Most advice on Malta nationality by investment is out of date. Many guides still describe a live, price-based passport route. That's no longer the right starting point for investors.

If you're evaluating Malta in 2026, the practical question isn't “How much does a Maltese passport cost?” It's whether Malta still offers an investment-linked route at all, and if so, whether that route is citizenship, residency, or merely a property commitment tied to a longer legal process.

That distinction changes everything for capital planning, property selection, liquidity, and tax structuring. Investors who miss it often compare Malta against Portugal, Greece, Spain, or even UK relocation strategies on the wrong basis. If you want a wider view of how these routes fit into broader mobility planning, start with this guide to investor visas and residency routes.

Understanding Malta's Investment Migration Landscape in 2026

Search demand still treats Malta as though it offers a straightforward citizenship-for-capital model. That framing is now misleading. Malta's former structured investor-citizenship route has ended, and current planning has to separate merit-based naturalisation from investment-linked residence.

For property investors, that means the old “buy property, pay the contribution, get the passport” narrative no longer works as a reliable roadmap. The market has shifted from a defined investor-citizenship framework to a more selective environment where residence remains relevant, but citizenship is no longer a fixed-price output.

What investors usually get wrong

The first mistake is assuming residency and citizenship are interchangeable. They aren't. Malta still has an investment-linked residence pathway that matters to internationally mobile families, but that is not the same as a guaranteed citizenship programme.

The second mistake is underestimating the role of property. In Malta, real estate has never been an incidental detail. It has been central to eligibility, holding periods, and total cost. That makes this a property strategy as much as an immigration one.

Malta should be analysed as a capital-allocation decision with an immigration overlay, not as a simple passport product.

Why this matters for serious buyers

If you're comparing Malta with other European options, the key issue isn't headline marketing. It's legal status. A route can look attractive on paper yet become unsuitable once you factor in discretion, residency clocks, illiquid property exposure, and the absence of a guaranteed citizenship outcome.

That's why Malta now sits in a different category from the one many intermediaries still market online. It remains relevant, but for a narrower type of investor. Usually, that's someone comfortable with residency first, property commitment second, and a far less mechanical path to nationality than the phrase “Malta nationality by investment” suggests.

