Poland’s housing market has just done something it hadn’t done in over a decade. In late 2025, average transaction prices across the country’s seven largest cities fell 0.8% year on year on the primary market and 0.4% on the secondary market, the first simultaneous annual decline since 2013 (Statista).

That single shift changes how investors should read house prices in Poland. This is no longer a market where buyers can assume momentum will do the work for them. It’s becoming a market where entry price, rental discipline, tax treatment and city selection matter far more than headline appreciation.

For UK and international investors, that’s not bad news. It’s often the point at which a market becomes more investable.

Introduction Poland's Property Market at a Crossroads

Poland entered 2026 after one of the sharpest sentiment shifts in European housing. A market that had recently ranked among the EU's fastest price growers is now being judged on rental income, financing costs and local supply discipline rather than on broad national momentum.

That change matters more than the headline slowdown.

For a UK or international investor, Poland now sits in an unusual position. It offers a larger yield spread than many mature Western European markets, yet it does not have the institutional depth of Germany, the UK or the Netherlands. The private rented sector is still relatively young, professionally managed stock remains limited, and that creates both pricing inefficiencies and operating risk. Investors who treat Poland like a late-cycle speculative market will misread it. Investors who assess it as an income market with selective growth potential are closer to the mark.

The immediate backdrop also supports a more selective approach. Credit conditions are tighter than during the subsidy-driven upswing, households are more price-sensitive, and developers in some locations are facing a slower absorption rate. International readers tracking how a housing market stalls can affect lending volumes and buyer behaviour will recognise the pattern. Once easy mortgage growth fades, transaction discipline usually returns first, and broad price acceleration often fades with it.

Why this matters to international investors

Poland's attraction is no longer just that it is cheaper than Western Europe. The more useful comparison is after-tax income potential. In the UK, gross yields can look acceptable on paper, but financing costs, compliance burdens and tax treatment often compress net returns sharply. In Poland, the opportunity set depends more on city selection, lease structure, maintenance assumptions and the tax position of the buyer, especially for non-residents assessing post-2025 rules on ownership and reporting.

This is also a market where the gap between headline pricing and investable pricing can be wide. Prime Warsaw stock may trade more like a core European market, while regional cities with strong labour demand can still offer better cash flow. That difference is likely to matter more in 2026 than any national average.

Practical rule: In Poland, gross yield alone is a weak screening tool. Foreign investors should underwrite net yield after tax, vacancy, service charges, currency exposure and local legal costs.

The key opportunity for investors in 2026

The primary opportunity in 2026 is disciplined buy-to-let acquisition in cities where wage growth, university demand, business services employment and limited rental institutionalisation support occupancy. That is a narrower proposition than buying into a rising market, but it is often the better one.

For investors used to the UK's mature PRS, Poland can offer stronger income upside because the sector is less saturated and institutional competition is thinner. It can also demand more local execution. Tenant management standards vary, legal process matters, and small differences in micro-location can have an outsized effect on reletting risk.

A sensible starting point is to compare Polish residential pricing with broader European housing-cycle indicators and financing conditions, then test whether projected net yields still work under slower capital growth assumptions. Our 2025 property market forecast for global investors provides that wider frame.

Poland has moved from a momentum market to a selection market. That usually improves entry conditions for investors willing to underwrite carefully.

Polish House Price Trends and Market Drivers

Poland entered late 2025 with house prices still near cycle highs, even as transaction momentum cooled. For investors, that combination matters more than the headline narrative of a "correction" because it points to repricing at the margin rather than broad-based distress.

Prices are softening from a high base

The long upswing left Poland with a much higher nominal price level than a decade ago, so the recent slowdown needs to be read in context. Owners who entered earlier in the cycle have already captured substantial capital growth. Buyers entering now face a different market. Less momentum, more negotiation, and a wider gap between strong and weak assets.

That is a familiar shift in housing markets moving from policy-driven demand to fundamentals-led pricing.

The drivers of the boom

Three forces explain most of the earlier surge.

First, Poland’s income convergence with Western Europe increased household purchasing power over time. Wage growth, urban job creation and demographic concentration in major cities supported both owner-occupier demand and rental absorption.

Second, mortgage support distorted timing. Subsidised lending pulled forward demand that would otherwise have been spread across several years, particularly in the entry-level segment. That matters for investors because demand brought forward by policy often leaves a softer patch after the programme effect fades.

Third, supply remained constrained where demand was strongest. In the largest cities, new delivery did not keep pace evenly with household formation, internal migration and investor appetite. Prices therefore reacted sharply when cheaper financing and subsidies hit the market together.

