Switzerland isn't merely expensive. It's structurally expensive, and that distinction matters to property investors.

According to Numbeo's Switzerland cost of living data, total living costs are 63.9% higher than in the United States, while rent is 32.7% higher. For an occupier, that can look like a warning. For an investor, it signals something more useful: a market where housing sits inside a broader high-cost system supported by strong local incomes, disciplined tenant behaviour, and limited tolerance for speculative pricing mistakes.

That's why living costs in Switzerland shouldn't be treated as background colour in an expat guide. They're a core market input. They influence who can afford to rent, where they cluster, how resilient demand remains across economic cycles, and what kind of property fits the local tenant base.

Understanding the Swiss Investment Case

Most investors first encounter Switzerland through a sticker-shock lens. They see high rents, high grocery bills, and expensive city life, then assume the market must be difficult to underwrite. That's only half right.

The more important reading is that high living costs in Switzerland help filter the tenant pool. In practice, that often means demand is concentrated among well-paid professionals, internationally mobile executives, skilled domestic workers, and households that budget around fixed obligations rather than impulse spending. For a landlord, that usually creates a very different risk profile from a lower-cost market where rent competes with more volatile discretionary expenses.

Why expensive can also mean defensive

Swiss tenants don't make housing decisions in isolation. They make them within a system where several major outgoings are effectively built into normal life. That tends to reward stable employment, careful budgeting, and longer holding periods from investors.

For global buyers comparing markets, the Swiss case often sits at the opposite end of the spectrum from yield-led emerging markets. You're generally not screening for the highest headline income return. You're screening for consistency, tenant quality, and the chance of owning in locations where demand remains durable because economic access is selective.

Investor lens: High living costs can reduce market breadth, but they can also improve tenant depth.

That's why Switzerland belongs in the same strategic conversation as other defensive allocation markets. If you're comparing stable jurisdictions before deciding where to buy investment property, Swiss affordability pressures are part of the investment thesis, not just a consumer concern.

