When you compare rental yield by country, a clear pattern emerges. Emerging markets in regions like Africa and Latin America often exhibit gross yields north of 8-10%, whilst the established, mature markets of Western Europe and North America typically offer a more modest 3-5%. That differential highlights the fundamental trade-off every global investor must weigh: higher potential income versus higher risk.

Understanding Rental Yield: A Core Metric for Global Investors

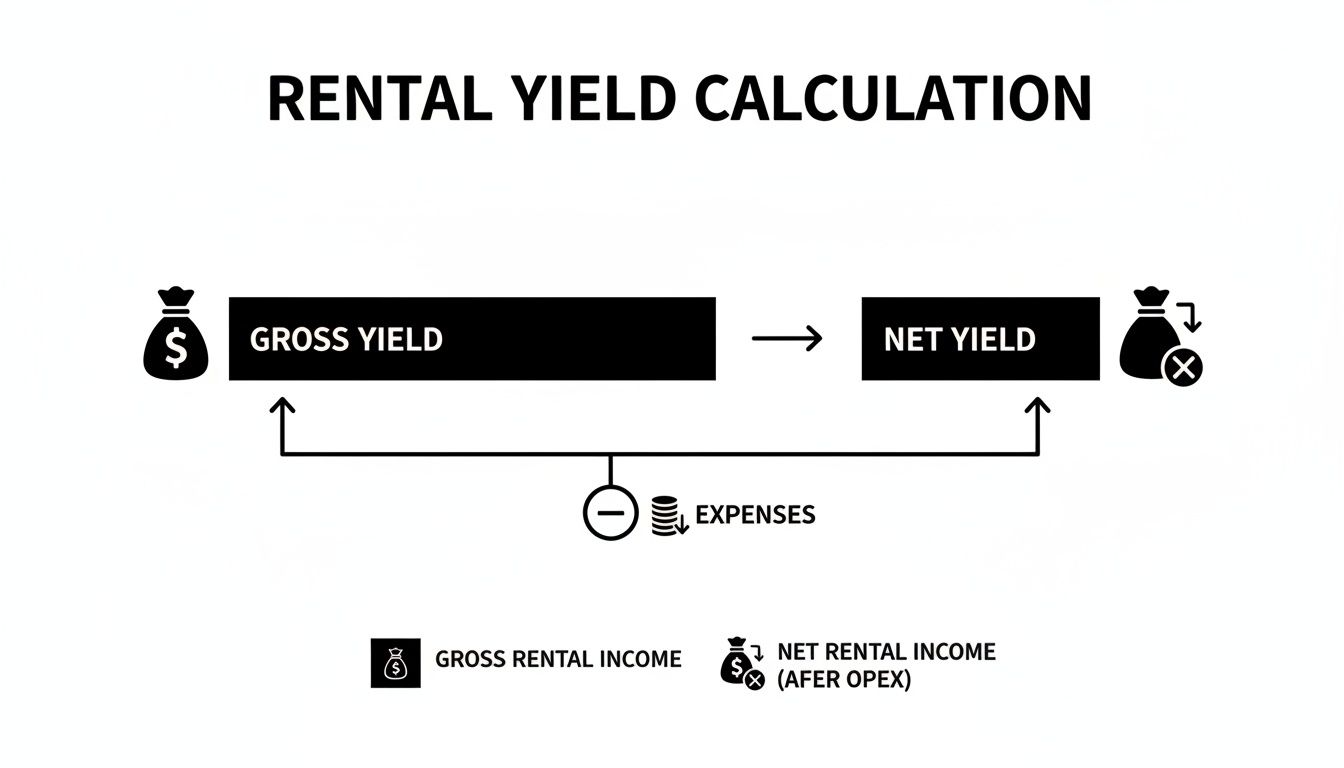

For any serious property investor, rental yield is a foundational metric. It is the most direct way to gauge an asset's income-generating performance. In essence, it shows your annual rental income as a percentage of the property's total cost, providing a clean snapshot of its efficiency before considering capital growth.

