For the global property investor, the Irish market presents a compelling narrative of resilient growth, underpinned by potent economic fundamentals. However, to appraise the opportunity accurately requires looking beyond national averages. Ireland is not a single, homogenous market but a collection of distinct regional markets, each with its own risk and return profile.

The State of Irish Housing Prices

Ireland remains a key focus for international investors due to a powerful, technology-led economy and favourable demographics. A young, highly educated workforce and consistent net migration create robust, ongoing demand for housing. This demand consistently outstrips the available supply of new homes.

This structural imbalance is the primary engine behind rising property values. Data from Ireland's Central Statistics Office (CSO) confirms a consistent upward price trajectory, a trend that has proven resilient through various economic cycles. For an investor, this points to a market built on solid fundamentals rather than speculative hype.

Key Market Fundamentals

An initial assessment of the market's vital signs reveals a clear picture. The Irish Property Market Key Metrics table below summarises the core data points defining the current investment landscape.

| Metric | National Average | Dublin vs. Regional Context |

|---|---|---|

| Average Price Growth | Consistent year-on-year increases | Growth in Dublin is often slower but from a higher base; regional cities show faster percentage growth. |

| Price Disparity | Significant | Dublin prices remain substantially higher than in established secondary cities like Cork or Galway. |

| Gross Rental Yields | 3-4% in Dublin; 5-7% or more elsewhere | Yields are materially stronger in regional cities and commuter towns due to lower acquisition costs. |

| Housing Supply | Chronic shortfall | Supply constraints are a national issue, impacting both urban and rural markets. |

| Economic Outlook | Strong, FDI-driven | Major multinational employment hubs are a key driver of local housing demand and rental stability. |

These figures highlight a market with broad-based strength but with clear distinctions between the capital and the rest of the country, offering different strategic opportunities.

The Irish property market is a classic case study in supply and demand. Chronic housing shortages, combined with a growing population and strong foreign direct investment, create a 'pressure cooker' environment that supports long-term price growth.

Navigating the Investment Landscape

Astute investors look beyond national averages. Dublin, the established economic powerhouse, behaves like a mature, blue-chip asset. It offers the potential for steady, long-term capital growth, but high entry costs compress rental yields.

In contrast, emerging regional cities and rapidly growing commuter towns represent a different opportunity. Here, lower purchase prices can lead to significantly more attractive rental yields—often exceeding 6%. There is also greater potential for accelerated price growth as infrastructure and employment expand outwards from the capital.

A foundational understanding of the economic drivers and regional opportunities is essential. This data sets the stage for a deeper analysis of the forces shaping returns across Ireland.

