Investing in off-plan property means purchasing a home directly from a developer before it has been built. This strategy allows an investor to secure a brand-new asset, based on architectural plans and projections, often at a price below its anticipated future market value.

The primary attraction of off-plan investments is the potential for capital appreciation during the construction period, allowing the property's value to increase significantly by the time ownership is transferred.

Understanding the Fundamentals of Off Plan Investments

At its core, buying off-plan is a forward-looking purchase. You commit to a property that currently exists only on paper, locking in a price based on today’s market for an asset that will not be delivered for several months or even years.

This gap between the initial deposit and final completion is a critical window—one where capital growth can occur before the full balance has even been paid.

The Developer's Motivation

Developers offer properties off-plan for several strategic business reasons. Early sales are a powerful tool for securing project financing, as demonstrating pre-sales to lenders significantly de-risks the project from a financial perspective.

These initial sales also generate essential cash flow and help the developer to gauge market appetite, providing the confidence and capital required to proceed with construction.

The Investor's Advantage

For buyers, the appeal is multi-layered. The principal draw is the opportunity to acquire an asset for less than its future market value. As the project is constructed and the surrounding area develops, the property’s value can appreciate considerably.

This creates what investors term "built-in equity"—the difference between the price you agreed to pay and the property's open market value upon completion.

For example, assume you agree a purchase price of £250,000. If the local market experiences average price growth of 5% per annum during a two-year construction period, your property could be worth approximately £275,625 at handover. This represents an immediate paper gain of over £25,000 before a tenant is secured.

The primary draw for many is locking in today's price for an asset that will be delivered in the future. If the market moves favourably during the construction phase, investors can realise substantial capital appreciation before the final payment is even due.

This is not a speculative gamble but a calculated approach that relies on robust market fundamentals and, crucially, meticulous due diligence. To understand these core concepts better, our beginner's guide to real estate investing is an excellent starting point. A firm grasp of the basics is essential to maximising the opportunities off-plan investments can offer.

The Financial Engine Behind Off-Plan Property

The appeal of buying off-plan extends beyond acquiring a brand-new home. It is driven by powerful financial mechanics that work in unison to build wealth, often before the final balance has been paid.

At its core, the strategy allows investors to leverage market dynamics to their advantage. By entering the market early, you can unlock value that is simply not available with existing properties.

Securing a Below-Market-Value Price

A significant advantage of off-plan investments is the opportunity to purchase a property at a below-market value (BMV). Developers are motivated to secure early sales to demonstrate demand to lenders and obtain project funding. To achieve this, they often offer substantial "early bird" discounts to the first wave of buyers.

This provides an immediate pricing advantage. You are not just buying a property; you are acquiring an asset with a built-in discount compared to its projected completion value. This head start is a cornerstone of successful off-plan investments.

For example, off-plan properties in key UK cities such as Liverpool and London are frequently sold at considerable discounts. Market data suggests savings of 10-15% are common in the initial launch phases, giving early investors a significant advantage. You can read more about the growing demand for UK off-plan property.

The Power of Capital Appreciation During Construction

The initial discount is only part of the equation. The period between paying a deposit and the property's completion—often lasting one to three years—is a crucial window for capital growth. While your property is under construction, the wider market continues to move.

If the local property market appreciates during this time, the value of your asset grows with it. Crucially, you benefit from this uplift on the property's full value, despite having only paid a fraction of the purchase price upfront.

This is a classic example of leveraged growth. An initial deposit of, say, 20% gives you exposure to 100% of the asset's capital appreciation. A 5% rise in the property's market value can translate into a much higher percentage return on your actual cash invested.

Staggered Payments and Improved Cash Flow

Unlike purchasing a completed property, which typically requires a full mortgage and upfront payment, off-plan transactions are structured with a staggered payment plan. This significantly improves an investor's cash flow and allows their capital to work more efficiently.

The payment process typically follows this structure:

- A small reservation fee to secure the unit.