However, relying on a single headline number can be misleading. It is crucial to distinguish between the two main types of yield:

- Gross Rental Yield: This is the preliminary, high-level calculation. You simply divide the total annual rent by the property's purchase price. It is useful for a quick initial comparison but ignores all the real-world costs associated with property ownership.

- Net Rental Yield: This is the figure that truly matters. It is a much more accurate reflection of performance because it subtracts all annual running costs—such as maintenance, insurance, management fees, and potential void periods—from the rental income before the calculation.

Why Net Yield Paints the Truer Picture

Relying solely on gross yield is a common error for new investors. Consider two properties in different countries, purchased for the same price and generating identical rent. They can deliver vastly different returns once local taxes and operational costs are factored in. A flat in a country with high service charges, for example, will see its profitability significantly eroded.

An investor who fails to calculate net yield is operating with incomplete data. It is the only way to accurately compare the true cash flow potential of properties across different international markets.

Let's examine a simple, practical comparison to see how this plays out:

| Metric | Property A (Established Market) | Property B (Emerging Market) |

|---|---|---|

| Purchase Price | £300,000 | £300,000 |

| Annual Rent | £15,000 | £24,000 |

| Gross Yield | 5.0% | 8.0% |

| Annual Expenses | £3,000 | £9,000 |

| Net Rental Income | £12,000 | £15,000 |

| Net Yield | 4.0% | 5.0% |

As you can see, Property B’s attractive gross yield is tempered by higher expenses, which narrows the profitability gap considerably. This demonstrates why a deeper, more detailed analysis is essential.

Knowing how to properly calculate the return on investment (ROI) for real estate is the first step toward building a successful global portfolio. It compels you to be methodical about every cost impacting your bottom line, enabling you to make strategic, data-driven decisions beyond headline figures.

Comparing Global Rental Yields: A Snapshot Of Top Performers

Scanning the global property market reveals a wide spectrum of rental yields. Some countries consistently post headline figures that appear incredibly lucrative, while others offer more modest, stable returns. Understanding this landscape is the first step toward identifying regions that align with your investment strategy.

The primary distinction lies between established and emerging markets. Mature economies like Germany or France tend to have high property prices and robust tenant protections, which naturally compresses yields into the 3-5% range. Conversely, emerging markets in regions like Latin America or Southeast Asia can offer gross yields exceeding 8%, often driven by lower acquisition costs and surging rental demand from rapid urbanisation.

This diagram illustrates the difference between the headline figure (gross yield) and the number that truly impacts your finances (net yield).

As it shows, the journey from an attractive gross yield to a realistic net figure requires accounting for all running costs—and these can vary significantly from one country to the next.

Top Countries By Average Gross Rental Yield

To provide a practical starting point, here is a look at countries that often appear at the top of global rankings. These figures are averages and will fluctuate based on city-specific trends and economic shifts, but they highlight the clear divide between different market types.

| Country | Average Gross Yield (%) | Example City Yield (%) | Market Type |

|---|---|---|---|

| South Africa | 9.0% – 11.0% | Johannesburg: ~10.5% | Emerging |

| Colombia | 7.5% – 9.5% | Bogotá: ~8.2% | Emerging |

| Philippines | 6.0% – 8.0% | Manila: ~7.1% | Emerging |

| United Arab Emirates | 5.5% – 7.5% | Dubai: ~6.8% | Emerging |

| Portugal | 5.0% – 7.0% | Lisbon: ~5.9% | Established |

| United Kingdom | 4.5% – 6.5% | Manchester: ~6.2% | Established |

| Netherlands | 4.0% – 6.0% | Amsterdam: ~4.7% | Established |

This data immediately shows that the highest potential rental income is often found outside traditional Western European and North American markets. It is a clear illustration of how emerging economies can deliver stronger cash flow, at least on paper.

A high rental yield is not an automatic sign of a superior investment. It is often a reflection of perceived risk. The highest yields frequently represent a premium the market offers to compensate investors for currency volatility, political uncertainty, or less predictable legal systems.