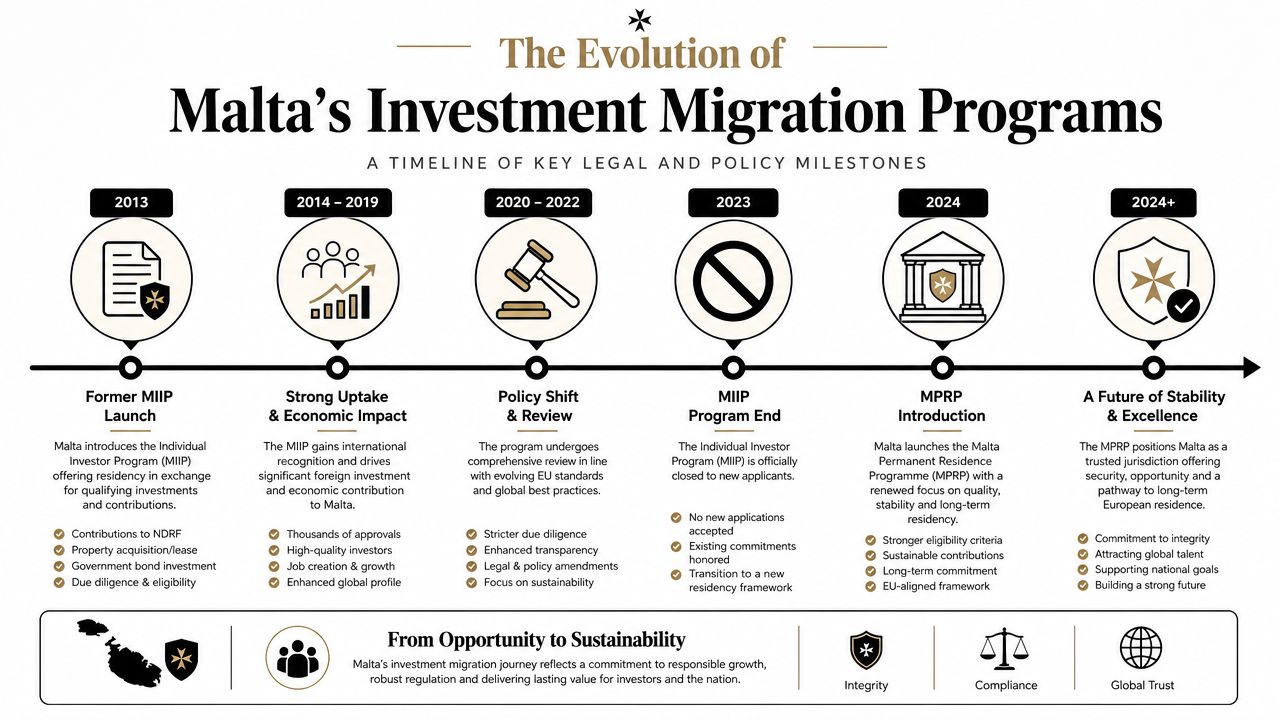

The End of an Era for Direct Citizenship by Investment

Malta did have a structured investor-citizenship regime. That's the regime most older articles still describe. But the legal reality has moved on.

A major point that many guides still miss is that Malta has ended the structured investor-citizenship programme and now uses a merit-based naturalisation framework, while the Malta Permanent Residence Programme remains a residency route, not citizenship, as outlined by CSB Group's update on Malta citizenship by investment. For UK-based readers in particular, that matters because the legal pathway has changed, and the merit route has no fixed price list or guaranteed approval.

What replaced the old model

The old logic was transactional. The modern logic is discretionary. Following the 2025 legal changes, Malta shifted from a fixed-price investment model to merit-based naturalisation, so there is now no guaranteed citizenship outcome tied solely to capital deployment, according to Andersen's analysis of Malta's citizenship framework.

That doesn't mean investment is irrelevant. It means capital alone no longer gives investors a predictable legal result. Applicants now face discretionary assessment based on exceptional merit, national interest, and full due diligence. In practice, that makes the route more suitable for applicants with a demonstrable business, scientific, cultural, or philanthropic profile.

Why the old language is now dangerous

Calling Malta a live “citizenship by investment” market creates planning errors. It encourages investors to budget for a threshold rather than prepare for a case-by-case review. It also leads buyers to over-focus on contribution size and under-focus on legal uncertainty.

For advisers, the sharper way to describe Malta today is this:

- Citizenship route. No longer a structured, guaranteed investor scheme.

- Residence route. Still relevant, still investment-linked, still property-sensitive.

- Investor suitability. Stronger for applicants who can show broader value than passive capital alone.

If you're benchmarking this against other passport-led jurisdictions, it helps to compare it with the broader market for citizenship by investment programmes. Malta no longer sits comfortably in that same box.

The search term survived. The legal product didn't.

The Investor Gateway Malta Permanent Residence Programme

For most property-led investors, the workable Maltese route is now the Malta Permanent Residence Programme, commonly shortened to MPRP. It's the nearest thing Malta still offers to an investment-linked entry point.

That matters because many searches for Malta nationality by investment are really searches for mobility, optionality, and a base in an EU jurisdiction. The MPRP addresses some of those goals, but it does so through permanent residency, not immediate citizenship.

Why the MPRP is the route that matters

The MPRP is relevant because it preserves a concrete legal pathway where the citizenship side has become discretionary. Investors can still establish a long-term foothold in Malta through a programme tied to property and qualifying financial commitments.

For buyers who want practical relocation options, family planning flexibility, or Schengen-linked mobility, that makes the MPRP the main programme worth analysing. Anyone still searching for a simple passport package is solving for a route that Malta no longer offers in structured form.

How to think about it as an investor

This is best viewed as a residency platform. You're buying legal presence and optionality, not a guaranteed nationality outcome. That changes how you should assess the deal.