- An initial deposit, usually between 10% and 30% of the purchase price, paid upon exchange of contracts.

- The remaining balance is due only when the property is legally completed and handed over.

This structure means the bulk of your capital is not tied up for the entire construction period. It can remain invested elsewhere, earning returns, until the final payment is due. This financial flexibility is a key reason why portfolio investors favour this strategy. For a deeper analysis of return calculations, you can check out our guide on how to calculate ROI for real estate.

Higher Rental Yields from Day One

These financial advantages culminate in stronger performance once the property is completed. Brand-new properties attract high-quality tenants and command premium rental rates from the outset.

New-builds require minimal initial maintenance, are constructed to the latest energy and safety standards, and often include modern amenities that today’s tenants actively seek. This translates into higher rental yields and a more reliable income stream from the moment of completion, ensuring the investment performs robustly for years to come.

Understanding and Mitigating Investment Risks

While the promise of strong returns attracts many to off-plan property, a prudent investment is built on a clear-eyed assessment of the potential downsides. Every investment carries risk, and off-plan is no exception. The objective is not to find a risk-free deal—they do not exist—but to understand and manage the risks involved.

This practical approach transforms vague concerns into a manageable part of your strategy. By addressing challenges upfront, you can build in safeguards to protect your capital and keep your long-term objectives on track.

Construction Delays and Financial Impact

One of the most common risks associated with off-plan property is construction delays. These can arise from various factors, including supply chain disruptions, labour shortages, or planning permission hold-ups. While a minor delay may be a mere inconvenience, a significant one can create genuine financial problems.

For example, a prolonged delay could cause your mortgage offer to expire, as lenders typically issue them with a six-month validity period. Re-applying may result in less favourable terms if interest rates have risen. Furthermore, every month of delay represents a month of lost rental income, directly impacting your projected returns.

Mitigation Strategy: Your legal contract is your primary defence. Ensure it includes a "long-stop date"—a final, non-negotiable deadline for the developer to complete the property. If this date is missed, the clause should grant you the unequivocal right to rescind the contract and receive a full refund of your deposit.

Developer Insolvency Risks

A more severe, though less frequent, risk is developer insolvency. This is the worst-case scenario where the development company ceases trading before your property is completed. If your deposit is not adequately protected, it could be lost.

Reputable UK developers have safeguards for this eventuality. Deposits are typically held in a secure escrow account managed by a solicitor or protected by a new-build warranty provider like the NHBC (National House Building Council), which includes deposit protection. This effectively ring-fences your money for return in case of developer default.

- Vetting is crucial: You must investigate the developer’s financial health and track record. Look for a solid history of successfully completed projects and positive feedback from previous buyers.

- Verify protection: Never take a developer's word for it. Your solicitor must confirm in writing that your deposit will be held in a protected scheme or secure escrow account before you exchange contracts.

This level of due diligence is non-negotiable and forms the bedrock of a secure off-plan investment.

Market and Completion Risks

Property markets can fluctuate during the construction period. This is known as market risk. If property values in the area decline between contract exchange and completion, you could face a valuation shortfall. This occurs when the lender's final valuation is lower than the agreed purchase price, potentially requiring you to fund the difference in cash.

Finally, there is completion risk—the possibility that the finished property does not meet the specifications promised in the marketing materials. This can range from minor cosmetic issues to significant problems with the layout or quality of fixtures and fittings.

Here is how you manage these risks:

- Conduct thorough market research: Do not invest indiscriminately. Focus on areas with strong economic fundamentals, such as population growth and major infrastructure investment, which help to insulate against downturns. ONS data often shows that regions with diverse job markets tend to have more resilient property prices.

- Scrutinise the contract: Your purchase agreement must be meticulously detailed. It should specify everything from materials and appliance brands to flooring types. A watertight contract empowers you to hold the developer accountable.

- Arrange a snagging survey: Before completion, hire an independent professional to conduct a "snagging" survey. They will compile a list of any defects or incomplete work that the developer is legally obliged to rectify before you take ownership.