The important point is not that these supports vanished overnight. It is that they stopped reinforcing one another.

Once subsidy effects weakened, affordability became more sensitive to interest rates, deposit requirements and real household budgets. That shift also helps explain why lenders have become more exposed to lower origination volumes when the housing market stalls.

2025 looked more like a plateau than a reversal

Quarterly movement through 2025 suggested a market losing speed rather than one entering a forced unwind. Short-term fluctuations at high price levels usually indicate price discovery. Buyers test vendors. Sellers anchor to the boom period. Transactions still happen, but only where financing, micro-location and unit quality line up.

That is usually healthy.

During a broad rally, weaker stock can rise alongside prime stock. In a flatter market, asset selection starts to matter more. For a UK or international investor, this is the point where Poland begins to resemble a less institutionalised version of a mature market. Price growth becomes less automatic, while execution quality matters more to total return.

Funding conditions matter, but they are no longer enough on their own

Mortgage conditions improved in late 2025, which should support activity at the margin. Even so, lower borrowing costs alone are unlikely to recreate the earlier surge because the market is adjusting to more normal buyer behaviour after a subsidy-led phase.

That changes the investment case.

In the UK, investors often underwrite residential assets within a mature PRS where competition compresses yields and operational standards are well defined. Poland offers a different proposition. The PRS remains relatively young, institutional ownership is thinner, and local fragmentation can leave room for better gross yields. But after-tax returns depend much more on unit selection, management quality, vacancy risk and local legal execution than on broad market appreciation.

Readers comparing Poland with other housing cycles should place it against the wider European repricing pattern outlined in this global property market forecast for 2025.

What is likely to drive prices in 2026

National averages now matter less than local resilience. In practical terms, investors should focus on four variables:

- depth of employment in the target city and district

- affordability for the likely tenant or end-buyer pool

- local supply pressure, especially in competing new-build schemes

- unit liquidity, with smaller apartments typically easier to let and resell

The non-obvious conclusion is that a slower market can improve entry conditions for disciplined buyers. In a momentum phase, overpaying is easy to hide. In a selection market, underwriting discipline shows up faster in both net yield and exit flexibility.