The Economic Engine Driving the Market

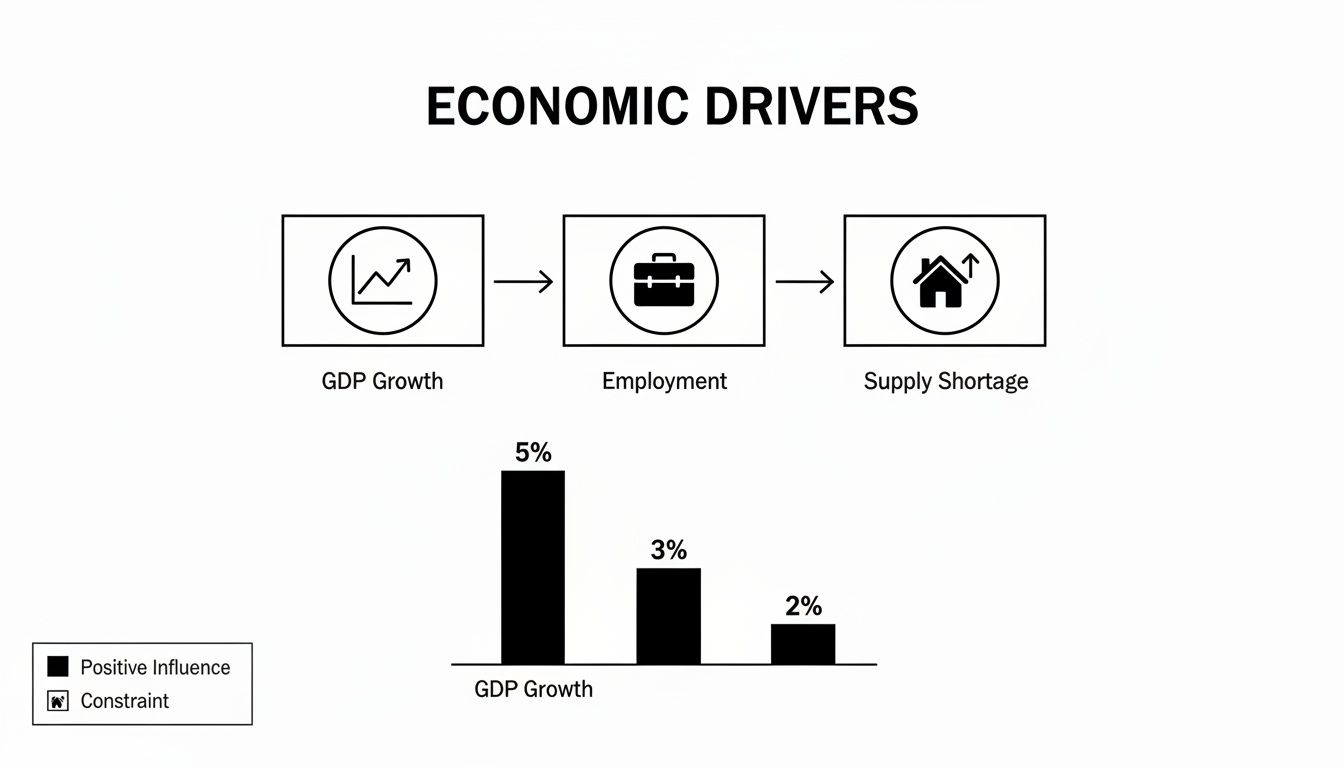

To understand Irish property prices, one must examine the economic engine powering the market. Its performance is the direct result of several powerful, interconnected forces. For any investor appraising long-term value and risk, a firm grasp of these fundamentals is non-negotiable.

The main driver is Ireland's remarkably strong, export-oriented economy. As a European hub for multinational giants in technology, life sciences, and finance, the country attracts high levels of Foreign Direct Investment (FDI). This, in turn, creates a constant flow of well-paid, secure employment, directly fuelling housing demand from both domestic and international workers.

This economic strength translates into impressive employment figures. Official data from bodies like the CSO shows Ireland has consistently maintained one of the lowest unemployment rates in the Eurozone. A high employment rate bolsters consumer confidence and, critically, the ability of households to secure and service a mortgage, which forms a solid foundation for property price growth.

Demand and Demographics

Beyond the robust economy, Ireland's demographic profile adds another layer of upward pressure on house prices. The nation has one of the youngest populations in Europe and benefits from consistent net inward migration. In simple terms, this means new households are constantly being formed, and they all require accommodation.

This demographic tailwind is colliding with a chronic, well-documented housing supply shortage. For years, the number of new homes being built has fallen far short of what is needed to meet demand. This fundamental imbalance is the core reason Irish property prices have proven so resilient.

The Role of Interest Rates

While demand sets the market's general direction, interest rates act as the financial thermostat, controlling affordability and leverage. As a member of the Eurozone, Ireland’s mortgage rates are directly influenced by the monetary policy of the European Central Bank (ECB).

When the ECB held rates at historic lows, borrowing was cheap, enabling buyers to absorb higher prices. Conversely, as the ECB began raising rates to combat inflation, mortgage affordability tightened, which acts as a natural brake on runaway price growth. For investors, ECB policy is a critical indicator to watch; lower rates reduce borrowing costs and can boost capital growth, while higher rates can cool the market and, over time, potentially improve rental yields. You can learn more about assessing returns in our guide on what rental yields are and how to calculate them.

Key Economic Drivers to Monitor

For any prospective investor, monitoring these core indicators provides a clear view of the market's health and potential future direction.

- GDP and Employment Growth: Strong figures signal sustained housing demand. Refer to reports from Ireland’s Central Statistics Office (CSO) and major economic bodies.

- Net Migration and Population Data: Positive trends indicate a growing pool of potential buyers and tenants—a fundamental support for both capital values and rental income.

- Housing Completions vs. Demand: The gap between new homes built and the number needed is the single most important supply-side metric. Government housing reports provide the best data.

- ECB Interest Rate Announcements: ECB policy decisions directly impact mortgage costs and investor sentiment across the entire Eurozone.

By understanding how these elements—a strong economy, population growth, supply shortages, and interest rate policy—interact, an investor can move beyond reacting to headline price changes towards a strategic assessment of long-term market fundamentals.

Dublin vs The Regions: A Tale of Two Markets

Investing in Irish property is not a single national decision. It is a choice between two distinct markets offering different risk-return profiles: the mature, high-cost Dublin market versus the more dynamic, high-yield opportunities emerging in regional hubs. Understanding this distinction is the first step towards a sound investment strategy.