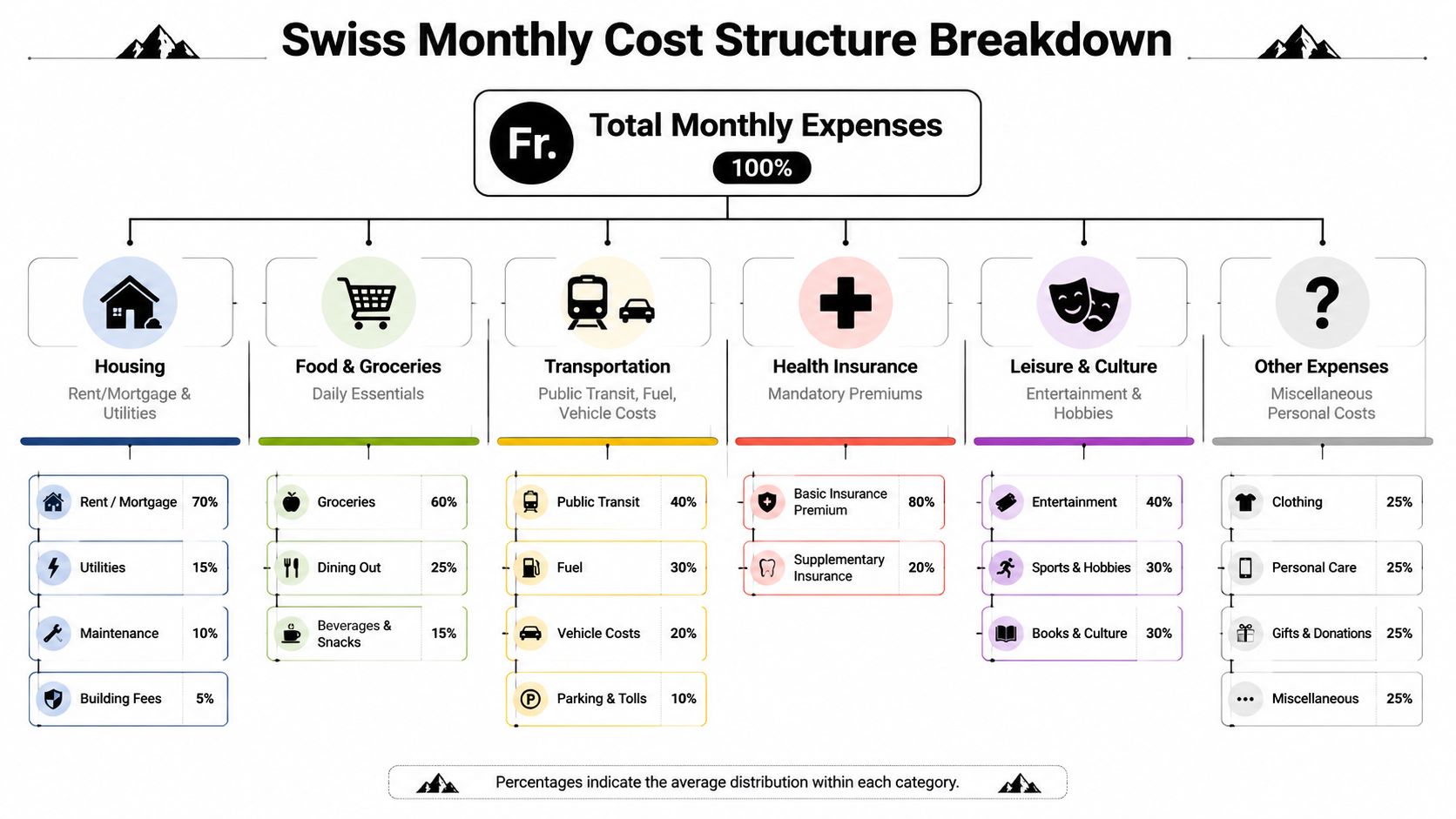

A Breakdown of the Swiss Cost Structure

Switzerland's cost burden extends well beyond headline rent. For property investors, that matters because tenant resilience depends on the full budget stack, not just on salary relative to lease payments.

As noted earlier, national cost data places Switzerland well above many peer markets on everyday spending as well as housing. The investment implication is straightforward. A tenant in Zurich or Geneva is not only paying more for an apartment. That tenant is also operating in a system where groceries, insurance, transport, and routine services consume a larger share of monthly income than in lower-cost European markets.

The fixed-cost problem for tenants

This is the core underwriting issue.

In Switzerland, several major expenses behave as fixed or semi-fixed obligations. Rent is the largest item, but health insurance, transport needs, utilities, and recurring administrative costs also limit how much a household can cut when income is pressured. In practical terms, that produces a narrower affordability buffer than headline salaries can suggest.

For investors, this changes how rental demand should be read. High wages do support high rents, but they do not automatically create broad tenant flexibility. A tenant who can comfortably absorb Swiss fixed costs is often a stronger credit profile. A tenant who is only marginally above the threshold can become fragile quickly because the rest of the household budget has limited room to adjust.

A useful way to assess the structure is to separate spending into four layers:

- Housing costs: The primary budget anchor, especially in the largest employment centres.

- Everyday consumption: Food and household goods remain expensive enough to affect savings capacity and rent tolerance.

- Required recurring charges: Insurance and administrative obligations reduce discretionary room.

- Optional lifestyle spending: This can be cut, but it is usually not large enough to offset a structurally expensive monthly base.

That pattern helps explain why Swiss rental markets often favour tenants with stable employment, predictable income growth, and lower debt stress. It also helps explain why smaller, well-located units can outperform larger stock on a risk-adjusted basis. One professional tenant with a strong income often fits the Swiss cost structure better than a household whose non-rent spending rises across several dependants.

Why this matters to property selection

The key question is not whether Swiss rents are high. It is whether a specific asset fits the budget mechanics of the tenant cohort it targets.

A central one-bed near major employment nodes often aligns with the finances of internationally mobile professionals, pharmaceutical staff, private banking employees, and senior service-sector renters. Those tenants may accept high nominal rent because they are optimizing commute time and job access inside an already expensive system. A larger family apartment requires different underwriting. Household income may be higher, but so are healthcare, transport, childcare, and food costs. That can compress the margin available for rent and lengthen vacancy risk if pricing is pushed too far.

For investors building tenant affordability models, guides on mastering your household spending can help translate broad expense categories into realistic monthly cash flow assumptions. The same budgeting logic applies directly to rent-setting and unit selection.

The non-obvious conclusion is that Switzerland's high living costs can support asset stability while capping yield expansion. They narrow the pool of viable tenants, but they also concentrate demand among households with stronger earning power and clearer budgeting discipline. That is one reason Swiss residential property often behaves more like a capital-preservation allocation than a yield-maximisation trade.

