Investing in South African property has always been a game of contrasts, blending clear opportunity with calculated risk. On one hand, you have the potential for strong rental yields in the country’s economic powerhouses. On the other, there’s the lure of solid capital growth in the stunning, lifestyle-driven coastal regions. For a global investor, success hinges on understanding the fundamentals on the ground—region by region and street by street.

Is South African Property a Good Investment in 2026?

For any global property investor analysing South Africa in 2026, the narrative is one of gradual stabilisation and pockets of pronounced growth. After a period of sluggish performance, key economic signals are becoming more encouraging. Interest rates, which were elevated to control inflation, are stabilising. This stability is critical, as it improves mortgage affordability and coaxes more buyers back into the market.

This recovery is not uniform across the country; the market is a collection of distinct regional stories. Coastal areas, particularly in the Western Cape, continue to benefit from "semigration"—a domestic trend of affluent South Africans relocating for a better quality of life, which underpins robust price growth. In contrast, economic centres like Johannesburg offer more attractive rental yields, making them a prime target for buy-to-let investors focused on cash flow.

The Power of Youth-Driven Demand

A powerful force shaping the market is the rise of the younger buyer. According to data from the South African Deeds Office, buyers under the age of 44 now account for half of all property purchases. This demographic is driving demand for specific property types: modern, secure, and well-located sectional title units within lifestyle estates.

This creates a clear opportunity for investors who can supply what this market demands. The primary drivers for these buyers are:

- Security: Gated communities and secure apartment blocks are in extremely high demand.

- Affordability: The sweet spot for this group is properties in the R800,000 to R1.5 million price bracket.

- Lifestyle Amenities: On-site gyms, parks, and retail facilities are a significant drawcard.

To understand the numbers and what lies ahead, this table offers a snapshot of key indicators shaping the market.

South African Property Market Key Indicators 2026

For prospective investors, these data points offer a clear view of the opportunities and considerations shaping the South African property market.

| Metric | Figure / Trend | Investor Implication |

|---|---|---|

| Prime Interest Rate | Stabilising around 11.75% | Improved mortgage affordability should stimulate buyer demand. |

| House Price Growth | National average 2-4%; Western Cape 5-7% | Strong regional variations make location choice critical for capital growth. |

| Youth Buyer Segment | 50% of all property purchases | Strong demand for secure, modern sectional titles in the R800k-R1.5m bracket. |

| Average Rental Yield | 6-9% nationally | Johannesburg and Gauteng offer higher yields; Cape Town is more growth-focused. |

| ZAR/USD Volatility | Moderate to high | Currency risk is a key factor; consider hedging or pricing rentals in major currencies. |

These figures highlight a market that is stabilising but remains diverse. Success hinges on matching an investment strategy—be it yield- or growth-oriented—to the correct location and property type.

Understanding the Investment Fundamentals

While the outlook is improving, a clear-eyed, practical approach is vital. The South African market has its challenges, from currency volatility to socio-economic risks. However, the country’s sophisticated legal system and transparent property registration process provide foreign investors with a solid and reliable foundation.

For a shrewd investor, the current market represents a moment of opportunity. With prices still relatively subdued in many areas and rental demand firming, the potential for both capital appreciation and healthy yields is tangible, provided due diligence is meticulously performed.

If you are just beginning to explore the possibilities, a good first step is to read up on the basics. This guide on How to Invest in a Real Estate in South Africa provides excellent foundational knowledge. For a broader view on the trends leading into 2026, our detailed property market forecast for 2025 offers essential context.

Where to Invest in South African Property

Choosing where to invest is the most critical decision in the South African property market. It is not a single market but a patchwork of distinct regional economies, each with its own profile, risks, and rewards. For an international investor, understanding these local nuances is essential to aligning your goals—whether high rental income or long-term capital growth—with the right location.

South Africa’s property landscape is dominated by its three major metropolitan areas: Cape Town, Johannesburg, and Durban. Each offers a different proposition. Beyond these hubs, several smaller cities and lifestyle towns are emerging as intelligent long-term investment locations.

The Big Three Major Metros

A sound investment strategy almost always begins with an analysis of the country’s primary economic and lifestyle centres. Each of these three cities caters to a different investor appetite.