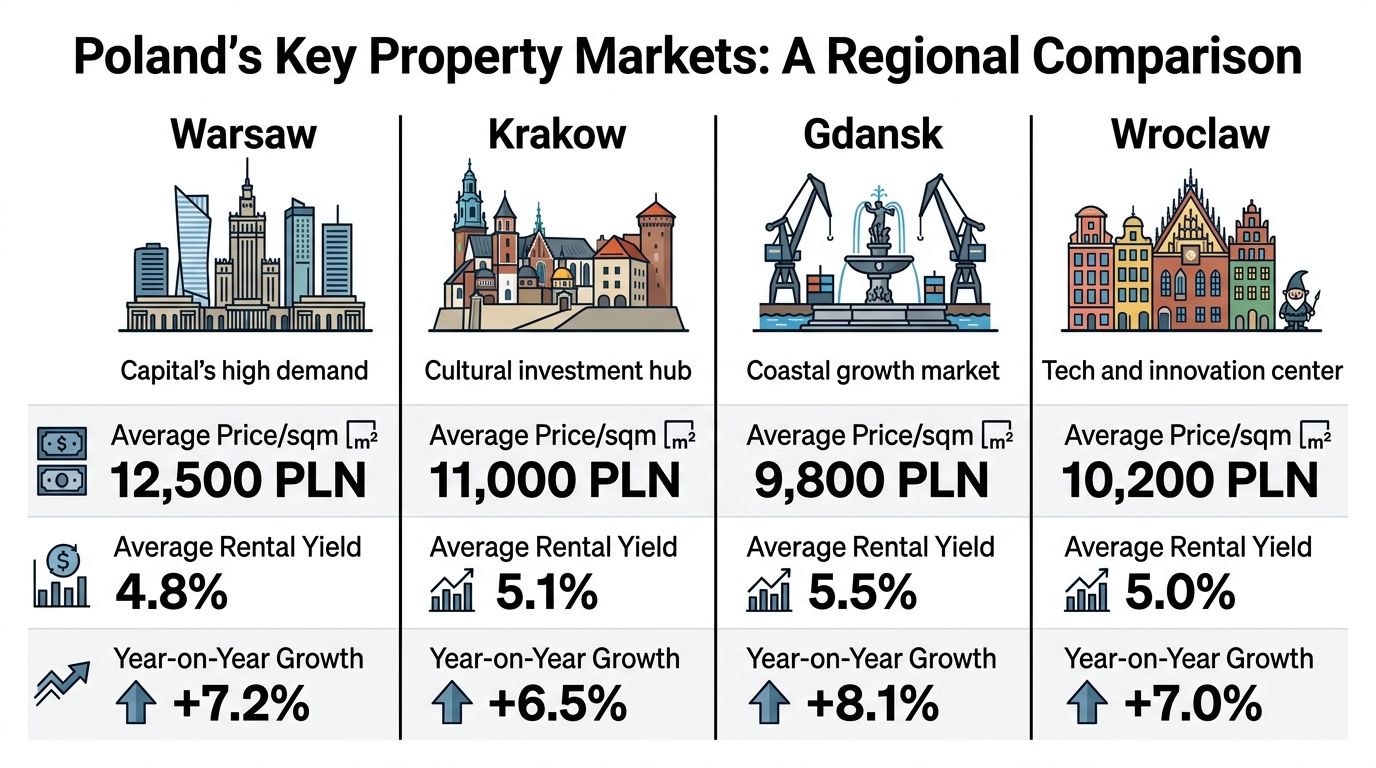

Regional Market Analysis A City-by-City Comparison

Secondary-market prices in Warsaw were roughly twice Łódź levels in 2025. That gap matters more to an investor than the national average because it changes yield tolerance, tenant targeting and exit strategy from the outset.

Poland works less like a single residential market and more like a portfolio of distinct city economies. For a UK or international buyer comparing it with a mature PRS market, the practical question is not merely where prices are highest. It is where pricing, rental depth and local regulation combine to produce a defendable after-tax return.

2026 Polish City Property Market Snapshot

| City | Avg. Price/sqm (Secondary) | Avg. Price/sqm (Primary) | YoY Price Change (Secondary) | Estimated Gross Rental Yield |

|---|---|---|---|---|

| Warsaw | PLN 16,405 | Not specified in verified data | Qualitatively softer in late 2025 | Qualitatively lower than value cities |

| Kraków | Not specified in verified data | Not specified in verified data | Not specified in verified data | As noted earlier, major cities such as Kraków have been associated with mid-single-digit to high-single-digit gross yields |

| Wrocław | Not specified in verified data | Not specified in verified data | Not specified in verified data | As noted earlier, major cities such as Wrocław have been associated with mid-single-digit to high-single-digit gross yields |

| Gdańsk | Not specified in verified data | Not specified in verified data | Not specified in verified data | Qualitatively competitive |

| Gdynia | Not specified in verified data | Not specified in verified data | -5.9% on the secondary market in Q4 2025 | Qualitatively mixed after sharp movements |

| Łódź | PLN 8,038 | Not specified in verified data | +5.9% on the secondary market in Q4 2025 | Qualitatively stronger relative yield potential |

Warsaw for liquidity, not yield leadership

Warsaw is still the reference market for foreign capital. It has the deepest employment base, the broadest buyer pool and the clearest institutional relevance if Poland’s PRS expands further after 2025.

Those strengths come at a price. At around PLN 16,405 per square metre on the secondary market in 2025, Warsaw leaves less room for pricing mistakes than most regional cities, according to the National Bank of Poland housing market database. For a UK investor used to lower net spreads in London or the South East, Warsaw may feel familiar. Strong liquidity, thinner income margin.

The non-obvious point is that Warsaw can still be the lower-risk choice for capital preservation even if it is not the best city for income. If your hold period is short, or if you expect to sell to another international buyer, liquidity has value that does not show up in a simple gross-yield comparison.

Kraków and Wrocław for balanced underwriting

Kraków and Wrocław usually sit in the most investable middle ground. They are large enough to support consistent rental demand, but typically do not require Warsaw-level entry pricing.

For international buyers, that matters because Poland’s residential market is still less institutionalised than the UK’s PRS. Operating performance depends more heavily on micro-location, unit size and management execution. In cities such as Kraków and Wrocław, that often creates a better balance between tenant depth and purchase price than in the capital.

Kraków has a broad tenant mix tied to business services, tourism-related demand and higher education. Wrocław tends to appeal to investors looking for a major employment centre with less aggressive pricing pressure. In both cities, smaller units near transport and office clusters usually make more sense than high-spec family stock bought on optimistic rent assumptions.

