You’re probably looking at the Philippines for one of two reasons. Either mature markets now feel too expensive for the yield on offer, or you want exposure to a faster-moving part of Asia without stepping blindly into a speculative story.

That instinct is reasonable. Philippine property sales attract attention because the market sits at an awkward but potentially rewarding intersection of urban growth, domestic demand, overseas money, and aggressive developer marketing. It can work well for investors who stay disciplined. It can disappoint those who buy on brochure logic.

The first mistake I see is treating the Philippines as a simple “high-growth emerging market” play. It isn’t simple. Location quality varies sharply. Legal ownership rights for foreigners are narrow. Rental demand can be genuine in one district and largely theoretical in the next. A tower can look sold out on paper and still feel half-empty in practice.

The second mistake is assuming Metro Manila is the whole market. It isn’t. Recent coverage has started to highlight stronger affordable housing momentum in provincial cities while parts of Manila struggle with weaker demand and oversupply in some segments.

An Introduction for the Global Investor

For an international buyer, philippine property sales are best approached as a selective market, not a blanket country bet. The upside comes from urban expansion, the depth of local housing need, and the way different city economies are maturing at different speeds. The downside comes from weak asset selection, poor legal structuring, and buying into developer narratives that don’t hold up once you test them against occupancy, resale depth, and tenant demand.

If you’re new to international acquisitions, it helps to start with a broader framework for how to buy property abroad before drilling into Philippine-specific rules. The Philippines rewards investors who compare legal rights, cash flow assumptions, management practicalities, and exit options before they compare glossy amenities.

Three forces usually draw investors in:

- Urban demand: Major business districts continue to anchor white-collar housing demand, especially around offices, transport links, schools, and hospitals.

- Diaspora capital: Overseas Filipino buyers influence purchasing patterns, particularly in pre-sale and investor-led condominium stock.

- Market spread: The country doesn’t behave like a single-city market. Manila, Cebu, Davao, Clark, Iloilo, and Cagayan de Oro can offer very different risk and income profiles.

Practical rule: In the Philippines, don’t ask first whether a unit is “selling”. Ask whether people actually want to live there, rent there, and buy it from you later.

That distinction matters more here than in many mature markets. In London, Manchester, or Singapore, transaction evidence and occupancy patterns are usually easier to test. In the Philippines, due diligence often requires more legwork and more scepticism.

A Kenyan Research market note places the Philippine luxury real estate and villas market at USD 5 Bn, driven by high-net-worth individuals, investors, and infrastructure, but that same source doesn’t provide the kind of local submarket precision most overseas buyers need for practical deal analysis in everyday residential investing (Ken Research on the Philippines luxury real estate and villas market). That gap is exactly why investors need a more grounded approach.

Philippine Property Market Fundamentals 2026

A foreign buyer reviews a glossy sales pack for a new Manila tower. The reservation numbers look strong, the branding is polished, and the location sounds familiar. Six months later, the harder questions start. How many units are occupied? Who is the tenant base? How many similar units will hit the rental market at the same time?

That is the right frame for reading philippine property sales in 2026. The market is segmented, uneven, and often misread by overseas buyers who confuse launch momentum with durable demand.

Why headline demand can give a false signal

National growth stories are easy to sell. They are much less useful when you are assessing one building on one street. In the Philippines, the main practical risk is the gap between units reported as sold and units that are genuinely lived in or rented out. That gap helps create what investors informally call ghost condos. Buildings with high take-up at launch but weak day-to-day occupancy, limited rental depth, and thin resale demand.

For investors, that changes the checklist. The core question is not whether a project sold well in pre-sale. It is whether the surrounding area can support real household formation, repeat leasing activity, and a future resale market that is not dependent on the next marketing cycle.

A workable submarket usually needs four things in place at the same time:

- Real occupier demand

- Controlled competing supply

- Practical access to jobs, schools, transport, and services

- A resale buyer pool beyond fellow speculators

If one of those is weak, the downside shows up later in vacancy, rent discounts, or poor exit liquidity.

Metro Manila attention versus provincial traction

Metro Manila still draws the bulk of international attention because it contains the best-known CBDs, the largest concentration of launches, and the most recognisable developer brands. It also carries the greatest risk of buying into a story that has already been heavily marketed and fully priced.

