You're probably looking at two listings right now. One has stronger monthly rent. The other looks cheaper to buy. On paper, both seem investable.

That's where most new landlords make their first mistake. They compare properties by rent alone, not by how efficiently each property turns purchase price into income after costs, vacancies, and friction. A flat that looks “high income” can still be a weak investment if too much of that rent leaks out through fees, maintenance, and empty periods.

Rental yield is the metric that brings discipline to that decision. It gives you a common language for comparing a city-centre flat in Manchester, a suburban house in Birmingham, or an apartment in an emerging overseas market. It stops you confusing a busy rent roll with actual return.

What Is Rental Yield and Why Does It Matter

A landlord buys a flat in Leeds for a modest price and collects steady rent from day one. Another buys in central London, charges more per month, and still ends up with less cash left over after costs. The difference is yield.

Rental yield measures how hard a property works as an income asset. It shows the annual rent as a percentage of what you paid for the property, or what the property is worth today. In practice, investors look at yield because rent alone can be misleading. A higher monthly figure does not automatically mean a better investment if the purchase price, running costs, or vacancy risk are also higher.

That matters even more once you move beyond headline figures and focus on the money that ultimately reaches your bank account.

In mature markets such as the UK, the drag usually comes from management fees, repairs, compliance, insurance, and periodic voids. In higher-growth emerging markets, the headline yield can look stronger, but the risks often shift. Currency volatility, weaker tenant enforcement, title issues, and inconsistent maintenance standards can eat into what looked like an attractive return. On paper, two properties can show a similar gross yield. In reality, their real net yield can be miles apart.

Why investors start with yield

Yield is the first filter because it answers a basic commercial question. Is this property producing enough income for the capital tied up in it?

When I review deals with clients, I use yield early because it helps cut through sales language and compare unlike assets quickly. A small terrace in Liverpool, a new-build flat in Birmingham, and an overseas apartment in a fast-growing city all come with different stories. Yield gives you one common measure before you spend time on the finer details.

It is also one of the fastest ways to test whether a deal is being marketed accurately.

- Income efficiency: It shows whether the rent is strong relative to the purchase price.

- Comparability: It lets you assess very different properties on the same basis.

- Reality check: It exposes listings where “strong rental demand” does not translate into a strong return after costs.

For investors who want more than a one-off purchase, yield sits inside a broader plan for building long-term wealth through property investment.

Why yield still needs context

Yield is useful, but it is not the whole investment case. It will not tell you whether the local market has pricing power, whether regulation is tightening, or whether the quoted rent is optimistic. It also will not tell you how painful the downside looks if the property sits empty or needs capital works.

That is why experienced investors pay close attention to net yield, not just gross yield. The gross number gets attention in listings. The net number is closer to what you keep. If you want a second perspective on that distinction, these expert tips on rental yield give a useful breakdown.

Used properly, rental yield is not a shortcut. It is a discipline. It helps you compare deals faster, ask better questions, and stay focused on real income rather than brochure numbers.

