The most popular advice about citizenship in germany is also the most misleading. Many investors assume that if they buy a flat in Berlin, a commercial unit in Frankfurt, or a retirement property near Munich, citizenship will eventually follow. It won't.

Germany is attractive for global investors because it combines legal stability, a deep economy, and a property market that often suits long-horizon capital. But German nationality law doesn't reward passive ownership in the way some residency-by-investment schemes do elsewhere. It rewards residence, integration, documentation, and patience.

That distinction matters more now because the system is active, not dormant. Germany's citizenship system hit a modern high in 2023, when the Federal Statistical Office reported 200,095 naturalisations, the highest total since records began in 2000, according to the European Commission's note on record naturalisations in Germany. That same update notes that access to nationality has become more open than it was under the older model.

For investors, that creates both opportunity and confusion. Germany is more accessible than it used to be, but it still isn't selling passports. If your objective is long-term European mobility, family security, and a second base backed by substance rather than marketing, Germany deserves attention. If your objective is a fast citizenship shortcut through real estate alone, you're looking at the wrong country.

Investors comparing mobility options across Europe often start with broad lifestyle questions before they narrow into law and tax. A useful first filter is to review the best EU countries to live in and then test whether Germany fits your priorities on residence, family planning, and long-term asset positioning.

Introduction Germany's Growing Appeal for Global Investors

Germany appeals to investors for sensible reasons. It offers institutional depth, mature banking, strong tenant demand in major cities, and a legal environment that generally rewards careful planning rather than speculation. That profile suits buyers who think in decades, not in exit cycles.

But the primary attraction for many international families isn't only property. It's optionality. A home, a base, access to Europe, and in time, a route to nationality for the family unit. That's where many otherwise discerning buyers make a basic error. They treat Germany as if it operates a property-led immigration model. It doesn't.

Why investors keep getting this wrong

Much of the online content around German nationality focuses on ancestry claims, restitution, or highly specific historical categories. Those routes matter for eligible families, but they don't answer the question most property buyers ask: can I buy my way into Germany and turn that into a passport?

The practical answer is no.

Germany can absolutely form part of a serious residency and citizenship strategy. What works is combining a lawful residence basis with a genuine life on the ground. What doesn't work is assuming that title deeds replace residence history, language ability, or financial compliance.

Practical rule: In Germany, property can strengthen a broader immigration file. It cannot substitute for the immigration file.

What a realistic investor strategy looks like

A strong German plan usually starts with three linked decisions:

- Choose the immigration route first: Employment, self-employment, or family connection comes before property.

- Buy property for strategic reasons: Accommodation, long-term wealth preservation, and local ties are useful. A passport shortcut isn't.

- Treat citizenship as a medium-term objective: Germany rewards consistency. Buyers who plan accordingly tend to make better decisions on tax residence, financing, and family relocation.

That's the lens worth using throughout this guide.

Understanding German Citizenship The Integration Principle

Germany does not offer a golden visa or a citizenship-by-investment programme tied to property acquisition. That's the core point investors need to grasp before they spend money, sign contracts, or build a cross-border plan around the wrong assumptions.

The ordinary route is based on integration. That means lawful residence, a real life in Germany, language ability, and financial independence. The European Commission's December 2025 update states that Germany's standard naturalisation path was shortened to 5 years and continues to require language skills and financial independence, confirming that buying real estate does not create a shortcut, as outlined in the European Commission note on changes to citizenship requirements in Germany.

Property ownership helps differently

Property still matters. It just matters in a narrower and more realistic way.

A well-chosen German property can support your overall profile because it may show stable accommodation, long-term commitment, and financial substance. If you're applying through self-employment or another residence category, that broader picture can help. But immigration authorities are looking at your legal basis to live in Germany, not at the mere fact that you own an asset there.

Think of it this way. In some countries, capital is the main test. In Germany, integration is the test, and capital is only relevant when it supports that integration.

Germany versus transactional programmes

For a high-net-worth client, this is often a strategy issue rather than a legal one. If you want a jurisdiction where funds can replace physical presence, Germany will feel restrictive. If you want a jurisdiction where citizenship reflects an established personal and economic connection, Germany is coherent.