That is why provincial cities deserve more respect than they usually get. In practice, many overseas buyers search where branding is strongest, while local end-user demand may be firmer in secondary cities with lower entry prices and less speculative inventory. The better opportunity is not always the better-known skyline.

This matters most in the middle of the market. Affordable and mid-market housing tied to local employment tends to produce steadier occupancy than investor-heavy condo towers aimed at absentee owners. A family renting near a hospital, university, logistics hub, or BPO cluster is usually a more reliable signal than a showroom full of reservation forms.

In the Philippines, a boring building with stable occupancy often outperforms a fashionable tower with weak end-user demand.

That does not make Metro Manila unattractive. It means buyers need stricter filters there. District, product type, competing pipeline, building management, and tenant profile all need close examination before price is even discussed.

What supports demand on the ground

Demand is strongest where employment is broad-based and recurring. Business process outsourcing, healthcare, education, logistics, tourism, and local services all matter because they create tenants who need to live near work or study, not just investors who want to hold paper gains.

Infrastructure also matters, but only when it shortens real travel times or improves access to established employment nodes. Announced projects are less useful than completed roads, functioning rail links, and operational airports. I would rather buy in a secondary city with proven local economic activity than in a Manila micro-location that depends on a future promise.

Technology adoption is part of that operating backdrop. Investors who want context on the country’s digital business environment can review REDCHIP's insights on local tech. It helps explain how businesses, tenants, and service providers increasingly expect reliable connectivity and modern operating standards.

For broader context, it also helps to compare the Philippines against the wider regional cycle through this property market forecast for 2025. That comparison is useful because Philippine pricing, yields, and absorption should be judged against alternatives, not in isolation.

The practical reading for 2026

Treat the country as a set of local markets, not one national trade.

Established Manila districts can still suit investors who prioritise recognisable locations and a larger resale audience, but only if occupancy, rentability, and supply pressure check out. Provincial cities can offer a better balance of entry price and genuine end-user demand, especially where growth is being driven by jobs and migration rather than marketing. In 2026, that distinction matters more than headline sales volume.

Understanding Foreign Ownership and Property Types

The legal starting point is simple. Foreigners generally can’t own land in the Philippines. That single rule shapes almost every sensible investment decision.

What a foreign buyer can usually own

For most overseas investors, the most straightforward route is a condominium unit in a properly constituted condominium project. That structure gives you ownership of the unit itself, while the land and common areas sit within the condominium regime.

In plain terms, this is why most foreign investment in philippine property sales concentrates in apartments and condo towers rather than landed houses.

The practical appeal is obvious:

- Clearer legal pathway: Condominiums are the standard route for non-Filipino buyers.

- Easier management: Security, building operations, and maintenance are handled centrally.

- Better fit for remote ownership: This matters if you live abroad and need professional management.

There is, however, an important limit. The foreign share of a condominium project is capped. Investors should verify current compliance directly with the developer, counsel, and title records before committing. Don’t rely on a sales agent’s verbal assurance.

What foreigners usually can’t own directly

A house and lot may look attractive, especially to buyers comparing the Philippines with markets where freehold land is standard. But that comparison breaks down quickly.

If the investment case depends on direct land ownership by a foreign individual, you’re already outside the cleanest legal route.

That’s why understanding the distinction in freehold versus leasehold ownership structures is so useful before reviewing Philippine deals. The local legal framework makes that distinction more than a technicality. It determines what you can securely control.

Other structures exist, but risk rises fast

Some investors explore alternatives such as long leases, corporate structures, or family arrangements involving Filipino nationals. These routes exist in practice, but they are not equivalent to simple, direct ownership.

Here’s the honest view:

- Long-term lease arrangements can make sense for use value, especially for business or lifestyle purposes, but they don’t give the same ownership profile as a condominium title.

- Domestic company structures may be discussed in more advanced planning, yet they introduce governance, control, compliance, and beneficial ownership risks.

- Nominee-style informal arrangements should be treated with extreme caution. If your security depends on side agreements and personal trust, the legal risk is already too high.

Buy only what you can defend legally, document clearly, and exit cleanly.