A useful investor lens is:

| Decision area | What to focus on |

|---|---|

| Legal outcome | Permanent residency rather than automatic citizenship |

| Capital structure | Property plus government-linked payments and holding commitments |

| Portfolio fit | Whether Maltese property exposure suits your liquidity needs |

| Strategic use | Relocation, mobility planning, family residence, and long-term optionality |

The MPRP often gets bundled into “golden visa” discussions, but that can oversimplify the planning. If you want a fuller breakdown of the current route, this overview of the Malta golden visa and residency framework is a useful companion.

Where property investors should be cautious

Property is not just a qualifying asset here. It's part of the programme's structure. That means your real estate decision has to work on its own merits as far as possible, not just as an immigration checkbox.

A weak property choice can turn a viable residency strategy into an expensive, illiquid obligation. That's especially true if your original intention was citizenship and you now have to reframe Malta as a long-term residence play instead.

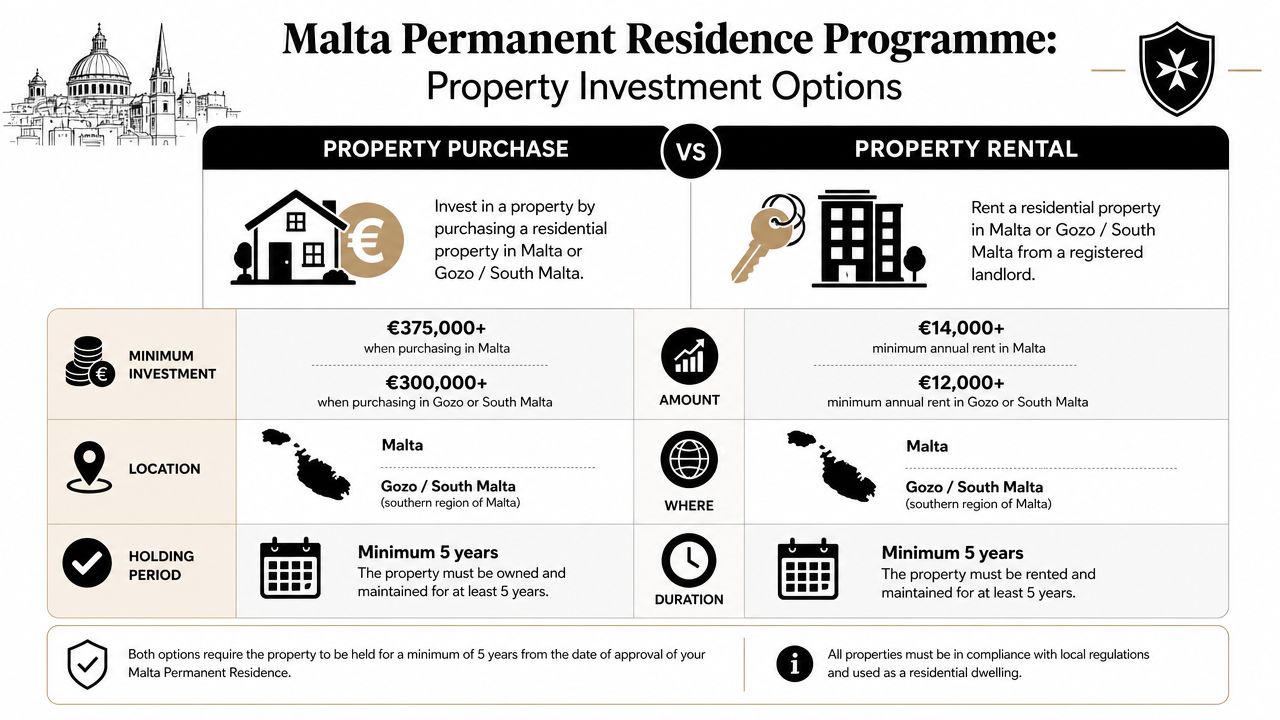

The Property Investment Requirement Explained

The property requirement is where Malta becomes tangible. It's also where many guides blur old citizenship rules with current residence planning.

For UK-facing planning, the closest investment-linked Maltese option remains the residence or permanent residency route. Investors must either buy residential property for at least €700,000 and hold it for five years, or rent for at least €16,000 per year over the same period, alongside a government contribution of €600,000 after 36 months of residency or €750,000 after 12 months, plus a €10,000 donation, according to Wise's breakdown of Malta citizenship and residency costs.