That makes Germany different from the programmes investors often compare it with.

| Model | What drives the route | Role of property |

|---|---|---|

| Germany | Residence, integration, language, financial independence | Supportive at best |

| Transactional investment model | Capital deployment into an approved route | Often central |

| Descent or restitution route | Family history and documentary proof | Usually irrelevant |

The misconception that causes poor decisions

An investor buys first, assumes the immigration part will be easy later, and then discovers that residence status is the main hurdle.

The better sequence is the reverse:

- Confirm your residence route

- Model your family's physical presence

- Plan language and compliance early

- Only then buy property that fits that plan

Buying a property in Germany can be commercially sound and personally useful. It still doesn't answer the citizenship question on its own.

This is why investors should view German real estate as a supporting asset within a residency strategy, not as the strategy itself.

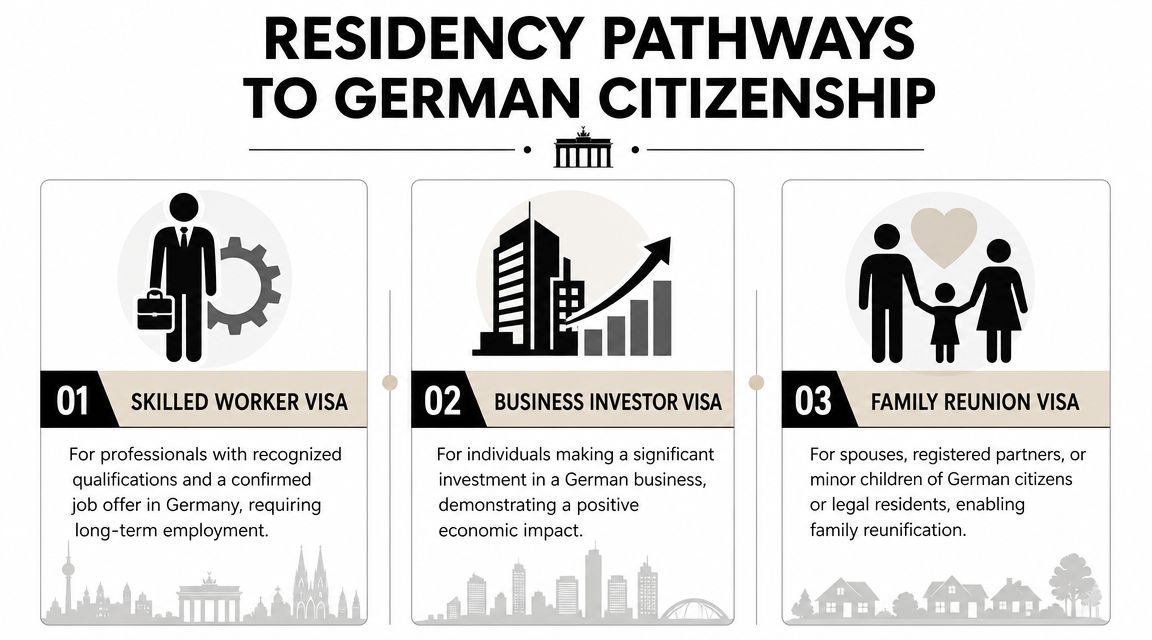

Your Foundation Key Residency Pathways to Citizenship

The route to citizenship starts with lawful residence. Germany's current framework anchors naturalisation to a five-year lawful residence threshold, replacing the old eight-year standard, and that makes a valid residence permit the foundation of any serious plan, as explained in the official-style guidance on Germany's five-year residence threshold for naturalisation.

If you're assessing cross-border mobility routes more broadly, it helps to compare Germany with other visa options for investors before deciding whether Germany's residence-led model matches your goals.

Self-employment and investor residence

This is the route many entrepreneurs naturally explore first. It can suit business owners, consultants, principals relocating part of an operating business, or investors building a genuine commercial activity in Germany.

