For international investors assessing the Spanish property market, understanding the mortgage landscape is a critical first step. As of late 2024, a non-resident can typically expect fixed mortgage rates between 3.5% and 4.5%. For variable-rate products, the offer is usually the Euribor benchmark rate plus a lender’s margin of 0.7% to 1.5%.

These figures represent the baseline for calculating the cost of capital and potential investment returns in Spain.

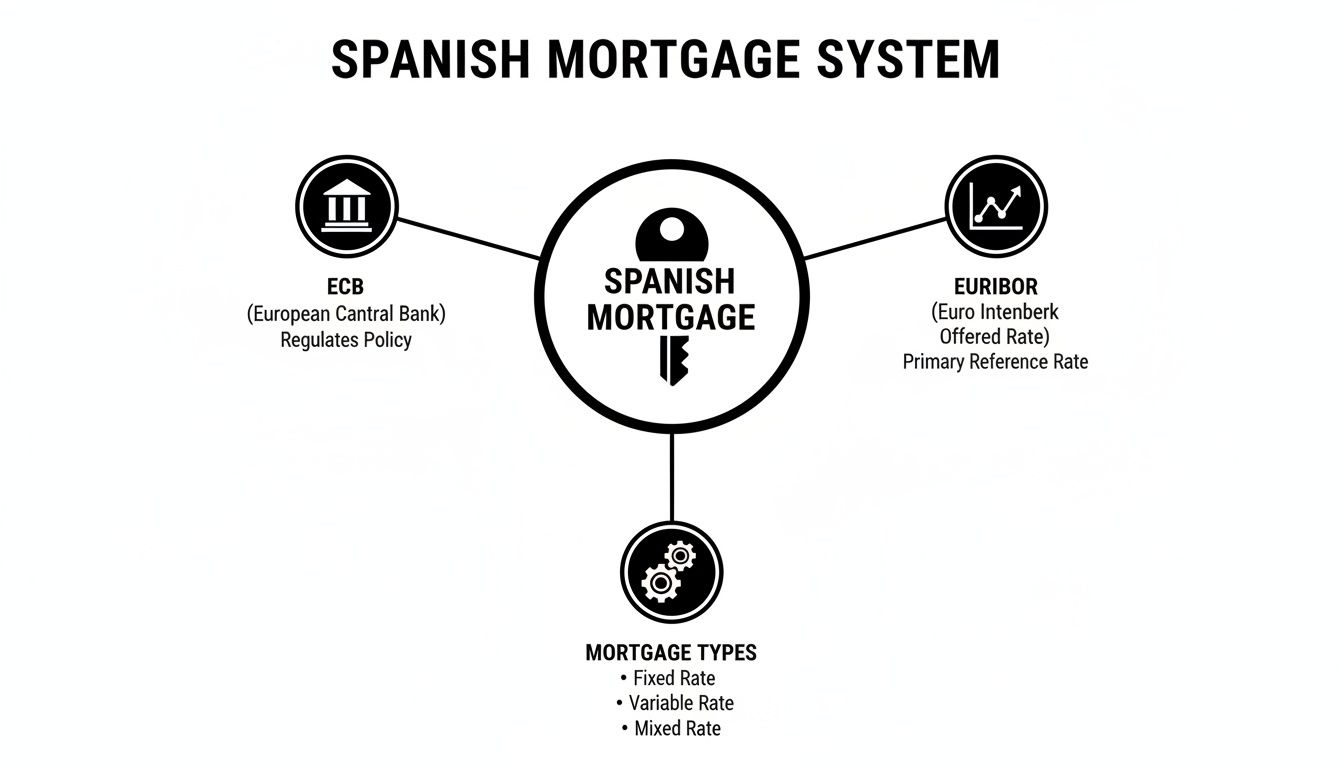

Decoding the Spanish Mortgage Market

For any global property investor, a firm grasp of local financing mechanics is fundamental. Spain continues to attract significant international capital, driven by its lifestyle appeal, strong rental yields in key markets, and potential for long-term capital appreciation. However, its mortgage system differs substantially from those in the UK or North America, presenting unique risks and opportunities.

The market is shaped by two primary forces: the European Central Bank (ECB) and the Euribor benchmark rate. The ECB's monetary policy dictates the foundational cost of money across the Eurozone, which directly influences the mortgage products Spanish banks offer.