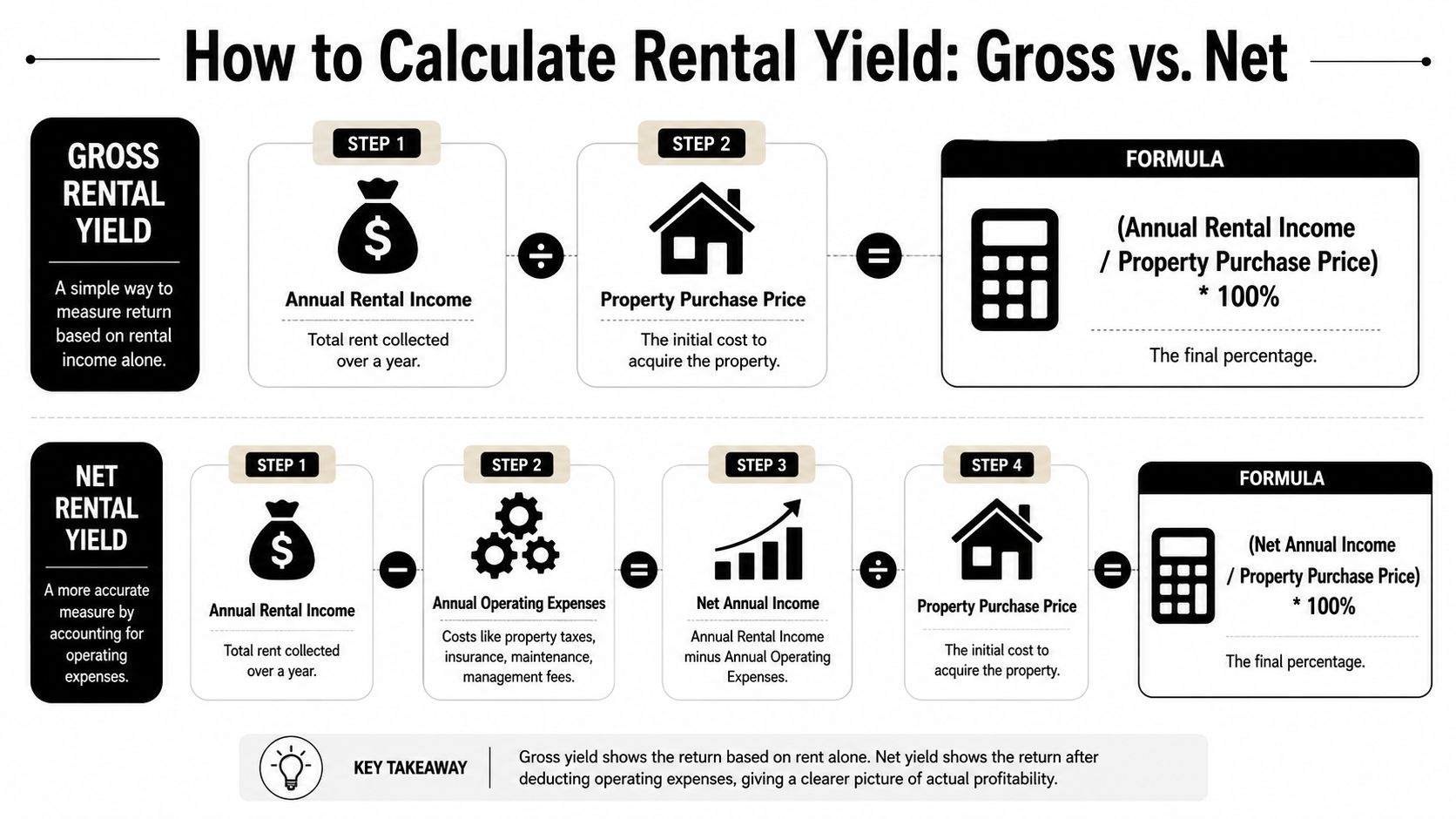

How to Calculate Rental Yield Gross vs Net

A listing shows a clean 6% yield. On paper, it looks bankable. Then the first year brings letting fees, a few repair callouts, insurance, a service charge, and a void period. The number you feel in your bank account is much lower.

That gap is why serious investors calculate two figures from the start.

- Gross rental yield = annual rent ÷ purchase price (or current market value) × 100

- Net rental yield = annual rent minus annual operating costs, then ÷ purchase price (or current market value) × 100

Gross yield helps you screen deals fast. Net yield shows what the asset is likely to produce after the routine costs of owning it. In mature markets such as the UK, those costs are often more predictable but harder to ignore because compliance, management, and service charges can eat into income quickly. In higher-growth emerging markets, the headline yield may look stronger, but cost control, vacancy risk, currency shifts, and local execution can make the actual net number less stable.

Here is the simplest way to run both calculations on the same property.

Assume a flat costs £250,000 and rents for £1,250 per month. Annual rent is £15,000. Gross yield is:

- £15,000 ÷ £250,000 × 100 = 6%

That is the brochure figure.