The key point is that Germany is generally interested in the substance of the activity. Authorities will usually want to see that the proposed business has an economic rationale, a coherent plan, and a lawful basis for supporting the applicant's life in Germany. A property purchase alone won't do that. A business linked to asset management, development, serviced accommodation compliance, or an operating company may be more persuasive if it is real, documented, and locally grounded.

For property investors, this route works best when the property forms part of a wider enterprise. For example:

- Portfolio management activity: You relocate to Germany and actively manage a legitimate business structure tied to your holdings.

- Development or refurbishment business: The value lies in the operating business, not just in owning units.

- Advisory or operating company: Property may support the balance sheet or local presence, but the residence case rests on business activity.

What doesn't work is buying one or two properties and calling yourself an investor without demonstrating a credible self-employed role in Germany.

EU Blue Card and skilled employment

This route often gets overlooked by wealthy clients because they assume employment is irrelevant to them. That's a mistake. A senior role in your own group, or a genuine executive hire by a German company, can be one of the cleanest ways to build residence history.

For applicants with recognised qualifications and a real employment relationship, the Blue Card or another work-based permit can provide clarity. From a citizenship perspective, that clarity matters. Salary, tax records, social integration, and continuous residence are easier to evidence when the underlying status is straightforward.

Property fits here in a supporting role. Buying a home can strengthen practical settlement, but it doesn't create the permit. The job does.

Family reunification

Family-based residence is often the most overlooked route in investor planning because advisers focus too narrowly on capital. If a spouse, registered partner, or child has the relevant status in Germany, family reunification may be the right basis.

This route can be especially effective for internationally mobile families who stagger relocation. One spouse may enter through work or business, while the other secures accommodation, schooling, and household logistics. In that context, property can be useful because it stabilises the family's centre of life in Germany.

A strong family file often looks more convincing when residence, schooling, registration, and housing all point in the same direction.

Choosing the right route as an investor

The best route depends less on wealth and more on credibility. German authorities usually respond better to a coherent story than to a flashy balance sheet.

A practical comparison helps:

| Pathway | Best suited to | Where property helps | Main weakness |

|---|---|---|---|

| Self-employment | Entrepreneurs and active operators | Shows local commitment and may support business activity | Weak if the business is superficial |

| Employment or Blue Card | Executives and skilled professionals | Useful as stable housing | Doesn't suit buyers with no real employment basis |

| Family reunification | International families with an existing German connection | Reinforces settled family life | Depends on another family member's status |

Residence continuity matters more than many buyers expect

Once you have the right permit, the next challenge is staying consistent. Germany's system is not designed around occasional visits. If your real life remains elsewhere and Germany is only a property destination, the route weakens.

That affects practical decisions such as:

- Where you spend most of your time

- How your tax and financial records line up

- Whether your registration and daily life are credible

- Whether absences interrupt the story your documents tell

Investors who do well in Germany usually treat residence as an operational commitment. They organise the family, the paperwork, the language learning, and the property ownership around that commitment.

The Naturalisation Process Timelines and Dual Citizenship

Once lawful residence is in place, the naturalisation phase becomes a compliance exercise. The legal change that matters most for investors is not only timing. It's flexibility on nationality.

Germany's expanded tolerance of dual nationality from June 2024 materially improves the case for applying because people can typically keep their existing passport, as noted in SE Legal's overview of German citizenship by descent and reform-related implications. For British, American, Australian, and other internationally mobile families, that removes one of the biggest historic objections to citizenship in germany.

What the standard file usually needs

In practice, a strong naturalisation file usually rests on a handful of recurring elements:

- Lawful and habitual residence: Your permit history and registration record need to align.

- German language ability: B1 level is the key legal threshold mentioned in the verified materials.

- Financial self-sufficiency: Applicants need to show they can support themselves.

- Integration evidence: This typically includes the naturalisation test and a clean documentary trail.

For investors, the main challenge is not usually wealth. It is coherence. Authorities want to see that the applicant lives in Germany and can prove it across multiple records.

Language planning is where delays start

Many applicants underestimate the language side because B1 sounds manageable on paper. In reality, adults running businesses, managing portfolios, or moving with family responsibilities often postpone structured study until late in the process.

