For international property investors, a European golden visa is far more than an ordinary travel document. It is a powerful financial tool that offers a direct route to living, working, and studying across the continent for you and your family. In essence, these are formal residency-by-investment programmes where a significant financial contribution—most commonly a real estate purchase of €250,000 or more—grants a non-EU citizen residency rights.

Unlocking Europe Through Strategic Investment

A golden visa is a strategic key that unlocks the stability, lifestyle, and economic opportunities of an entire continent. These government-backed schemes provide a clear pathway to residency, acting as a valuable hedge against economic and political uncertainty in an investor's home country.

The principle is straightforward. An investor makes a qualifying investment—usually in property, though some schemes allow for government bonds or business ventures—and in return, the host country grants a residence permit. One of the greatest attractions is that this permit typically includes visa-free travel throughout the 26-country Schengen Zone, a significant advantage for global business professionals and high-net-worth families.

Why Investors Pursue This Route

The motivations for seeking a European golden visa extend beyond mere convenience. For most, it is a long-term strategy for wealth preservation and securing a brighter future for their family. The core benefits driving these decisions include:

- Schengen Area Access: The freedom to travel, conduct business, and live across most of Europe without border controls is a primary driver.

- A Pathway to Citizenship: While not an immediate outcome, most golden visas offer a structured route to permanent residency and, eventually, full citizenship. This typically requires meeting specific stay requirements over a period of five to ten years.

- Family Inclusion: Nearly all programmes permit the main applicant to include their spouse and dependent children, securing access to high-calibre education and healthcare for the entire family.

- Asset Diversification: Investing in a stable European property market adds a tangible, hard-currency asset to a portfolio, balancing risks associated with other markets. You can learn more about international property investment in our dedicated guides.

Investor Takeaway: For a high-net-worth individual, a European residence permit acts as an insurance policy. It provides a 'Plan B'—a safe harbour with high living standards, excellent schools, and a stable political environment, accessible at short notice.

This guide will analyse the leading programmes in countries such as Greece, Spain, and Malta. We will break down their investment thresholds, examine property market fundamentals, and outline the practical steps required to convert an investment into European residency, providing the clarity needed to make an informed decision.

Comparing the Top Golden Visa Programmes

Selecting the right golden visa programme is not merely about identifying the lowest investment threshold. It is a strategic decision, balancing the initial capital outlay with long-term value and lifestyle objectives. Each country offers a distinct package of benefits and obligations, tailored to different investor profiles.

Demand for these programmes is increasing, particularly among UK investors seeking a viable Plan B post-Brexit. Recent data from major search engines shows UK search interest for 'Golden Visa' rose by 93.5% in the year to October 2025. More significantly, searches for 'Investment Visa' increased by 377.8% over the same period, indicating a growing sense of urgency as traditional immigration routes become more constrained. You can see the full analysis in the latest outbound investment research.

Let's break down the main contenders—Greece, Spain, Portugal, Malta, and Italy—to assess what they offer a property investor.

Greece: The Affordable Gateway (Established Market)

For a considerable time, Greece has offered one of the most direct and accessible routes into the EU via property investment. Its programme is recognised for its simplicity and relatively low cost, making it a preferred choice for investors seeking residency without excessive bureaucracy.

The minimum real estate investment was famously €250,000, but this has recently changed. For prime locations including Athens, Thessaloniki, Mykonos, and Santorini, the threshold has been raised to €800,000. In most other regions, the minimum is now €400,000, which still represents significant value.

- Processing Time: It is one of the fastest in Europe, typically taking just 3-6 months.

- Stay Requirement: There is none. You are not required to live in Greece to maintain your residency permit.

- Investor Takeaway: Greece is ideal for an investor wanting a straightforward, low-maintenance residency card that offers complete freedom of travel across the Schengen Area. The rising minimums in popular areas also suggest strong potential for capital appreciation in the property market.

Spain: A Mature Market with Lifestyle Appeal (Route Closed)

Spain's Golden Visa was a dominant force in the investment migration sector, attracting substantial capital into its prime coastal and urban property markets. However, on 3 April 2025, the Spanish government terminated the property-for-residency route, citing pressure on local housing availability.

