chasing a reservation, the question usually isn't whether you can buy. It's whether you can buy safely, finance it sensibly, move funds cleanly, and avoid the expensive mistakes that happen after the glossy brochure stage.

Spain is accessible, but it isn't frictionless. The paperwork is formal. The legal process is document-heavy. And for UK buyers in particular, post-Brexit ownership has become less about permission and more about compliance, banking, tax filings and practical cross-border execution.

That distinction matters. Buying the asset is straightforward. Owning it well takes planning.

Answering the Big Question Can Foreigners Buy Property in Spain

The short answer remains yes. Spain allows foreigners to buy residential, commercial and land assets, and foreign buyers enjoy the same property rights as Spanish citizens under Spain's open regulatory framework. For many investors, that's the first hurdle cleared.

The second hurdle is knowing what "open" means in practice. It doesn't mean casual. It means the legal framework is available to you, provided you follow the formal steps correctly, document your funds properly and complete through the Spanish system rather than trying to improvise from abroad.

A typical buyer at this stage is comparing Spain with other jurisdictions where foreign ownership is restricted, approval-based or structured through leaseholds. Spain is much more straightforward by comparison, which is why it continues to attract international capital. If you're weighing Spain against other markets, it's useful to compare it with broader foreign ownership restrictions by country before you commit your capital.

What matters more than the yes

The headline answer is easy. The execution is where deals either stay orderly or become messy.

Three issues usually decide whether the purchase feels smooth or stressful:

- Documentation quality: Your identity documents, proof of funds, tax paperwork and translated financial records need to be consistent.

- Independent legal review: The lawyer acting for you must check title, charges, planning status and contract wording before you send meaningful money.

- Post-completion discipline: Taxes, registration and ownership administration don't take care of themselves after key handover.

Practical rule: In Spain, the buyer who prepares early usually buys better. The buyer who rushes to secure the "perfect" property often spends more time fixing preventable problems later.

For UK investors, that practical layer matters more than ever. You can buy. The smarter question is whether the structure of your purchase, funding and long-term ownership still makes sense once Spanish tax and banking reality are applied to it.

Understanding the Legal Requirements Your Spanish Property Checklist

A UK buyer agrees a price on Monday, wires a reservation deposit on Tuesday, and only then learns the NIE appointment is weeks away, the bank wants more source-of-funds evidence, and the seller's paperwork is incomplete. That is how straightforward Spanish purchases become expensive, slow, and unnecessarily tense.

Start with the NIE

The document that sits at the centre of a non-resident purchase is the NIE, or Número de Identidad de Extranjero. Spain's official guidance confirms that foreigners commonly need an NIE for tax and economic activities, including property-related transactions, through the Spanish government information on the NIE.

For UK investors, the practical point is simple. The NIE is an identification and tax number. It is not residency status, it is not a visa, and it does not solve your banking or mortgage position. It does, however, appear throughout the purchase: contracts, tax filings, utilities, and registration.

Leave it late and the whole timetable tightens. Sellers rarely want to wait while a buyer scrambles for an appointment.

The documents that control risk

Once the NIE is in motion, attention should shift to the paperwork that protects capital and keeps the purchase executable. First-time overseas buyers often misread the deal at this stage. The contract can look fine, the property can photograph well, and the seller can sound cooperative. None of that replaces a clean file.

A prudent checklist includes:

- Nota Simple: the Land Registry extract showing ownership, charges, and a first view of the legal status of the property.

- Escritura de Compraventa: the sale deed that will be signed before the notary on completion.

- Proof of funds pack: bank statements, source-of-funds records, and supporting evidence for anti-money laundering checks. Post-Brexit, UK buyers should expect closer scrutiny where funds move across multiple accounts, currencies, or entities.

- Property compliance file: planning permissions, first occupancy or habitation documentation where relevant, and community information if the asset sits within a building or development.

- Identity and authority checks: if the seller is a company, confirm the legal entity, its directors or attorneys, and whether they have proper signing authority.

- Reservation terms: before paying a holding deposit, review the wording carefully. Tools such as PDF AI's real estate offer tool can help you spot clauses that merit lawyer review before funds are committed.

Missing paperwork does not always kill a deal. It changes the risk pricing. Sometimes the right answer is to renegotiate. Sometimes it is to walk away.

Who should handle what

Spanish transactions work well when each adviser stays in their lane.

