For any global property investor, the distinction between freehold and leasehold is not legal jargon; it is the foundation of the asset. The difference determines ownership rights, long-term costs, and ultimate return on investment.

The core distinction is simple but critical:

- Freehold: Absolute ownership of a property and the land it is built on, in perpetuity.

- Leasehold: Ownership of the property for a fixed term, but the land is owned by a third party—the freeholder.

This single factor fundamentally shapes an investor's control, ongoing financial liabilities, and long-term capital appreciation.

Understanding Core Ownership Rights

The choice between freehold or leasehold is a primary strategic decision for an investor. It establishes the legal and financial framework for the asset, influencing everything from annual expenses and capital growth potential to the ability to undertake simple alterations.

Key areas affected by this choice include:

- Long-Term Control: Freehold provides complete autonomy, limited only by local planning regulations. Leasehold properties are subject to covenants and restrictions set by a freeholder, often requiring permission for alterations.

- Ongoing Financial Liabilities: Leasehold properties invariably involve recurring costs such as ground rent and service charges, which do not apply to freehold assets.

- Asset Longevity: A freehold is owned indefinitely. A leasehold is a diminishing asset; as the lease term shortens, its value and mortgageability can decline significantly.

At a Glance: Key Differences Between Freehold and Leasehold

To understand the practical impact of these ownership structures, a side-by-side comparison is essential. This foundational knowledge is crucial before undertaking a detailed financial analysis. For more on these core concepts, see this beginner's guide to real estate investing.

Here is a straightforward breakdown:

| Investment Factor | Freehold | Leasehold |

|---|---|---|

| Asset Ownership | You own the building and the land it sits on indefinitely. | You own the property for a fixed term; the land belongs to the freeholder. |

| Ongoing Costs | No ground rent or service charges. You are responsible for all maintenance. | Annual ground rent and service charges are typically payable to the freeholder. |

| Property Control | Full control over alterations and use, subject only to planning permission. | Restrictions (covenants) apply; permission is often needed for alterations. |

| Typical Property Type | Most common for houses in the UK and "fee simple" properties in the USA. | Standard for flats/apartments in the UK and condominiums in other markets. |

| Resale Value | Value is tied to market fundamentals without the complication of lease length. | Value can be negatively impacted if the lease term becomes too short (under 80 years). |

A freehold offers simplicity and total control. A leasehold introduces the freeholder into the investment equation, bringing a different set of rules, costs, and risks that require careful management.

Financial Implications of Ownership Structure

The choice between freehold and leasehold directly impacts an investment's financial performance. Two properties with an identical purchase price can yield vastly different returns based on their tenure. Understanding these financial mechanics is essential for accurate forecasting and achieving investment objectives.

A freehold property is financially straightforward. The primary costs are the purchase price, transaction fees (e.g., Stamp Duty Land Tax), and maintenance. The absence of ground rents and service charges provides greater control over annual outgoings and simplifies profit-and-loss calculations.

This simplicity often correlates with stronger long-term capital growth. As the landowner, the appreciation of the land contributes directly to the asset's total value—a trend supported by long-term data from bodies like the UK's Office for National Statistics (ONS).

The Leasehold Cost Structure

A leasehold introduces layers of recurring and one-off costs that erode net yield. These are legally binding obligations within the lease agreement and must be factored into any financial analysis.

Common leasehold costs include:

- Ground Rent: An annual fee paid to the freeholder. While many are nominal, some modern leases contain escalating clauses that can significantly impact profitability and mortgageability.

- Service Charges: A contribution towards the maintenance of communal areas, such as hallways, lifts, roofs, and the building's insurance. These charges can be unpredictable and are liable to increase, particularly if major works are required.

- Administration Fees: Charges levied by the freeholder for granting permissions, such as consent to sublet or make alterations.

These ongoing costs directly reduce net rental income. It is vital to scrutinise the service charge history and ground rent terms before making an offer. For a detailed guide, see our breakdown on how to calculate your real estate return on investment (ROI).

The Risk of a Diminishing Lease Term

The single greatest financial risk of a leasehold property is the diminishing lease. As a wasting asset, its value falls as the term shortens. This becomes a critical issue when the lease drops below 80 years.