A useful comparison is other high-cost Northern European markets. Reviewing Norway's living cost profile helps frame whether Switzerland's cost structure is expensive or unusually restrictive for renters. Switzerland tends to sit closer to the restrictive end, which is exactly why tenant selection and micro-location matter so much.

City and Canton Investment Analysis

National averages don't tell the whole story. In Switzerland, the investment case changes materially by city.

Instarem's market guide gives a useful city snapshot. It lists average after-tax monthly salary at CHF 5,808 in Zurich, CHF 5,774 in Geneva, CHF 6,641 in Basel, and CHF 5,168 in Lausanne, alongside single-person living costs of CHF 2,993, CHF 2,892, CHF 2,497, and CHF 2,397 respectively, based on its Switzerland cost overview. For investors, the implication is immediate. Tenant affordability is not a national concept. It's local.

Comparing the main urban markets

| City | Avg. Monthly Salary (After Tax) | Est. Monthly Cost (Excl. Rent) | Avg. 1-Bed City Centre Rent | Remaining Disposable Income |

|---|---|---|---|---|

| Zurich | CHF 5,808 | CHF 2,993 | Commonly quoted at CHF 1,500–3,000 per month in Switzerland | Salary minus living costs leaves a meaningful but pressured margin before rent at the upper end |

| Geneva | CHF 5,774 | CHF 2,892 | Commonly quoted at CHF 1,500–3,000 per month in Switzerland | Similar to Zurich, with tight affordability for prime central stock |

| Basel | CHF 6,641 | CHF 2,497 | Commonly quoted at CHF 1,500–3,000 per month in Switzerland | Stronger income-to-cost balance than Zurich or Geneva |

| Lausanne | CHF 5,168 | CHF 2,397 | Commonly quoted at CHF 1,500–3,000 per month in Switzerland | Moderate budget balance, but rent sensitivity remains high |

The rent column needs careful reading. The available verified data supports a Swiss city-centre one-bed range of CHF 1,500 to CHF 3,000 per month, but doesn't break that out by city in a consistent way. Even so, the salary and non-rent cost figures are enough to show why some cities create more breathing room than others.

What the numbers imply for strategy

Zurich suits investors targeting high-income professional tenants, but that doesn't automatically make it the best affordability market. A tenant earning Zurich-level income still faces substantial monthly cost pressure before rent is paid.

Basel stands out differently. Based on the same city guide, it combines the highest listed after-tax salary with the lowest listed single-person cost among the named cities except Lausanne's slight difference in costs against a much lower salary base. For a landlord, that can translate into a tenant base with more residual income and potentially less rent stress.

Practical rule: The best Swiss city for rent security isn't always the one with the highest salary. It's often the one where salary outruns non-rent costs by the widest margin.

For investors used to a market like London, where affordability and yield often pull in opposite directions, this is a useful comparison point. Our guide to rental yield in London shows how city-level economics can alter the quality of returns even when headline rents look strong.

The Swiss Housing Market Explained

Swiss housing costs do more than raise a tenant's monthly budget. They shape who rents, how long they stay, and what kind of property income an investor can realistically expect.

City-centre apartment rents sit at a level that keeps renting central to urban housing demand, especially in markets such as Zurich, Geneva, and Basel, as noted earlier. For investors, that matters because high living costs filter the tenant base. Households that remain in these markets tend to have stronger incomes, stable employment, and a clear reason to pay for location, transport access, and time savings.

Why renting remains structurally important

Switzerland's rental market works as a long-term tenure model, not merely as a waiting room for ownership. That distinction changes the investment case.

In markets where buying is the expected end point, landlords often face higher churn and more tenant decisions driven by short-term convenience. Swiss urban renters are more likely to choose for durability. Commute quality, school catchments, building condition, energy efficiency, and lease stability carry real weight. An asset that performs well in this environment usually wins through consistent management and durable location value rather than aggressive repositioning.

That has a direct effect on income quality. Longer holding periods by tenants can reduce reletting friction, lower vacancy risk between occupiers, and make cash flow less dependent on constant remarketing.

What high housing costs signal to investors

High rents in Switzerland usually indicate a market with constrained access and disciplined demand, not an easy yield story.

Several features matter at once:

- Demand is concentrated in a small number of urban economies. The deepest renter demand sits in cities with strong professional employment and international business activity.

- Micro-location matters more than headline city averages. Proximity to rail links, employment clusters, and established residential districts supports pricing power.