Understanding The Yield-Risk Relationship

The most important takeaway for any investor is that yield and risk are two sides of the same coin. A country offering a 10% gross rental yield may seem more appealing than one offering 4%, but that rarely tells the whole story. The higher figure could be masking significant underlying challenges.

For instance, high yields in some emerging markets might be accompanied by:

- Currency Fluctuation: Sharp devaluations can erode your rental income and capital when converted back to your home currency.

- Political Instability: Sudden changes in government policy, property ownership laws, or tax rules can negatively impact your returns overnight.

- Economic Volatility: Markets heavily reliant on a single industry, such as tourism or oil, can experience dramatic swings in rental demand.

In contrast, the lower yields in a market like the UK are essentially the price paid for stability. Investors accept a smaller income return in exchange for a strong legal system, transparent acquisition processes, and a historically resilient property market. This is why such locations remain a cornerstone for conservative portfolios focused on long-term wealth preservation. To see how this risk-reward balance plays out, you can learn more about some of the best countries to invest in property.

Ultimately, this high-level snapshot is not a definitive guide but a starting point for deeper due diligence. The goal is to use these yield figures to identify potential markets, then proceed to a much more detailed analysis of the underlying economic and political factors driving those returns.

Established Markets: Analysing Yields In The UK And Europe

For many global investors, the established property markets of the United Kingdom and Western Europe form the bedrock of a balanced portfolio. These are regions defined by economic stability, transparent legal systems, and mature real estate sectors. However, that security almost always comes with a trade-off: lower rental yields compared to their emerging market counterparts.

This yield compression is a natural consequence of market maturity. High property prices, driven by decades of consistent demand and limited housing supply, mean the initial capital outlay is significant. When combined with slower rental growth and robust tenant protection laws, the rental income as a percentage of the property’s value naturally settles in a more modest range, often between 3% and 5% net.

The UK: A Market Of Contrasting Opportunities

The United Kingdom is a perfect case study in the nuances of an established market. While a national average provides a useful benchmark, it masks a landscape of dramatic regional differences. Major economic hubs do not perform uniformly; yields in London are notoriously compressed by some of the highest property values on the planet, often struggling to surpass 3-4% gross.

In stark contrast, other major UK cities offer a far more attractive proposition for income-focused investors. Northern cities like Manchester and Liverpool, alongside Scottish powerhouses such as Glasgow, consistently deliver healthier returns. These areas benefit from lower purchase prices, large student populations, and ongoing urban regeneration projects that sustain high rental demand.

The key takeaway for investors is that a single country, especially one as economically diverse as the UK, should never be treated as a single market. Lucrative returns are often found by looking beyond the capital and identifying regional hubs with strong local economic drivers.

This highlights a critical principle of investing in established markets. You may sacrifice the headline-grabbing yields of developing economies, but you gain access to stable political systems, clear property laws, and the potential for steady, long-term capital growth.

A Look At The Numbers Across The UK

Recent data from sources like the Office for National Statistics (ONS) shows just how significant these regional differences are. While the national average yield is a solid indicator of market health, drilling down into specific cities is where opportunities appear.

For example, while London yields remain low, cities in the North West and Scotland often lead the UK. Data consistently shows locations like Glasgow and Manchester offering gross yields well above the national average, driven by a mismatch between rental demand and housing supply. This makes them prime targets for investors prioritising cash flow within a stable G7 economy.

Germany And France: Stability Over High Income

The story is much the same in other major European economies like Germany and France. Both countries are known for their strong tenant rights and regulatory environments that prioritise housing stability. In Germany, for instance, rent control mechanisms in major cities like Berlin and Munich are common, placing a ceiling on how quickly rental income can grow.

This regulatory environment, combined with high property values, means investors should expect gross yields to average between 2.5% and 4.5%. The appeal here is not high cash flow but exceptional stability. The German economy is Europe's largest, and its property market is famously resilient to economic shocks, making it a safe haven for capital preservation. To pinpoint high-performing pockets within these stable markets, it’s worth exploring detailed guides on the best buy-to-let locations that analyse local fundamentals.

Ultimately, established markets demand a different mindset. Investors are not chasing the highest possible monthly income. Instead, they are buying into legal security, economic predictability, and the high probability of long-term capital appreciation, making these countries an essential component of any diversified global property strategy.