Your Essential Due diligence Framework

Successful off-plan property investment is not a matter of luck; it is the result of methodical, meticulous due diligence. Without a structured approach, you are investing blind. This framework serves as your practical checklist, breaking down the complex process into four non-negotiable areas for investigation.

Treat this as your blueprint for de-risking the purchase and making an informed, secure investment. Each step is designed to build a complete picture, from the people behind the project to the legal fine print and the economic health of the location itself.

Investigating the Developer's Track Record

First, you must scrutinise the developer. Remember, you are not merely buying a property; you are entrusting a company with significant capital to deliver on a major promise. Their history, financial stability, and reputation are paramount.

Begin by examining their portfolio of completed projects. Do they have a consistent track record of delivering on time and to a high standard? Look for evidence of past developments, seek online reviews, and check for recurring complaints about build quality or delays. A developer with a long history of successful handovers is a far safer proposition than a new entity with no proven experience.

A financially healthy developer is also less likely to become insolvent mid-project. While full financial accounts may not be accessible, your solicitor can conduct checks for red flags, such as county court judgements or winding-up petitions.

Key Takeaway: A developer's past performance is the most reliable indicator of their future behaviour. Prioritise established developers with a transparent and verifiable history of delivering high-quality projects on schedule.

Forensic Review of the Legal Pack

Once you are confident in the developer, the focus shifts to the legal paperwork. This is not a DIY task; you must engage a specialist solicitor with experience in off-plan conveyancing. They will conduct a forensic review of the legal pack, which contains all the crucial documents protecting your interests.

Their key responsibilities include:

- Verifying Land Title: Ensuring the developer legally owns the land and has the full right to build on it.

- Confirming Planning Permission: Checking that full and final planning consent has been granted by the local authority—not just outline permission. UK government guidance is clear that projects must adhere strictly to approved plans.

- Analysing the Contract: Scrutinising the purchase agreement for protective clauses, such as the "long-stop date" for completion, and obtaining clear details on how your deposit is protected.

- Reviewing Leases and Covenants: Identifying any restrictive covenants or unusual leasehold terms that could affect your ownership or ability to let the property.

This legal deep-dive is your safety net, ensuring there are no hidden surprises that could jeopardise your investment.