The Tri-City requires submarket discipline

The coastal markets are attractive, but they are less uniform than many foreign buyers assume. In Q4 2025, Gdynia’s secondary-market prices fell by 5.9% year on year, while its primary market prices rose by 11.9% in the same period, according to GetHome.pl research on asking prices in Poland’s largest cities.

That split has investment implications. It suggests buyers were still willing to pay for new product even as resale stock repriced. In practical terms, investors in Gdańsk, Gdynia and Sopot need to underwrite the exact segment they are buying. “Tri-City exposure” is too vague to be useful.

A wider international comparison is useful here. Coastal Polish cities can look compelling beside Western European resort-adjacent markets, but they also carry more pricing dispersion and seasonal demand sensitivity. This broader guide to the best cities to invest in property gives useful context on how city-level demand profiles shape returns.

Łódź as the value market

Łódź remains the clearest value case among Poland’s major cities. At PLN 8,038 per square metre on the secondary market in 2025, entry pricing was far below Warsaw, and the city still recorded 5.9% year-on-year secondary-market growth in Q4 2025, based on the same National Bank of Poland data series cited above.

That combination deserves attention from yield-focused investors. Lower capital outlay can leave more room for acceptable after-tax returns, especially for buyers comparing Poland with compressed yields in the UK or Germany. But value investing in Łódź requires a stricter employment and district screen. A low headline purchase price does not protect you from weak tenant demand in the wrong micro-market.

How I would segment the shortlist

A client screening Polish cities for 2026 can group them more usefully by function than by prestige:

- Warsaw: best for liquidity, institutional relevance and easier exits

- Kraków and Wrocław: best for balanced income potential and broad occupier demand

- Tri-City: best for diversification, but only with careful asset and submarket selection

- Łódź: best for value-led entry, provided the local demand story is clear

For a foreign investor, that is the main conclusion. Poland offers a less mature PRS field than the UK, so city choice has a bigger effect on returns. The right market depends on whether your priority is income, resale liquidity, or buying into a city where current pricing still leaves room for error.

Calculating Returns Rental Yields and Investment Potential

A one-point swing in net yield matters more than a double-digit headline price move if you are comparing Poland with the UK. For an overseas investor, returns in Poland are won or lost in the gap between gross yield, tax treatment, operating costs, and exit liquidity.

Recent price growth has been stronger than rent growth, as noted earlier. That matters because it compresses yields for buyers entering at 2025 and 2026 pricing. The practical conclusion is simple. Poland can still offer better headline income than many mature Western European markets, but purchase discipline matters more now than it did earlier in the cycle.

Why the Poland versus UK comparison matters

For a UK-based buyer, Poland sits in an unusual position. Gross yields can look more attractive than in many established UK city markets, while the rental market itself remains less institutionalised and less operationally standardised. That creates both the opportunity and the risk.

The opportunity is clearer after-tax income if you buy well and control costs. The risk is that a less mature PRS environment places more weight on local execution. Tenant selection, building management, lease structure, and reletting speed have a larger effect on realised returns than many foreign buyers expect.

This is why Poland should not be assessed as a simple yield trade.

It is better viewed as a market where private investors can still capture some of the operational premium that large landlords and institutions have already competed away in the UK. In practical terms, that means stronger upside for investors who can source well, manage tightly, and avoid weak micro-locations. It also means less room for passive ownership mistakes.

Start with gross yield, then move quickly to net

Gross yield is a screening tool. Net yield decides whether the asset belongs in your portfolio.

A disciplined review usually follows this order:

- Estimate realistic annual rent. Use achieved rents from comparable units where possible, not optimistic asking rents.

- Calculate gross yield. Divide annual rent by the full acquisition cost, not just the agreed headline price.

- Apply tax correctly. Local tax treatment can materially change the cash return available to a foreign owner.

- Deduct operating costs. Include management fees, insurance, repairs, vacancy, and any service charges the tenant does not cover.

- Stress test the income. Model slower reletting, a softer rent on renewal, and higher maintenance than expected.

If you want a structured model, this guide on how to calculate return on investment property is a useful starting framework.

The financing side also deserves separate modelling, especially for overseas buyers balancing sterling income against zloty exposure and local borrowing costs. A practical primer on how to finance an investment property can help frame that decision.

The after-tax point is where Poland often holds up well

Many broad market guides stop at gross yield. That is not enough for a cross-border investor.

What matters is the amount left after tax, recurring costs, and vacancy. In a market such as Poland, where rental yields can still screen well against the UK, after-tax return is the more useful comparison because it captures the actual advantage rather than the marketing headline. A property with a slightly lower gross yield but cleaner building economics and more stable tenant demand can outperform a cheaper flat bought in the wrong district.