Emerging Markets: The Pursuit Of Higher Yields

While established markets offer stability, the search for high rental yields often leads investors to emerging economies. For those with a higher risk appetite, regions across Southeast Asia, Latin America, and Eastern Europe frequently top global charts for rental income potential, promising significantly greater returns.

These markets are typically defined by rapid economic growth, a burgeoning middle class driving rental demand, and lower property prices compared to their Western counterparts. An influx of expatriates or a booming tourism sector can further create a fertile environment for buy-to-let investors. However, this potential for high income is invariably linked to a unique set of challenges.

High Yields Meet High Volatility

The fundamental trade-off in emerging markets is simple: you accept higher risk for the chance of higher reward. These are not abstract risks; they are practical factors that can directly impact net returns and must be thoroughly understood before committing capital.

Key risks include:

- Currency Volatility: A sharp depreciation in the local currency against your home currency can easily erode—or even eliminate—rental profits. It can also diminish the value of your capital when you eventually decide to sell.

- Political and Economic Instability: Sudden changes in government, new property ownership laws, or unexpected economic downturns can create an unpredictable investment climate.

- Less Predictable Legal Frameworks: Property rights may not be as robustly protected as they are in established markets. Navigating legal disputes can become a complex and frustratingly slow process.

Real-World Scenarios From High-Yield Markets

To understand the dynamic between opportunity and risk, let’s look at two common scenarios faced by investors in these markets.

Scenario One: The Success Story in Southeast Asia

An investor acquires a condominium in a high-growth area of a major Southeast Asian city. The local economy is booming, driven by foreign investment and a growing tech sector, which creates strong rental demand from young professionals and expats. The investor achieves a gross rental yield of 8.5%. Thanks to a stable political environment and favourable exchange rates, their net returns remain strong when converted back to pounds sterling.

Scenario Two: A Cautionary Tale from Latin America

Another investor is attracted by a 10% gross yield on a coastal property in a popular Latin American tourist destination. Initially, the returns are excellent. However, an unexpected election result leads to political instability and a currency crisis, causing the local currency to devalue by 30%. Suddenly, the impressive local rental income is worth significantly less, and new foreign ownership regulations create uncertainty about the future of their investment.

The lesson is clear: in emerging markets, high rental yield is only the starting point. Extensive due diligence into the political climate, economic forecasts, and legal protections is not just recommended—it is absolutely essential for long-term success.

A Framework for Assessing Opportunity

While the risks are real, the rewards can be transformative for a well-diversified portfolio. Countries like South Africa, Colombia, and the Philippines consistently show strong yield potential, often exceeding 7-9% in major urban centres. These figures are driven by fundamental supply-and-demand imbalances that are unlikely to change overnight.

Investors considering these markets must adopt a rigorous approach. This means looking beyond the headline yield and assessing the underlying drivers of the local economy. Researching the top emerging property investment markets can provide a structured starting point for your analysis.

Success in these regions requires a higher tolerance for risk, a long-term perspective, and a willingness to conduct deep, on-the-ground research before making any commitments.

The Key Factors That Influence National Rental Yields

To accurately compare rental yields by country, you must look beyond headline percentages. A high yield figure means very little without understanding the fundamental forces shaping that nation's property investment climate. These underlying factors determine not only your potential income but also the long-term security of your asset.

A clear grasp of these drivers provides a practical framework for analysis, allowing you to dissect any market's potential. Let's walk through the four critical pillars that influence rental returns on a national scale.

Economic Stability and Interest Rates

The macroeconomic environment is arguably the most powerful force affecting any property market. A country's economic stability, GDP growth, and employment rates directly influence rental demand and affordability. More specifically, the policies set by a nation's central bank have a profound impact on rental yields.

When central banks lower interest rates to stimulate the economy, borrowing becomes cheaper. This often sparks a surge in property purchases, inflating house prices at a pace that rental growth cannot match. This dynamic directly squeezes rental yields, as the purchase price (the denominator in your yield calculation) grows much faster than the rental income (the numerator).