While new applications based on real estate purchases are no longer accepted, the programme's history remains relevant for understanding the market and for existing visa holders. The minimum requirement was a €500,000 property purchase, which granted the right to live and work in Spain. Investors must now consider alternatives such as the Non-Lucrative Visa or Digital Nomad Visa if their focus is on Spain. For most, exploring other golden visa countries is the most direct path. To understand the wider landscape, consult our guide to the best countries to invest in property globally.

Portugal: A Shift from Property to Funds (Market Shift)

Portugal’s Golden Visa was once synonymous with property acquisition in Lisbon or the Algarve. Following major legislative changes, the programme has completely pivoted away from real estate to stimulate investment in other sectors of the economy.

Direct property investment and capital transfer options were eliminated in October 2023. Today, the primary routes for new applicants are focused on funds or cultural donations:

- Investment Funds: A minimum investment of €500,000 into a qualifying venture capital or private equity fund.

- Cultural Heritage: A €250,000 donation to support the arts or protect national cultural heritage.

Investor Takeaway: Portugal's pivot is a critical lesson for all investors: these programmes are dynamic. The focus has shifted from physical assets to financial products, which will appeal more to those comfortable with fund-based investing rather than direct property ownership.

For those who entered via the former property route, the pathway to citizenship after five years remains a significant advantage, requiring an average stay of just seven days per year.

Malta: English-Speaking EU Residency (Emerging Market)

Malta offers a unique proposition: residency in an English-speaking EU nation with excellent connections to both Europe and North Africa. Its scheme, the Malta Permanent Residence Programme (MPRP), is more complex than others and requires a multi-faceted contribution.

Instead of a single property purchase, applicants must meet several criteria:

- Property Investment: Either purchase a property for at least €350,000 (€300,000 in the south/Gozo) OR rent one for a minimum of €12,000 per annum (€10,000 in the south/Gozo). The property must be held for at least five years.

- Government Contribution: A non-refundable payment of €28,000 if you purchase a property, increasing to €58,000 if you rent.

- Philanthropic Donation: A mandatory €2,000 donation to a registered Maltese charity.

The entire process takes approximately 4-6 months. While the total cost, particularly for those who rent, can be lower than other schemes, the structure necessitates careful financial planning.

Italy: The High-Value Alternative

Italy’s "Investor Visa for Italy" is aimed squarely at high-net-worth individuals and is not structured around a direct real estate route like Greece or the former Spanish programme. It is designed to attract significant capital into the Italian economy through specific channels.

The primary investment options are:

- €2 million in Italian government bonds.

- €500,000 in an Italian limited company.

- €250,000 in an innovative Italian start-up.

- €1 million as a philanthropic donation.

While an investor can, of course, purchase property in Italy, it will not qualify for this particular visa. This programme is better suited for investors seeking to deploy large sums into financial assets or businesses, with residency as a valuable secondary benefit. It also features an attractive flat-tax option, capping tax on all foreign income at €100,000 per annum for new residents.

The Investment and Application Process Step by Step

So, you have determined that a Golden Visa for Europe aligns with your strategic objectives. What are the next steps? The process from initial decision to holding a residence permit is a clear, sequential journey. It is not something to be daunted by, but it demands a methodical approach and expert guidance to avoid common pitfalls that can cause delays and unnecessary expense.

Consider it a well-defined path. With the right legal and financial advisors, what appears complex becomes a manageable series of actions, turning a long-term ambition into a reality.