- Estate agent: sources the property, relays offers, and helps keep momentum. Useful commercially. Limited legal protection.

- Independent lawyer: checks title, debts, planning position, community liabilities, tax exposure, and contract wording. This is the adviser protecting your downside.

- Notary: oversees the formal signing of the public deed and verifies the legal act. The notary does not replace buyer-side due diligence.

For non-resident buyers, I would also separate "Spanish-speaking" from "cross-border capable." Those are not the same thing. A lawyer may know local conveyancing well and still be weak on UK source-of-funds evidence, powers of attorney, non-resident tax setup, or buying through a foreign company. If you are selecting counsel from scratch, use an international real estate lawyer guide and look for someone who regularly handles non-resident transactions from instruction to post-completion tax registration.

The safer deal is usually the one where your lawyer is methodical, sceptical, and comfortable slowing the process when documents do not align.

Bank account, finance, and post-Brexit friction

A Spanish bank account is not the legal gateway to ownership, but in practice it often becomes part of the operating setup. Taxes, utilities, community charges, insurance premiums, and direct debits are easier to run through a local account.

The friction point for UK buyers is that opening the account, proving source of funds, and arranging finance can each run on different timetables. Spanish lenders may ask for translated income documents, UK tax returns, asset statements, and a wider financial profile than buyers expect. Buyers planning to complete from UK funds without a Spanish mortgage still need a clean audit trail for the money arriving in Spain.

That is the part many guides gloss over. You are not just buying an asset. You are building a non-resident ownership structure that has to keep working after completion, with the right identification, payment rails, tax administration, and legal records in place.

From Offer to Ownership The Spanish Property Buying Process

You find the right apartment in Madrid on Friday. By Monday, the agent wants a reservation deposit, the seller wants speed, and your funds are still sitting in the UK waiting for compliance checks. That is how Spanish purchases become expensive for overseas buyers. The risk rarely starts at completion. It starts when money moves before the legal position is clear.

A well-run transaction follows a clear order. Property selected. Terms agreed in principle. Reservation reviewed properly. Due diligence completed. Private contract negotiated. Finance aligned. Completion before the notary. Registration and post-completion administration handled without delay.

Offer stage and reservation deposit

Start with the asset, but do not let the asset control the timetable. View in person where possible, test whether the asking price reflects condition and location, and check whether any furnishings, parking, storage, or rental licence are included. Small ambiguities at offer stage often turn into larger disputes once a deposit has been paid.

The reservation document deserves line-by-line review. It should state the amount paid, when it becomes non-refundable, what happens if legal defects appear, and how long the property is held off the market. If the wording is vague, the seller usually benefits. If you want an early sense-check before your lawyer marks it up, PDF AI's real estate offer tool can help identify clauses that need legal attention before funds are sent.

For UK buyers, timing matters as much as wording. A seller may expect a reservation within days, while a Spanish bank, currency provider, or compliance team may still be reviewing source-of-funds documents. That mismatch is one of the common post-Brexit friction points. I advise clients to prepare identity, banking, and proof-of-funds paperwork before they make an offer, not after acceptance.

Due diligence and the private contract

The private purchase contract is where the deal becomes real. It is also where a disciplined buyer finds out whether the property is worth owning on the proposed terms.

Your lawyer should verify the seller's title, check for charges and embargoes, confirm cadastral and Land Registry details match, review planning position, and identify any community fee arrears or building disputes. Holiday-let investors should also confirm whether the property can legally be used as intended, because projected income is irrelevant if the licensing position is weak or restricted.

New-build and off-plan purchases need a stricter review of the developer, the build status, bank guarantees where applicable, specifications, delivery dates, and the paperwork required for lawful occupation. Sales material is not protection. Signed contract terms and supporting documents are.

A broader guide to buying property overseas is useful at this stage because the core principle is the same in every market. Commit to the legal facts first, then commit to the property.

The safest Spanish transaction is usually the one that feels slower than the agent wants.

To see the process visually, this walkthrough is a useful primer before you go to contract:

Finance, completion, and what happens after the signing

If a mortgage is involved, the loan timetable must match the contract deadlines. Non-resident underwriting can take longer than buyers expect, especially where income is earned in the UK through multiple entities, dividends, or international structures. Do not assume the bank will accommodate an aggressive completion date just because the seller wants one.

