For a global property investor, a second passport is not merely a travel document; it is one of the most powerful strategic tools available. But how do you get dual citizenship? Most investors follow one of three primary routes: tracing their ancestry (descent), long-term residency (naturalisation), or through direct investment programmes.

This guide provides a practical breakdown of these pathways, offering the actionable insights required to build a more resilient and diversified global property portfolio.

Why Dual Citizenship Is a Strategic Asset for Investors

Dual citizenship is the legal status of being a citizen of two countries simultaneously. The UK, for instance, has permitted this since the British Nationality Act of 1981, and for a UK-based investor, this status can be genuinely transformative.

For example, holding a second passport from an EU country reopens the door to frictionless investment across the continent, bypassing many of the post-Brexit hurdles non-EU nationals now face.

Conversely, for an international investor targeting the UK market, obtaining British citizenship can provide a significant competitive advantage. It may offer relief from certain foreign buyer taxes and often improves access to more favourable mortgage financing from UK lenders.

Unlocking Market Access and Mitigating Risk

A second passport is the ultimate ‘Plan B’, providing a safe harbour for you, your family, and your capital during periods of economic or political instability. It also acts as a powerful key, allowing you to enter property markets that might otherwise be restrictive or less profitable for foreign nationals.

Beyond market access, dual nationality offers tangible benefits that directly impact your bottom line:

- Tax Optimisation: Holding citizenship in a low-tax jurisdiction can create pathways to legally reduce your tax burden on rental income and capital gains. This requires careful planning with international tax specialists, but the benefits can be substantial.

- Enhanced Mobility: Visa-free travel to a wider range of countries simplifies everything from on-the-ground research and property management to closing deals in person. A passport from a Schengen Area country, for example, grants unrestricted movement across 29 European nations.

- Generational Wealth: In many cases, dual citizenship can be passed down to your children, securing their global mobility and future investment opportunities for generations to come.

Key Takeaway: For the strategic property investor, dual citizenship is less about collecting passport stamps and more about building a firewall against global uncertainty. It provides the legal and financial architecture to operate seamlessly across borders, turning international markets into local opportunities.

Contrasting Established and Emerging Markets

The strategic value of a second passport changes depending on the market you're targeting. In established economies like the UK or Germany, citizenship grants stability and access to mature legal and financial systems. Credible data from bodies like the ONS consistently shows that property prices in these economies often deliver slower but more reliable long-term growth.

In contrast, emerging markets may offer the promise of higher rental yields and faster capital appreciation, but they also come with greater political and currency risk. A second citizenship can act as an anchor, giving you a secure base from which to make calculated investments in these higher-growth regions. It provides an edge in both worlds.

To see how this works in practice, you can explore our detailed guide on EU Golden Visa options.

To help you compare the main routes, this table summarises what each pathway typically involves.

Dual Citizenship Pathways at a Glance

| Pathway | Typical Timeframe | Key Requirement | Best For Investors Who… |

|---|---|---|---|

| Citizenship by Descent | 6-24 months | Provable ancestry (parent, grandparent) | Have a family connection and want the most direct, low-cost route. |

| Citizenship by Naturalisation | 5-10+ years | Long-term legal residency in the country | Are planning to live in and integrate into a new country long-term. |

| Citizenship by Investment | 3-12 months | A significant financial contribution (e.g., property) | Prioritise speed and efficiency and have the capital to invest. |

| Citizenship by Marriage | 3-5 years | A legally recognised marriage to a citizen | Are in a genuine, long-term relationship with a foreign national. |

Each path has its own set of rules, timelines, and costs. The right choice depends entirely on your personal circumstances, your long-term goals, and how quickly you need to secure your new status.

Unlocking Citizenship Through Your Family Tree

For many investors, the most direct and affordable route to a second passport involves neither large capital outlays nor years of residency. It is found in their own family history. This is citizenship by descent, or jus sanguinis (right of blood), and it is a powerful option if you have parents, grandparents, or in some cases, even great-grandparents from another country.

If you qualify, this path is a game-changer. It allows you to sidestep the long-term commitments of naturalisation and the high costs of investment programmes. Your eligibility is based purely on lineage, and the primary challenge is gathering the necessary documentation.