- Regulation affects who can buy and what they can buy. Foreign investors need to assess legal structure, property type, and local rules before underwriting any residential acquisition.

- Tenant standards are high. In an expensive market, occupiers expect quality maintenance, efficient layouts, and professional communication from landlords.

These factors help explain why Swiss residential property often attracts capital focused on preservation and stability rather than headline income. Investors comparing this profile with other mature markets should pair local housing analysis with a broader property market forecast for 2025.

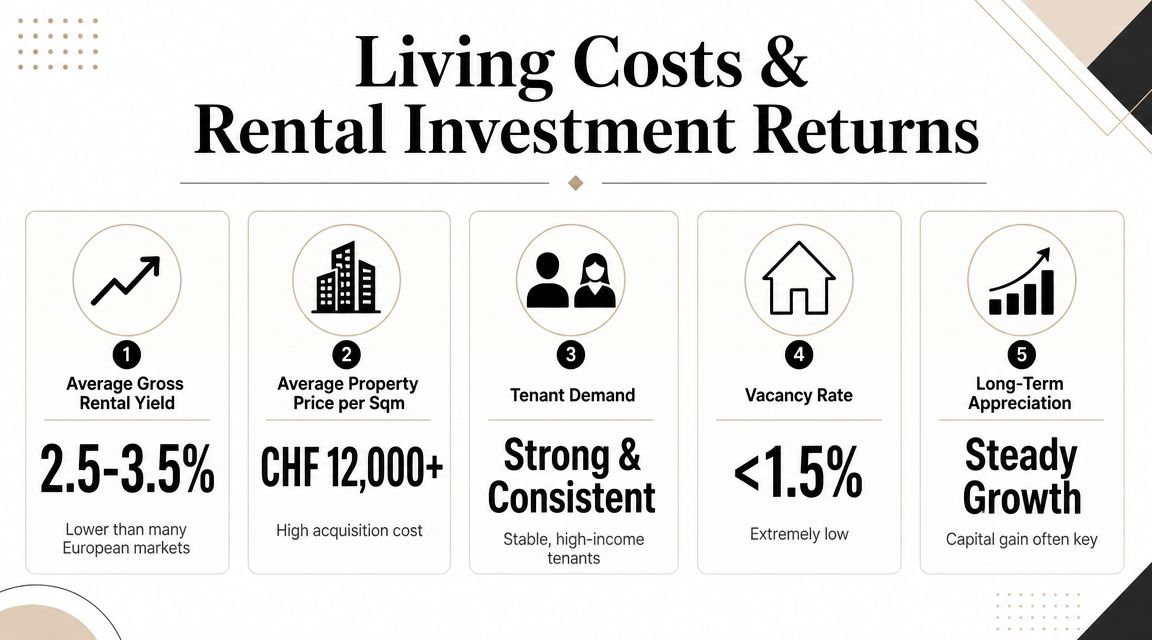

Yield still matters, but it needs the right frame. A unit with modest gross income on paper can still compare well on a risk-adjusted basis if tenant retention is strong and vacancy is low. That is why understanding rental yield formulas is useful before judging Swiss assets against higher-yield jurisdictions with weaker tenant resilience.

A concise visual overview helps if you're assessing the rental culture and urban context from abroad:

How Living Costs Shape Rental Yields and Returns

Switzerland becomes clearer. The return profile is driven as much by cost structure as by rent collection.

When households live in a high-cost system supported by high salaries, landlords often get a tenant pool that treats housing as a priority expense. That doesn't eliminate risk, but it can change its character. In lower-cost, higher-yield markets, rent can be one of several competing monthly obligations. In Switzerland, the budget is often built around fixed commitments first.

The investor's real return question

Swiss property rarely appeals on a simple yield-chasing basis. It tends to attract investors who care about capital preservation, tenant resilience, and low drama in the income stream.

That's why yield analysis needs context. Gross yield is only one part of the picture, and anyone comparing markets should understand the mechanics before making simplistic side-by-side decisions. A good refresher on understanding rental yield formulas is useful here because Swiss assets can look modest on paper if you ignore tenant quality and risk-adjusted income stability.

Why fixed costs can support rent security

One of the more subtle points in the Swiss market is that many large expenses are non-discretionary. That can make household spending patterns more predictable than in markets where a larger share of the budget is optional.

The implication for landlords is straightforward:

- Budget discipline tends to be higher because tenants have to plan around recurring obligations.

- Rental decisions are more selective because location mistakes are costly.