For global investors, it is helpful to think of this in portfolio terms. Dublin is the ‘blue-chip stock’ of Irish property. As the country’s economic engine and home to countless multinational headquarters, it offers a deep, reliable pool of professional tenants. That stability provides a solid foundation for long-term capital appreciation, but it comes at a significant cost.

In contrast, the key regional cities—such as Cork, Galway, and Limerick—are the ‘emerging growth stocks’. These markets offer much lower entry prices, which translates directly into more attractive rental yields. For an investor focused on cash flow, the difference is material.

The Price and Yield Divide

The most obvious disparity is cost. A two-bedroom apartment in a prime Dublin postcode can easily command €450,000 or more. An equivalent property in Cork or Limerick might be acquired for closer to €275,000. This price differential has a powerful and direct impact on your rental yield.

In Dublin, where capital values are high, gross rental yields typically hover in the 3-4% range. While this is a stable return backed by a strong tenant market, it is unexceptional. In cities like Limerick and Waterford, however, it is entirely possible to achieve gross yields of 6-7% or higher, providing a much stronger income stream from day one.

Takeaway: For a €300,000 investment, one might acquire a small one-bedroom apartment in Dublin generating circa €1,500 per month—a 6.0% gross yield. In a regional city, the same capital could secure a three-bedroom house generating €1,600 per month, delivering a 6.4% gross yield with stronger potential for localised growth.

The Ripple Effect and Regional Growth

A key dynamic in the Irish market is the ‘ripple effect’. As prices in Dublin approach affordability ceilings, both homebuyers and investors look outwards for value. This pressure first impacts commuter towns and then extends to the main regional cities.

This trend is not just about affordability. It is also being fuelled by significant infrastructure improvements and a corporate shift towards regional hubs. More companies are establishing major operations in cities like Cork and Galway, bringing a skilled workforce that requires quality rental accommodation. This is creating localised economic ecosystems that are less dependent on Dublin and have their own powerful growth drivers.

Identifying Untapped Opportunities

For the discerning investor, the opportunity lies in identifying regional areas poised for growth before it is fully reflected in prices. The key is to monitor early signals.

Key factors to monitor include:

- Employment Announcements: Watch for news of multinational companies expanding or establishing new offices. A single major employer can transform a local rental market.

- Infrastructure Projects: New motorways, rail links, or university expansions are strong indicators of future demand, making an area more desirable to live and work.

- Local Authority Plans: Reviewing council development plans can reveal future zoning for residential areas, commercial hubs, and public amenities, all of which drive long-term property values.

By focusing on these drivers, you can pinpoint locations that offer the ideal mix of higher rental yields today and strong capital growth potential tomorrow. This strategy allows you to capitalise on the Irish growth story without the high barriers to entry of the Dublin market.

A Comparative Look at Northern Ireland's Property Market

For investors seeking diversification on the island of Ireland, a glance north reveals a distinct and compelling alternative. Northern Ireland's property market operates under UK law and uses Pound Sterling (£), immediately setting it apart as a different asset class within the same small geographic area. This provides a natural hedge against currency fluctuations and exposure to different economic cycles than those driving the Republic.

The most striking difference is price. Entry costs for property in Northern Ireland are significantly lower than in the Republic, especially when compared to Dublin. This lower capital outlay is precisely why investors can often achieve substantially higher gross rental yields.

This affordability makes the market particularly attractive. For perspective, a budget that might only secure a small one-bedroom apartment in a Dublin suburb could potentially acquire a three-bedroom house in a desirable part of Belfast. This fundamentally changes the investment equation for those focused on generating strong, consistent rental income.

Distinct Market Drivers and Performance

While sharing an island, Northern Ireland’s economy has its own unique drivers. Its post-Brexit position, with dual access to both the UK internal market and the EU single market for goods, has created unique economic dynamics. This is bolstered by a burgeoning technology and cybersecurity sector centred in Belfast, which continues to attract skilled professionals and strengthen rental demand.

This environment has supported a resilient housing market. According to ONS data, Northern Ireland has shown impressive growth. For example, the average house price stood at £178,000 at the end of 2023, representing a solid year-on-year increase and outperforming many UK regions. You can explore more about this performance in this detailed market report.

This steady appreciation highlights Northern Ireland’s appeal as a market with solid fundamentals and a proven track record of consistent growth.

Comparing Investment Fundamentals

A direct comparison of the two markets reveals their different strengths. The Republic of Ireland often promises stronger potential for rapid capital appreciation, driven by its high-growth, FDI-led economy and severe supply-demand imbalance. Northern Ireland, on the other hand, stands out for its superior rental yields and a much lower barrier to entry.