Completion takes place before a notary, who authenticates the public deed and checks identity, capacity, and formal execution. The notary is not your investigator and does not replace your lawyer. Buyers who rely on the notary to spot title, planning, or community problems are relying on the wrong safeguard.

Signing the deed is not the end of the process. The deed must then be filed and registered, taxes must be settled within the relevant deadline, utilities and local records need to be transferred, and the ownership file has to be set up so ongoing non-resident compliance does not start badly. For UK owners, that includes keeping clean records of purchase funds, costs, and ownership documents from day one, because those papers often matter later for tax reporting, refinancing, or sale.

What a disciplined buyer does differently

Strong buyers do a few things early. They get the offer structure right, insist on a reviewable reservation form, line up banking and currency transfers in parallel with legal work, and keep enough liquidity outside the purchase price to absorb delays and post-completion costs.

Weak process usually looks the same every time. Deposit paid too early. Lawyer instructed too late. Mortgage assumed rather than approved. UK funds moved at the last minute. Completion date agreed before the paperwork is ready.

Spain allows foreign ownership with relatively few barriers. The process still rewards preparation and punishes haste.

The Financials Taxes Purchase Costs and Mortgage Options

A UK buyer agrees a price in euros, assumes the balance is the hard part, then discovers the actual pressure sits in the layers around it. Tax, lender conditions, bank compliance checks, currency timing, and post-completion cash needs usually cause more friction than the headline price.

That is why serious buyers build the capital stack before they commit. Spain is accessible to foreign owners. Funding it cleanly, and holding it efficiently after completion, takes more planning than many first-time overseas purchasers expect.

Purchase costs beyond the agreed price

The total acquisition cost depends on three practical variables. Are you buying a resale or a new-build, which autonomous community is the property in, and are you borrowing against it. Those points change the tax treatment and some of the transaction costs.

I advise clients to budget by category first, then refine the numbers once the asset and region are fixed.

| Cost Item | Estimated Percentage / Cost | Notes |

|---|---|---|

| Purchase price | Varies by asset | The agreed acquisition amount |

| Transfer taxes or indirect taxes | Varies | Depends on whether the property is resale or new-build |

| Notary fees | Varies | Payable for formal deed execution |

| Land Registry fees | Varies | Required to register ownership properly |

| Legal fees | Varies | Usually charged for due diligence, contract review and completion support |

| Banking and transfer costs | Varies | Especially relevant for cross-border payments from the UK |

| Mortgage-related costs | Varies | Applies where lender due diligence and loan formalities are involved |

| Post-completion setup costs | Varies | Utilities, direct debits and ownership administration |

The mistake I see most often is simple. Buyers reserve enough cash for the deposit and completion balance, but not enough for tax, lender fees, account funding, insurance, and the first few months of ownership.

For UK investors after Brexit, the friction is often cross-border rather than legal. A delayed transfer from the UK, an unresolved source-of-funds query, or a poorly timed currency conversion can put pressure on the completion timetable and expose the buyer to exchange-rate movement at exactly the wrong moment.

Mortgage reality for non-residents

Spanish banks do lend to foreign buyers, but non-resident underwriting is stricter and the loan-to-value is usually lower than a resident borrower might obtain. In practice, that means a larger equity contribution, more supporting documents, and closer scrutiny of income, assets, liabilities, and the origin of purchase funds. Banco de España's consumer guidance on mortgage lending and APR disclosures is a better starting point than recycled agency summaries if you want to understand how Spanish lenders frame the loan product and borrower risk.

A prudent buyer tests three funding routes before making an offer:

- All-cash purchase: Operationally clean if the funds are already documented and easy to transfer.

- Spanish mortgage: Often the best match for the asset, but banks will want a full file and time to review it.

- UK-based borrowing against other assets: Sometimes attractive on price or flexibility, though execution can still be awkward when the property, notary, taxes, and ongoing payments all sit in Spain.

Bank choice matters more than many buyers expect. You need an account that can cope with completion funds, direct debits, non-resident administration, and day-to-day ownership payments. If you are trying to find the right Spanish bank, compare account requirements early, before legal work and mortgage paperwork start to overlap.

Mortgage pricing also needs context. A slightly cheaper rate is not automatically the better outcome if the lender is slower, more document-heavy, or less workable for a non-resident borrower. Review current mortgage rates in Spain for foreign buyers alongside arrangement fees, valuation costs, account conditions, and early repayment terms.