- Good units can hold demand well when they suit the income bracket they're targeting.

- Poorly targeted units can underperform because Swiss tenants don't have much room for affordability errors.

A Swiss rental asset is often less about stretching for maximum income and more about owning a dependable slice of a very disciplined housing system.

That's also why broad yield comparisons can be misleading. A market with a higher headline yield may still produce more volatility, weaker tenant quality, or longer empty periods. Switzerland tends to sit closer to the defensive end of the spectrum. Investors who want a primer on how to frame that trade-off can compare approaches in this guide to what rental yields mean in practice.

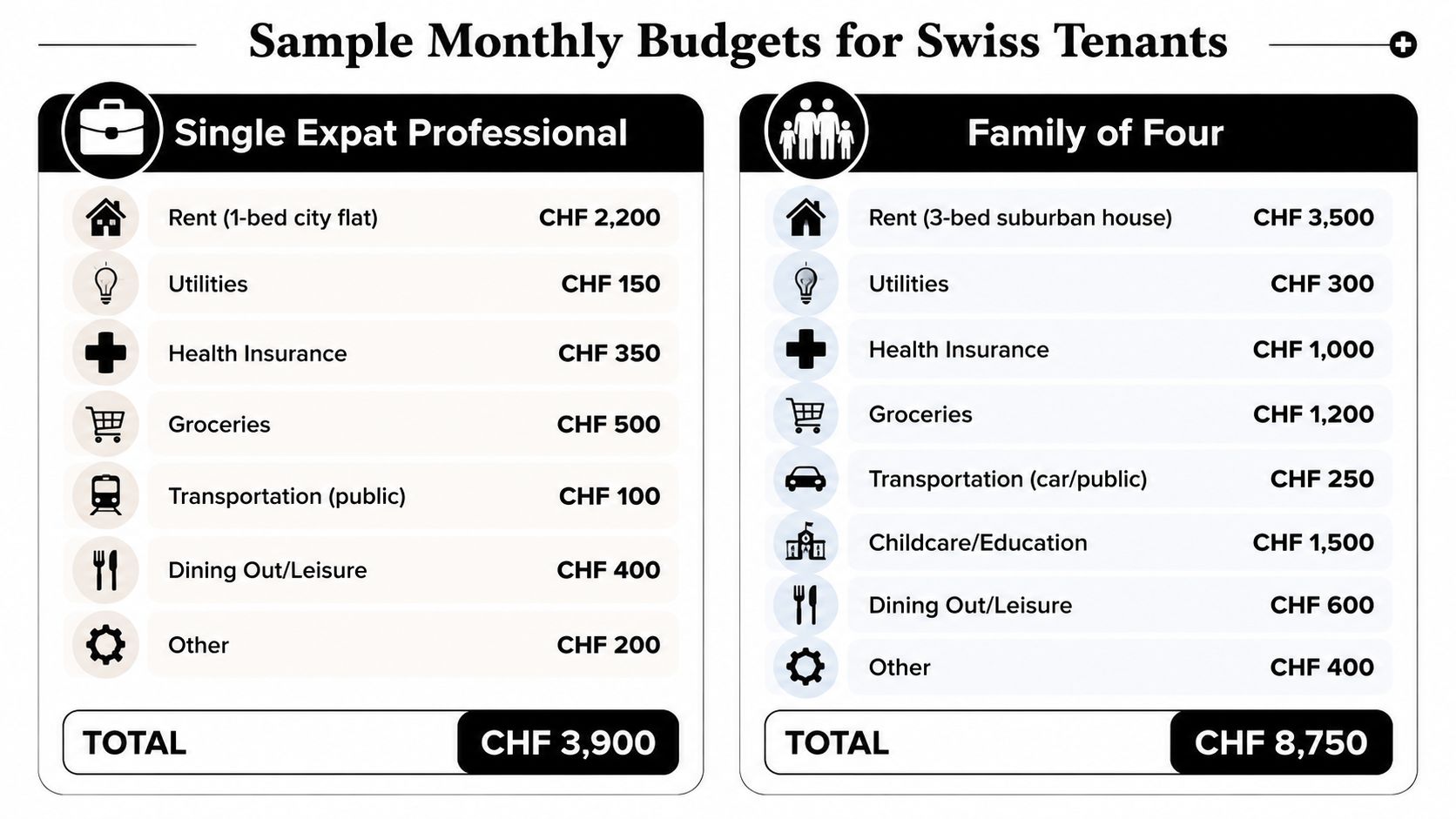

Sample Budgets for Typical Swiss Tenants

Household type matters as much as location in Switzerland.