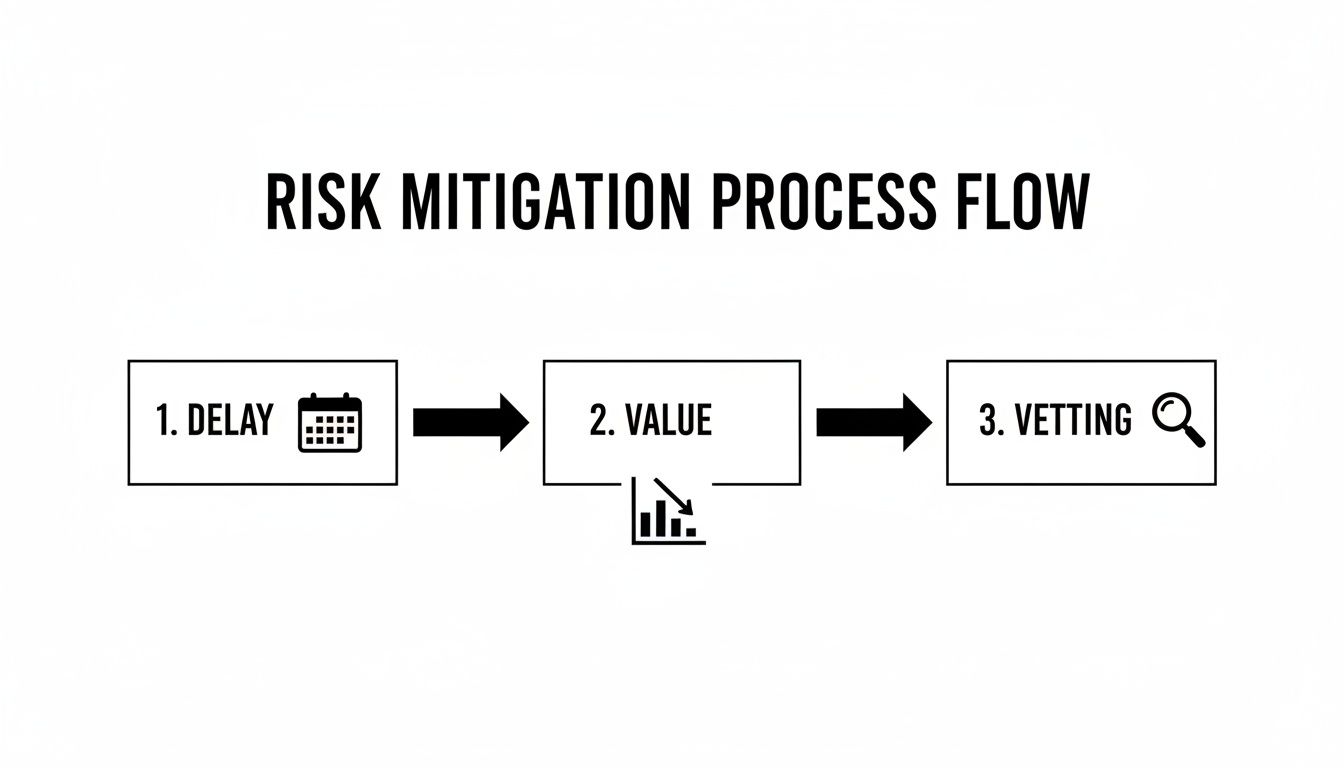

This infographic shows how good due diligence helps tackle the most common investment risks head-on.

The flow is simple: thorough vetting is the foundation for managing potential delays and protecting your asset's future value.

Scrutinising Property Specifications and Location

With the developer and legal checks complete, your attention should turn to the asset and its location. Never rely solely on marketing brochures. Instead, request detailed floor plans with precise measurements and a full schedule of specifications. This document should list everything from the brand of kitchen appliances to the type of flooring and quality of bathroom fixtures.

Simultaneously, conduct a deep-dive analysis of the location’s growth drivers. Strong fundamentals underpin future capital appreciation and rental demand. Look for tangible evidence of:

- Infrastructure Investment: Are new transport links, such as a train station or motorway junction, under construction? Projects like these significantly boost connectivity and property values.

- Regeneration Projects: Is the area part of a wider government or council-led regeneration scheme? This often signals sustained investment and future growth.

- Local Economic Health: Research local employment rates and major employers. A diverse and growing job market fuels rental demand. Data from bodies like the Office for National Statistics (ONS) can provide valuable regional economic insights.

- Rental Market Analysis: Check local rental listings on major portals to gauge demand and typical yields for similar new-build properties.

Understanding these factors is crucial to determine a property's investment potential and ensures you are buying in an area with a genuinely promising future.

Finally, remember that securing finance for an unbuilt property requires a specialist approach. Many high-street lenders are hesitant to offer mortgages on off-plan properties far in advance. It is wise to speak with a mortgage broker who specialises in new-build financing early in the process to understand your options and ensure you can secure the necessary funds upon completion.

Comparing UK Established and Emerging Markets

Choosing the right location is arguably the most critical decision in property investment. For those exploring off-plan investments in the UK, the choice often lies between two distinct paths: buying in a globally recognised prime market like London, or targeting a high-growth, emerging hotspot in another region.

Each strategy presents its own risk-and-reward profile, and the optimal choice depends entirely on your financial objectives.

An established market like London offers stability, prestige, and a proven track record. It is a global safe haven for capital. However, this security comes at a price: extremely high entry costs, compressed rental yields that often struggle to exceed 3%, and a market where growth has slowed compared to other UK regions.