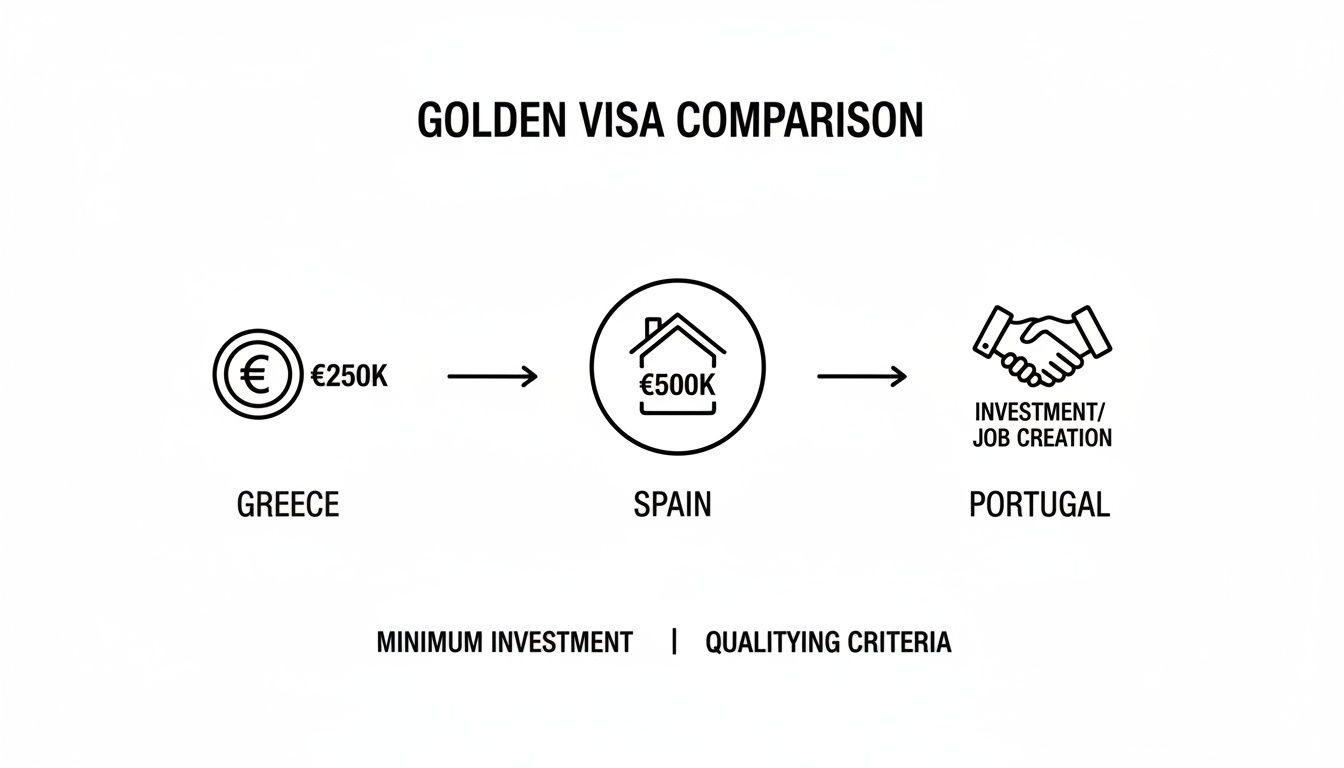

First, let's establish a clear overview. This chart offers a quick comparison of the investment routes for some of the most popular programmes.

As is evident, the minimum investment levels vary considerably. Greece offers one of the lower entry points for property, whereas Spain’s former real estate option was higher, and Portugal has now moved away from direct property investment altogether.

Stage 1: Initial Consultation and Programme Selection

Your journey begins with a strategic consultation. This is where you engage with a specialist advisor to evaluate your personal and financial ambitions against the available programmes. You will compare options like Greece versus Malta, examining the details of investment thresholds, family inclusion criteria, and long-term prospects for citizenship.

This stage forms the foundation for all subsequent actions. Is your primary goal maximum mobility across the Schengen Area? Or is a favourable tax regime the main attraction? Perhaps you simply require the quickest route to a residence card. Your answers will point directly to the country whose programme is the most suitable fit.

Stage 2: Legal Formalities and Financial Setup

Once you have selected a programme, the next step is to appoint a reputable, independent lawyer in your chosen country. This is non-negotiable. Your legal counsel will act as your representative on the ground, navigating local bureaucracy and ensuring every action is fully compliant with the law.