Numerous countries offer some form of citizenship by descent, though rules vary significantly. Italy and Ireland are known for generous policies that can reach back generations. Others, like the UK, have more specific but valuable pathways for those who qualify.

Putting Descent-Based Citizenship into Practice

The process hinges on creating an unbroken paper trail. You will need to locate official records such as birth certificates, marriage licences, and potentially old naturalisation papers for each ancestor linking you to your target country. It is detective work into your own family’s legal history.

For a property investor, the advantages are immediate. Consider a Canadian investor whose mother was born in the UK. By registering as a British citizen, they can operate in the UK property market like a local—potentially avoiding foreign buyer taxes, accessing better mortgage deals, and simplifying transactions.

Key Takeaway: The descent route is highly efficient. It unlocks the strategic benefits of a second passport—market access, tax advantages, and a solid 'Plan B'—often in under two years and for a fraction of the cost of investment-based citizenship.

A common way investors gain a foothold in the UK is through this exact route. If you were born abroad to a British parent, you can often register as a citizen without renouncing your current nationality, a provision allowed by the British Nationality Act 1981. According to Gov.uk Home Office statistics, thousands of individuals become British citizens this way each year, providing a direct route for investors eyeing the UK's stable buy-to-let market without residency requirements. You can read more on the nuances of UK dual citizenship policy.

Tackling the Paperwork

Your application is only as strong as the documents supporting it. While specifics vary, gathering the following is a typical starting point:

- Your full birth certificate, listing your parents.

- Your qualifying parent's or grandparent's birth certificate to prove their place of birth.

- Your parents' marriage certificate (if applicable).

- Proof of your identity, such as your current passport.

- Documents for any name changes, such as a deed poll or marriage certificate, to connect records if names do not match.

Do not submit photocopies. You will need originals or officially certified copies. Any documents not in the country's official language must be professionally translated and certified. This part of the process is meticulous; one missing paper can cause months of delay.

For example, an American investor claiming Irish citizenship through a grandparent born in Cork before 1922 would need to produce birth and marriage certificates and get their name onto the Foreign Births Register. Due to high demand, processing by Ireland's Department of Foreign Affairs can take over a year, demonstrating the need for organisation and patience.

The Residency Pathway to Citizenship via Naturalisation

For many property investors, the objective is not just owning assets abroad—it is becoming a true local. Naturalisation is the traditional route to achieving this. It is the 'long game' of dual citizenship, where you establish legal residency in a country, integrate into society, and after several years, earn the right to apply for a passport.

Unlike citizenship by descent, this path is open to almost anyone who can meet a country's legal and residency criteria. It demands a serious commitment of time and physical presence, but the reward is full citizenship. For a property investor, this is transformative: you are no longer a foreign buyer but are treated as a local for tax, finance, and purchasing purposes.

The UK Naturalisation Process for Investors

In the United Kingdom, the road to a British passport through naturalisation is a well-defined, multi-year journey. It begins with securing a long-term visa that permits you to live in the country, which acts as your initial residency permit.

The path generally follows these key milestones:

- Initial Residency: First, you must live in the UK legally for a set period. For most visa routes popular with investors, this qualifying period is five years.

- Permanent Residency: After five years, you can apply for 'Indefinite Leave to Remain' (ILR). This grants you permanent resident status and frees you from most immigration controls.

- Citizenship Application: Once you have held ILR status for at least 12 months, you can apply for naturalisation to become a British citizen.

Key Takeaway: This entire process, from obtaining your first visa to holding a British passport, takes a minimum of six years. It is a marathon, not a sprint, designed for those who see the UK not just as a place to invest, but as a long-term base or future home.

For property investors, this deep integration pays clear dividends. As a resident and eventual citizen, you are no longer subject to potential foreign buyer stamp duty surcharges, and high-street lenders are often more willing to offer competitive mortgage rates. You can explore our guide on the different types of visas available for investors to understand these crucial first steps.