Once a lease crosses this 80-year threshold, securing a mortgage becomes significantly more difficult, which shrinks the pool of potential buyers upon resale. Furthermore, the cost to extend the lease (the 'premium') increases substantially because "marriage value" becomes payable—a 50% share of the property's potential value increase that is due to the freeholder.

Investor Takeaway: Extending a lease well before it approaches the 80-year mark is a critical defensive strategy. While the cost may be substantial, failure to act can devalue the asset by a far greater amount.

The Impact Of Recent UK Reforms

The financial landscape for leaseholders in England and Wales is shifting following recent legislation. The Leasehold and Freehold Reform Act 2024 is designed to rebalance the system, making it easier and cheaper for leaseholders to extend their lease or buy their freehold. Key changes include removing the two-year ownership requirement before a leaseholder can exercise these rights.

The reform also aims to cap existing ground rents and abolish marriage value from the premium calculation. For investors, these changes make certain leasehold properties a more viable and less risky proposition. You can find out more by reading this comprehensive guide to UK leasehold purchasing.

Freehold vs Leasehold: A Real-World Example

Consider two identical flats in the same London block, both valued at £500,000.

- Property A (Share of Freehold): No ground rent. Service charges are £2,000 per annum, controlled by the resident freeholders. The lease is 999 years, so extension costs are not a factor.

- Property B (Leasehold): Has just 75 years remaining on the lease. Ground rent is £250 per annum, doubling every 20 years. Service charges, set by an external freeholder, are £3,500 per annum.

Despite the same purchase price, Property B carries an immediate and significant liability. An investor must budget an estimated £20,000 – £30,000 for a lease extension to protect its value and ensure it is mortgageable. Furthermore, its annual running costs are £1,750 higher, directly reducing the rental yield each year.

Over a decade, that amounts to an additional £17,500 in expenses, before accounting for the escalating ground rent. This demonstrates that the headline price is only the starting point; a thorough investigation of the lease is fundamental to understanding the true cost and potential return of an investment.

Navigating Legal Rights, Risks, and Responsibilities

Understanding the legal framework is as vital as analysing financial returns. The property's tenure—freehold or leasehold—fundamentally dictates an owner's control, obligations, and risks. These are not minor contractual details; they are central to investment strategy.

For a freehold owner, the legal position is clear: near-complete autonomy. Ownership of the building and the land it occupies grants final say on its management and use. This freedom, however, is coupled with total responsibility.

The Autonomy and Obligations of a Freeholder

As a freeholder, you are solely responsible for all aspects of the property. From repairing a roof to insuring the structure, the liability is yours. You are also responsible for ensuring any alterations comply with local planning regulations and building controls.

This complete control allows for asset enhancement without requiring a landlord's permission. The trade-off is the absence of any party with whom to share the financial or legal burden of maintenance and compliance.

Investor Insight: Freehold ownership offers maximum control but demands a proactive approach to property management and legal duties. An unexpected major repair, such as addressing subsidence or undertaking a full re-roofing, is the owner's sole financial and logistical problem.