One of their first tasks is to secure a local tax identification number for you (such as an NIF in Portugal or an AFM in Greece). You will require this to open a local bank account, into which you will transfer the investment funds. Correctly establishing these initial financial mechanics is critical; for a deeper analysis of this, you may find our guide on financing an investment property useful.

Stage 3: Property Search and Due Diligence

With the legal and banking framework established, you can commence the property search. This is about more than finding an attractive villa or a chic city apartment; it involves rigorous due diligence. Your legal team must verify the property’s title deed, confirm it is free of any debts or liens, and check that all building permits are in order.

A classic mistake investors make is rushing the due diligence process. A thorough check protects your capital and, equally important, ensures the property qualifies for the golden visa. This prevents any last-minute application rejections.

This stage should also include market analysis to ensure the property is a sound long-term investment, well beyond its visa-qualifying function.

Stage 4: Executing the Investment and Application Submission

After completing your due diligence and making a final decision, it is time to execute the investment. This involves signing the final purchase deed and transferring the full investment amount from your local bank account to the seller.

Once the property is legally yours, your lawyer will compile the entire residency application package. This file typically includes:

- Proof of Investment: The final property deed and bank transfer confirmations.

- Personal Documents: Passports, birth certificates, and marriage certificates for all applicants.

- Proof of Funds: Evidence showing the investment capital was obtained legally.

- Clean Criminal Record: A certificate from your home country and any other country where you have resided for more than one year.

- Health Insurance: A valid policy providing coverage in your new host country.

Stage 5: Biometrics and Final Approval

With the application submitted, you and your family will need to visit the host country for a biometrics appointment. This is a straightforward procedure where you will provide fingerprints and photographs for your residence cards.

After your biometrics are captured, the application enters its final review stage. Government authorities conduct final checks before issuing approval. Timelines can vary widely, from a few months to over a year, depending on the country and its current application volume. Once approved, your residence cards are issued, and you and your family officially hold European residency.

Building Your Golden Visa Property Strategy

Choosing a property for your golden visa for Europe is not simply about meeting a minimum investment threshold. It is a serious financial decision. The property must serve a dual purpose: it must satisfy the legal requirements for residency while also functioning as a solid, profitable asset within your portfolio. A rushed purchase can result in an underperforming property that becomes a liability long after the visa has been secured.

A successful strategy involves treating this purchase with the same rigour as any other international property investment. You must look beyond marketing brochures and analyse market fundamentals, genuine rental income potential, and a clear exit strategy. The objective is simple: acquire an asset that works as hard for your portfolio as the visa does for your freedom of movement.

Conducting Thorough Due Diligence

Before any capital is transferred, exhaustive due diligence is non-negotiable. This is the crucial step that protects you from legal issues and ensures the property is worth its purchase price. Your first line of defence should always be your own independent legal counsel, who will verify the critical details that can define a transaction's success.

As a bare minimum, they should investigate:

- Title Deed Verification: Confirming the seller has the undisputed legal right to sell the property and that all registered details are correct.

- Absence of Liens and Encumbrances: Ensuring the property is free from any outstanding debts, mortgages, or legal claims that could become your responsibility.

- Planning Permissions and Zoning: Verifying that the property was built legally and complies with all local regulations—this is especially critical for new-build or off-plan projects.

- Developer Reputation: For new developments, this means a deep dive into the developer's track record, financial stability, and history of delivering on their promises.

Investor Takeaway: A common pitfall is to use the lawyer recommended by the property developer. Always appoint your own independent legal advisor. Their sole priority should be protecting your interests—a small step that can prevent significant financial and legal problems later.

Analysing Rental Yields and Market Fundamentals

Your golden visa property should be a performing asset, not merely a sunk cost. The key metric is potential rental yield—the annual rental income as a percentage of the property’s value. This is crucial for forecasting your return on investment (ROI) and requires analysis of real-world data, not aspirational marketing figures.

Let’s compare two distinct scenarios:

-

A Holiday Let in the Algarve, Portugal (Established Market): This market can deliver high seasonal yields, often between 6-10% during peak summer months. However, this income is inconsistent. Managing short-term lets is also labour-intensive and can involve substantial management fees. Off-season vacancies can reduce the annualised yield significantly.