Comparing Established vs. Emerging Markets

The UK’s six-year path provides a solid benchmark. How does it compare to Portugal, another popular destination for property investors? The Portuguese naturalisation timeline is also five years of legal residency. However, the residency requirement can be far less demanding, especially for those on its well-known 'Golden Visa' programme, which has historically required an average of just seven days per year in the country.

This highlights a critical point for investors: analyse both the total time and the actual physical presence required.

| Country | Minimum Residency Before Citizenship | Key Requirements | Investor Suitability |

|---|---|---|---|

| United Kingdom | 6 years (5 years residency + 1 year ILR) | Continuous physical presence, 'Life in the UK' test, English proficiency. | Best for investors planning to relocate and live full-time in the UK. |

| Portugal | 5 years | Basic Portuguese language test (A2 level), clear criminal record. | Ideal for investors who want a path to EU citizenship with minimal physical stay requirements. |

This distinction is fundamental. The UK path is a perfect fit for an investor genuinely relocating their family or business. In contrast, the Portuguese route has been tailored for those seeking a second passport for portfolio diversification and EU access, without having to completely uproot their lives.

For EU nationals, naturalisation has become a key route to UK dual citizenship post-Brexit. The UK permits dual nationality, and after five years of lawful residence, passing the Life in the UK test, and proving B1-level English, the path is clear. According to Home Office data, over 90,000 main applicants are granted British citizenship via naturalisation annually, showing a strong and sustained trend. You can find more insights on dual citizenship trends.

While routes like ancestry or long-term residency are the standard ways to get a second passport, they can take years. For many global property investors, that timeline is not viable. You need to move faster to seize opportunities.

Thankfully, there are quicker options. Two pathways stand out for their speed: marriage to a citizen and a formal Citizenship by Investment (CBI) programme. These can cut the process down from years to, in some cases, a matter of months.

For a property investor, faster citizenship is not just a travel perk. It means you can integrate into a new market, access local financing, and potentially avoid hefty foreign buyer taxes much sooner. It is a serious competitive advantage.

The Marriage Pathway

Marrying a citizen of your target country is often an accelerated route to citizenship. This is a common path for couples building a life—and often a property portfolio—together. This is built on a genuine relationship, and governments are rightly scrupulous in verifying that a marriage is legitimate and not one of convenience.

Take the UK, for example. Marrying a British citizen offers a much quicker dual citizenship track. Normally, you would need five years of residency to apply for naturalisation. On a spouse visa, that drops to just 3 years of continuous residency, provided you meet other criteria.

Home Office statistics confirm that family-related grants are a significant component of naturalisations. As the UK’s policy allows dual nationality, a high percentage of these applicants keep their original passport. You can find more details on countries that permit dual nationality.

You'll typically need to provide:

- Proof of a genuine relationship: This includes joint bank accounts, property deeds in both names, photos, and statements from friends and family.

- Financial stability: You must show you can support yourselves without relying on public funds.

- Residency: You must live in the country for the required period, which is almost always shorter than for other visa types.

Citizenship by Investment: The Direct Route

For high-net-worth investors, Citizenship by Investment (CBI) programmes are the most direct route to a second passport. These programmes allow you to make a significant financial contribution—often through buying real estate or donating to a national fund—in return for full citizenship.

Key Takeaway: The primary appeal of CBI is speed and certainty. A successful application can grant you and your family citizenship in as little as three to six months, providing immediate global mobility and unrestricted investment freedom. For investors who value efficiency above all, this is the ultimate tool.

It is important not to confuse these with 'Golden Visas'. A Golden Visa typically grants residency, which can be a stepping stone toward citizenship. CBI, on the other hand, is the final destination.

Comparing CBI Markets: Established vs. Emerging

The CBI landscape is diverse, with a clear choice between long-running Caribbean programmes and newer European options. Each comes with a different risk and reward profile for a property investor.

Established Caribbean Programmes (e.g., St Kitts & Nevis, Grenada)

These are the pioneers of the CBI world. The mechanism is simple: you either purchase a piece of government-approved real estate (often a share in a resort) or make a non-refundable donation to a state fund.