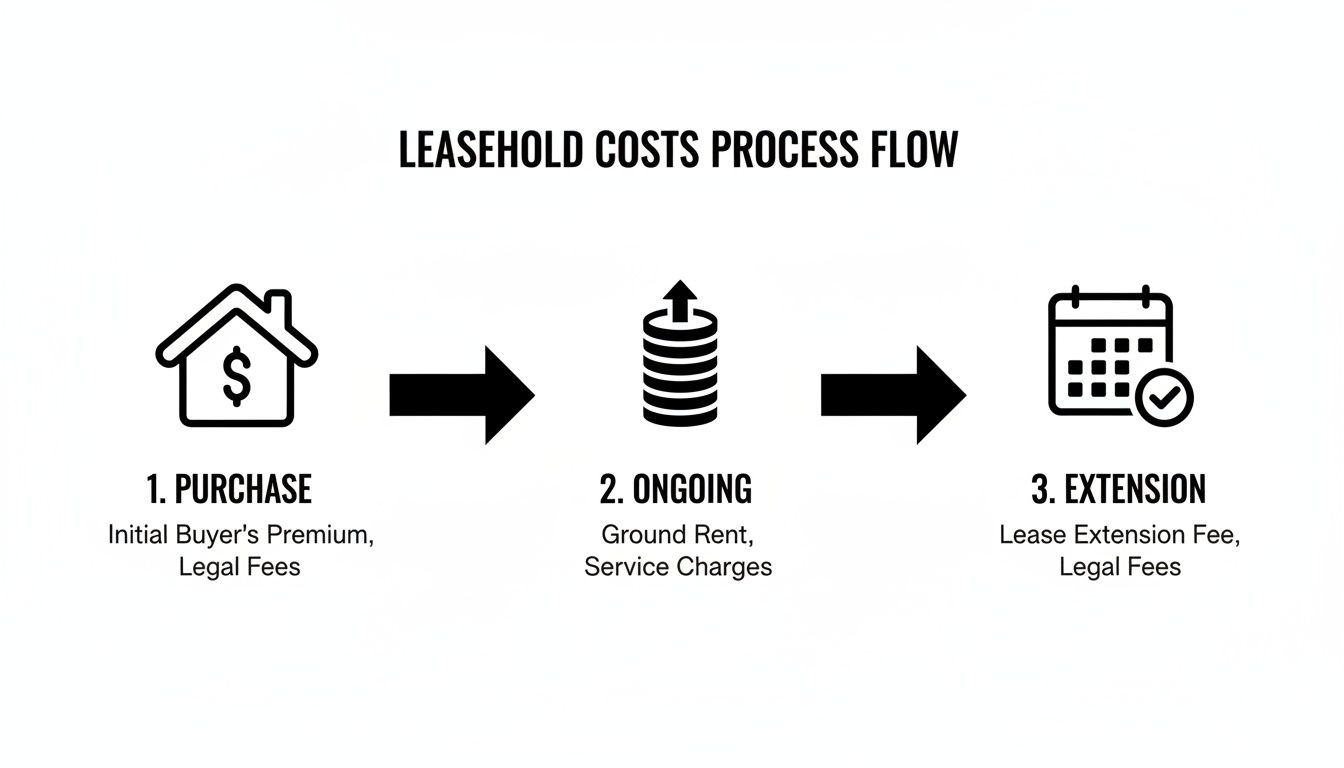

This flowchart shows the typical cost journey for a leasehold investment, from initial purchase through to the eventual—and often necessary—lease extension.

As illustrated, leasehold ownership involves a multi-stage financial commitment with ongoing charges and significant future capital outlay for lease extension.

The Lease Agreement: Your Governing Document

For a leaseholder, the lease agreement is the definitive rulebook. This legal document defines the relationship between the leaseholder and the freeholder, setting out precisely what can and cannot be done with the property. It must be scrutinised by a qualified legal professional.

The lease contains specific covenants—legally binding promises and restrictions. These can cover a range of issues affecting the use of your investment:

- Restrictions on Alterations: Many leases prohibit structural changes without the freeholder's formal consent, which often incurs a fee. This can limit an investor's ability to add value through refurbishment.

- Subletting Clauses: The lease dictates the ability to rent out the property. Some require notification to the freeholder, payment of a fee, or adherence to specific tenancy terms.

- Rules on Property Use: Covenants can control activities from running a business from home to keeping pets.

Breaching these covenants can lead to legal action from the freeholder. Understanding these limitations before acquisition is essential. You can learn more about how these duties connect with other financial obligations when you understand property taxes in our detailed guide.

Demystifying Lease Extension and Enfranchisement

Two key legal rights can secure a leasehold investment: lease extension and enfranchisement. These statutory processes allow a leaseholder to extend their lease or, in some cases, collectively purchase the freehold.

A lease extension is the right for a qualifying leaseholder to add years to their existing term (typically 90 years for a flat). This is a crucial tool for protecting a property's value as the lease term approaches the critical 80-year mark. The process involves legal notices, valuation negotiations, and significant costs.

Enfranchisement is the process where leaseholders in a building collaborate to purchase the freehold from the landlord. This converts their properties to a 'share of freehold' arrangement, granting them direct control over the building's management, service charges, and ground rent.