Property types that fit foreign investors best

A practical shortlist usually looks like this:

| Property type | Foreign buyer suitability | Main use case |

|---|---|---|

| Condominium unit | Strongest fit | Buy-to-let, second home, urban base |

| Serviced apartment style unit | Selective fit | Short stays, flexible letting where allowed |

| House and lot | Weak fit for direct ownership | Usually unsuitable without complex structuring |

| Land parcel | Very weak fit | Not a standard route for foreign individuals |

| Long lease interest | Case by case | Lifestyle use or strategic occupation |

Most international investors don’t need legal creativity. They need legal certainty. In the Philippines, that usually means sticking to well-documented condominium assets in locations with proven occupier demand.

Navigating the Purchase Process Step by Step

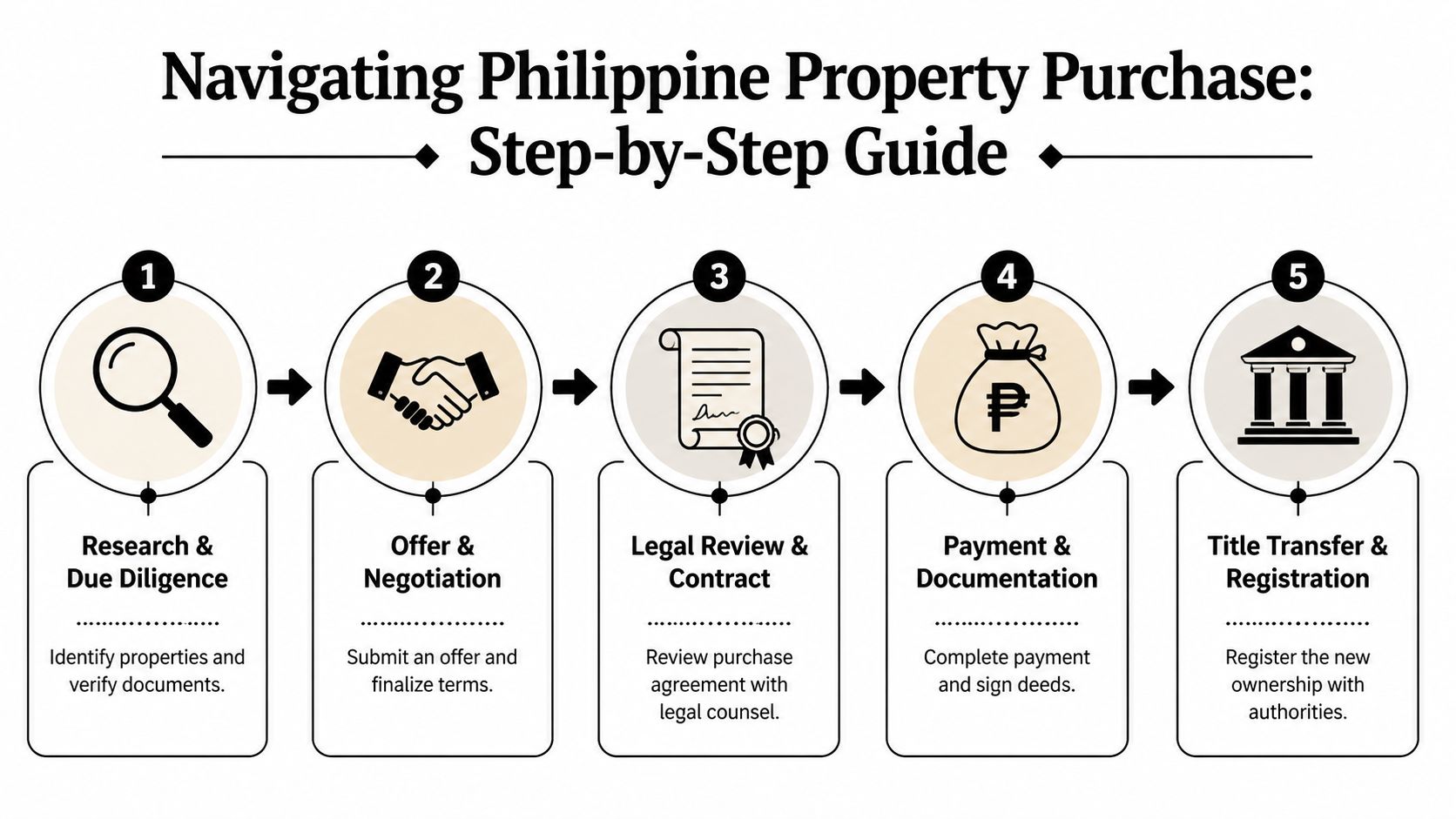

Buying in the Philippines isn’t difficult in theory. It becomes difficult when buyers skip document checks, rely on agent assurances, or assume the process works like it does at home.