- The Investment & ROI: The passport itself is the primary return on investment. While the real estate can generate rental yields, the resale market is often restricted to other CBI applicants, which can limit capital growth. Deep due diligence on the developer is critical.

- The Risks: The biggest risk is the long-term value and liquidity of the property. If it cannot be sold on the open market, its value is tied to the programme's future success. The passport’s travel benefits can also change depending on international agreements.

Emerging European Markets (e.g., Malta, Turkey)

European programmes demand a much higher investment, but the prize is often an EU passport or citizenship in a strategically vital location. Malta’s programme requires a mix of property purchase/lease, an investment, and a direct contribution. Turkey offers citizenship for a qualifying real estate purchase.

- The Investment & ROI: The real estate here is usually part of an open, liquid market. Buying an apartment in Istanbul or a villa in Malta gives you an asset with mainstream potential for capital growth and rental income, entirely separate from the CBI programme.

- The Risks: These programmes face more scrutiny from bodies like the EU, which can lead to sudden policy changes. The higher investment levels also mean more capital is at risk.

For any investor pursuing this fast-track route, it is vital to look beyond the passport. A detailed analysis of the property itself—its location, yield potential, and exit strategy—is just as important as the citizenship benefits it unlocks.

You can check out our guide on Citizenship by Investment programmes for a deeper dive into the specific options available.

Navigating the Legal and Financial Complexities

Gaining a second passport is a major achievement, but it is only half the journey. The other half is mastering the new legal and financial duties that come with it. Rushing into this without a clear plan can lead to expensive mistakes.

Without doubt, the most critical area to understand is taxation. This is a corner you cannot cut—seeking professional advice is not just a good idea, it is essential. The rules vary dramatically between countries and will directly impact the real-world returns of your property portfolio.