The ongoing costs many guides gloss over

Completion is only the beginning of the financial commitment.

Non-resident owners may face annual Spanish tax filing obligations even if the property produces no rental income. If it is rented, the tax treatment changes again, and the reporting standard becomes more demanding. Add local property tax, community fees, insurance, maintenance, utilities, bank charges, and occasional compliance costs, and the holding cost can look very different from the brochure version.

Post-Brexit ownership has become more technical for UK clients. You are not just buying an apartment or villa. You are adding an asset that sits inside another tax system, in another currency, with another banking framework. The right question is not only "Can I afford to buy it?" but "Can I fund it, report it, and hold it properly for the next five to ten years?"

Buyers who answer that question early usually make better purchases. They also avoid the common mistake of stretching for the property and underestimating the cost of owning it well.

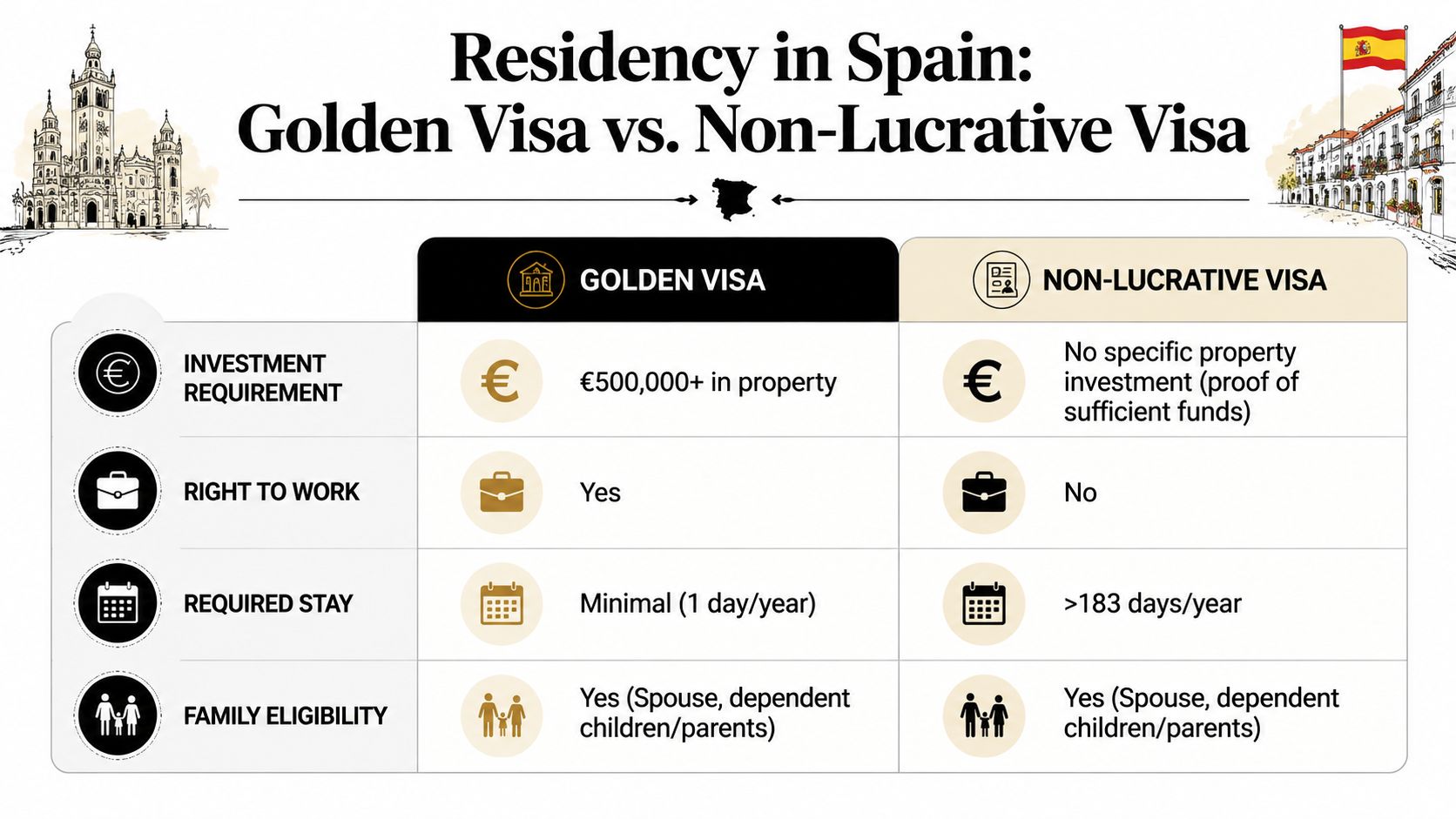

The Golden Visa and Other Residency Pathways

Many buyers still assume property ownership and residency come as a package. They don't.