Now price the property like an operator, not a marketer. Add the recurring costs that reduce spendable income:

- Letting and management fees

- Landlord insurance

- Repairs and routine maintenance

- Safety certificates and compliance

- Service charge or block fees

- Vacancy allowance

- Admin and accountancy

If those costs come to £4,000 for the year, net income falls to £11,000. Net yield is:

- £11,000 ÷ £250,000 × 100 = 4.4%

That 4.4% is the figure worth underwriting.

The gross number still has a job. It lets you compare ten listings quickly and discard weak stock without building a full model on every address. But once a deal gets serious, gross yield stops being enough. I tell clients to treat gross yield as a filter and net yield as the decision metric.

A simple table makes the distinction clear:

| Metric | What it includes | Best use |

|---|---|---|

| Gross yield | Rent only | Fast screening across multiple deals |

| Net yield | Rent minus operating costs | Assessing true income potential |

Investors new to cross-border property often miss how location changes the cost stack. A UK flat may have tighter regulation, more transparent data, and steadier rent collection, but fees and compliance can compress net yield. An apartment in an emerging market may advertise a higher gross return, yet weaker tenant enforcement, patchier management, or extra ownership friction can make the cash result less predictable. The formula stays the same. The assumptions do not.

For a second check against your own model, these expert tips on rental yield are a useful reference.

Use this process every time:

- Verify achieved rent, not just the asking rent

- Annualise income based on realistic occupancy

- List every recurring operating cost

- Include a vacancy allowance even in strong rental areas

- Calculate net yield

- Stress-test the deal with softer rent or higher costs

If you want to compare multiple properties quickly, a rental yield calculator for gross and net returns can save time. The quality of the result depends on the assumptions you enter.