Buying versus renting

The purchase route appeals to investors who want asset ownership. The rental route appeals to those who want to reduce capital tied up in one market. Neither is automatically better. The right choice depends on your time horizon and tolerance for illiquidity.

Here's the practical comparison:

| Property path | Core requirement | Main investor implication |

|---|---|---|

| Purchase | Buy for at least €700,000 and hold for five years | Higher capital lock-up, but ownership may suit buyers who want a physical base |

| Rental | Lease for at least €16,000 per year for five years | Lower upfront capital tied to property, but no owned asset at the end |

The real issue is capital lock-up

The headline thresholds matter, but the holding period matters more. Five years is long enough for market conditions, personal plans, and liquidity needs to change. That's why the Maltese property element should never be treated as a passive formality.

The technical implication is a capital-lockup structure that combines illiquid property exposure with a residency clock. For high-net-worth applicants, the important due diligence questions are usually these:

- Exit flexibility. How easy will it be to sell or unwind after the holding period?

- Use case. Will the property serve as a real residence, a family base, or only a compliance asset?

- Opportunity cost. What else could this capital do in another market or structure?

- Mismatch risk. Does the property choice still make sense if your citizenship outcome is uncertain?

Practical rule: If the property wouldn't make sense without the residency benefit, scrutinise it twice as hard.

Which route tends to suit which investor

The buy option often suits investors who already want Malta exposure for lifestyle or family reasons. The rental option often suits those who prioritise flexibility and don't want to concentrate more capital in one residential asset than necessary.

Neither route is “cheap”. Even the rental path involves a multi-year commitment. Malta's appeal lies in legal stability and strategic residence planning, not in low-cost entry.