Cape Town: The Premium Lifestyle Market

Cape Town operates in its own league as South Africa's premium market. It is fuelled by a potent mix of natural beauty, a reputation for effective local governance, and a steady influx of high-net-worth individuals from other provinces. This "semigration" trend has sustained strong house price growth, especially in coveted areas like the Atlantic Seaboard, the City Bowl, and the Southern Suburbs.

This quality comes at a price. Cape Town has some of the lowest rental yields among the major cities, often between 4% and 6% gross. An investment here is typically a long-term play on capital growth, not immediate cash flow. Target tenants are high-income professionals, international expatriates, and corporate lets, particularly for properties in secure, modern blocks with sea or mountain views.

Johannesburg: The Economic Powerhouse

As the country’s economic engine, Johannesburg presents a different value proposition focused on cash flow. It is not unusual to find rental yields from 7% to over 10% in well-chosen areas. The city's property landscape is incredibly diverse, from the corporate hubs of Sandton and Rosebank to more affordable neighbourhoods with high concentrations of students and young professionals.

Johannesburg's property market is a pure economic play. Success lies in identifying neighbourhoods with strong corporate and student rental demand, where cash flow is king. Investors must conduct granular research, as performance can vary significantly from one suburb to the next.

For example, a two-bedroom flat near a major business hub or university can be a dependable income-generating asset. The primary drivers here are security and convenience. The city’s tenant pool is vast and varied—from corporate employees and government workers to a large student population—making it a versatile buy-to-let destination.

Durban: The Coastal Value Proposition

Durban and the rapidly developing KwaZulu-Natal North Coast offer a compelling blend of lifestyle and relative value. Areas such as Umhlanga and Ballito are experiencing a boom in new developments, attracting both holidaymakers and permanent residents. While it lacks Cape Town's explosive price growth, Durban provides a solid middle ground with decent rental returns and good potential for long-term appreciation.

Property here is often geared towards tourism (short-term lets) and families pursuing a coastal lifestyle. The tenant base is a mix of local professionals, retirees, and a steady flow of holidaymakers, particularly during peak seasons.

Emerging Markets and Secondary Cities

Beyond the main metros, several smaller markets offer interesting opportunities for investors with a longer-term perspective. These locations often have lower entry prices and strong potential for future growth. For those looking to diversify, understanding the global principles of where to invest in property can provide a valuable framework.

- The Garden Route: Towns like Plettenberg Bay, Knysna, and George are significant semigration hotspots, mirroring the trend seen in the Western Cape. They offer an exceptional quality of life and are experiencing steady, reliable price growth.

- Gqeberha (Port Elizabeth): As a major port and the heart of South Africa’s automotive industry, Gqeberha has some of the most affordable property of any major city. It is a good location for yield-focused investors betting on the region's economic backbone.

- The Winelands: Stellenbosch and Franschhoek are world-renowned lifestyle destinations. The property market here is driven by a mix of tourism, the large student body at Stellenbosch University, and wealthy buyers acquiring country estates.

Ultimately, the best place to invest in South African property depends on your personal strategy. Whether you seek the reliable capital growth of Cape Town or the powerful cash flow of Johannesburg, a clear understanding of what makes each market tick is your most important tool.

Analysing Price Trends and Rental Yields

To make an informed investment in South Africa, one must look beyond marketing materials and become comfortable with the data. Headline figures about market growth can be encouraging, but it is the granular data on price trends and rental yields that reveals how a property will perform financially. For any international investor, this means analysing city-specific performance and understanding the difference between nominal growth and real, inflation-adjusted returns.

The national property market is on a slow but steady path to recovery. According to FNB data, when adjusted for inflation, residential prices saw a slight dip of 0.59% in the first ten months of 2025, a sign of a market still mending. However, nominal growth is ticking along at over 6% year-on-year. With interest rate cuts widely expected in 2026, forecasters anticipate this will stimulate buyer demand and support a solid 6% average nominal growth for the coming year. For a deeper look at the data, you can explore the price history from Global Property Guide and FNB.