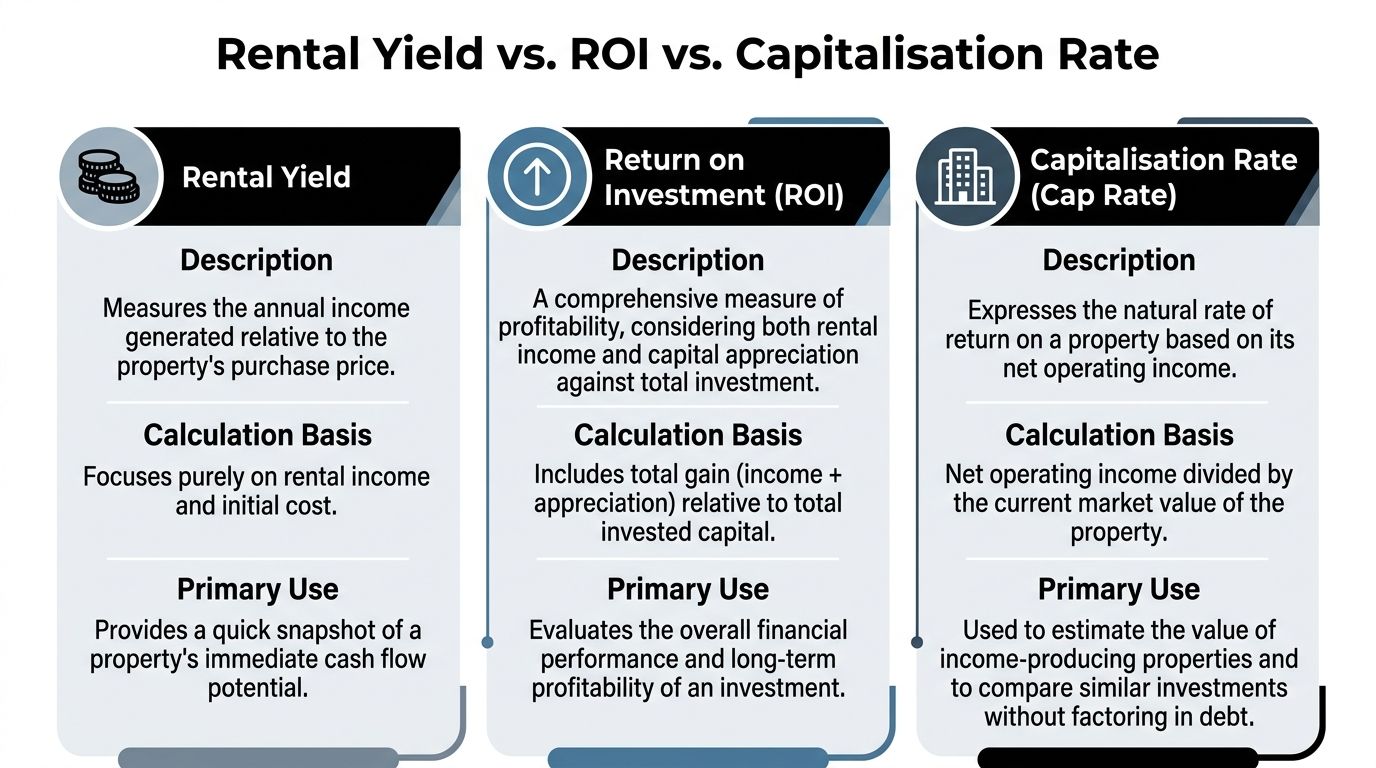

Yield vs ROI and Capitalisation Rate

Investors often use these terms as if they mean the same thing. They don't. Each metric answers a different question.

Three metrics, three jobs

Think of them like three lenses on the same property.

| Metric | What it tells you | When to use it |

|---|---|---|

| Rental yield | How efficiently the property generates annual rent relative to value | Early screening and income comparison |

| ROI | The broader profitability of the investment | Full investment review |

| Capitalisation rate | The property's unleveraged income return based on net operating income and current value | Commercial assets and debt-neutral comparisons |

Rental yield is the quickest lens. It's useful when you need to compare a batch of potential deals and narrow the field.

ROI is wider. It pulls in more of the financial picture, often including income, purchase costs, improvement costs, finance structure, and eventual capital growth. Yield is one part of ROI, not a substitute for it.

Cap rate sits closer to net yield in spirit, but investors often use it in commercial property, blocks, and larger income-producing assets where debt is deliberately excluded to compare the underlying asset itself.

Where investors get confused

The usual mistake is trying to force one metric to do every job.

- A landlord shopping for a buy-to-let flat may start with yield.

- An investor reviewing whether a refurbishment was worth doing needs ROI.

- A buyer comparing two income-producing buildings on a debt-free basis may lean on cap rate.

That's why good analysis is layered, not one-dimensional.

A simple way to remember it

Use this shorthand:

- Yield asks, “What income does this asset produce relative to price?”

- ROI asks, “Was this investment worth the money and effort overall?”

- Cap rate asks, “What return does the property produce before debt enters the picture?”

If you want to go deeper on the broader return picture, this guide on how to calculate return on investment for property is the right companion metric to pair with yield.

Investor mindset: Yield helps you buy well. ROI helps you judge whether the whole strategy worked.

Decoding Real Net Yield Beyond the Formula

A property can look strong on a portal and still disappoint once the rent starts landing in your account. I see this most often with buyers who underwrite to the advertised rent, strip out only the obvious bills, and treat the gap as profit.

Net yield only becomes useful when the cost assumptions are honest.

The costs that actually reduce your return

The main question is simple. What income will still be there after the property has been run properly for a full year?

That means using achieved rent where you can verify it, not the highest asking rent in the building. It also means budgeting for the ordinary friction that comes with ownership, including management, repairs, compliance, insurance, leasehold charges, and periods without a paying tenant.

This principle applies in every market. For example, an analysis from CostiCohen on gross versus net rental yield shows how quickly routine costs and vacancy assumptions can pull headline yield down once a property is modelled on a realistic basis. The exact percentages will vary by country, but the lesson does not. Small gaps between gross and net can decide whether a deal produces dependable cash flow or constant top-ups from your own pocket.

Before buying, I would pressure-test these lines:

- Letting-agent fees: Full management, tenant-find, renewals, and check-out costs all reduce usable income.