Both are legally complex processes requiring specialist surveyors and solicitors. However, they are powerful tools that can fundamentally improve the risk profile and value of a leasehold property, transforming a diminishing asset into one with renewed longevity and greater owner control.

A Global Perspective on Property Ownership Models

For the international investor, understanding the British freehold and leasehold system is a starting point. To identify opportunities worldwide, one must recognise how different legal systems approach property ownership. While terminology varies, the core concepts—perpetual versus fixed-term ownership—are common globally, each with local nuances.

This global perspective allows for a consistent due diligence framework, regardless of the market. Understanding local models is essential to accurately assess risks, rights, and potential returns. This is critical when investing in overseas property and navigating unfamiliar legal jurisdictions.

Established Markets: UK vs. USA

The UK's system, particularly in England and Wales, is notable for its high volume of leasehold properties, a legacy of its historical land ownership patterns. According to Gov.uk data, there were an estimated 4.98 million leasehold dwellings in England in 2021-22, representing 20% of the housing stock. This figure rises to 46% in the private rented sector, making it a dominant model for investors, especially in major cities like London. You can discover more about England's leasehold market statistics on Gov.uk.

In the USA, the equivalent of freehold is 'fee simple' ownership, granting the most complete rights to the property and land. The parallel to leasehold is found in 'condominium' (condo) or 'cooperative' (co-op) ownership. A condo owner holds the title to their individual unit, while sharing ownership and costs for common areas via a Homeowners' Association (HOA). This structure is functionally similar to a UK leasehold with service charges.

Emerging Markets: The UAE and Southeast Asia

Emerging markets often utilise leasehold-type structures to attract foreign capital while retaining national control over land.

In Dubai (UAE), foreigners are typically restricted to buying in designated 'freehold' zones. However, 'freehold' in this context usually means a long lease, often for 99 years, granted by a master developer who retains ultimate ownership of the land. This differs fundamentally from the perpetual ownership implied by UK freehold.

Similarly, in Thailand, foreign nationals are generally prohibited from owning land. They can, however, own a condominium unit outright ('freehold condominium') or enter into a long-term lease (typically 30 years, often renewable) for land or landed property.

Investor Takeaway: Terminology is market-specific. A 'freehold' title in one jurisdiction may not grant the same perpetual rights as in another. Whether it is an HOA fee in the USA or a 99-year lease in Dubai, due diligence must always include a forensic examination of what is actually owned, for how long, and under what conditions.

A Practical Due Diligence Checklist For Investors

A successful property investment is built on rigorous due diligence. The choice between freehold and leasehold fundamentally alters the scope of this investigation. Methodical due diligence is the primary defence against unforeseen liabilities.

This checklist provides a structured approach. While some checks are universal, the process for a leasehold property is far more extensive, as it involves the complexities of a third-party freeholder.

Essential Checks For All Property Types

Regardless of tenure, certain foundational checks are non-negotiable. These steps verify the asset’s physical and legal condition. Your solicitor and surveyor are key partners in this process.

Universal checks must include:

- Verifying Title Deeds: Confirm the seller's legal right to sell. This is a standard check performed by your solicitor via the Land Registry.

- Checking Planning Permissions: Investigate existing planning restrictions and confirm permissions for past works to ensure compliance with the local authority.

- Conducting a Structural Survey: Engage a qualified surveyor to assess the property’s physical integrity. A survey can uncover latent defects like subsidence, damp, or structural issues that represent significant future costs.

These steps are fundamental to understanding what you are acquiring and form the baseline to determine a property’s investment potential.

The Detailed Leasehold Investigation

For leasehold properties, due diligence must be significantly deeper, focusing on the lease document and the building's management structure. The long-term performance of the investment is tied to the lease's fine print and the freeholder's competence.

Your solicitor should request a comprehensive management pack from the seller. This contains the critical information needed to properly assess the asset and its liabilities.

Investor Insight: Never rely on verbal assurances regarding service charges or planned works. Insist on official documentation, including at least three years of service charge accounts and minutes from recent residents' meetings. This paperwork is the primary tool for uncovering hidden costs.