That is particularly relevant in a nascent PRS setting. Mature rental markets usually price operational quality more efficiently. Poland still has room for informed investors to gain an edge through better asset selection and tighter management.

A practical underwriting approach for 2026

I would treat Polish residential investments in three layers.

First, test whether the city supports consistent demand from students, professionals, or corporate tenants. Second, check whether the specific district and building support that demand in practice. Third, ask whether the numbers still work after a conservative vacancy and cost assumption.

That last step filters out many weak deals.

A flat can look attractive on a portal and still produce mediocre returns once you account for reletting friction, furnishing costs, and periods when the unit is empty between tenants. Foreign buyers often underestimate those frictions because the purchase price looks low relative to London, Manchester, or regional German cities. Low entry cost does not automatically mean high investment quality.

Investor filter: If the deal only works with full occupancy, minimal repairs, and no pricing pressure on rent, the underwriting is too optimistic.

A brief video overview can also help if you want a more visual primer on analysing overseas property returns:

Where the investment case is strongest

The best opportunities are usually not the most fashionable units in the most aggressively priced schemes. They are properties bought at a sensible basis in cities with broad tenant demand, in buildings that are easy to let and easy to resell.

For UK and international investors, that is the more useful conclusion than any headline yield range. Poland still offers a credible income case relative to mature markets, but the return profile depends on underwriting discipline and local execution. In a younger PRS market, those two factors have a larger effect on real performance than many buyers assume.

The Practical Guide to Buying Property in Poland

Good market selection can still be undone by weak execution. Buying abroad is usually less about finding a listing and more about managing process risk.

Start with ownership rules and legal checks

Foreign buyers need to establish early whether their purchase falls into a straightforward category or a more regulated one. In practical terms, apartments are often simpler than land-heavy assets or standalone houses, especially for non-EU investors. The legal route depends on nationality, property type and how the title is structured.

That means your first serious conversation shouldn’t be with a selling agent. It should be with an independent Polish lawyer or notary experienced in cross-border transactions.

Your legal review should confirm:

- Title integrity: Make sure the land and mortgage register matches what’s being sold.

- Seller authority: Check that the vendor has the right to dispose of the property.

- Building-level obligations: Review any management, service or use restrictions that affect rentals.

- Tenant status: Confirm whether the flat is delivered vacant or with an existing occupier.

- Foreign-buyer compliance: Clarify early whether a permit is required in your case.

Budget for costs before you negotiate

Many overseas buyers focus too narrowly on the purchase price. That’s a mistake. In Poland, your all-in basis can shift materially depending on whether you buy on the primary or secondary market, how the transaction is documented and what services you need to close.

The practical rule is simple. Build your full acquisition budget before making an offer. If you don’t, you can misread the true yield from the start.

For buyers who want a broader framework before approaching lenders or brokers, this primer on how to finance an investment property is a useful complement to local advice.

A sensible transaction sequence

The smoothest purchases usually follow a disciplined order.

Shortlist the asset properly

Don’t view Poland as one market. Narrow by city, unit type and tenant profile first.Engage local professionals early

Use an independent lawyer. If you’re financing, speak to lenders before you commit.Check the title and building documents

Many hidden issues surface during this process. Service obligations, encumbrances and use restrictions can all affect returns.Agree the economics in writing

Clarify fixtures, completion timing, deposit mechanics and any conditions tied to financing or legal review.Sign through a notarial process

In Poland, formal completion mechanics are central to enforceability and registration.Register ownership and set up operations

Once title is finalised, move immediately to utilities, tax administration, insurance and property management.

A foreign buyer’s edge rarely comes from speed. It comes from sequence. The more disciplined your process, the lower the chance of an expensive surprise after completion.

Financing and currency deserve more attention

Even when you’re buying for cash, currency is part of the deal. Most international investors are funding from GBP or EUR, while the asset and rental income are denominated in PLN. That means your return can move for reasons unrelated to the property itself.

If you’re borrowing, complexity rises again. Local mortgage terms, underwriting standards and documentation requirements can differ markedly from what UK investors expect. That doesn’t make financing impossible. It means you should test debt availability before treating borrowed funds as part of the investment case.

Operational setup is where many foreign buyers fall short

The easiest mistake is assuming acquisition is the hard part and management is routine. In reality, your net result often depends more on operations than on the purchase itself.