-

A Long-Term Rental in Madrid, Spain (Established Market): A two-bedroom flat in a business district like Salamanca might offer a more modest but stable gross yield of 3-5%. The income is predictable, tenant turnover is low, and management is far less intensive. For many risk-averse investors, this consistent cash flow is more appealing.

Beyond yield, you must factor in local property taxes. In Spain, you face the Impuesto sobre Transmisiones Patrimoniales (ITP) transfer tax, which can be 6-10% depending on the region. In Greece, the property transfer tax is a much lower 3.09%. Additionally, all countries levy annual property taxes (IBI in Spain, ENFIA in Greece), which impact your net returns. For a deeper analysis, consult our guide on investing in overseas property.

Planning Your Exit Strategy

Finally, every sound investment begins with the end in mind. A well-defined exit strategy is essential. Most golden visa programmes require you to hold the qualifying investment for a minimum period, typically five years, to maintain your residency. Selling the property before this period expires will almost certainly lead to the revocation of your visa.

Your strategy should map out when and how you plan to sell. Will you divest as soon as the mandatory holding period ends to free up your capital? Or does it make more sense to hold it as a long-term rental asset, benefiting from both ongoing income and potential capital growth? This decision will be shaped by market conditions, currency movements, and your own financial goals, and it is something you should consider from day one.

Understanding Residency Rules and Tax Implications

Securing a golden visa is a significant achievement, but for a discerning investor, it is merely the start of the journey. It is absolutely essential to understand the distinction between holding a residence permit and becoming a tax resident. These two concepts are frequently confused, yet they have entirely different financial consequences.

Simply possessing a residency card does not automatically make you liable for taxes in that country. Tax residency is almost always determined by a single factor: the amount of time you physically spend there. This separation is a deliberate feature of most golden visa schemes, designed for investors who want the freedom of EU residency without completely altering their tax arrangements.

Physical Stay Requirements Explained

Each country has its own rules for maintaining an active residence permit. These minimum stay requirements are often surprisingly lenient, designed for investors who do not plan to relocate full-time. However, failing to meet them can jeopardise your entire residency status.

Here is an overview of how minimal they can be:

- Greece: There is no minimum stay requirement. You can retain your permit without ever visiting the country, which is a major attraction for passive investors.

- Spain (for existing holders): To renew an existing golden visa, you only need to visit Spain at least once per year. This simple check-in maintains your status with minimal disruption.

- Portugal (for existing property-based visas): This programme was known for its flexible rule: an average stay of just seven days per year over the five-year permit period.

Navigating the Tax Landscape

The critical number for tax purposes is 183. If you spend more than 183 days—approximately six months—in a single calendar year in most European countries, you will almost certainly be classified as a tax resident. This is where the implications become serious.

Investor Takeaway: Once you become a tax resident, you are generally liable for tax on your worldwide income, not just what you earn in that country. This could include rental income from properties in your home country, business profits, and investment dividends. Professional tax advice is non-negotiable before you consider extending your stays.

That said, some countries offer attractive tax regimes for new residents. Italy, for instance, provides a special flat-tax system where new residents can pay a fixed lump sum of €100,000 per annum to cover all foreign-sourced income. For high-net-worth individuals, this can be an extremely favourable arrangement.

This issue is becoming more critical as tax policies tighten globally. According to reports from major wealth migration consultancies, London has seen a significant outflow of high-net-worth individuals over the past decade amid concerns over tax changes. This trend, also highlighted in a report on goldenvisas.com, underscores why investors are actively seeking jurisdictions with more stable and predictable tax environments.

Ultimately, your property investment is just one element of a larger financial picture. It is vital to work with a qualified tax advisor to structure your affairs in a way that aligns with your residency goals and preserves your wealth for the long term. You might also find our general guide on understanding property taxes for investors useful.