- Maintenance reserve: Every property needs one. Older stock usually needs a larger one.

- Landlord insurance: A direct cost of staying protected.

- Service charges and ground rent: Common with flats and often underestimated in leasehold stock.

- Compliance spending: Safety certificates, licensing, inspections, and legal updates all carry a cost.

- Void periods: Lost rent is only part of the hit. Cleaning, remarketing, and minor re-letting works often follow.

- Tax treatment: This sits outside the operating calculation, but it changes what you keep.

Why mature markets and emerging markets produce different net outcomes

In the UK, costs are usually easier to identify before you buy. Management fees are clearer, compliance rules are better defined, and historic rent data is often easier to check. That makes underwriting cleaner, but it also means there are fewer places to hide a weak deal. If the margin is thin, the numbers will show it.

In higher-growth emerging markets, the headline yield can look stronger at first glance. Entry prices may be lower relative to rent, which helps the top-line figure. The trade-off is that more of the risk sits in execution. Local management quality, legal enforcement, currency movement, resale liquidity, and building standards can all change the net result you collect.

That is the comparison serious investors need to make. Higher headline yield does not automatically mean higher retained income. A lower-yield market with tighter operations can leave you with more predictable cash flow than a high-yield market with poor collection, weak maintenance control, or slow exits. If you want to compare those trade-offs market by market, this guide to rental yield by country is a useful starting point.

Build your model conservatively

A workable underwriting model is usually a conservative one.

- Use achieved rent where possible

- Add a vacancy allowance that reflects local letting conditions

- Budget routine maintenance every year, even in newer property

- Separate recurring operating costs from one-off buying costs

- Check local tax treatment before relying on the projected cash flow

If you also invest in markets where depreciation affects after-tax returns, this ADU depreciation schedule is a helpful reference point for thinking about cost timing and what reaches your bank account after ownership expenses are accounted for.

What works in practice

The investors who hold up best over time usually do the dull things well. They use conservative rent assumptions, keep cash reserves, verify service charges before exchange, and budget for repairs before a tenant calls.

Underwriting from a brochure causes most of the pain. Asking rent is not contracted income. Gross yield is not cash flow. A deal only works if the net income still looks attractive after the boring costs, the missed months, and the local risks have all been priced in.