That's avoidable. If you want a sense of what sustained study looks like beyond the minimum threshold, this breakdown of study hours for German B2 is a useful planning reference. Even if your legal target is lower, the article helps applicants budget time realistically rather than treating language as a last-minute task.

Clients who start language training early tend to make better residence decisions, because language forces regular contact with local systems, paperwork, and daily life.

Why dual citizenship changes the equation

Historically, many high-net-worth applicants hesitated because naturalisation could force a painful trade-off. Keep the original passport or gain the German one. That dilemma made Germany less attractive than it otherwise should have been for internationally structured families.

That calculation has changed. Being able to keep an existing nationality often makes the process commercially and personally worthwhile. It supports family continuity, preserves legacy arrangements, and avoids unnecessary disruption across banking, inheritance planning, and international travel patterns.

A lot of investors still compare Germany to classic citizenship by investment options. That comparison is understandable, but it misses the point. Germany now offers something different: not speed, but a stronger long-term value proposition for people willing to establish a genuine base.

A short explainer can help if you want a visual summary before speaking to counsel:

The investor's practical takeaway

Don't think of naturalisation as a final legal formality. Think of it as the point where every earlier decision gets audited at once.

If your permit basis was sound, your residence real, your finances transparent, and your language preparation started early, the process is manageable. If any one of those pieces was treated casually, the weaknesses usually show up at this stage.

How Property Investment Supports Your Citizenship Goal

Property supports a citizenship plan in Germany best when it serves the life you're building there. It is useful as infrastructure. It is weak as symbolism.

That distinction matters because many buyers overestimate what ownership proves. A notarised purchase shows commitment to an asset. It doesn't automatically show commitment to Germany as your place of residence. To help your broader file, the property must fit the rest of your facts.

What property can do well

A German property can strengthen your position in several practical ways:

- Stable accommodation: Owning your home makes your residential position easier to evidence than relying on temporary rentals or hotel stays.

- Local economic ties: It supports the argument that Germany is more than a convenience address.

- Income structure: In the right circumstances, rental income may form part of the financial picture behind self-sufficiency or a business plan.

- Family settlement: A fixed base supports school enrolment, registration, and daily life.

For investors, the best assets are usually those that make operational sense whether or not citizenship ever happens. A primary residence in the city where you live is more persuasive than a purely opportunistic holding in a market you barely use.

What property can't do

Property ownership cannot repair a weak residence case. It won't replace a valid permit. It won't solve absent language preparation. It won't cure gaps in registration, tax inconsistency, or a pattern of spending too little time in Germany.

That's why I generally advise clients to avoid buying solely for immigration optics. If the property doesn't work on portfolio grounds, lifestyle grounds, or both, it usually becomes a distraction.

Buy the asset because it fits your capital strategy and your life plan. Let the citizenship file benefit from that. Don't reverse the logic.

The numbers that matter are your own

In investor conversations, “returns” often dominate too early. For German planning, I look first at durability. Can the asset be financed prudently, held without strain, and integrated into your wider reporting? Can you document income cleanly? Can you show how the property fits your centre of life?

If you're reviewing a rental asset, it helps to work from a proper operating basis rather than headline rent. A clear primer on this is Clouddle's Net Operating Income guide, which is useful for separating gross expectations from real operating performance. That discipline matters because immigration files often benefit from financial records that are simple, consistent, and well organised.

Germany compared with property-led residency markets

Investors need emotional discipline at this stage. In some markets, the property itself is the immigration product. In Germany, it isn't.

If you're mainly seeking a capital-to-status exchange, you may prefer a classic EU golden visa comparison. If you want a market where the property can support a deeper family and residency strategy, Germany has a stronger long-term logic, but it demands more real presence and more work.

That's the trade-off. Less transactional convenience. More legal substance.

Documentation Checklist and Common Pitfalls to Avoid

Most German citizenship problems are paperwork problems disguised as legal problems. Investors often qualify in principle but fail in execution because their file is incomplete, inconsistent, or assembled too late.