Takeaway: Investing in Dublin is analogous to buying a high-growth, low-dividend technology stock. Investing in Belfast is more akin to acquiring a high-dividend utility stock—it provides a more predictable income stream with potential for steady, long-term growth.

For a global investor, a blended portfolio can be a powerful strategy. By holding assets in both jurisdictions, you can balance the high-growth potential of the Republic with the strong income generation and currency diversification offered by the North.

Key Considerations for Northern Ireland

It is crucial to understand the distinct legal and tax framework, which is aligned with the United Kingdom, not the Republic of Ireland.

- Transaction Costs: Stamp Duty Land Tax (SDLT) applies in Northern Ireland, with different rates and thresholds than the Stamp Duty in the Republic.

- Taxation: Rental income is subject to UK income tax, and Capital Gains Tax (CGT) is governed by HMRC, not the Irish Revenue Commissioners.

- Legal Process: The conveyancing process follows the UK system, which can differ in timelines and procedures from the process south of the border.

A combined portfolio across both jurisdictions allows an investor to spread risk and capture opportunities from two related but independent markets. If you are planning a broader strategy, consider our comprehensive guide on property investment in 2025.

Calculating Real Returns on an Irish Buy-to-Let

Appraising headline property prices is one thing; determining if a specific asset will generate a genuine profit is another exercise entirely. This is where an investor moves from market observation to rigorous financial analysis. This due diligence is non-negotiable.

From Gross to Net Rental Yield

The analysis begins with two key metrics: gross yield and net yield.

Gross yield is a quick, 'back-of-the-envelope' calculation: annual rent divided by the property’s purchase price. For instance, a €300,000 property generating €18,000 in annual rent has a gross yield of 6.0%.

However, this figure ignores the real-world costs of ownership. Net yield provides a much truer picture of an investor's actual return on investment (ROI).

Takeaway: The difference between gross and net yield is the difference between a rough estimate and a business plan. A property with a high gross yield can become unprofitable if it has high service charges or requires constant maintenance.

To calculate net yield, you must subtract all annual operating costs from the gross rental income before performing the calculation. These outgoings must be factored into any serious appraisal:

- Letting Agent Fees: Typically 8-12% of monthly rent for full management.

- Landlord Insurance: Essential to protect the asset.

- Annual Service Charges: Common in apartment blocks for communal area maintenance.

- Repairs and Maintenance: Prudent investors budget 5-10% of annual rent for this.

- Local Property Tax (LPT): An annual tax based on the property’s market value.

- Vacancy Periods (Voids): It is wise to budget for at least one month of vacancy per year.

To delve deeper into these calculations, learn how to calculate return on investment for a property in our detailed guide.

Taxation for Non-Resident Landlords

For an overseas investor, understanding Irish tax obligations is critical. In Ireland, rental income is subject to income tax at a standard rate of 20% after deducting all allowable expenses.

A key regulation exists for non-resident landlords: if a tenant pays rent directly to a landlord residing abroad, they are legally required to withhold 20% of the gross rent and remit it to the Irish tax authority, Revenue.

To avoid this complication, most non-resident investors engage a local collection agent, often the same firm managing the property. The agent collects the full rent, handles tax filings on behalf of the landlord, and ensures full compliance.

Finally, upon a future sale of the property, any capital gain is subject to Capital Gains Tax (CGT), currently at 33%. This must be factored into any long-term financial forecast.

A Worked Example: Regional City Apartment

Consider a practical example: a two-bedroom apartment in a regional hub like Cork, purchased for €275,000.

Upfront Costs:

- Purchase Price: €275,000

- Stamp Duty (1%): €2,750

- Legal Fees (approx.): €2,500

- Total Investment Cost: €280,250

Annual Financials:

- Monthly Rent: €1,600 (Annual Income: €19,200)

- Gross Yield: (€19,200 / €280,250) x 100 = 6.85%

A gross yield approaching 7% appears attractive. Now, we apply realistic operating costs.

- Management Fees (10%): €1,920

- Insurance: €400

- Service Charges: €1,500

- Repairs Fund (5%): €960

- Local Property Tax (LPT): €315

- Total Annual Costs: €5,095

Calculating Your True Return:

- Net Annual Rent (before income tax): €19,200 – €5,095 = €14,105

- Net Yield: (€14,105 / €280,250) x 100 = 5.03%

As demonstrated, the appealing 6.85% gross yield translates into a more realistic—but still solid—net yield of just over 5%. This level of detailed analysis is essential for making a confident, data-driven investment decision.