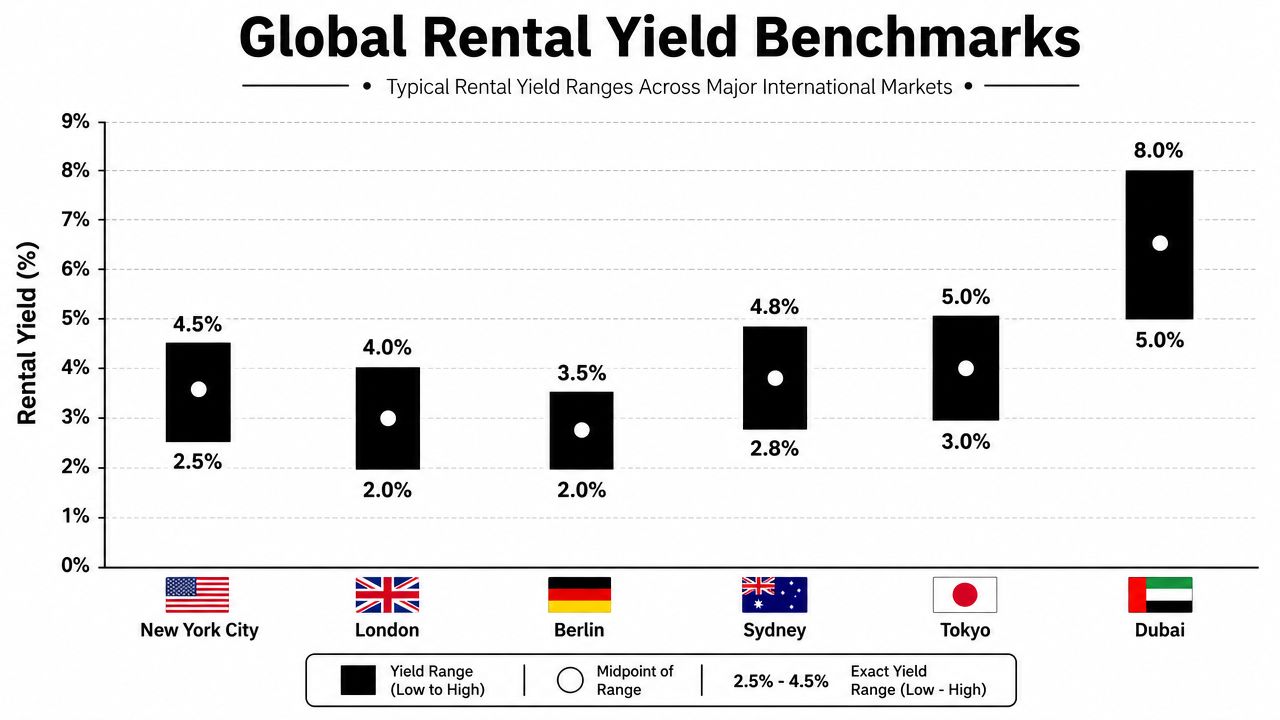

Rental Yield Benchmarks A Global Comparison

Two properties can both show a 7 percent gross yield on a spreadsheet and leave you with very different cash flow at the end of the year. One sits in a mature market with tighter regulation, better debt options, and predictable resale demand. The other sits in a faster-growth market where entry prices are lower, rents look stronger, and the operational risk is higher. The number is the same. The bank balance usually is not.

Why comparisons need context

A good benchmark starts with what kind of market you are buying into.

In established markets such as the UK, Germany, or Canada, investors often accept lower headline yields because financing is easier to arrange, ownership rights are clearer, and exit routes tend to be stronger. Those factors do not increase rent, but they can reduce costly mistakes and make your net income more dependable.

Emerging markets can produce stronger rent-to-price ratios. That is the part that attracts attention. The harder part is what sits underneath: patchier market data, more hands-on management, currency exposure, and a wider gap between advertised performance and what lands in your account after local costs and friction.

That is why a useful comparison is not just yield versus yield. It is net income, risk, and execution quality together.

The UK shows why headline yield can mislead

The UK is a good reference point because the market is transparent enough to benchmark properly, yet still full of local variation. National rental and house price series from the Office for National Statistics and the UK House Price Index make it easier to compare broad trends, but those averages still hide the core investment question.

A landlord in Manchester, Leeds, or Glasgow may see a very different net yield from a landlord in London or the South East, even when tenant demand looks healthy in both places. Service charges, licensing rules, maintenance intensity, financing terms, and void risk all change the outcome. In practice, mature markets often trade some headline yield for better visibility on costs and easier exits.

That trade can be sensible.

How to compare one market with another

Use a framework that reflects what you are trying to keep, not what an agent can print on a brochure.

- Headline yield: Start with the gross figure, but treat it as a screening tool only.

- Net operating reality: Estimate recurring costs in local terms, including management, maintenance, taxes, insurance, service charges, and realistic vacancy.

- Risk-adjusted cash flow: Ask how stable that net figure is if regulation changes, a tenant leaves, the local currency moves, or you need to sell faster than planned.

A key distinction often emerges between mature and emerging markets. Mature markets often give you more certainty around enforcement, financing, and resale liquidity. Higher-growth markets can give you stronger gross income, but the spread between projected yield and real net yield is often wider.

If you want a broad starting point, this country-level comparison of rental yield by country is useful for spotting where headline returns sit. Treat it as the first filter, not the final decision.

For overseas buyers looking at the Caribbean, Latin America, or similar markets, local execution matters as much as the quoted return. This guide for foreign real estate investors is the kind of market-specific reading worth reviewing before relying on an attractive advertised yield.