Jetpac's Switzerland cost guide notes that a single person might need CHF 2,500 to CHF 3,500 per month for comfortable living, while a family of four could require CHF 6,500 to CHF 7,500+, based on its budget discussion for Swiss renters. For investors, that's more than a budgeting fact. It's a tenant segmentation tool.

Single expat professional

The classic Swiss urban tenant is a single professional working in finance, pharmaceuticals, consulting, technology, or a multinational corporate role. This renter often prioritises proximity to transport, office districts, and international amenities.

The key investment implication is that this tenant can usually absorb a higher rent if the flat saves time and fits an efficient weekday routine. But they're also exacting. They'll compare building quality, energy performance, layout, and location with care because the rest of their monthly budget is already expensive.

A landlord targeting this segment should prioritise:

- Walkable urban locations: Time savings often justify higher rent.

- Efficient one-bed layouts: Dead space is costly in premium markets.

- Professional presentation: Finish quality matters more when rents are already high.

Family household

A family of four behaves differently. Housing still matters, but so do room count, school access, transport links, and neighbourhood stability. The total budget is much larger, and pressure rises quickly when multiple fixed costs stack up.

That makes family-oriented assets potentially attractive in the right suburb or secondary urban area. The rent may be lower than a prime city-centre unit on a per-square-metre basis, but the tenancy can be more durable if the property matches long-term household needs.

Here's the important distinction:

| Tenant type | Main pressure point | What they value most | Investor implication |

|---|---|---|---|

| Single professional | Time and convenience | Centrality, quality, low friction | Prime one-beds can fit this profile well |

| Family of four | Total monthly budget load | Space, schools, stability | Suburban or larger units may support longer stays |

Portfolio insight: In Switzerland, tenant profile often determines property performance more than the property category alone.

That's why living costs in Switzerland should push investors away from generic assumptions. A city-centre studio and a suburban family flat don't only serve different budgets. They serve different forms of financial behaviour.

Strategic Takeaways for Property Investors in 2026

Swiss households carry a high base level of recurring expenses. For property investors, that matters less as a consumer talking point than as a market mechanism. When health insurance, transport, childcare, and local taxes consume a meaningful share of monthly income, tenant demand becomes more selective, location premiums become more rational, and assets that fit real budget constraints tend to produce steadier occupancy.

That dynamic supports a specific investment case. Switzerland usually rewards investors seeking capital preservation, disciplined underwriting, and durable tenancy rather than aggressive yield expansion. High living costs act as a filter on demand. They concentrate renter interest around properties that reduce total household friction, whether through commuting efficiency, practical layouts, or access to services that lower daily time and cash costs.

The result is a market where tenant quality and asset suitability often matter more than headline rent levels alone. A unit that looks expensive on a gross basis can still be competitively positioned if it lowers the tenant's wider cost burden. By contrast, a cheaper property in the wrong micro-location can face weaker pricing power because Swiss renters evaluate housing as one component of a tightly managed monthly budget.

A disciplined Swiss acquisition process should include:

- Legal and cantonal review: Foreign ownership rules, permit structures, and local administrative practice can change what is investable.

- Tenant-budget underwriting: Assess the likely occupier's full cost stack, not just rent-to-income in isolation.

- Micro-market selection: Zurich, Geneva, Basel, and Lausanne serve different employer bases, income bands, and tenant retention patterns.

- Return discipline: Underwrite for stability, lower vacancy risk, and slower but more dependable rent growth.

This is why Switzerland works well as a portfolio stabiliser. It serves a different role from higher-yield markets. Investors are often accepting lower initial income in exchange for stronger tenant resilience, lower turnover risk, and an operating environment where abrupt market dislocation is less common.

For cross-border buyers, financing structure should be assessed alongside asset selection. Investors comparing Swiss property with nearby European opportunities may also find specialist resources such as Expat mortgage solutions for France useful when evaluating how lenders treat internationally mobile borrowers and foreign income profiles.

The strategic conclusion is straightforward. In Switzerland, living costs are not background noise around residential property. They help determine who can rent, where they stay longest, which units hold pricing power, and why the market remains comparatively stable over time.

If you're comparing Switzerland with other global property markets, World Property Investor offers country and city guides, rental yield analysis, and market-by-market research to help you assess where stability, income, and long-term value are most likely to align.