Future Outlook and Strategic Investment Recommendations

Attempting to predict the Irish property market's future with a single forecast is impractical. A more effective approach for the serious investor is to understand the potential scenarios and the key variables that will shape them. This allows for adaptive, informed strategic adjustments.

The path ahead for Irish housing prices depends on three primary factors: the health of the economy, the ECB's interest rate policy, and the government's ability to increase housing supply. The interplay of these forces will create different investment environments.

Scenarios for Irish Housing Prices

Thinking in scenarios allows you to prepare for multiple outcomes.

A "high-growth" scenario would see continued strong multinational investment, keeping employment high and wages rising. If the ECB begins to lower interest rates, this combination would almost certainly fuel further capital appreciation, making growth-focused strategies the clear winner.

Conversely, a "stagnation scenario" could be triggered by global economic instability or a downturn in the technology sector, upon which Ireland is heavily reliant. This would likely soften employment and consumer confidence, leading to flatter price growth. In this environment, high-yielding properties in regional cities would prove far more resilient.

Finally, a "supply-driven correction" could occur if government housing policies successfully accelerate the delivery of new homes, finally narrowing the supply-demand gap. While beneficial for the country, a significant increase in housing stock could cool price growth. Monitoring housing completion data from the CSO is the best way to track this trend.

Strategic Investment Recommendations

Based on current market conditions, a balanced and geographically diversified strategy is the most robust approach.

Our core recommendations are:

- Prioritise Regional Cities: Focus on established secondary cities like Cork, Limerick, and Galway. These hubs exhibit strong local employment growth and are benefiting from major infrastructure investment. They offer a compelling blend of lower entry costs and healthier rental yields compared to Dublin.

- Target Infrastructure Hotspots: Identify properties near new or planned transport links, university expansions, or business parks. These projects are powerful long-term drivers of rental demand and capital growth.

- Balance Your Portfolio: The most prudent strategy involves a strategic mix. A high-value Dublin property can provide stable, long-term capital growth, while a portfolio of higher-yielding properties in regional markets will generate much stronger day-one cash flow. Explore portfolio construction in our guide on property investment in 2025.

Takeaway: The most resilient investment strategies for Ireland involve a blend of assets. Combine the stability of a Dublin property with the superior cash flow from two or three properties in a growing regional city. This diversification protects your portfolio against localised market shifts while capturing growth across the country.

By building a strategy around these principles and monitoring key economic drivers, you can invest with clarity and confidence, prepared to adapt regardless of market direction.

Your Top Questions About Irish Property Investment Answered

Navigating a new property market involves understanding local regulations, risks, and data sources. Here are clear answers to the most common questions from investors considering opportunities in Ireland.

Is It Difficult for Foreigners to Buy Property in Ireland?

No. Ireland has one of the most open property markets in Europe for international buyers.

There are no restrictions on foreign nationals purchasing residential property. The legal process is identical for an Irish citizen and a non-EU national. You simply require a qualified local solicitor to manage the conveyancing.

It is important to note that property ownership does not confer residency rights in Ireland. Residency is a separate immigration matter. The purchase process itself, however, is transparent and well-established.

What Are the Biggest Risks to Consider?

Beyond standard property-specific risks, the two most significant macro factors to monitor in Ireland are interest rate policy and housing supply.

As a Eurozone member, Ireland's mortgage rates are heavily influenced by the European Central Bank (ECB). Sharp increases in the ECB’s base rate will directly impact borrowing costs and can cool price growth.

The other major variable is the government's ability to deliver new housing. The current supply shortage is a key driver of high prices and rents. Should construction suddenly accelerate and meet demand, it could soften the market, particularly for new-build properties in certain areas.

Takeaway: For investors in the Irish market, the most significant financial risks are often macroeconomic, not local. Monitoring ECB policy and Irish government housing reports is as crucial as analysing the financials of a specific property.

Where Can I Find Reliable Data on Irish Housing Prices?

For trustworthy, impartial data, it is best to rely on official and reputable sources.

The Central Statistics Office (CSO) publishes the official Residential Property Price Index. This is the definitive measure for tracking actual sale prices and is the most authoritative source available.

Another excellent resource is the quarterly Daft.ie House Price Report. It provides highly detailed analysis based on asking prices for every county in Ireland, offering granular market insights. Using these two sources ensures your decisions are based on robust data, not market sentiment.

At World Property Investor, we provide the in-depth analysis and data you need to invest with confidence. Explore our global property guides at https://www.worldpropertyinvestor.com.