Pay close attention to:

- Letting strategy: Long-term tenants and short-stay use produce very different risk profiles.

- Management quality: A good local manager protects income consistency and asset condition.

- Maintenance standards: Common areas and block governance matter for tenant retention.

- Record keeping: Keep clean documentation for tax and compliance purposes from day one.

If you want a broader framework for cross-border transactions before narrowing to Poland, this guide on how to buy property abroad is a useful checklist.

The best Polish acquisitions usually look slightly boring on paper. Clean title, ordinary unit, resilient tenant base, realistic yield. That’s often where the strongest long-term outcomes are found.

Risks Forecast and Concluding Thoughts for 2026

A market where resale sellers increasingly accept discounts is not a market to buy on autopilot. For a UK or international investor, that matters more than the headline price path, because Poland’s appeal in 2026 rests on execution: entry price, tax treatment, financing terms, and the gap between gross yield and what reaches your account after costs.

The positive case still stands. Poland retains large urban labour markets, a growing stock of professionally managed rental housing, and rental yields that can still exceed what many investors now see in mature UK or Western European cities. But the market is no longer forgiving. Returns depend less on broad appreciation and more on buying the right asset in the right micro-location at the right basis.

The risks that deserve the most attention

Currency remains the first filter. A flat year in zloty terms can still become a weaker result in sterling or euros if the PLN moves against you. That makes Poland less suitable for buyers who judge success only in local-currency terms and more suitable for investors willing to hedge selectively or hold for long enough that currency cycles matter less.

Second, the market could spend longer in a low-growth phase than many buyers expect. As noted earlier, late-2025 conditions pointed to a cooler pricing environment. That does not imply distress. It does imply that underwriting based on quick capital growth is weak discipline, especially in cities where new supply and stretched affordability are still working through the system.

Third, policy risk remains real. Housing demand in Poland has been influenced by state support schemes, and any replacement measures after 2025 may shift demand between first-time buyers, owner-occupiers and investors rather than lifting the whole market. Foreign buyers also need to watch how post-2025 rules are applied in practice, particularly where permitting, tax administration, reporting, or beneficial ownership checks add friction to the transaction process.

What the near-term outlook suggests

The base case for 2026 is a market with modest pricing power, slower deal velocity, and more room to negotiate than buyers had during the surge years.

That suits analytical investors. It gives disciplined buyers time to compare resale versus developer stock, test local rent assumptions, and reject deals that only work under optimistic appreciation scenarios. In practical terms, Poland now looks less like a momentum trade and more like an income strategy with selective upside.

That distinction matters if you are comparing Poland with the UK. In a mature PRS market, lower operational uncertainty often comes with lower yields and more efficient pricing. In Poland, the PRS is still developing, institutional ownership is smaller, and local execution risk is higher. The compensation is often a better starting yield, but only if tax, vacancy, management and FX costs are modelled properly.

Who Poland suits in 2026

Poland fits investors who can assess net income rather than rely on simple price narratives.

- Yield-focused buyers comparing Polish cities against lower-yield UK regional and London markets.

- Long-term holders who want exposure to urban demand growth without paying fully mature-market valuations.

- Investors comfortable with local complexity around management, tax filing, and city-specific liquidity.

- Buyers willing to negotiate hard in the resale market and walk away when underwriting does not hold.

It is a weaker fit for buyers expecting a fully institutional rental environment across every major city, or for anyone who needs debt, tax and operations to work exactly as they do in Britain. Poland can produce attractive after-tax returns, but it still rewards local knowledge more than passive expectations.

Buy Poland for disciplined income and medium-term urban demand. Buy it only if the numbers still work after tax, fees, vacancy and currency effects.

My concluding view

The Polish market is more investable in 2026 than the headline slowdown suggests. The reason is simple. Slower markets usually expose pricing errors, weaker stock, and overconfident sellers. That gives well-prepared buyers a better chance to secure acceptable entry yields.

City selection still matters, but so does market segment selection. Warsaw remains the deepest and most liquid market, though not always the highest-yielding one. Kraków and Wrocław remain strong for buyers balancing tenant demand with income. Łódź still deserves attention from value-oriented investors, but only where the local employment base and exit liquidity are clear.

For investors placing Poland in a wider allocation decision, this review of international property market trends is useful context.

The broad conclusion is straightforward. Poland no longer looks like a simple catch-up trade on rising prices. It looks more like a market where careful underwriting, realistic tax assumptions, and strong local execution can still produce returns that compare well with more mature rental markets.