That misunderstanding causes poor decisions. Some investors buy a Spanish property believing it will also solve their right-to-live question, only to discover later that ownership and immigration status are separate matters. For UK buyers after Brexit, this distinction is especially important.

Property ownership is not residency

A standard property purchase gives you the asset. It does not automatically grant the right to live in Spain on a long-term basis.

That isn't a technicality. It's one of the most important practical distinctions in the whole process. You can own the apartment, villa or commercial unit outright and still need a separate immigration pathway if your goal is relocation rather than occasional use.

As noted in Agave Abogados' guidance on legal considerations for foreign buyers, purchases must be formalised before a notary, the deed must be registered, taxes must be paid promptly after completion, and ownership remains separate from immigration status.

Golden Visa versus other routes

The investor conversation usually focuses on the Golden Visa because it ties residence rights to a qualifying property investment. A standard purchase below that threshold is purely a purchase. It does not create immigration rights by itself.

The comparison that matters is not "buy or don't buy". It is this:

- Asset-first buyer: Wants a holiday home, rental asset or diversification vehicle. Residency may be irrelevant.

- Relocation buyer: Needs a legal basis to spend substantial time in Spain.

- Flexibility buyer: Wants optionality for family use, travel and future residence planning.

If your objective is migration planning rather than pure property exposure, review investor residency alternatives before assuming one property transaction solves everything.

You can also compare the broader range of EU Golden Visa programmes if you're deciding between Spain and other residency-linked markets.

Buying property is an ownership decision. Residency is an immigration decision. Sometimes they align. Often they don't.

A practical way to decide

If the property still works for you without any residency benefit, the deal may be worth pursuing on investment fundamentals alone. If residency is the main reason you're considering Spain, start with immigration structuring before you choose the asset.

That order prevents the common error of buying the wrong property for the wrong reason.