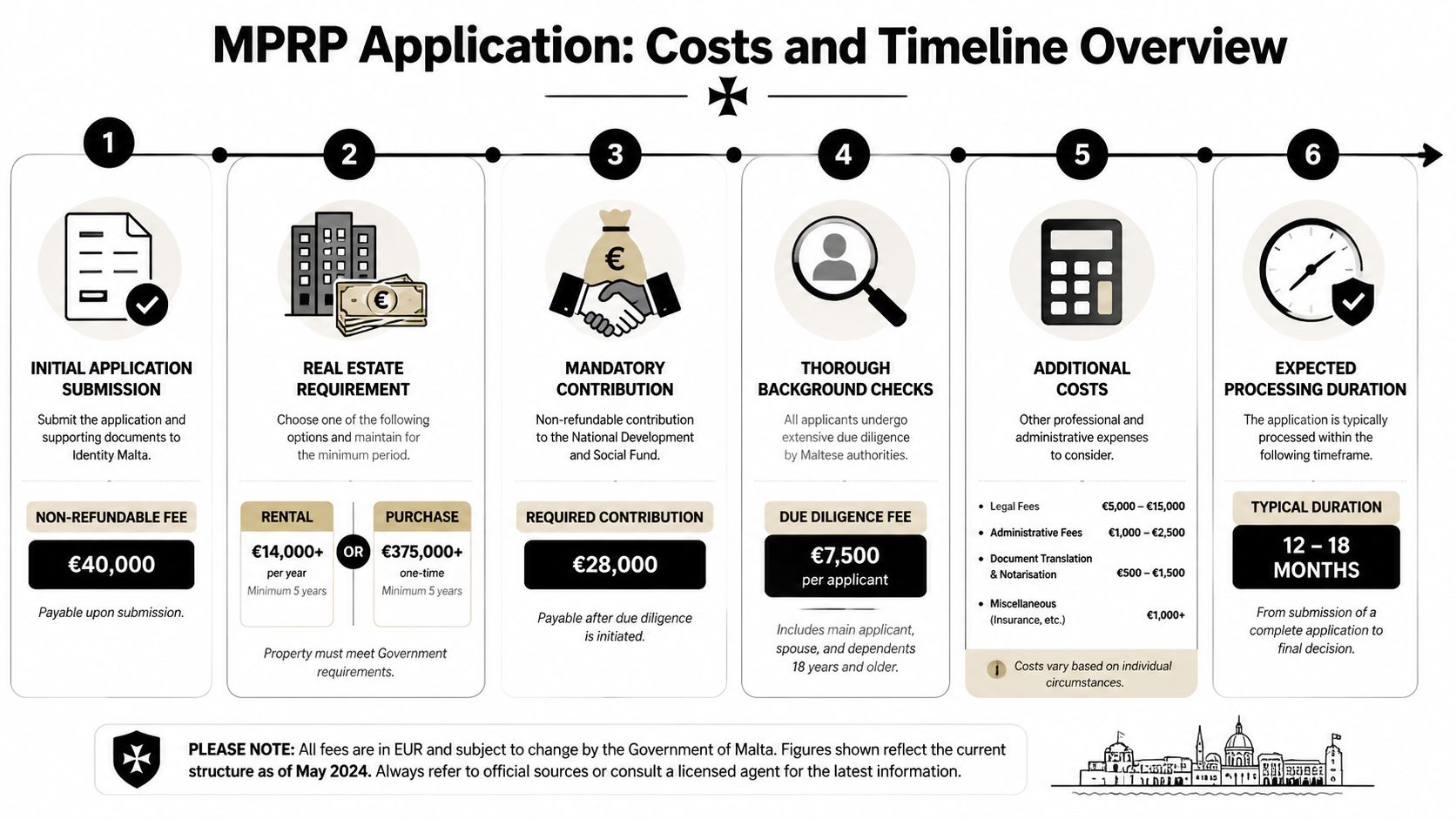

Calculating the Full Cost and Application Timeline

The full Maltese picture only becomes clear when you combine property, contribution, timing, and the legal evolution of the route.

Malta's investment-linked citizenship route was formally restructured in 2020, when the government revamped its framework into a citizenship by naturalisation model for exceptional services. The U.S. State Department's 2025 Investment Climate Statement for Malta still treats that 2020 revamp as the key milestone shaping the modern regime. Under the commonly cited rules, applicants could qualify after either 36 months of legal residence with a €600,000 contribution or 12 months with a €750,000 contribution, plus a €700,000 property purchase or a €16,000 annual lease held for five years, as set out in the U.S. State Department's Malta investment climate statement.

A visual summary helps before you start modelling the route:

The minimum financial architecture

Using the verified thresholds, the cost base has several moving parts.

Government contribution

The lower contribution applies after the longer residence period. The higher contribution applies to the faster track.Property commitment

You either buy qualifying residential property or lease qualifying residential property for the required holding period.Donation

A €10,000 donation forms part of the capital stack under the commonly cited rules in the verified data above.

This is why Malta was never a low-cost passport route. Even before the later legal changes, it required significant capital deployment and property commitment.

What the timeline means in practice

The core timeline choice was between a 12-month and 36-month legal residence period. Investors often focus on the headline contribution gap, but the more important distinction is behavioural.

The faster route reduces time uncertainty but raises the direct contribution. The longer route lowers that contribution but extends your residency clock. That means more time managing compliance, documentation, and personal planning around the process.

A practical way to think about it is:

| Timeline choice | Trade-off |

|---|---|

| 12 months | Higher payment for a shorter route |

| 36 months | Lower payment, but longer exposure to process risk and delay |

The process investors should expect

Even without inventing a rigid processing calendar, the sequence is clear:

- Initial eligibility review. Advisers examine source of funds, personal profile, and route suitability.

- Document preparation. This usually becomes the first friction point, especially for cross-border families with layered holdings.

- Residence period. The residency clock is not cosmetic. It is central to the framework.

- Property compliance. The property must remain compliant for the required holding period.

- Final review and issuance decision. Legal structure matters most at this stage, especially now that Malta no longer offers a purely mechanical citizenship result.

The useful conclusion isn't just that Malta costs a lot. It's that timing and liquidity are intertwined. A lower contribution can be offset by a longer planning burden. A faster route can reduce waiting but raise direct outlay.