The Future of European Golden Visas and Potential Risks

Securing a golden visa is a powerful strategic move for any global investor, but it is crucial to understand that this landscape is not static. The field of investment migration is constantly evolving, often in response to political pressures from within individual countries and the wider European Union. As an investor, you must remain aware of the political and market risks that can alter these programmes with little warning.

Recent history provides a clear illustration of how quickly circumstances can change. Portugal abruptly terminated its highly popular real estate route. Greece dramatically increased its investment minimums for Athens and the islands. And Spain, in a move that surprised many, scrapped its property visa entirely. These are not minor adjustments; they are fundamental shifts demonstrating that programmes can—and do—change or close, sometimes leaving investors who delayed on the sidelines.

Increasing Scrutiny and Stricter Rules

Looking ahead, the direction of travel is clear: greater regulation is inevitable. The European Union has become increasingly vocal about its concerns over residency-by-investment schemes, pushing member states for more robust due diligence, transparent sourcing of funds, and higher minimum investments. The objective is to ensure these programmes attract genuine, high-calibre investors who contribute to local economies, rather than simply fuelling speculative property bubbles.

For an investor, this means the window of opportunity on current, more favourable terms may be closing. Future schemes will almost certainly demand more exhaustive background checks and a larger financial commitment. This reality makes one thing clear: if a programme aligns with your goals, decisive action is a far better strategy than waiting for perfect conditions that may never materialise.

Managing Political and Investment Risks

Beyond the risk of a programme changing, you must also consider the standard risks associated with any international property investment. Factors such as political stability, currency fluctuations, and the natural cycles of the local property market all come into play. This is why having a solid exit strategy is not just advisable; it is essential. You need to know precisely how and when you can sell your property after the mandatory holding period without jeopardising your residency status.

Sudden programme closures are not a new phenomenon. The UK's Tier 1 Investor Visa, which was a major driver of foreign investment into prime London postcodes, operated from 2008 to 2022 and required a £2 million minimum investment. Its closure is a perfect example of how even long-established, high-value schemes can be terminated. It serves as a stark reminder that staying informed and being prepared to act is key. You can read more about the impact of the UK's former golden visa on the property market to understand how these dynamics play out.

Frequently Asked Questions

When investigating something as significant as a European golden visa, numerous practical questions arise. We have compiled clear, straightforward answers to the most common queries to help you understand the finer details.

Can My Family Join My Application?

Yes, absolutely. The inclusion of immediate family is one of the primary attractions of these programmes. In most cases, this includes your spouse or legal partner and any dependent children.

Some countries offer even greater flexibility. Greece, for instance, often allows the inclusion of both your own parents and your spouse’s parents, though you will likely need to provide proof of their financial dependence on you. Be prepared with all official documents, such as birth and marriage certificates; your legal team will manage the translation and apostille process.

Do I Have to Live in the Country?

This is a critical point. Holding a residence permit does not automatically oblige you to move there full-time. Many of these programmes were specifically designed for investors who plan to remain resident in their home country.

For example, Greece has no minimum stay requirement. You can maintain your residency without ever spending a night there. Others, like Spain, simply require a brief visit—once a year, for instance—to keep your permit active. This flexibility is a key part of what makes golden visas so appealing.

What Happens If I Sell My Investment Property?

You must hold your qualifying investment for a specified period, which is typically five years. If you sell the property before this mandatory holding period has elapsed, it will almost certainly result in the cancellation of your and your family’s residence permits.

Once you have surpassed that minimum timeframe, you are generally free to sell the asset without it affecting your residency status. However, if your long-term goal is permanent residency or citizenship, different rules might apply. It is always best to consult with your advisor before taking any action with the property.

Can I Use a Mortgage to Finance the Property?

Generally, no. The purpose of these programmes is to bring a significant amount of your own foreign capital into the country. This means the minimum investment—such as the €400,000 required in parts of Greece—must be paid in full with funds you have transferred from outside the country.

You may be able to obtain a mortgage for any amount you pay above that minimum threshold, but the core qualifying investment must be yours, free and clear of any loans.

At World Property Investor, we provide the data and analysis you need to make confident international property decisions. Explore our in-depth guides and market insights at https://www.worldpropertyinvestor.com.