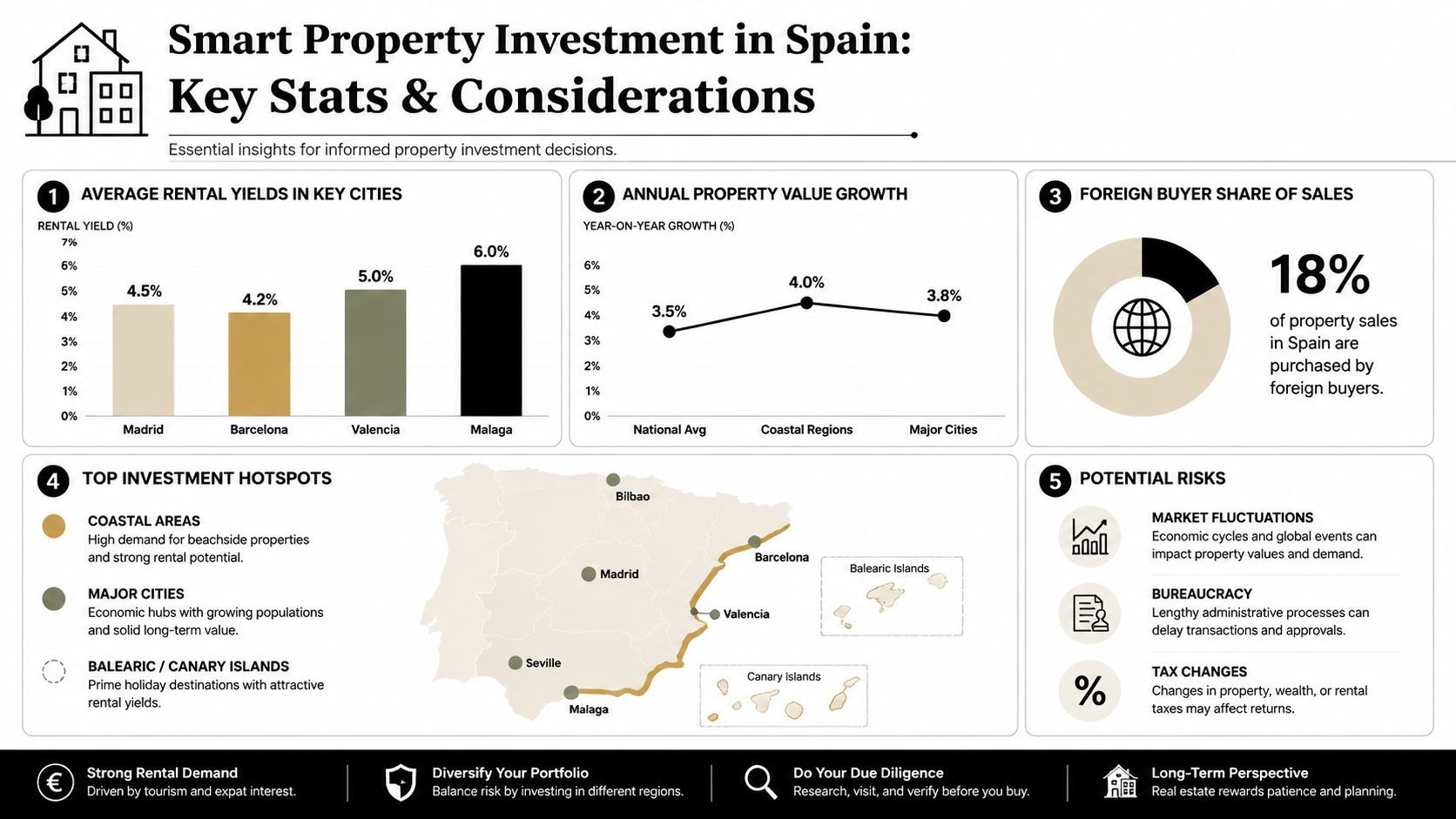

Smart Investing in Spain Markets Yields and Risks

A UK buyer who has cleared the legal work and lined up funds still faces the harder question. Which Spanish market is worth owning once non-resident tax, management friction, and resale risk are priced in?

Foreign demand is concentrated, not evenly spread. Idealista's report on where foreigners want to buy in Spain shows how heavily overseas buyers cluster in specific coastal provinces, with British purchasers still a major part of that flow. That matters because concentrated demand can support liquidity, but it can also push buyers into crowded submarkets where headline appeal hides weaker net returns.

Established markets versus emerging ones

For most high-net-worth clients, I frame the choice in practical terms. Buy in a market with proven depth, or accept more uncertainty in exchange for a lower entry price.

Established locations usually give you better resale prospects, more reliable year-round demand, stronger local professional support, and a wider buyer pool when you exit. The cost is obvious. You pay closer to full value, and it is harder to find a mispriced asset.

Less established areas can look compelling on a spreadsheet. The risk sits underneath the spreadsheet. Thin rental demand, inconsistent planning history, weak property management, or a buyer pool dominated by one foreign nationality can all hurt performance when conditions soften.

British demand has long favoured parts of Alicante, Murcia, and other coastal markets. That can be helpful if you want an asset another UK buyer will also understand and buy. It can also create concentration risk if your exit depends on a narrow overseas audience rather than broad domestic and international demand.

What a prudent investor checks

The strongest Spanish investments tend to be ordinary in the right way. Good location, clear legal status, easy use, sensible running costs, and a broad resale audience beat a flashy property with a narrow market.

I focus on five points:

- Depth of occupier demand: Holiday demand is useful, but year-round demand is safer.

- Exit liquidity: A property should appeal to local buyers, not just one foreign segment.

- Regulatory exposure: Short-let rules, licensing limits, and community restrictions can reduce income quickly.

- Asset usability: Homes with awkward layouts, unusual design, or excessive maintenance often underperform on resale.

- Management burden: Distance ownership only works if the asset is easy to run from abroad.

A property can rent well in August and still disappoint as an investment over five years.

That is where many first-time overseas buyers get caught. They underwrite the purchase on peak-season occupancy, then discover the investment case depends on off-season demand, compliance, and how easy the property is to sell in a slower market.