Core Mortgage Concepts in Spain

Unlike markets dominated by long-term fixed-rate products, such as the US, Spain offers a more varied landscape. The choice of mortgage structure has a direct and significant impact on an investment's cash flow and sensitivity to interest rate fluctuations.

- Variable-Rate Mortgages (Tipo Variable): Historically the dominant product in Spain, this mortgage's interest rate is directly pegged to the Euribor, plus a fixed margin (the spread) charged by the bank. As Euribor rises or falls, so do monthly repayments. This structure can offer lower initial costs but introduces significant interest rate risk.

- Fixed-Rate Mortgages (Tipo Fijo): This product offers stability by locking in a single interest rate for the entire loan term—typically 20-25 years for non-residents. This predictability is invaluable for investors forecasting rental income and calculating long-term return on investment (ROI) with accuracy.

- Mixed-Rate Mortgages (Tipo Mixto): A hybrid option that provides a fixed rate for an initial period (e.g., 3 to 10 years) before converting to a variable rate. This can offer a balance of initial stability while retaining the potential for lower payments if Euribor falls in the long term.

A key takeaway from European Central Bank analysis is that markets like Spain, where variable-rate mortgages are prevalent, transmit monetary policy changes to borrowers almost immediately. This makes understanding your mortgage structure crucial for effective cash flow management.

This framework necessitates a financing strategy that is carefully aligned with your market outlook and risk appetite. For a deeper analysis of portfolio strategy, our comprehensive guide for property investors provides further insights.

Let's now examine how a lender constructs your final mortgage rate.

How Spanish Banks Calculate Your Mortgage Rate

Understanding the methodology Spanish banks use to construct an interest rate provides a significant advantage, enabling investors to identify competitive offers and anticipate future costs.

The process begins with the European Central Bank (ECB), which sets the base interest rate for the Eurozone. This rate represents the fundamental cost at which commercial banks borrow capital. When the ECB raises its policy rate to manage inflation, the foundational cost of money increases for all lenders, including those in Spain.

This is the first and most powerful component.

As illustrated, ECB policy decisions create ripple effects that directly influence the benchmark rates forming the core of Spanish mortgage products.

The Role of Euribor: The Wholesale Price

While the ECB sets the macroeconomic stage, the Euribor (Euro Interbank Offered Rate) has a more direct impact on monthly mortgage payments.

Euribor represents the 'wholesale price' of money—the average interest rate at which major European banks lend to one another. Before a Spanish bank provides a mortgage (a 'retail' product), it must source the funds, and Euribor reflects this underlying cost.

Most variable-rate mortgages in Spain are linked to the 12-month Euribor. This means the interest rate is reviewed and reset annually based on the prevailing Euribor level. This direct linkage is why fluctuations in Euribor translate so rapidly into changes in mortgage payments for those on variable-rate deals.

The Bank's Margin: The Final Layer

The final component is the bank’s profit margin, known locally as the 'diferencial' or spread. This is a fixed percentage the bank adds to the Euribor rate.

For example, if the 12-month Euribor is at 3.0% and the lender offers a spread of 1.0%, your total interest rate for that year will be 4.0%.

The table below deconstructs this calculation.

| Components of a Spanish Variable Mortgage Rate |

| :— | :— | :— |

| Component | Description | Example Value |

| Euribor (12-Month) | The benchmark interbank lending rate. This is the 'wholesale' cost of money and it fluctuates with the market. | 3.0% |

| Bank's Spread (Diferencial) | The fixed percentage added by the bank as its margin. This is the negotiable part of your rate. | 1.0% |

| Total Interest Rate | The final rate you pay for that year. (Euribor + Spread). | 4.0% |

This structure clarifies that while Euribor is a market-driven variable, the spread is subject to negotiation.

The spread is the primary point of competition among lenders. Your perceived risk as a borrower—determined by your income, credit score, and the asset itself—will directly influence the spread a bank is willing to offer.

Deconstructing the rate into these three elements—ECB policy, Euribor, and the bank's spread—is essential for analysing any mortgage offer. For detailed guidance on the loan approval process, our guide on financing an investment property covers the subsequent steps. This knowledge allows you to properly assess your options and understand the economic forces shaping your investment's performance.

Fixed vs Variable Rates: A Strategic Mortgage Choice

Choosing between a fixed and a variable mortgage is a critical strategic decision that will define an investment's cash flow, risk profile, and long-term profitability. Understanding the mechanics of each—and their appropriate application—is key to aligning your financing with your investment objectives.