This trend has played out in many established markets. Analysis from bodies such as the Bank of England shows that over recent decades in the UK, rental yields have seen a substantial decline as house prices surged relative to rental growth. This phenomenon was largely attributed to a sustained drop in real risk-free interest rates, which compressed landlord returns. You can discover more about how these economic policies impacted the UK property market.

Taxation Regimes

Tax is one of the biggest variables that can turn an attractive gross yield into a disappointing net return. Each country has a unique tax regime for property investors, and these rules must be scrutinised before making an investment.

The key taxes to analyse include:

- Property Taxes: Annual taxes levied by local authorities (e.g. council tax in the UK), which can vary significantly even between cities in the same country.

- Income Tax on Rent: The rate at which your rental income is taxed. Some countries offer more generous deductions for expenses than others.

- Capital Gains Tax (CGT): The tax you will pay on your profit when you eventually sell the property. High CGT can seriously diminish your total return on investment.

Forgetting to account for the full tax burden is a critical error. A country with zero income tax on rent but high annual property taxes may be less profitable than a country with moderate taxes across the board.

Investment Climate Comparison: Key Influential Factors

To see how these factors play out in the real world, this table offers a snapshot comparison of the investment climate in an established market (the UK) versus two distinct emerging markets (the UAE and the Philippines). It highlights just how differently taxation, regulation, and economic conditions can impact your bottom line.

| Factor | United Kingdom (Established) | UAE (Emerging) | Philippines (Emerging) |

|---|---|---|---|

| Property Tax | Council Tax is levied on tenants, not landlords. Landlords pay a 3% Stamp Duty surcharge on purchase. | No annual property tax. One-off registration fees apply (e.g., 4% in Dubai). | Annual Real Property Tax (RPT) applies, typically 1-2% of the assessed property value. |

| Income Tax | Rental income is taxed at 20-45%. Mortgage interest relief is capped at a 20% tax credit. | Zero income tax on rental earnings in Dubai, offering a significant boost to net yields. | Progressive income tax on rental income. Non-resident foreigners are taxed at a flat rate of 25%. |

| Regulation | Strongly pro-tenant. Features lengthy eviction processes and increasing compliance demands (EPC ratings, safety checks). | Pro-landlord framework. Clear, efficient eviction processes managed through the RDC (Rental Disputes Centre). | Balanced but can be slow. The legal system can make eviction processes for non-payment time-consuming. |

| Economic Drivers | Stable but slow-growth economy. High interest rates have compressed yields and affordability. | Strong economic growth fuelled by tourism, trade, and foreign investment. High demand from expats. | Rapidly growing economy driven by remittances, BPO industry, and a young, urbanising population. |

This comparison shows there is no single "best" environment. The UK offers stability but higher taxes and tenant-friendly laws, whereas markets like the UAE provide a tax-efficient, pro-landlord climate. The Philippines offers high growth potential but with its own set of regulatory and tax considerations. Your choice depends entirely on your risk appetite and investment goals.

Regulatory Environments

The legal framework governing landlord-tenant relationships is another crucial piece of the puzzle. Some countries have strongly pro-landlord laws, allowing for swift evictions and flexible rent increases. Others have pro-tenant regulations that can include strict rent controls, lengthy eviction processes, and mandatory rental contracts that favour the tenant.

A pro-tenant environment can significantly limit your ability to increase rents in line with market rates, capping your income potential. It can also increase risk, as dealing with problematic tenants may become a costly and time-consuming legal battle. Conversely, a stable and fair regulatory system provides security for both parties and is a hallmark of a mature investment market.

Local Supply and Demand Dynamics

Finally, at the most fundamental level, rental yields are driven by the simple economic principle of supply and demand. A chronic housing shortage coupled with strong population growth or urbanisation will inevitably push rents higher.

Investors should analyse demographic trends, new housing construction rates, and migration patterns. A city with a growing university population or one attracting a major new industry will likely see sustained rental demand. Conversely, a region with a declining population and an oversupply of new-build properties is a major red flag for future rental income and yield stability. This is why a national average yield figure should always be the start of your research, not the end.