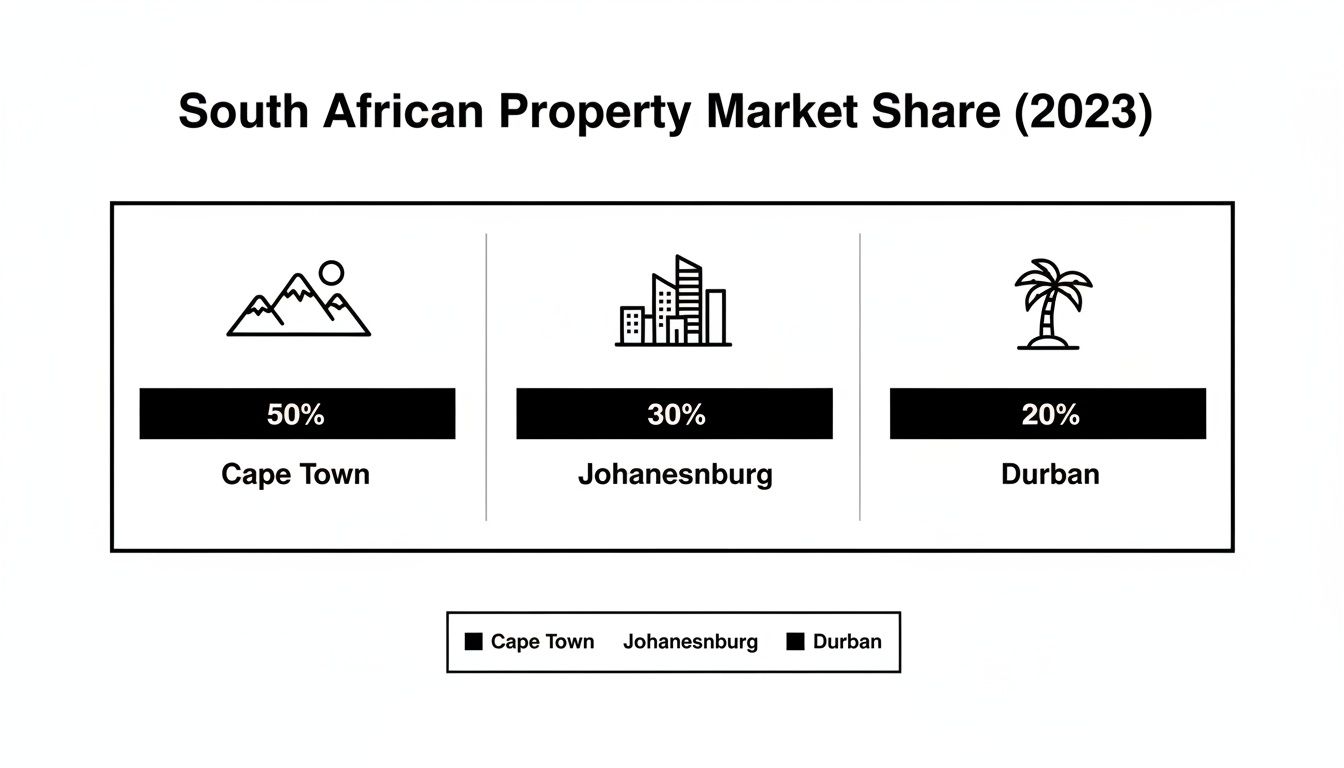

This infographic provides a snapshot of where activity is concentrated across South Africa's three main property hubs.

As shown, Johannesburg and Cape Town are the heavyweights, but Durban holds a significant and stable share of the market, reinforcing its position as a key investment location.

Deconstructing Rental Yields Across Key Cities

For buy-to-let investors, rental yield is the metric that matters most. It is a simple percentage that indicates the income a property generates annually relative to its value. The formula for gross rental yield is (Annual Rental Income / Property Value) x 100.

In practice, yields vary dramatically from one city—and even one neighbourhood—to another. This is where strategic analysis is crucial.

Johannesburg consistently delivers the highest rental yields in the country. In suburbs with strong demand from corporates or students, it is not uncommon to find gross yields ranging from 8% to over 11%. This is fuelled by a massive tenant pool and property prices that remain relatively affordable.

Cape Town, by contrast, tells a different story. Here, yields are much lower, typically between 4% and 6%. The city’s high property values mean rental income constitutes a smaller fraction of the asset's overall cost. An investment in Cape Town is primarily a long-term play on capital appreciation, with rental income as a secondary benefit.

A high gross yield looks attractive on paper, but it is the net yield that reaches your bank account. This figure accounts for all operating costs—levies, rates, insurance, and maintenance—providing a realistic picture of your investment’s cash flow.

To provide a clearer picture, here is a comparative table of expected gross yields across the major cities.