The fundamental difference lies in their reaction to macroeconomic conditions, particularly the Euribor rate. A fixed-rate mortgage (tipo fijo) provides certainty, with an interest rate locked in for the entire term (typically 20-25 years for non-residents). Conversely, a variable-rate mortgage (tipo variable) moves with the market, potentially offering lower initial rates but exposing the borrower to interest rate risk.

The Case for Fixed-Rate Mortgages: Predictability and Risk Mitigation

For most international investors, particularly those acquiring buy-to-let properties, a fixed-rate mortgage is the prudent choice. Its principal advantage is absolute predictability in debt servicing costs. You know precisely what your mortgage payment will be every month for the life of the loan.

This stability is invaluable when forecasting rental income, calculating net yield, and ensuring positive cash flow.

Consider an investor acquiring an apartment in an established market like Marbella to generate rental income. Locking in a fixed rate of 4.0% ensures the largest single expense is constant. This simplifies budgeting for other operational costs like maintenance, taxes, and management fees. Subsequent interest rate hikes by the ECB will not disrupt the investment's financial model.

This security explains the significant shift towards fixed-rate mortgages in Spain, a reversal of historical trends. It is a foundational strategy detailed in our beginner's guide to real estate investing.

A fixed-rate mortgage acts as an insurance policy against interest rate volatility. For investors who prioritise predictable, long-term returns, this certainty often outweighs the potential for short-term savings from a lower initial variable rate.

The Case for Variable-Rate Mortgages: A Tool for Specific Scenarios

A variable-rate mortgage links monthly payments directly to the 12-month Euribor, plus the bank’s fixed margin. When Euribor is low, payments can be significantly cheaper than a fixed-rate equivalent. For many years, this was the standard product in Spain during a prolonged period of low interest rates.

However, recent sharp increases in Euribor have resulted in payment shocks for many borrowers, highlighting the inherent risks.

A variable rate may still be suitable for an investor with a higher risk tolerance and a shorter investment horizon.

- Scenario: An investor acquires a property in an emerging area of Valencia with the intention to renovate and sell within three to five years.

- Rationale: They might speculate that Euribor will remain stable or fall during their holding period, allowing them to benefit from lower initial payments and maximise short-term cash flow.

- The Risk: An unexpected rise in Euribor could inflate monthly costs, eroding the profit margin upon exit.

This risk is tangible. Data from the ECB confirms that in markets like Spain with a high prevalence of variable-rate loans, monetary policy shifts have an immediate impact on household finances. This makes variable-rate borrowing a higher-stakes strategy that demands constant market monitoring and a sufficient capital buffer to absorb payment increases.

The choice must be a calculated one, carefully weighing potential savings against the real risk of market volatility.

Navigating Mortgage Requirements as a Non-Resident

Securing a mortgage in Spain as an international investor is entirely feasible but involves a different set of criteria compared to local borrowing. Spanish banks view non-resident applicants with greater caution, which results in stricter underwriting standards and less generous terms.

The most significant difference is the Loan-to-Value (LTV) ratio. While a Spanish resident may obtain a mortgage for up to 80% of a property's appraised value, the maximum LTV for non-residents is typically capped at 60% to 70%.

This requires a substantially larger down payment—often 30-40% of the property's value, plus an additional 10-15% to cover taxes and transaction fees.

Proving Your Financial Strength to Spanish Lenders

As your income, employment, and credit history are based outside of Spain, lenders will conduct rigorous due diligence. They require complete confidence in your ability to service the debt from foreign income.

Presenting a comprehensive and well-organised application is critical. Lenders need a complete financial picture, and thorough preparation will significantly strengthen your position.

Key documentation required includes:

- Proof of Income: For employees, the last six months of payslips. For the self-employed, the last two to three years of tax returns.

- International Credit Report: A detailed credit history from your country of residence is mandatory. Reports from major bureaus such as Experian or Equifax are standard.

- Bank Statements: A minimum of six months of statements from your primary current account to demonstrate consistent income and savings.

- Proof of Funds: Clear evidence of the capital available for the deposit and all associated purchase costs.

Lenders place strong emphasis on your debt-to-income (DTI) ratio. As a general rule, your total monthly debt obligations (including the proposed Spanish mortgage) should not exceed 30-35% of your gross monthly income. A low DTI is a key indicator of a reliable borrower.