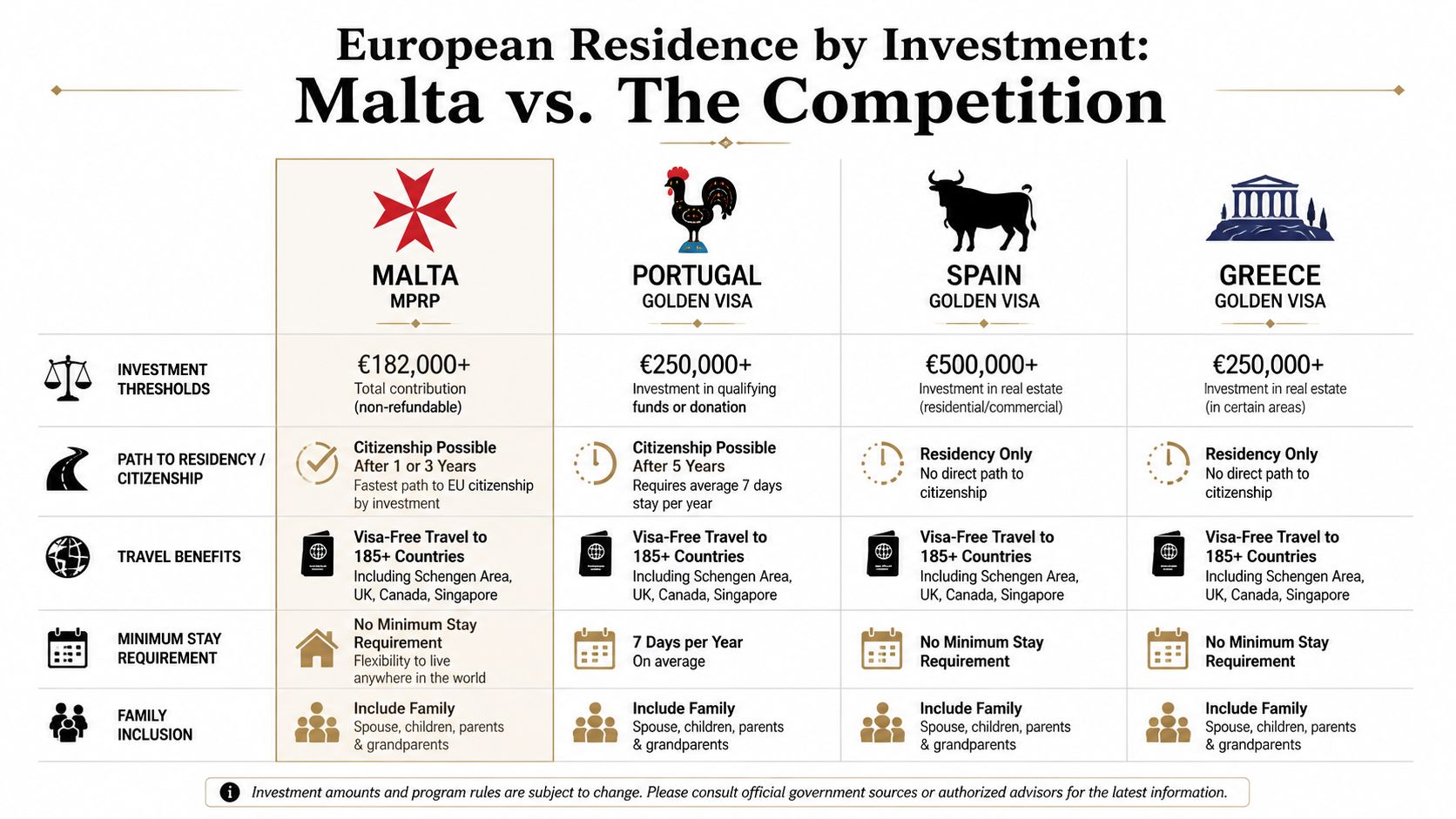

How Malta Compares to Other European Investment Hubs

Malta only makes sense when you compare it against alternatives. Most investors aren't choosing Malta in isolation. They're choosing between different mixes of property exposure, residency rights, legal certainty, and long-term optionality.