Start with the asset, not the brochure

The first task is to identify a property that works on fundamentals. That means transport links, tenant profile, competing supply, building upkeep, and legal eligibility for a foreign buyer.

A reservation fee or expression of interest often comes early in the process. Treat that step carefully. Before money goes in, you need to know what document trail you’ll receive and whether the reservation remains refundable under defined conditions.

Due diligence is where good deals survive

This is the stage that separates investors from speculators. You need independent legal review, not just a developer sales pack.

Check, at minimum:

- Title status: For a condo, verify the Condominium Certificate of Title where applicable, or the project’s title status if an individual title hasn’t yet been issued.

- Seller authority: Confirm that the seller has the legal right to sell, especially in resale transactions.

- Project compliance: Ask whether foreign allocation remains available and documented.

- Building issues: Review house rules, management quality, dues, and any known defects or disputes.

Due diligence test: If you can’t explain exactly what you’re buying, who owns it, and how title transfers, you’re not ready to sign.

Offer, reservation, and contract review

After identifying a suitable unit, the commercial terms are usually agreed before the full closing set. This can include price, payment schedule, included fixtures, turnover condition, and allocation of certain transaction costs.

At this point, have a lawyer review every document, particularly:

- Reservation agreement

- Contract to Sell

- Deed of Absolute Sale

- Developer disclosures and building rules

Many disputes begin because buyers sign a reservation document casually, then discover later that key points were never properly negotiated.

Payment mechanics matter

For overseas buyers, payment logistics need to be clean and traceable. Use formal banking channels. Keep records of every transfer, acknowledgement, invoice, and receipt.

If you’re buying pre-completion or directly from a developer, payment may be staged. If you’re buying resale, payment timing usually needs tighter coordination with document execution and handover.

Watch for these practical issues:

- Currency exposure: Exchange movements can alter your real acquisition cost.

- Delayed handover risk: Especially relevant in developer purchases.

- Mismatch between marketing and contract wording: The contract governs, not the showroom discussion.

Signing and notarisation

Once conditions are satisfied and funds are ready, the transaction proceeds to signing. The Deed of Absolute Sale is the core transfer document in a completed sale. It must be properly executed and notarised.

Notarisation isn’t a formality. It affects enforceability and triggers the next administrative steps, including tax and registration processes.

Transfer and registration

Ownership isn’t secure just because money has changed hands. The transfer process has to be completed through the relevant authorities and records updated accordingly.

The usual end-stage checklist includes:

- Taxes and transfer fees settled

- Registration documents filed

- Title transferred or updated

- Tax declaration aligned with the new owner

- Building management notified

- Utility and association records updated

A foreign buyer should insist on a closing checklist with named responsibility for each item. In some deals, the seller handles parts of this. In others, the developer or counsel coordinates the sequence. Either way, responsibility should never be vague.

The safest operating habit

Use your own lawyer, your own accountant if needed, and your own valuation logic. Agent relationships can be helpful, but they shouldn’t be your control system.

In philippine property sales, the process is manageable. What isn’t manageable is trying to fix a weak legal file after completion.

Decoding Taxes and Transaction Costs

The purchase price is only your starting number. Your real acquisition cost is the full stack of taxes, fees, registration charges, legal costs, and any negotiated extras written into the contract.

The budget line items investors usually face

Some costs are commonly associated with the seller, others with the buyer, but local practice can vary by negotiation and deal structure. That’s why every offer should state cost allocation clearly.

The broad categories usually include:

- Capital Gains Tax

- Documentary Stamp Tax

- Transfer Tax

- Registration fees

- Notarial fees

- Legal fees

- Brokerage or agency fees where relevant

A useful comparative reference for international investors is this guide to capital gains tax on foreign property, especially if you’re assessing how Philippine transaction costs fit into a wider cross-border tax picture.