Understanding Key Differences in Lending Terms

Beyond the LTV and documentation, other conditions typically differ for non-residents. Mortgage terms are often shorter, capped at 20 or 25 years compared to 30 years for residents. Lenders also impose an age limit, requiring the loan to be fully amortised by age 70 or 75.

Interest rates may also be slightly higher. It is common for a non-resident to be quoted a mortgage rate in Spain that is 0.25% to 0.50% higher than that offered to a resident with an identical financial profile. This premium reflects the bank's pricing of the perceived additional risk of cross-border lending. For strategies on managing such costs, our guide on investing in overseas property offers a broader perspective.

The following table provides a clear comparison of typical mortgage conditions.

Resident vs Non-Resident Mortgage Conditions in Spain

This side-by-side comparison highlights the more demanding requirements for international buyers.

| Metric | Typical for Residents | Typical for Non-Residents |

|---|---|---|

| Maximum Loan-to-Value (LTV) | Up to 80% | 60% – 70% |

| Minimum Deposit Required | 20% + costs | 30% – 40% + costs |

| Maximum Mortgage Term | Up to 30 years | 20 – 25 years |

| Affordability Checks | Standard DTI assessment | More rigorous DTI and income verification |

| Interest Rate Spread | Standard market rates | Often +0.25% to +0.50% above resident rates |

While the requirements for non-residents are more stringent, they are consistently met by thousands of international investors each year. Success depends on thorough preparation, sound financial standing, and a clear understanding of the lender's perspective.

Calculating the True Cost of Your Spanish Mortgage

Securing a competitive mortgage rate is only one part of the financial equation. A realistic investment appraisal must account for all ancillary costs and fees associated with property acquisition and financing in Spain.

These expenses are substantial, often adding 10% to 15% to the purchase price. This has a material impact on the total upfront capital required and the overall return on investment. Failure to budget accurately is a common and costly error.

A precise financial projection requires a detailed breakdown of every fee involved in the mortgage and purchase process.

A Checklist of Core Mortgage and Purchase Costs

Several mandatory expenses must be settled before the mortgage is finalised. These are standard across Spain and form the bulk of the upfront costs.

- Property Valuation (Tasación): The bank requires an independent valuation to confirm the property's market value. This typically costs between €300 and €600. The valuation figure is critical as it determines the maximum loan amount.

- Notary and Property Registry Fees: These are statutory fees for formalising the deed of sale (escritura) and registering the new ownership. Calculated on a sliding scale based on the property price, they generally total between 1% and 2.5% of the property’s value.

- Stamp Duty (AJD): Actos Jurídicos Documentados is a regional tax levied on legal documents, including mortgage deeds. The rate varies between Spain's autonomous communities, typically ranging from 0.5% to 1.5% of the mortgage liability.

Beware of Bundled Products (Productos Vinculados)

A key feature of the Spanish mortgage market is the use of bundled products (productos vinculados). Banks often offer a lower headline interest rate conditional upon the borrower subscribing to other financial services.

While appearing attractive, the cumulative annual cost of these products can negate the savings from the discounted interest rate.

A lower interest rate tied to mandatory products is not always the most cost-effective option. You must calculate the total annual cost of these services to determine if the discounted rate offers genuine value or simply reallocates the expense.

Commonly bundled products include:

- Life Insurance: Almost always mandatory, with the bank as the beneficiary.

- Home Insurance: A standard requirement to protect the underlying asset.

- Bank Account Fees: Requiring the maintenance of a specific, often fee-bearing, account.

- Pension Plans or Credit Cards: Occasionally included to secure the most preferential rate.

A Worked Example of Total Capital Required

This practical example illustrates how these costs accumulate for a non-resident investor.

Assume the acquisition of a property valued at €300,000. As a non-resident, the bank offers a 70% LTV mortgage, resulting in a loan of €210,000. The required upfront capital is significantly more than the €90,000 deposit.

A realistic breakdown is as follows:

- Deposit (30%): €90,000

- Purchase Taxes (e.g., ITP at 8%): €24,000

- Notary & Registry Fees (approx. 1.5%): €4,500

- Valuation Fee: €400

- Stamp Duty (AJD at 1% of mortgage): €2,100

- Total Upfront Capital: €121,000

In this scenario, the total capital required exceeds 40% of the property price. Incorporating this reality into your budget is essential. For a framework on how these outlays affect profitability, our guide on how to calculate return on investment (ROI) for real estate provides the necessary formulas and analysis.