A useful UK-relevant angle is the tax and relocation question that many entry-threshold guides ignore. Golden Visas' Malta analysis notes that the unanswered issue for many UK nationals isn't just eligibility. It's whether Malta residence produces a superior after-tax outcome once UK residency rules, professional advice costs, and property lock-up periods are included.

Where Malta sits in the European field

Malta tends to appeal to investors who prioritise a stable EU jurisdiction and are comfortable with a structured property obligation. Portugal, Spain, and Greece often attract buyers for different reasons, such as market familiarity, scale, or broader property choice.

Without inventing thresholds for those competing schemes, the strategic contrast looks like this:

| Market | Typical investor appeal | Main trade-off |

|---|---|---|

| Malta | Legal residence in a compact EU jurisdiction with a defined property component | Significant capital commitment and a strict property-holding logic |

| Portugal | Broad international recognition and strong demand from globally mobile investors | Programme design and route details need close review because the market has evolved |

| Spain | Familiar property market and strong lifestyle demand | Buyers need to separate lifestyle appeal from immigration efficiency |

| Greece | Often seen as an accessible entry point into southern European property | Market selection and asset quality matter more than headline accessibility |

Why Malta can look cheaper than it feels

Malta can appear competitive if you focus only on one part of the stack. That's a mistake. Once you add property hold requirements, professional advice, cross-border tax work, and liquidity constraints, the economic picture changes.

That's especially true for UK-based investors. A Maltese residence card doesn't by itself solve UK tax residence, remittance issues, or broader compliance. Those outcomes depend on facts, timing, and specialist advice.

For many UK families, the best Malta analysis starts with tax residence and family structuring, not with property brochures.

A better way to compare programmes

Most comparisons focus on minimum entry requirements. Experienced investors compare four deeper criteria:

- Outcome clarity. Is the route to residence or citizenship clearly defined, or heavily discretionary?

- Property quality. Are you buying into a market you'd want to hold anyway?

- Flexibility. Can you adapt if family plans or tax residence changes?

- Administrative drag. How much ongoing oversight, reporting, and legal management does the route create?

If you're comparing jurisdictions across the continent, this broader guide to the European golden visa landscape helps place Malta in the right competitive frame.

Key Considerations for Global Property Investors

The cleanest conclusion is also the one most marketing pages avoid. Malta nationality by investment, in the old direct sense, is no longer the product investors think they're buying.

What Malta still offers is more specific. There is a meaningful residence route linked to property, capital commitment, and a real holding period. There is also a merit-based naturalisation framework, but not a guaranteed investor-citizenship package priced off a simple schedule.

The benchmark serious investors should remember

Independent statistics on Malta citizenship cases show how limited the programme was even when it existed in structured form. Chetcuti Cauchi Advocates reported that 143 main applicants had been approved and granted Maltese citizenship, with the rest still being processed, according to Chetcuti Cauchi's Malta citizenship statistics. That's an important benchmark because it shows a tightly controlled route rather than a mass-market scheme.

For UK investors and advisers, that older benchmark also reinforces where Malta sat in the market. The scheme was already at the high end of European investment migration, with minimum outlays commonly starting at about €690,000 once the contribution, property, and donation requirements were combined.

The practical investor checklist

Before committing capital, focus on these questions:

- Legal objective. Are you seeking residence, relocation flexibility, or citizenship? Those are no longer the same thing in Malta.

- Property logic. Would you still want the asset if immigration rules changed again?

- Tax exposure. How will Maltese residence interact with your existing tax position, especially if you have UK links?

- Family fit. Does the route work for dependants, schooling, travel patterns, and long-term succession planning?

A cost-of-living lens matters too, especially if Malta is meant to become more than a compliance jurisdiction. This guide to the cost of living in Malta is useful once the legal route looks viable.

Malta works best for investors who want strategic residence in an EU jurisdiction and are prepared to treat property, liquidity, and tax advice as part of one joined-up decision.

The wrong way to approach Malta is as a shortcut passport purchase. The right way is as a structured residence strategy with meaningful real estate implications and a more selective, less predictable nationality pathway than many legacy guides admit.

If you're comparing Malta with other residency and property-led investment destinations, World Property Investor publishes practical country guides, market comparisons, and real estate analysis to help you assess where each route fits in a global portfolio.