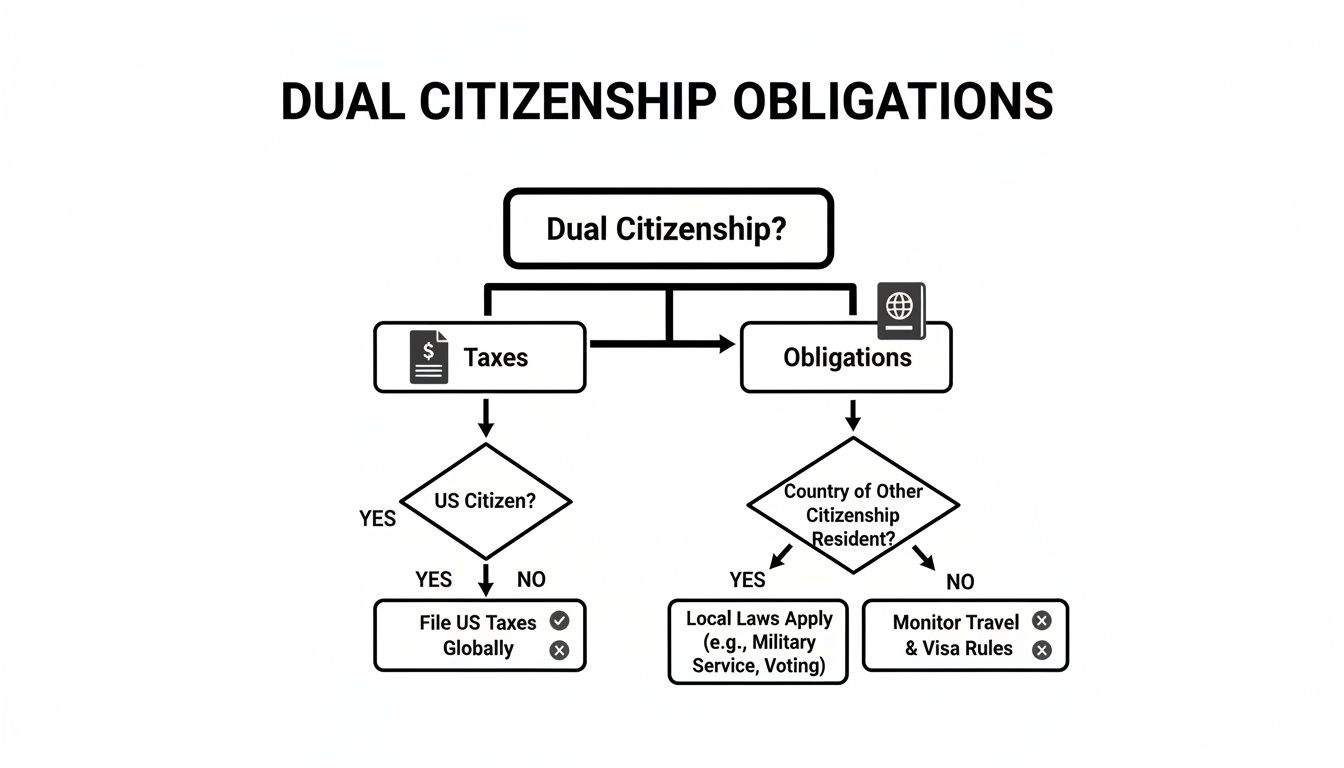

This decision tree gives you a clearer picture of the main responsibilities that come with dual citizenship, from taxes to other legal duties you’ll need to manage.

As you can see, your obligations extend far beyond filing an extra tax return, touching on everything from local laws to how you travel.

Understanding Your Tax Obligations

First, you need to master the concept of tax residency. The UK, for example, primarily taxes individuals based on their residency status. A UK tax resident is generally taxed on their worldwide income and capital gains. A non-resident is usually only liable for tax on UK-sourced income.

However, some countries, like the United States, operate on a citizenship-based taxation system. This means they tax their citizens on worldwide income, regardless of where they live. An investor holding both British and US passports could face tax bills in both countries.

This can lead to double taxation—where the same income is taxed twice. Fortunately, many countries have Double Taxation Agreements (DTAs) to prevent this. The UK has one of the world's largest networks of tax treaties, but interpreting their specific clauses requires an expert who can apply them to your situation.

Key Takeaway: A second citizenship complicates your tax profile but need not complicate your life. The key is proactive engagement with international tax advisors specialising in your relevant jurisdictions. They can structure your affairs to remain compliant while legally optimising your tax position.

Legal and Personal Obligations to Consider

Beyond taxes, a new citizenship can introduce personal and legal duties. These are often overlooked but can have serious consequences if you are not prepared.

- Renunciation of Previous Citizenship: Not all countries permit dual nationality. Before starting an application, you must confirm whether your home country—or the country you're applying to—will require you to give up your existing citizenship.

- Mandatory Military Service: Some nations, including Greece and Turkey, have compulsory military service for male citizens. Exemptions often exist for those living abroad or gaining citizenship later in life, but you must check the specific rules.

- Inheritance and Estate Planning: Dual nationality directly affects how your global property portfolio is handled for inheritance tax and estate planning. The laws governing how assets are passed to heirs can differ dramatically. Your will may need to be redrafted to be valid and tax-efficient across multiple countries.

For investors exploring routes like the Portugal Golden Visa, understanding these wider implications from day one is crucial. The journey to Portuguese residency and eventual citizenship comes with its own set of legal factors that must be woven into your long-term plan.

The takeaway is clear: engage qualified immigration lawyers and international tax professionals from the very beginning. Their initial fee is a small price to pay to avoid far more expensive problems later.

Your Practical Dual Citizenship Checklist

Knowing the theory is one thing; turning it into a successful application is where the real work begins. This practical checklist breaks down the key steps and documents you will need.

Think of this as your roadmap. A strong application is about meticulous organisation. Getting your affairs in order before you commit any serious capital is non-negotiable.

First, a Reality Check: Self-Assessment and Strategy

Before gathering documents, the first step is an honest self-assessment. Answering these questions will quickly identify which pathways are viable and will shape your entire approach.

Examine Your Family Tree: Do you have parents or grandparents born in another country? If yes, citizenship by descent is almost always your most direct and affordable route.

Consider Your Lifestyle: Are you prepared to relocate and live in a new country for 3-6 years to meet naturalisation requirements? This is a significant commitment.

Assess Your Investment Capital: Do you have the liquid funds to meet the minimum for a Citizenship by Investment (CBI) programme? These typically start around £200,000 and can exceed £2 million.