Estimated Property Transaction Costs in the Philippines

| Cost Item | Typical Rate | Paid By |

|---|---|---|

| Capital Gains Tax | Often seller-side under standard practice, subject to contract | Usually seller |

| Documentary Stamp Tax | Commonly allocated to buyer, subject to negotiation | Usually buyer |

| Transfer Tax | Usually buyer-side, subject to local rules and contract | Usually buyer |

| Registration Fee | Payable on title registration | Usually buyer |

| Notarial Fee | Varies by arrangement | Often shared or negotiated |

| Legal Fee | Depends on lawyer and scope | Each party usually covers own counsel |

| Broker Commission | If a broker is engaged | Usually seller |

What matters more than the exact label

For budgeting, I focus on three questions.

First, which charges are fixed by law or routine practice, and which are negotiable? Second, when are they payable? Third, who is responsible if the contract is silent?

Those points are often more important than memorising each fee name, because a buyer’s surprise costs usually come from assumptions, not from the tax code itself.

Don’t accept “standard allocation” as an answer. Ask for the exact cost schedule in writing before you proceed.

How to underwrite this properly

Build your model using the full cash outlay, not just the sticker price. Include legal review, bank charges, furnishing, vacancy allowance, building dues, and set-up costs for leasing.

If you skip that discipline, your projected yield will be inflated from day one. In a market where tenant demand can vary sharply by building and district, that’s a mistake you can’t afford.

Analysing Returns Rental Yields and Financing Options

A Philippine deal only makes sense when the numbers work after friction. Gross yield can look attractive in a sales deck. Net income is what you keep after reality arrives.

Start with net yield, not gross yield

The basic structure is simple.

- Gross yield is annual rent divided by total purchase cost.

- Net yield is annual rent minus operating costs, then divided by total purchase cost.

That second number is the one worth using. In philippine property sales, operating friction can be material. Management quality, void periods, fit-out spend, and building charges all affect returns.

A practical workflow is to run the numbers through a rental yield calculator for property investors and then stress-test your assumptions. The stress test matters as much as the headline result.

Three property profiles and how they differ

Consider three common formats without forcing false precision.

Small studio in a Manila CBD

This is the classic foreign investor entry point. The attraction is liquidity, recognisable location branding, and easier remote letting.

The trade-off is equally clear. You may face heavy competition from near-identical units in the same building or nearby towers. If many owners bought speculatively, rents can soften quickly when several units hit the market together.

Family unit near schools or hospitals

This segment often gets less attention, yet it can produce steadier demand. Families and longer-stay tenants usually care more about layout, commute, and liveability than rooftop pools or lobby design.

That can support lower churn. The downside is a narrower resale audience if the unit is large, expensive, or in a building with rising maintenance issues.

Holiday-let style property in Cebu

This works only if local rules, building policies, and management execution align. A strong tourist city doesn’t automatically create a strong holiday-let investment.

Short-stay income can be volatile. You need operational control, good reviews, reliable cleaning, local compliance, and a realistic occupancy assumption. Without those, the gross income story falls apart.

The costs investors understate

Many first-time overseas buyers focus on mortgage-free income and ignore operating drag. That’s where returns usually disappoint.

Common deductions include:

- Association dues or building charges

- Agent or property management fees

- Repairs and replacement of furnishings

- Vacancy periods

- Utilities or service costs in some letting formats

- Tax compliance and accountancy support

- Marketing and tenant turnover costs

A unit can be profitable on paper and mediocre in practice if management is weak or turnover is constant.

A useful visual explainer on investor thinking is below.

Financing options for foreign buyers

Financing is where many overseas investors need a reality check. Local borrowing can be harder for foreigners than sales agents imply. Approval standards, documentation demands, and product availability often make debt less straightforward than in the UK, Australia, or parts of Europe.

In practice, most foreign buyers consider one of these routes:

| Financing route | Strength | Weakness |

|---|---|---|

| Cash purchase | Cleanest execution | Highest capital tied up |

| Developer financing | Useful for staged purchases | Terms may be less competitive |

| Home-country borrowing | Familiar banking relationship | FX and cross-border complexity |

| Local bank finance | Potential leverage | Often harder for non-residents |

What works and what doesn’t

What works is buying where tenant demand has a clear source, underwriting conservative occupancy, and budgeting for real operating costs.

What doesn’t work is assuming a premium tower automatically produces premium income. It often produces premium competition instead.

Investment Hotspots and Strategic Risks

A foreign buyer lands in Manila, tours three glossy show flats in a day, hears that units are “nearly sold out”, and leaves thinking demand is settled. That is often the wrong conclusion.