Conversely, emerging markets, particularly in the North West of England, offer a compelling alternative. These areas are experiencing powerful economic growth and deliver a potent combination of lower property prices, healthier rental yields, and strong potential for capital appreciation.

The Appeal of Established Prime Markets

Investing in an off-plan development in prime central London is akin to buying blue-chip stock. It is a globally recognised asset that attracts international capital, providing investors with a sense of security and a liquid market for future resale.

The main benefits of established markets include:

- Resilience: Prime markets tend to hold their value better during economic downturns, acting as a defensive asset in a wider portfolio.

- Prestige and Demand: The global appeal of a city like London ensures a consistent pool of high-calibre tenants and future buyers.

- Long-Term Stability: While short-term growth may be modest, the long-term outlook for capital preservation is exceptionally strong.

The high cost of entry, however, is a significant barrier. A one-bedroom flat in a new London development can easily exceed £700,000, making it a capital-intensive strategy with yields that are often outpaced by inflation.

High-Growth Emerging Hotspots

For investors seeking stronger returns, emerging markets such as Manchester and Liverpool present a more dynamic proposition. These cities are evolving into economic powerhouses, attracting billions in infrastructure investment, major corporate relocations, and a rapidly growing population of young professionals.

This economic momentum directly fuels the property market. Lower entry prices mean capital goes significantly further. An investor can often secure a new-build city-centre flat for a fraction of the London equivalent, typically in the £200,000-£300,000 range. This lower cost base is the foundation for superior returns.

The core investment case for emerging UK markets is simple: you can acquire high-quality, new-build assets in economically thriving city centres for a price that allows for both strong rental income today and significant capital growth tomorrow.

Data strongly supports this shift in focus. In recent years, the North West of England has become the UK leader in off-plan flat sales, overtaking London. According to research from Hamptons, 63% of all new-build flats in the region were sold off-plan, compared to just 55% in the capital. Salford stood out with 80% of its new flats sold before completion, with Liverpool close behind at 75%. Discover more insights about these market shifts from MPA Magazine.

A Data-Led Comparison

To illustrate the difference, let us compare the key metrics for an investor. The table below provides a snapshot of how a typical off-plan investment might perform in an established market versus an emerging one.

| Metric | Established Market (e.g., London Zone 2/3) | Emerging Market (e.g., Manchester/Liverpool) |

|---|---|---|

| Average Entry Price | £700,000+ | £250,000 – £350,000 |

| Gross Rental Yield | 2.5% – 3.5% | 5.5% – 7.0% |

| Capital Growth (5yr) | Modest/Stable | High Potential |

| Economic Drivers | Global finance, tech, tourism | Regeneration, infrastructure, diverse economy |

| Investor Focus | Capital Preservation | Yield and Growth |

As the figures show, the financial case for emerging markets is compelling. An investor can often purchase two, or even three, high-yielding properties in the North West for the price of a single, lower-yielding asset in London. This not only generates superior cash flow but also diversifies risk across multiple assets. To explore this further, you might be interested in our guide on the top 7 emerging property investment markets.

Ultimately, the decision rests on your investment horizon and risk appetite. For stable, long-term wealth preservation, established markets retain their appeal. However, for those pursuing a strategy focused on maximising both rental yields and capital growth, the data clearly points towards the UK's thriving emerging hotspots.

Navigating Legal and Financing for Global Investors

Purchasing an off-plan property in the UK as a global investor is a structured, well-defined process. It is designed to be secure, but requires an understanding of the key stages and the professional support necessary—it differs from buying a completed property.

The process typically begins with a reservation deposit, a small fee to take the chosen unit off the market while initial legal checks are conducted. This is followed by the exchange of contracts, a significant legal step where you commit to the purchase and pay a deposit of typically 10-30% of the property’s value. The final stage is completion, when the building is finished, the remaining balance is paid, and ownership is formally transferred.