Average Gross Rental Yields by Major City and Property Type

| City | 2-Bed Apartment Yield | 3-Bed House Yield | Market Driver |

|---|---|---|---|

| Johannesburg | 8% – 11% | 7% – 9% | High tenant demand, affordability |

| Cape Town | 4% – 6% | 3.5% – 5.5% | Capital growth, lifestyle appeal |

| Durban | 6% – 9% | 5% – 8% | Affordability, coastal lifestyle |

These figures provide a solid starting point for comparing opportunities. However, they only tell half the story. To truly understand an investment’s potential, one must calculate the net yield.

Calculating Net Yield: A Practical Example

Let’s analyse a 9.5% gross yield from a Johannesburg apartment to see what happens when real-world costs are factored in. This is how you move from an estimate to a bankable figure.

Consider a typical two-bedroom apartment in a good Johannesburg suburb:

- Property Purchase Price: R1,200,000

- Monthly Rent: R9,500 (Annual Income: R114,000)

- Gross Yield: (114,000 / 1,200,000) x 100 = 9.5%

Now, let's subtract typical monthly expenses:

- Sectional Title Levy: R1,800

- Municipal Rates & Taxes: R700

- Letting Agent Fee (10%): R950

- Maintenance Provision (essential to budget for): R500

- Total Monthly Costs: R3,950 (R47,400 per year)

Your net annual income is R114,000 (rent) – R47,400 (costs) = R66,600.

So, your Net Yield is (66,600 / 1,200,000) x 100 = 5.55%.

The difference between the gross yield of 9.5% and the net yield of 5.55% is significant. It is crucial to obtain accurate estimates for all costs before committing to avoid overestimating returns. For a complete walkthrough of this vital metric, our guide on what are rental yields will give you the confidence to analyse any potential buy-to-let opportunity professionally.

A Foreigner’s Guide to the South African Buying Process

One of the most attractive aspects of investing in South African property is the legal system's accommodating stance towards international buyers. Unlike many countries, South Africa has almost no restrictions on non-residents owning freehold property, granting you the same ownership rights as a local citizen.

In practice, this means you can buy a house, an apartment, or land directly in your own name. Your ownership is then officially recorded and secured at the Deeds Office, a well-established and trusted institution. The process is transparent and regulated, but it has unique steps and rules every foreign buyer must understand.

The Key Professionals on Your Team

To ensure a smooth transaction, you will work with a few key professionals. First is an experienced estate agent, who will act as your representative on the ground, helping you find suitable properties and negotiate the initial Offer to Purchase. This becomes a legally binding contract once signed, so a legal review is advisable.

The most important professional in this process is the conveyancing attorney. Appointed by the seller but legally required to act impartially, their job is to handle the legal transfer of the property title. They verify all paperwork, manage funds in a secure trust account, and lodge the transfer at the Deeds Office. You cannot buy property in South Africa without one.

The Step-by-Step Buying Timeline

Understanding the sequence of events makes the process less intimidating. While every deal varies slightly, a typical purchase follows a clear path from offer to handover.

Make an Offer to Purchase: Once you find a suitable property, you submit a formal written offer. This document outlines the price, conditions (such as financing), and other key terms.

Secure Financing (If Required): If you plan to obtain a mortgage, you will apply to a South African bank. As a non-resident, expect a maximum loan-to-value of 50%. This means you must fund at least half the purchase price yourself as a deposit.

Appoint a Conveyancer and Complete FICA: The conveyancing attorney will request your FICA documents. This is a mandatory identity verification required under the Financial Intelligence Centre Act, designed to prevent financial crime.

Pay the Deposit and Costs: You will transfer your deposit and funds for transaction costs into the conveyancer’s trust account. This covers transfer duty, legal fees, and bond registration costs if you have a mortgage.

Sign the Transfer Documents: The conveyancer prepares all necessary legal documents for you and the seller to sign.

Lodge and Register at the Deeds Office: With all documents in order, the file is lodged at the Deeds Office. This registration process typically takes 8-10 working days, after which the property is officially and legally yours.

Understanding the Costs Involved

Budgeting for transaction costs is crucial to avoid unforeseen expenses. These costs are paid in addition to the purchase price and typically amount to 8-10% of the property's value.

A crucial point for non-resident investors is understanding the flow of money. Foreign investors need a clear understanding of the regulatory landscape, particularly concerning South African Exchange Control Regulations. Properly documenting all incoming funds with the South African Reserve Bank via your bank is essential for the future repatriation of proceeds when you decide to sell.