The overlooked ownership costs and risks

The ongoing costs are where post-Brexit friction becomes real for UK owners. The purchase completes, then the annual obligations begin.

Non-residents may have to file Spanish income tax returns even if the property is only for personal use. Spain's tax agency explains that non-resident owners can be taxed on imputed income from urban property that is not their main residence, under the Agencia Tributaria guidance on non-resident income from real estate. The tax charge is often modest relative to the asset value. The main issue is compliance. Missed filings, poor record-keeping, or assuming your gestor is handling everything without verification can create penalties and unnecessary stress.

For UK buyers, financing can also distort returns more than many guides admit. A euro mortgage may reduce currency mismatch if the asset and rental income are in euros, but non-resident lending is usually more document-heavy and less flexible than domestic borrowing. If you fund from sterling and own euro costs, exchange rate swings affect both acquisition and annual running costs.

Post-completion pressure points usually include:

- Annual non-resident tax filings: These continue whether or not the property is rented.

- Community fees: Prime urbanisations and apartment blocks can carry meaningful fixed costs.

- Local taxes and service charges: IBI, rubbish collection, insurance, and maintenance add up quickly.

- Letting restrictions: Income assumptions fail fast if the building or region limits short-term rentals.

- Cross-border banking administration: Direct debits, account monitoring, and payment timing matter more when you are absent.

A buyer who treats Spain as a simple lifestyle purchase often underestimates these items. A buyer who treats it as an operating asset makes better decisions from the start.

A market view worth holding

Spain offers genuine choice. You can buy for personal use, rental income, long-term diversification, or a mix of all three. The right market depends on which of those goals comes first.

If capital preservation and resale flexibility matter most, proven city districts and established coastal markets usually justify the higher entry price. If yield is the priority, test the assumptions hard. Gross rental projections mean very little until tax, vacancy, management, financing, and local restrictions are stripped out.

The right question is not whether foreigners can buy property in Spain. It is whether this specific asset still works once the annual tax filings, euro funding decisions, ownership costs, and likely exit route are all examined without optimism.

Your Final Checklist Before Buying Property in Spain

A typical mistake looks like this. A UK buyer agrees a price on Friday, books flights for signing, then discovers on Monday that the bank wants more proof of income, the lawyer has raised a registry issue, and the expected completion date is no longer realistic.

That is how avoidable costs start.

The final review before exchange and completion should be strict. By this stage, the question is no longer whether foreigners can buy property in Spain. It is whether this specific purchase still works once legal checks, euro funding, non-resident ownership costs, and post-Brexit admin are tested properly.

The pre-completion checks that matter

- Get the NIE early: Leave this too late and the rest of the transaction can slow down around it.

- Use an independent lawyer: The seller's representatives are there to close the deal. Your lawyer is there to check title, documents, permissions, debts, and contractual risk.

- Confirm what you are buying: Registry details, cadastral position, boundaries, licences, charges, and occupation status should match the commercial story being presented.

- Pressure-test the funding route: UK-source funds, anti-money-laundering checks, lender conditions, and currency timing often create more delay than the property itself.

- Hold extra liquidity: Purchase tax, notary, registry, legal fees, bank fees, and setup costs need to be covered without relying on perfect timing.

- Prepare for day-two ownership: Utilities, insurance, community payments, local taxes, and non-resident tax filings begin immediately. They do not wait until the property starts earning income.

New-build purchases need even more discipline. Before signing, confirm the developer exists in good standing, the signatory has authority to bind the company, the building permissions are in order, and the property can lawfully be occupied on completion. If any of that is unclear, pause the deal and get the point resolved in writing.

I tell clients to make one final pass through the file as if they were buying an operating asset, not a holiday home. Can the money arrive on time. Are the documents complete. Have the ongoing annual costs been priced accurately. Is there a realistic plan if the property is vacant, the mortgage offer changes, or the local letting rules tighten.

That discipline matters most for overseas buyers. Distance makes small administrative problems expensive.

Buy when the title is clean, the funding is ready, the tax position is understood, and the ownership plan holds up under pressure.

The Spanish market is accessible to foreign buyers. Good outcomes depend on buying with enough margin for legal checks, banking delays, and the actual carrying cost of owning from abroad.

If you're comparing Spain with other international markets, researching taxes, yields and foreign-buyer rules, World Property Investor offers data-driven guides to help you assess where a property purchase fits your wider portfolio strategy.