The Legal Framework for Off-Plan Investments

This process hinges on one key professional: your UK-based solicitor. They are more than just a legal professional handling paperwork; they are your safeguard on the ground. Their role is to conduct thorough due diligence on the developer, the land title, and all planning permissions.

Your solicitor will review the purchase contract meticulously, ensuring your interests are fully protected. They will check for clauses covering deposit protection, confirm the "long-stop date" (the absolute deadline for completion), and ensure the property’s final specifications are contractually binding. A solid legal footing is non-negotiable for any secure off-plan investment.

A solicitor experienced in off-plan conveyancing for international buyers is essential. They act as your eyes and ears on the ground, ensuring every legal requirement is met and protecting your capital throughout the construction phase.

Securing Finance as a Non-Resident

Securing a mortgage can be more complex for overseas buyers. Many UK high-street lenders are cautious about lending to non-residents, and their mortgage offers often expire after six months, which is unsuitable for properties with a one- or two-year build time.

Consequently, most international investors work with specialist lenders or the UK branches of international banks. These institutions are more accustomed to assessing overseas income and offer mortgage products specifically designed for non-resident buyers.

Be prepared for stricter lending criteria:

- Higher Deposit Requirements: While a UK resident might secure a mortgage with a 10-15% deposit, overseas buyers are often required to provide 25-40% of the property's value.

- Proof of Income: Lenders will require extensive, verified documentation of your global income to ensure affordability.

- Credit History: While not always essential, having some form of UK credit footprint can be beneficial. Specialist lenders are adept at evaluating international credit reports.

Understanding Your Tax Obligations

Tax is a critical component of any property investment budget. For international buyers in the UK, the primary tax to consider is Stamp Duty Land Tax (SDLT), which is payable upon completion of the purchase.

As a non-UK resident, you will be liable for a surcharge on top of the standard SDLT rates. As per the latest government guidance, this is an additional 2% for non-residents purchasing residential property in England and Northern Ireland.

This means your total stamp duty liability will be higher than that of a UK resident for the same property. It is crucial to factor this cost into your budget from the outset to avoid any surprises. We cover how to manage these costs in our full guide to investing in overseas property.

Answering Your Top Off-Plan Questions

When exploring off-plan property, several key questions frequently arise. Here are answers to the most common queries from investors.

Can I Sell an Off-Plan Property Before It’s Finished?

Yes, this is possible. The strategy is known as ‘flipping’ or an ‘assignment sale’, and it allows investors to realise capital growth without completing the purchase or securing a mortgage. In essence, you sell your contract to another buyer before the building is finished.

However, you must check the small print of your purchase agreement. Many developers include clauses that either prohibit assignment sales or charge a significant fee for permission. Your solicitor must confirm the specific terms before you sign the contract.

What Happens if the Final Valuation Comes in Lower Than My Purchase Price?

This is a key risk known as a ‘valuation shortfall’. If the lender's official valuation at completion is lower than the price you agreed to pay, they will only lend against the lower figure. This would require you to fund the difference in cash.

The most effective way to mitigate this risk is to select your location carefully. Focus on areas with strong economic fundamentals and major regeneration projects, as these markets tend to be more resilient and less prone to sharp downturns.

How Are Off-Plan Sales Performing in the Current UK Market?

The market presents a mixed picture. Nationally, UK off-plan sales have fallen to 31% of all new-build homes sold—the lowest level since 2012. However, a closer look reveals that astute investors are following growth into new hotspots.

While London’s share of off-plan sales has decreased from a peak of 66% in 2016 to just 37% today, the North West has surged ahead. An impressive 63% of flats in the region are now sold before completion, with cities like Salford reaching 80% and Liverpool 75%. You can discover more insights on these UK off-plan trends to see the full picture. The data indicates a clear shift: smart capital is moving to where the growth is.

At World Property Investor, we provide the data-driven guides and market analysis you need to make informed decisions. Explore our resources to compare global markets, analyse deals, and invest with confidence. Visit https://www.worldpropertyinvestor.com to start your research today.