The main costs to plan for include:

- Transfer Duty: A government tax on property sales. On a R2 million property, for instance, the transfer duty would be approximately R50,250.

- Conveyancing Fees: The legal fees paid to the attorney for managing the transfer, based on a sliding scale set by the legal profession.

- Bond Registration Costs: If you take out a mortgage, a separate attorney registers the bond, and their fees are also based on an official tariff.

For anyone new to buying property overseas, the process can feel complex. Our comprehensive guide on https://www.worldpropertyinvestor.com/how-to-buy-property-abroad/ offers a broader framework that can help you prepare, regardless of the destination. Understanding these fundamental steps is key to a secure and successful investment.

Choosing the Right Property Type for Your Goals

Deciding where to buy is only half the equation. What you choose to buy is just as critical to your success as an investor in South Africa. The market is experiencing a clear and accelerating shift from traditional freestanding houses towards sectional title properties like apartments and townhouses, especially those inside secure complexes.

This trend is a direct response to major market pressures: affordability, security, and a growing desire for a low-maintenance lifestyle. With rising living costs and security a top priority, buyers are favouring properties that offer "lock-up-and-go" convenience in a guarded environment. This is fundamentally reshaping residential development across the country’s urban centres.

The Rise of Sectional Title Properties

Sectional title ownership means you own a specific unit within a larger development, plus a share of the common property (e.g., gardens, pools, security systems). This model has become the preferred choice for first-time buyers, young professionals, and shrewd buy-to-let investors for several compelling reasons.

Data from ooba Home Loans shows that townhouses now account for around 20% of all property purchases in 2024. This reflects intense demand for more affordable housing, particularly in the R800,000 to R1.5 million bracket, which is the sweet spot for new buyers and investors. These properties also appeal to those looking to downsize. You can see how this is reshaping the market in The African Vestor's recent analysis.

For an investor, the advantages of a sectional title are clear:

- Lower Maintenance: The body corporate is responsible for external upkeep, simplifying management.

- Built-in Security: Most complexes have 24-hour security, a major selling point for potential tenants.

- Predictable Costs: Monthly levies cover shared expenses, making budgeting easier.

Sectional titles offer a scalable and relatively straightforward entry point into the South African property market. The consistent demand from both tenants and future buyers makes them a more liquid and predictable asset class compared to larger, high-maintenance freehold homes.

Freehold Homes Versus Sectional Titles

While sectional titles are gathering momentum, traditional freehold homes—where you own both the building and the land it sits on—still have their place. They appeal to a different market segment, offering more freedom but also greater responsibility. It is vital to understand the trade-offs.

Sectional Title (Apartments, Townhouses)

- Pros: Better security, lower purchase prices, shared maintenance costs, and access to amenities.

- Cons: Monthly levies can be high, and you must adhere to the rules of the body corporate, limiting your freedom to make alterations.

Freehold (Freestanding Houses)

- Pros: Complete control over your property, no levies, and more privacy and space.

- Cons: You bear the full burden of maintenance, security, and insurance, which can lead to significant and unpredictable costs.

Gated Estates: The Premier Choice

A powerful sub-trend is the high demand for homes within gated lifestyle estates. These developments offer the best of both worlds: the space and privacy of a freehold home with the top-tier security and communal facilities of a sectional title scheme. They are particularly popular with affluent families and the "semigrants" relocating to the Western Cape and other coastal areas.

Ultimately, your choice of property must align with your investment goals. If your primary objective is to generate consistent rental income with minimal hassle, a sectional title unit in a high-demand urban area is often the smarter bet. If your strategy is focused on long-term capital growth and you are targeting a high-income family tenant, a house in a secure gated estate could be the ideal investment.

Exploring the core principles of a successful buy-to-rent investment will help clarify which path best suits your portfolio and long-term financial ambitions.

Understanding the Risks and Long-Term Outlook

No credible discussion about investing in South African property is complete without a frank assessment of the risks. While the opportunities are real, every market has its challenges. An intelligent investor does not ignore these issues; they understand them, plan for them, and factor them into the investment from day one.

One of the first factors any foreign investor will encounter is the currency. The South African Rand (ZAR) is known for its volatility against major currencies like the pound, dollar, and euro. This means your returns can be affected by more than just property price movements. For example, a 10% capital gain in Rand could shrink to a 5% gain in your home currency—or even become a loss—if the exchange rate moves against you.