Strategies to Secure the Best Possible Mortgage Rate

Securing the most favourable mortgage rate in Spain is not a matter of chance; it is the result of proactive preparation, negotiation, and strategic positioning. For non-resident investors, optimising financing terms can have a significant impact on long-term returns.

Engaging an independent mortgage broker who specialises in financing for international clients is a highly effective strategy. A single bank can only offer its own products and operates within its specific risk framework. A specialist broker, however, provides access to a wide network of lenders, including private banks and institutions experienced in assessing foreign income and complex financial profiles.

This creates a competitive dynamic where lenders must compete for your business, often leading to more favourable terms than could be achieved directly.

Strengthening Your Borrower Profile

The primary objective is to present yourself as a low-risk, high-quality borrower. The strength of your application directly influences your negotiating power, particularly regarding the bank’s spread.

A robust application is built on several key pillars:

- A Substantial Deposit: Offering a deposit larger than the minimum required (e.g., 40% instead of 30%) significantly reduces the bank's perceived risk and signals strong financial standing.

- A Low Debt-to-Income (DTI) Ratio: Spanish lenders generally require total monthly debt service to be below 30-35% of gross income. Reducing other liabilities before applying can materially strengthen your application.

- Impeccable Documentation: Flawlessly organised financial paperwork—from international credit reports to tax returns, officially translated where necessary—demonstrates diligence and professionalism.

Your borrower profile is your most powerful negotiating tool. Lenders are more inclined to be flexible on their margin for applicants who represent minimal risk. A small reduction in the spread, for example from 1.2% to 0.9%, can result in thousands of euros in savings over the life of the loan.

Critically Evaluating 'Bonificaciones'

Spanish banks frequently offer rate reductions, known as bonificaciones, in exchange for contracting other products such as home insurance, life insurance, or pension plans. While a discounted rate is appealing, a thorough cost-benefit analysis is essential.

Before accepting a bundled offer, calculate the total annual cost of all mandatory products. Compare this figure against the annual savings generated by the reduced interest rate.

It is often the case that high premiums on bundled insurance products erode or eliminate the benefit of the lower mortgage rate. Always request a quote without the bonificaciones to facilitate a clear comparison. This is the only way to ensure the chosen mortgage rate genuinely maximises your investment's profitability.

Spanish Mortgage FAQs

This section addresses common questions from international property investors, providing clear and practical answers to key concerns.

Can I Still Get a Mortgage in Spain as a UK Citizen After Brexit?

Yes, UK citizens can still obtain mortgages in Spain. However, post-Brexit, UK applicants are assessed as non-EU residents.

This typically results in more stringent underwriting. Lenders will likely offer a lower Loan-to-Value (LTV) ratio, usually 60-70%, and will conduct more intensive verification of your UK-based income and financial stability. Providing a comprehensive UK credit report from a major agency like Experian is essential. Engaging a mortgage broker with expertise in non-EU applications is highly advisable.

What Is a Typical Mortgage Term Length in Spain?

For non-residents, mortgage terms in Spain are generally 20 years, with a maximum of 25 years available from some lenders. This is shorter than the 30-year terms often available to Spanish residents.

A critical factor for older investors is the age limit. Spanish banks typically require the mortgage to be fully repaid by the borrower's 70th or 75th birthday. This can significantly shorten the available term, thereby increasing monthly repayments.

Is It Possible to Remortgage a Spanish Property?

Yes, remortgaging is possible, though the process, known as 'subrogación', differs from the UK system. It allows a borrower to transfer their existing mortgage to a new lender to secure more favourable terms.

However, this is not a cost-free transaction. The process involves fees similar to those for a new mortgage, including notary and registry charges, and may require a new property valuation. It is vital to conduct a thorough cost analysis to ensure that the long-term savings from a lower interest rate outweigh the upfront costs of the transfer.

Do I Need a Spanish Bank Account to Get a Mortgage?

Yes, this is a non-negotiable requirement. You cannot obtain a mortgage from a Spanish bank without holding a Spanish bank account.

This account will be used for all mortgage-related transactions, including monthly direct debits. It is also used for paying local property taxes (IBI) and utility bills. Furthermore, before finalising any property purchase or mortgage, you must obtain a Spanish fiscal ID number, the NIE (Número de Identificación de Extranjero).

At World Property Investor, we provide the in-depth guides and market analysis you need to make confident investment decisions across the globe. Explore our resources to find your next opportunity.

Learn more about global property investment at World Property Investor