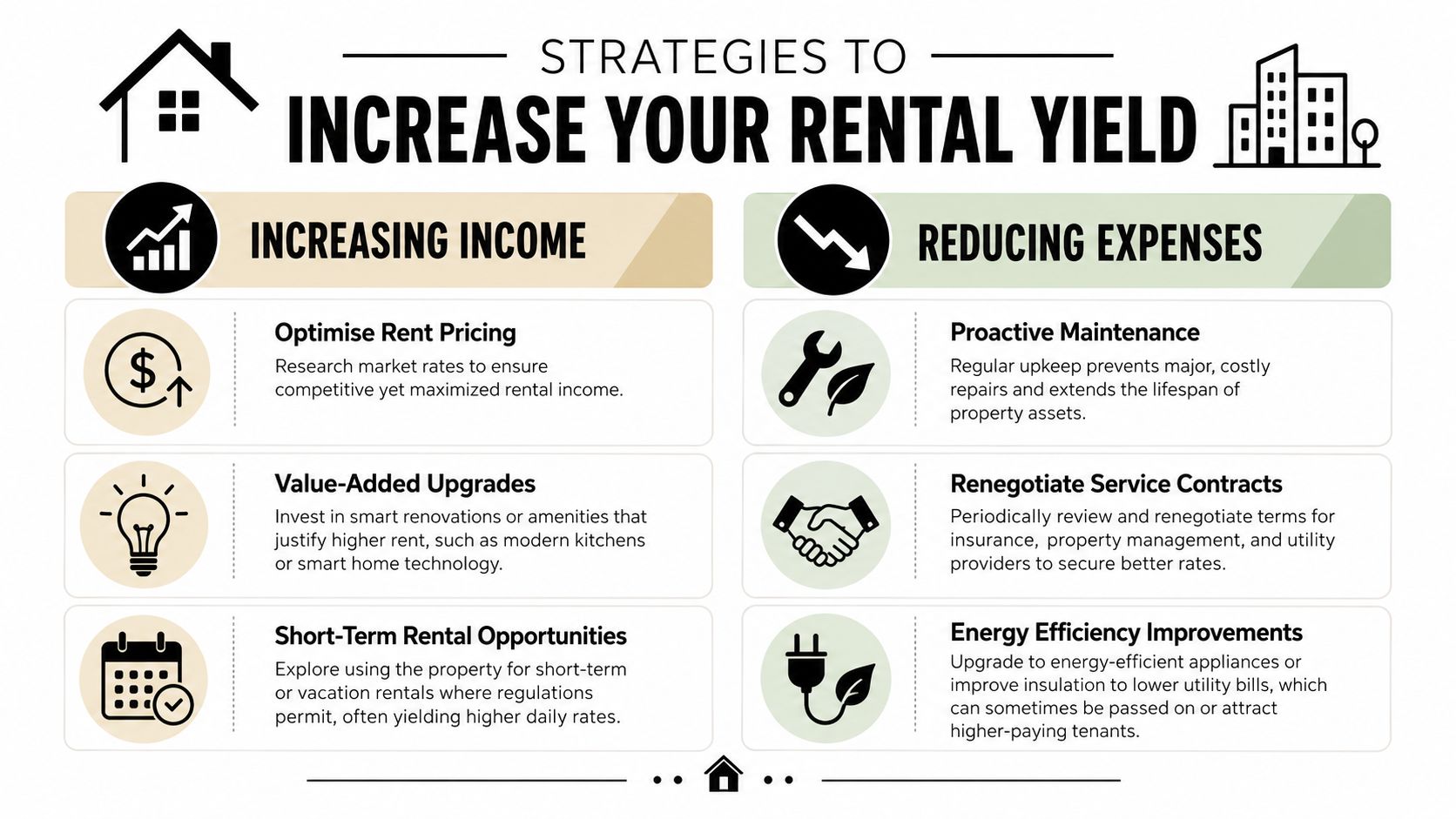

Actionable Strategies to Increase Your Rental Yield

Most yield improvement comes from operational decisions, not miracles. You either raise sustainable income, reduce avoidable cost, or do both.