Building A Diversified Global Property Investment Strategy

Bringing country-by-country rental yield data together into a coherent plan is where the real work begins. It is about aligning a market's character with your own financial goals and risk tolerance.

A successful global portfolio is rarely built by chasing the highest numbers. Instead, it is a careful balancing act between generating reliable income and securing capital for the long term. The right strategy depends entirely on what kind of investor you are.

The Conservative Income-Focused Strategy

If your priority is stable, predictable income and capital protection, a core-satellite approach is effective. This means you allocate the bulk of your capital (70-80%) to a stable, established market like the UK or Germany. While the yields may be lower, you gain the security of a robust legal system and a predictable economy.

The remaining portion (20-30%) is then used for a tactical investment in a carefully chosen higher-yielding emerging market. This blend provides a reliable income stream from your core holding while offering controlled exposure to the higher growth potential of a developing economy.

For conservative investors, the core message is diversification. A prime property in a stable market acts as a defensive foundation, while a smaller, high-yield asset can give your portfolio’s overall cash flow a significant boost without exposing you to unnecessary risk.

The Growth-Oriented High-Yield Strategy

For investors with a greater risk appetite and a focus on maximising cash flow, it makes sense to lean more heavily into emerging markets. This strategy involves concentrating investments in countries offering yields of 7% or more, but it demands a much deeper level of due diligence.

Success here hinges on meticulous local market research and proactive risk management. Key considerations are:

- Currency Hedging: You need a plan to protect your rental income and capital from sharp movements in exchange rates. This is crucial.

- On-the-Ground Partners: Working with reputable local property managers and legal advisors is non-negotiable. They are your eyes and ears, helping you navigate complex local regulations.

- Exit Strategy: Given the potential for market volatility, you must have a clear plan for how and when you will eventually sell the property.

It is worth remembering that even the most stable markets experience fluctuations. For instance, data from credible sources like Trading Economics shows that while long-term rent inflation in the United Kingdom has been moderate, recent years have seen significant jumps, highlighting that even mature markets require constant monitoring. You can dig into the latest UK's rent inflation trends on Trading Economics.

Ultimately, rental yield is an excellent starting point, but it must be viewed within the broader context of political stability, economic fundamentals, and capital growth potential. Mastering the art of investing in overseas property means using yield as a guide, not a guarantee, to build a resilient and profitable global portfolio.

Frequently Asked Questions About Global Rental Yields

Investors navigating international property markets often encounter the same practical questions. Here are clear, straightforward answers to help you understand the realities of calculating returns, managing risk, and interpreting data on rental yields around the world.

What Is Considered a Good Rental Yield?

A "good" rental yield depends entirely on the market context. In a stable, low-risk country like the UK or Germany, a net yield of 3-5% is often considered solid, particularly when factoring in the potential for steady capital growth.

In emerging markets, however, investors expect higher returns to compensate for the additional risk. For these locations, a net yield above 7% is a more common target, as it helps to offset potential challenges like currency volatility or political uncertainty.

How Do I Account for Currency Risk?

Currency risk is a major factor when investing abroad and can significantly impact your returns. A sudden depreciation in the local currency’s value can erode your rental income when converted back to your home currency.

Experienced investors manage this in several ways:

- Maintaining rental income in a local bank account to cover local expenses.

- Using financial instruments like forward contracts to lock in a favourable exchange rate for future transfers.

- Diversifying across several countries to avoid over-exposure to a single currency.

Can I Deduct Expenses on a Foreign Property?

Tax laws vary hugely from one country to another, but most jurisdictions allow landlords to deduct operational costs from rental income before tax is calculated. This typically includes mortgage interest, property management fees, maintenance bills, and insurance.

It is essential to seek advice from a tax specialist who understands the regulations in both your home country and your target investment market to ensure compliance and optimise your tax position.

At World Property Investor, we provide the in-depth analysis and data you need to compare international markets and make informed decisions. Explore our comprehensive country guides to build your global property portfolio with confidence at https://www.worldpropertyinvestor.com.