Key Risks and Practical Mitigation Strategies

Navigating these challenges is not about avoiding the market but about building a resilient strategy. This means identifying the main risks and implementing practical mitigation measures.

The key risks include:

- Economic and Political Stability: South Africa has ongoing socio-economic hurdles that can affect policy and investor confidence. Monitoring reports from major economic bodies provides crucial context.

- Crime and Security: Security is a major consideration in the property market and directly shapes demand. This has led to sustained demand for homes in secure gated estates and apartment complexes, which often command a rental premium and prove more resilient during market downturns.

- Infrastructure Challenges: The most prominent issue is the electricity supply, with rolling blackouts known as 'loadshedding'. This can be a deal-breaker for tenants unless a property is equipped with backup power, such as an inverter or solar panels.

A savvy investor doesn’t run from these risks—they factor them into their financial model. By focusing on secure, well-managed properties in economically sound areas and perhaps looking into currency hedging tools, you can dramatically de-risk your investment.

The Long-Term Outlook and Fundamental Strengths

Despite the headlines, the long-term fundamentals of the South African property market are what keep seasoned investors engaged. The country has a sophisticated legal framework that strongly protects property rights—a critical safeguard not always found in other emerging markets. The Deeds Office operates a transparent and reliable system for registering title, providing genuine security of ownership.

More importantly, South Africa's demographics provide a powerful tailwind for future housing demand. With a large, young, and rapidly urbanising population, the need for quality housing in economic hubs like Johannesburg and Cape Town is set to grow. This structural demand is the bedrock of the rental market, particularly for affordable and mid-range apartments.

By taking a balanced view—understanding both the risks and the underlying strengths—you can make an informed decision. This allows you to position your investment to ride out short-term volatility while tapping into the country's long-term growth potential. That balanced perspective is the foundation of any successful international property strategy.

Answering Your Key Questions as a Foreign Investor

Once you have identified South Africa as a target market, broad research gives way to practical, operational questions. Clarity on mortgages, taxes, and ownership rules is what turns an idea into a confident investment. Here are answers to some of the most common queries from international buyers.

Can a Foreigner Get a Mortgage in South Africa?

Yes, they can. South Africa's major banks are accustomed to lending to non-residents, but the process is more stringent than for a local buyer.

The biggest difference is the deposit requirement. Banks typically cap their loan-to-value (LTV) ratio at 50% for foreigners. This means you must be prepared to fund at least half the purchase price in cash. For example, on a R2 million property, a cash deposit of at least R1 million would be required.

Approval also hinges on your ability to provide verifiable proof of income from your home country and pass the bank's standard affordability checks.

What Are the Annual Property Taxes and Costs?

Your calculations should not stop at the purchase price. The ongoing costs of ownership are a crucial part of calculating real-world returns. The main recurring expenses are:

- Municipal Rates: This is the local property tax, calculated on the value of the land and buildings, paid to the local municipality.

- Sectional Title Levies: If you buy in an apartment block or townhouse complex, you will pay a monthly levy. This fee covers the upkeep of common areas, security, and building insurance.

- Income Tax: Rental income earned in South Africa is taxable in the country. However, you can deduct all legitimate operating costs—such as rates, levies, and agent fees—to reduce your taxable income.

How Do I Repatriate Funds After Selling a Property?

You can take all capital and profits out of the country, but this requires correct paperwork from the outset. The South African Reserve Bank mandates that when you first bring investment funds into the country, the transaction must be properly documented through an authorised dealer (usually your bank).

When it comes time to sell, this initial documentation is your golden ticket. It proves the funds originated overseas, allowing the conveyancing attorney to get the necessary tax clearance and send the proceeds back to you. Meticulous record-keeping isn't just a good idea here—it's non-negotiable.

Is It Better to Buy in My Personal Name or a Company?

This is a trade-off between simplicity and protection, and the right answer depends on your personal tax position and risk appetite.

Buying in your personal name is the most straightforward route. It is simpler, faster, and involves less administration.

However, setting up a South African company to own the property can create a valuable firewall, separating the asset from your personal finances and limiting your liability. It can also offer advantages for estate planning. The downside is the extra cost and compliance of running a company.

It is absolutely essential to seek professional tax and legal advice on this point to determine which structure will serve you best.

At World Property Investor, we provide the clarity and data-driven insights you need to confidently navigate international markets. Explore our in-depth guides to find your next global property investment at https://www.worldpropertyinvestor.com.