Increase income without damaging tenant demand

A lot of landlords jump straight to “put the rent up”. Sometimes that works. Often it just increases churn.

Better options tend to be more targeted:

- Improve the offer, not just the price: A clean refurb, better lighting, modern flooring, or practical storage can justify stronger rent more reliably than cosmetic flash.

- Match the product to the tenant type: A professional sharer property, a furnished city flat, and a family house should not be presented or managed the same way.

- Reduce friction in the letting process: Faster response times, better photos, cleaner move-in condition, and clear tenancy terms can reduce voids and improve achieved rent.

- Add useful features: Secure parking, broadband readiness, white goods, or energy-efficiency improvements often matter more than expensive decorative upgrades.

This video gives a useful practical overview of ways landlords think about improving return:

Cut costs that don't improve the asset

Reducing expenses is usually less glamorous and more reliable.

- Review management structure: Some landlords pay for full management when a lighter service would do. Others self-manage badly and create bigger costs through mistakes.

- Challenge recurring charges: Insurance, maintenance contracts, and block-related charges deserve regular review.

- Use preventative maintenance: A small repair done early is usually cheaper than a neglected problem that grows.

- Standardise replacements: Keeping consistent appliance models, paint colours, and fittings across a portfolio simplifies maintenance and lowers hassle.

Field note: Net yield usually improves faster from disciplined cost control than from aggressive rent pushing.

Focus on changes tenants will pay for

Not every improvement deserves capital. Good upgrades either protect the building, reduce future cost, or support higher achieved rent from the right tenant profile.

A practical decision test is simple:

| Upgrade type | Usually worthwhile when | Often poor value when |

|---|---|---|

| Kitchen or bathroom refresh | Existing finish is tired and clearly holding back rent | You're over-specifying for the local tenant base |

| Energy improvements | Bills, comfort, or lettability are affected | The upgrade is expensive with no rent or demand benefit |

| Furniture package | Tenant profile expects furnished stock | Local demand is mainly for unfurnished lets |

For more ideas on improving investment performance at property level, these tips for investment property are a useful starting point.

The High Yield Trap and How to Avoid It

A listing shows 11% gross yield in an emerging market and 5% in a solid UK city. On paper, the 11% looks like the obvious winner. In practice, the cheaper asset can demand far more management, suffer longer voids, carry weaker tenant covenants, and produce less reliable cash in your bank account.

That is the high-yield trap.

Headline yield rises for a reason. Sometimes the reason is positive, such as a landlord buying well in an undersupplied rental area. Often, though, the market is pricing in a problem. It may be a secondary location, older stock with recurring repairs, weak resale demand, political or currency risk, or a tenant base that turns over too often. Mature markets like the UK usually offer lower gross yields but more predictable operating conditions. Higher-growth markets can offer stronger rent multiples, but they often come with wider swings in costs, vacancy, enforcement, and exit liquidity.

The practical mistake is treating all yield as equal. It is not. A 7% gross yield with stable occupancy, enforceable leases, and controlled costs can outperform a 10% gross yield that leaks cash through voids, bad debt, service charges, or repeated refurbishments.

Before buying, pressure-test the income story from several angles:

- Why is the yield high in this location?

- Who makes up the tenant base, and how stable is demand in a weaker market?

- What happens to net yield after management, maintenance, taxes, insurance, and vacancy?

- How easy is it to sell if local conditions or regulation change?

- Would you still want this asset if rent growth slows and capital growth disappoints?

One more point matters. Chasing a slightly higher yield does not always improve the overall investment result. If the trade-off is poorer asset quality, weaker financing options, more operational hassle, or slower long-term growth, the extra percentage on day one can be expensive.

Good investors still care about yield. They just judge it in context. The target is durable net income, manageable risk, and an asset you can hold with confidence when the market gets tougher.

If you want help comparing markets, stress-testing net yield assumptions, and finding property opportunities that make sense on more than just a headline percentage, explore the research and guides available at World Property Investor.