Critical Questions For The Lease

Analyse the lease agreement and management information in detail. The answers to these questions will determine the long-term viability and profitability of the investment.

1. The Lease Term

- How many years remain? This is the most critical question. If the term is near or below 80 years, the immediate and significant cost of a lease extension must be factored into your valuation.

- Is the lease term sufficient for mortgage purposes? Most lenders require the lease to have at least 30-40 years remaining after the mortgage term ends.

2. Ground Rent and Service Charges

- What is the current ground rent and are there review clauses? Scrutinise the lease for review mechanisms. Aggressive clauses, such as those doubling every 10 years, can render a property unmortgageable.

- What is the service charge history? Demand the accounts for the last three years to identify trends, sudden increases, or inconsistencies.

- Are any major works planned? Review AGM minutes and correspondence for information on upcoming capital expenditure (e.g., roof replacement, lift modernisation). A Section 20 notice is a formal consultation for major works and signals a significant future bill.

3. The Freeholder and Management

- Who is the freeholder? Research their reputation. An institutional freeholder may be professional but commercially aggressive. A small private landlord could be disorganised.

- Is the management company financially sound? Review the accounts. A healthy reserve or 'sinking' fund is a positive indicator of prudent financial planning for future major works.

- Have there been any disputes? Inquire about past or ongoing legal conflicts between leaseholders and the freeholder, which often indicates poor management.

Answering Key Investor Questions

This section addresses practical questions that investors frequently ask when comparing freehold and leasehold properties, providing clear, actionable answers.

Can a mortgage be secured on a short lease property?

Securing a mortgage on a property with a short lease from a mainstream lender is difficult. Most UK banks consider a lease term below 80 years to be high-risk. Many require the lease to run for at least 30-40 years beyond the end of the mortgage term.

From a lender's perspective, a short lease is a depreciating asset that compromises their security. If considering a property with a lease below 85 years, consult a specialist mortgage broker. They may have access to niche lenders, but be prepared for higher interest rates and a larger deposit requirement.

What is a 'share of freehold'?

A 'share of freehold' is a hybrid ownership model where a leaseholder also owns a portion of the building's freehold. This is typically structured in one of two ways: either all flat owners' names are on the freehold title, or a limited company is formed to own the freehold, with each flat owner holding a share in that company.

This arrangement offers significant advantages:

- Control: The owners collectively manage the building, setting service charges and appointing contractors.

- No Ground Rent: As you are your own landlord, ground rent is not payable.

- Simplified Lease Extensions: Leases can typically be extended to 999 years for minimal legal costs, permanently solving the issue of a diminishing lease term.

The responsibility for managing the building is shared, which requires effective collaboration among owners.

Investor Insight: A 'share of freehold' is often seen as the optimal structure for flats. It combines the practicalities of apartment living with the control and long-term security of freehold ownership, making these properties highly desirable on the resale market.

Is purchasing the freehold a good investment?

Yes, buying the freehold of a leasehold property—a process known as enfranchisement—can be an excellent investment. It eliminates ground rent, transfers control of building management, and allows the owner to grant a very long lease. These factors can significantly increase the property's value and marketability.

The process, however, can be legally complex and costly. The purchase price is determined by a formula considering the property's value, remaining lease term, and ground rent. For a house, an owner can act alone. For a block of flats, at least 50% of qualifying leaseholders must participate in a collective enfranchisement. Despite the initial outlay, the long-term financial upside and increased control often provide a strong return on investment.

How should a dispute with a freeholder be handled?

Disputes with freeholders often arise over service charge levels, quality of maintenance, or breaches of the lease. The first step is to consult the lease agreement to understand your rights and the freeholder's obligations.

If informal communication fails, a formal legal route is available. In England, the First-tier Tribunal (Property Chamber) is an independent body that adjudicates on such disputes. It is crucial to maintain a complete record of all correspondence—emails, letters, and call logs—as evidence. Given the legal complexities, seeking advice from a solicitor specialising in leasehold law before initiating formal proceedings is strongly recommended to ensure you are arguing from a position of strength and following correct legal procedure.