Core documents to organise early

Build the file as if you'll need to explain your full life in Germany to a cautious caseworker. In practice, that usually means collecting documents across four categories.

- Identity documents: Current passport, previous passports where relevant, birth certificate, marriage certificate, divorce records if applicable, and children's civil status documents.

- Residence documents: Residence permits, registration records, address history, tenancy agreements or title deeds, and correspondence showing actual occupation.

- Financial documents: Tax returns, bank statements, proof of income, business records for self-employed applicants, and property-related documents such as deeds, mortgage statements, and rental records.

- Integration documents: Language certificate, naturalisation test evidence, school records for children where relevant, and any completion records for integration-related requirements.

Property-specific records investors should not neglect

Many files become messy at this stage. Property investors often keep acquisition documents but neglect the operating trail.

Make sure you can readily produce:

| Document type | Why it matters |

|---|---|

| Purchase deed and land registry evidence | Confirms ownership and timing |

| Mortgage and repayment records | Shows financial structure and ongoing obligations |

| Rental contracts and rent receipts | Supports income evidence where relevant |

| Tax filings connected to the property | Reinforces transparency |

| Insurance and utility records | Helps show actual occupation or management continuity |

Mistakes that delay or weaken applications

Some problems are avoidable if you spot them early.

- Gaps in residence history: If your address trail is fragmented, the application becomes harder to follow and harder to trust.

- Weak financial presentation: Wealth alone isn't enough. Authorities need understandable documents, not a pile of disconnected statements from multiple jurisdictions.

- Assuming lawyers can fix bad records: Good counsel helps, but they can't invent clean chronology where none exists.

- Late language planning: Waiting until the final stretch creates pressure and often delays the filing.

- Confusing ownership with presence: Owning a property you rarely use can undermine, not strengthen, the narrative.

The strongest application file is rarely the most complex one. It's the one where identity, residence, income, and daily life all match without friction.

A practical way to manage the file

Use one master chronology. I usually recommend a dated timeline that lists addresses, permit periods, travel patterns, employment or business activity, and major property transactions. Then match each item to supporting documents.

That sounds basic, but it prevents the most common investor error. They know the story in their head, yet the documents tell it badly.

Your 5-Year Strategic Plan for German Citizenship

A workable plan for citizenship in germany is built in phases. The investors who succeed treat it like a long-term project, not a hopeful by-product of buying real estate.

Phase 1 Choose the route before the asset

Start with the immigration basis.

- Test the strongest lawful route: Employment, self-employment, or family reunification should be assessed before any purchase.

- Map family logistics: Schooling, spouse status, and travel patterns affect the credibility of residence.

- Decide whether Germany is a real base: If you only want occasional access, Germany may not be the right fit.

For British readers in particular, broader relocation planning often starts with a wider review of how to emigrate from the UK before narrowing the route down to one country.

Phase 2 Acquire property that fits the residence story

Once the route is viable, buy accordingly.

- Prioritise usability over narrative: The property should work as a home, a base, or a properly structured investment.

- Keep financing transparent: Clean banking and tax records will matter later.

- Align the asset with your actual geography: If your permit and daily life are in one city, don't buy somewhere that weakens that picture without a good reason.

Phase 3 Build the evidence year by year

This phase is where most of the actual work happens.

- Maintain continuous lawful residence

- Register and document each address properly

- Handle taxes and income reporting consistently

- Start German study early

- Keep a single organised file for all records

A citizenship application is much easier when you've been preparing for it all along.

Phase 4 Apply from a position of strength

By the time you file, your goal is simple. No surprises.

Your permit history should be clear. Your language position should already be settled. Your finances should be understandable. Your property ownership should support the broader life you've built in Germany, not stand alone as the only visible tie.

Germany can be an excellent citizenship destination for investors. But only for investors who understand the model. It is residence-led, integration-driven, and document-heavy. Buyers who accept that usually make better choices from day one.

If you're comparing Germany with other residency and property strategies, World Property Investor publishes practical guides for international buyers who want to weigh markets, visa routes, and long-term portfolio decisions without the usual hype.