Check Your Home Country's Rules: This is critical. Does your current country of citizenship permit holding a second passport? Some nations require renunciation, so confirm this from the outset.

This initial review acts as a filter, narrowing your focus to the one or two routes that are actually viable for you.

Assembling Your Core Documents

Once you have identified a promising pathway, it is time to gather evidence. While specific requirements change from country to country, almost every application relies on the same core documents. Start sourcing these early, as it can take months to obtain official copies.

Key Takeaway: A classic mistake is underestimating how long it takes government agencies to issue certified documents. Order birth certificates, marriage licences, and other official records the moment you decide on a path. Your application can only move as fast as its slowest piece of paper.

Your essential document file should contain:

Personal IDs: Your current passport (with at least 12 months of validity), driver’s licence, and any national ID cards.

Vital Records: Your full, long-form birth certificate and, if relevant, your marriage certificate. For descent applications, you will need these for your parents or grandparents too.

Proof of Financial Stability: Bank statements for the last 6-12 months, payslips or tax returns, and evidence of any investment capital.

Proof of Address: Recent utility bills, a tenancy agreement, or property deeds showing your current address. For naturalisation, you'll need years of these to prove continuous residency.

Clean Criminal Record: A police clearance certificate from your home country and any other country where you have lived for more than 12 months as an adult.

Key Dos and Don'ts for a Smooth Application

Navigating government bureaucracy requires a sharp eye for detail. Simple mistakes can cause major delays.

Do:

- Get Official Translations: Any document not in the official language of the country you're applying to must be translated by a certified professional.

- Certify Your Copies: Never submit original documents unless explicitly told to. Use a solicitor or notary public to make certified copies of everything.

- Hire Professionals Early: The cost of an initial consultation with an immigration lawyer and an international tax advisor is an investment. It is a fraction of what a mistake could cost.

Don't:

- Underestimate the Timeline: Official processing times are often optimistic. Always build a buffer into your plans, especially for background checks.

- Make Unchangeable Plans: Avoid booking non-refundable flights or signing binding contracts until your visa or citizenship approval is in hand.

- Assume Anything: Rules change. What was true six months ago might not be today. Always double-check requirements on the country's official government website, such as Gov.uk for UK applications.

Your Dual Citizenship Questions, Answered

When you start exploring second passports, many questions arise. It is a complex world, and clear answers are essential. Here, we tackle some of the most common queries from investors.

Can I Have Dual Citizenship with the UK?

Yes. The United Kingdom permits its citizens to hold passports from other countries. If you become a British citizen, you will not be asked to renounce your original nationality.

The real question, however, is whether your home country shares this view. Some nations insist you renounce your existing citizenship when you gain a new one. Always check your country of origin’s rules first.

Which Country Is Easiest to Get Citizenship by Investment?

For investors who value speed and a clear process, a handful of Caribbean nations offer the most straightforward Citizenship by Investment (CBI) programmes. Countries like St Kitts & Nevis, Grenada, and Dominica have run these programmes for years and have highly efficient systems.

Typically, the path involves either buying a government-approved property or making a direct donation to a national development fund. Because the process is so refined, timelines can be as short as a few months. Our guide on the Saint Lucia passport breaks down how one of these popular options works in practice.

Key Takeaway: The term 'easiest' usually means 'fastest and most predictable'. These established CBI programmes have spent years honing their due diligence and application workflows, creating a clear—albeit expensive—route to a second passport for qualified investors.

Does Buying a House in the UK Give You Citizenship?

No. This is one of the biggest misconceptions among international property investors. Simply buying a property in the UK, at any price, does not automatically grant you residency or a passport.

While owning a home can support a visa application—for example, it demonstrates an established base if you are applying for a work or business visa—it is not a direct pathway. You still have to qualify for citizenship through a recognised route, such as long-term residency (naturalisation), ancestry, or close family ties.

At World Property Investor, we provide the data-driven analysis you need to make confident decisions in global real estate. Explore our guides and start building your international portfolio today. Find out more at https://www.worldpropertyinvestor.com.