For investment purposes, the better question is simpler. Where is there durable occupier demand at a sensible entry price, and where is “sales” activity masking weak real use?

Metro Manila still matters, but selectivity is brutal

Metro Manila remains the country’s reference market for foreign capital. Makati, Bonifacio Global City, Ortigas, and a few adjacent districts still offer the strongest concentration of office demand, international schools, healthcare access, and recognisable residential stock.

That does not make them easy buys.

The practical problem is saturation in the exact segments overseas buyers are pushed towards. Small investor-grade condos in premium towers face heavy competition on both rent and resale. If ten landlords in the same building are chasing the same tenant profile, headline location quality stops protecting your returns.

I would only consider Manila stock where demand is visible before purchase, not assumed after turnover. Commuting professionals, medical staff, family renters near schools, and residents tied to long-established business districts usually give a better income base than a generic promise of capital growth.

Provincial cities deserve closer scrutiny

Many international guides remain superficial in their analysis. They mention Cebu or Clark as side notes, then return to Metro Manila. That misses a real shift in buyer logic.

As noted earlier, recent reporting has pointed to stronger housing momentum in several provincial markets while parts of Metro Manila have faced softer demand. For foreign investors, that does not mean “buy anything outside Manila”. It means some provincial cities now deserve the same level of analysis that Manila has received for years.

Three markets stand out for different reasons:

- Cebu: The broadest business and tourism profile outside the capital, with stronger name recognition among overseas buyers.

- Davao: Lower entry points in many submarkets and a more local-user-driven demand story.

- Clark: A clearer infrastructure and business expansion thesis than many speculative condo locations in Manila.

The trade-off is straightforward. Provincial cities can offer cleaner occupier demand and less overheated pricing, but they often come with thinner resale liquidity, fewer direct comparables, and weaker property management depth. An investor buying there needs more local verification, not less.

The ghost condo problem

This is the filter too many investors skip.

A building can be largely sold and still feel half-empty at night. Commentary in a recent discussion on speculative buying and under-occupied towers points to the gap between developer sell-through and actual lived-in use (discussion on ghost condos and speculative buying). That gap matters far more than brochure demand.

If a project is heavily owned by investors, especially buyers who do not intend to live there, “sold” can mean that inventory has been transferred off the developer’s books. It does not confirm a stable tenant base, a healthy building community, or resilient resale demand.

That changes the investment case in four ways:

- Rental risk: Empty investor units can hit the leasing market at the same time and pressure rents.

- Exit risk: Your likely buyer may be another yield-chasing investor rather than an owner-occupier.

- Building quality in practice: Low occupancy can weaken day-to-day atmosphere, amenity use, and long-term reputation.

- Pricing interpretation: Strong sell-through can overstate true end-user demand.

Market warning: High sales velocity without real occupancy is a warning sign for a landlord, not a comfort.

Overseas investors, especially those used to reading pre-sales as a positive signal, must apply a stricter test. In the Philippines, developer sell-through and tenant absorption are separate measures.

Risk filter for any target location

Before committing capital, I would pressure-test any building and any city against the same basic questions:

| Risk area | What to check |

|---|---|

| Occupancy reality | Are units visibly occupied, or are large sections dark at night? |

| Developer quality | Has the builder delivered on time and maintained older projects properly? |

| Tenant depth | Who actually rents here, and what anchors that demand? |

| Supply pressure | How many near-identical units are competing within the same catchment? |

| Exit liquidity | Will your future buyer be an end-user, a landlord, or only a speculator? |

| Currency exposure | Could exchange-rate movement erode returns at purchase, during ownership, or on exit? |

What usually works best

The better-performing strategy is often less glamorous than the marketing pitch.

A legally clean condo in a district with visible everyday demand will often outperform a fashionable tower bought on launch momentum and resale hope. Manila can still work well, but mistakes are expensive and competition is intense. Provincial cities can offer stronger relative value, but only if the local demand base is real and the building is managed properly.

The Philippines offers genuine opportunity. It also has a habit of dressing speculation up as demand. Serious investors need to separate the two.

If you want country-by-country guidance, practical buying frameworks, and clear comparisons across global markets, World Property Investor is a strong place to continue your research before making a cross-border property decision.